There was a preferential issue in September 2024 with approx 20% dilution in which promoters also invested. Subsequently in December 2024 promotors sold out 15% stake to provide entry to Larsen & Toubro.

I am not able to do any decent technical analysis myself, so in fact did not catch the bottom there.

I don’t have any technical entry, I don’t have knowledge of technical analysis. I like to think that I am a pure value investor.

Selection criteria are

5 Likes

Hi Vikas, it’s fascinating to read this as being a full time investor is kind of dream for me. How long you have been the full time investor? How has been the journey so far? You live in metro /non metro town? How do you plan for your expenses, emergency needs?

1 Like

Hi @vikas_sinha

I wanted to understand your views and thought process on Freshara Agro in light of the recent Spain acquisition.

During the last concall, the promoter spoke at length about the acquisition, but did not explicitly mention that the Spanish entity being acquired was promoter-owned. Also, when asked about the reason for the Spanish company’s bankruptcy, the explanation given was that it was a family-owned business where internal differences led to a breakdown in operations. That explanation felt somewhat brief and did not clearly address the underlying business or financial factors.

For better transparency, it might have helped if the related-party nature of the transaction had been highlighted upfront during the concall (though to be fair, it has been clearly disclosed in the subsequent SEBI filing).

The promoter commentary around strategy, scale, and growth certainly sounds very promising. How do you view this gap in communication? Do you see this as a minor issue that can be overlooked, or something that deserves closer tracking from a governance perspective?

Looking forward to hear back from you.

3 Likes

As per my limited understanding, the target Spanish company is itself not related to promotors but only the acquisition method is by using another company, calling it a special purpose vehicle SPV. The SPV in one case is promotor owned, there are two SPVs, another one is for the real estate, this is not promotor owned.

As overall understanding of international bankruptcy deals is quite limited, I can’t comment much, but it doesn’t look like wrong intent. A more direct acquisition would have perhaps made disclosure of target company financials, as you have missed so far in the company discussion.

The LinkedIn profile for target company mentions Rs 295 cr turnover in 2024, didn’t find the losses reported anywhere.

https://www.linkedin.com/company/aceitunas-sarasa-sa/about/

Freshara pays 7.7 million euros, about a quarter of the turnover amount, seems decent.

2 Likes

So I tried riding the compounding trend, quite optimistically, but failed badly in September 2017, as also described at the beginning of the thread. Then I was living with the joint family in ancestral hometown, a non metro.

Success was only achieved in January 2021, so it’s been 5 years now, living all the while in metro.

Journey has been very good, except the bad start, in the pre 2020 phase. After that dramatic recovery from the 2020 lows have given overall 10x returns on investment, till the peak about a year ago, but 10% drawdown since then as of now, which mainly occurred last month.

I just sell only to meet expense, keeping about 1-2% of the total as cash.

11 Likes

Thats look great Vikas, in this kind of market sustaining at 10% loss is remarkable. From July till now its a rollar coaster ride. Since Covid, gains were close to 50X, peak registered in Jan 25, which is close to 33 times of my annual expenses. I have habit of withdrawing capital whenever markets become euphoric, last year took out 5-6% of PF and invested in a property in hills which has gone 100% now. AB Capital and force performed very good but lost 7-8 % of PF in ABFRL demerger due to huge size of bet, overall at 10% of portfolio loss from Jan peak, planning to liquidate one of investment property to generate cash. First time this month had to sell stocks to generate college fee for my son. Last three months are ruthless. Even swing trades are not working, very narrow market, hoping to see tide turn in 2026. Markets took downturn the day i took VRS(2nd Sept 2025)![]()

![]()

8 Likes

Thank you @vikas_sinha. Missed the SPV part. I got confused due to companie’s SEBI filing directly linked to SPV. Thank you very much for the clarification.

1 Like

A solid, easy‑to‑read piece on the European pickle market—and how major exporting countries fit into it—would really help understand the broader macro setup in which Freshara operates.

5 Likes

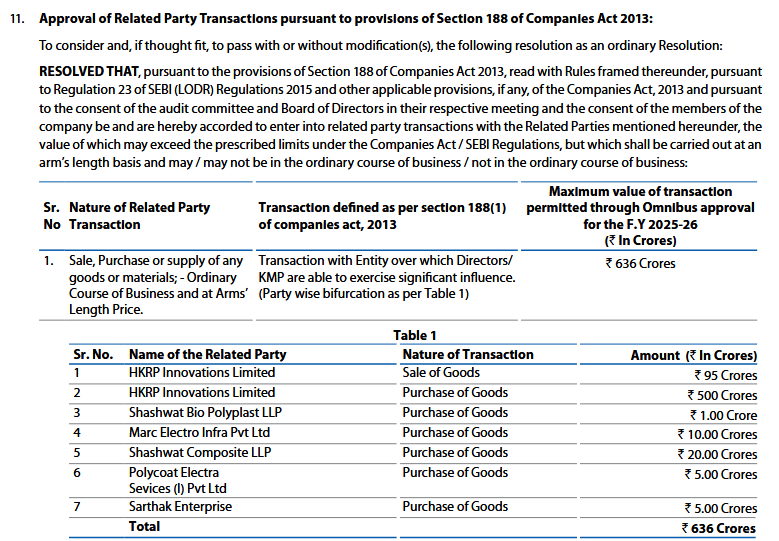

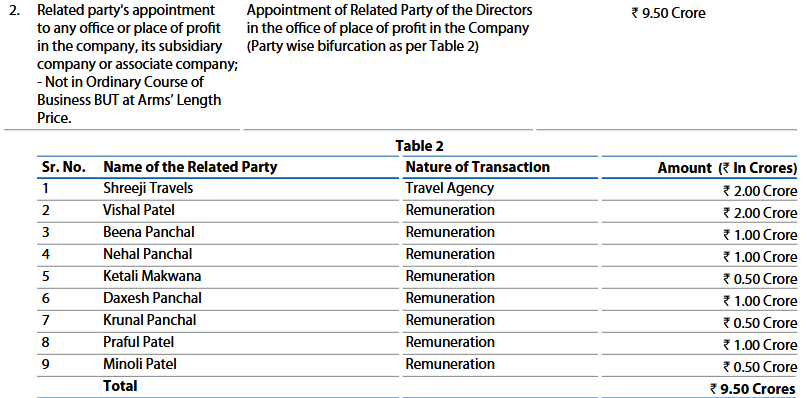

Some CG Issues in Rajesh Power:

-

~120 Cr purchases from associate company HKRP (same promoters) in FY25 (10.8% of FY25 Revenue). Board has pre-approved up to 500 Cr for FY26 (i.e 50% of FY25 revenue). As per annual report, HKRP specializes in IoT and Cloud based solutions for power grids. If HKRP sells these smart devices or software to Rajesh Power at a high profit margin, the money moves from the public company (Rajesh Power) to the private / associate company (HKRP). Since the promoters own a larger percentage of HKRP than they do of Rajesh Power, they benefit more if the profit sits in HKRP rather than Rajesh Power. If Rajesh Power will do 2000 Cr in FY26, spending 25% of that on IoT devices & software for a power EPC company dosn’t seem right to me.

-

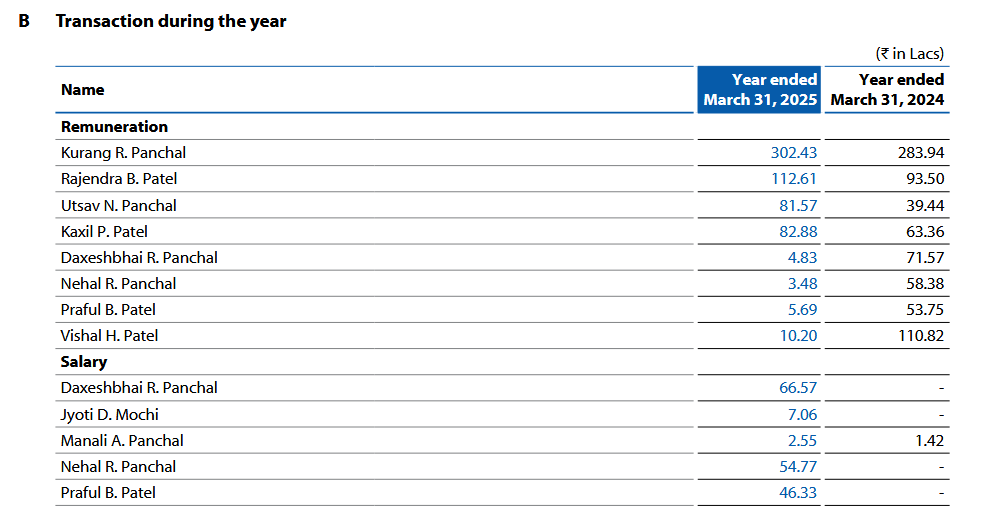

Relatives of promoters draw 1-2 Cr each as salaries. 2 Cr payment to a family linked travel agency (Shreeji Travels). Most of the names below are not part of the core team mentioned here: RPSL LeadershipThe actual payment to Shreeji Travels in FY25 was only 14.68 Lakhs, not 2 Cr. The 2 Cr figure is a budgetary approval limit being sought for the next financial year (FY 26). Similarly, while relatives of promoters drew salaries in FY 2024-25, the amounts were mostly between 50-70 Lakhs, with only one individual drawing approx. 1.05 Cr. The 1-2 Cr figures mentioned are, again, future approval limits for FY 26, not actual payouts.

-

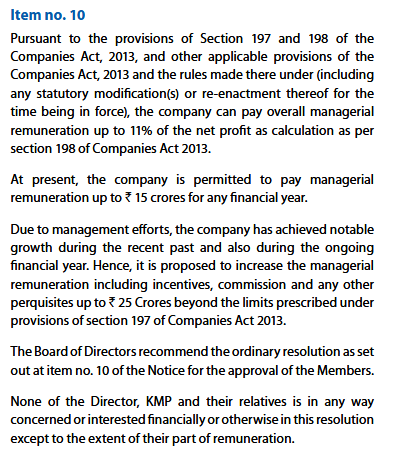

Managerial pay cap raised from 15 Cr to 25 Cr, above the legal limit (11% of net profits).

-

Regular big transactions with promoter linked LLPs / companies.

9 Likes

Thanks for the details!

HKRP setup looked strange to me too, them giving it boasting space on the 2nd last slide of the corporate presentation deck.

-

I would discount the transaction by 25%, the amount of stake held by Rajesh in HKRP. So, FY25 transaction amount is only 8% of revenue. Yes, sanctioned amount is almost doubling in percentage terms for FY26 but let’s see what actually happens since a sanction is set up bigger just for convenience.

-

Will try to go through the annual report, thanks again for double checking about the relatives!

-

Pay cap looks like is just a proportionately done adjustment for the increase from FY25 to FY26.

-

RPTs are indeed a flag, they are often used to make money for promotors rather than the public shareholders. We just need to judge the amount of impact on the company, if within limits.

5 Likes

Sold off 3b blackbio, about 6% of overall folio, and moved it to Sai life sciences and Jeena sikho lifecare.

One was diagnostics, the new one is like blue jet, in the CDMO domain, thanks to @phreakv6 thread on this.

3b blackbio was slowing down, and new triggers will take more than a year, so nothing great happening here.

Jeena sikho is an ayurveda+hospital chain which is growing into a biggie size entity now getting certified by the insurance folks also.

3b blackbio recent quarter profit was inflated by one time sales in Belgian subsidiary, whilst the subsidiary is actually barely breakeven, so possibly later quarters will look worse. EU trade deal may make things better but it means waiting for more than a year.

Disc: unqualified to advise, hence please do your own research.

17 Likes

Bought balu forge, about 3% weight in folio, they got big order for artillery shells from NATO, sold some of Shilchar and Zen tech in that order.

Shilchar is in an industry with a long runway but overcapacity risk is also present.

Zen technologies has been facing issues with orders because as per them they are not providing critical emergency procurements being prioritised currently.

The issue with balu forge is that their growth has been mainly by buying European plants for cheap and shifting them to India. People don’t believe their capital expenses. Recently there was an income tax search also. The shells export order is not yet fully completed but only an agreement. Export of defense goods will require govt approval.

Disc: unqualified to advise, hence please do your own research.

13 Likes

Balu Forge is new entry in my PF as well, NATO order is quiet huge, was surprised with automated shell production unit, margins will be high, annual revenue from NATO order is close to current turnover, if no hidden facts than it should skyrocket soon.

10 Likes

Regarding Zen Technologies, what would be your opinion regarding the danger of drones and the need of the hour for anti drone systems. Recently Iran has terrorised the middle east with drones and most capital is flowing into drones rather than anti drone systems. I feel Zen could benefit though I agree that timing mismatch on order wins are always a threat.

I have a position in Zen and looking to add a bit given the geopolitical situation

Zen technologies has projected itself as the only thoroughly indigenous provider of anti drone systems. But I don’t feel that their sales match with the claims. The most basic technology of jammers is very much likely to be commoditised. Hard kill or laser based interdiction possibly provides a bit of a moat. Noting that this domain is very different from their simulation background and relatively recent. Robotized kinetic kill or lasers or even anti-drone drones can rapidly attract many startups and there are already bigger names like adani in the race too. Another question mark maybe the defense strategic thinking and how much is the establishment serious about countering drones and spending money on the threat, given that there is a multi layered/faceted air defense architecture and only one layer is provided by Zen. So, I will only take their anti drone pitch with a helping of salt.

7 Likes

Dear Vikas,

Balu Forge appears to be in a very sweet spot. However, it could be my lack of knowledge or lack of understanding, but I am finding it little difficult to interpret their recent disclosure.

As per their filing:

“The serial commencement of supplies will be from April 2026 and will be ramped up in a phased manner. The initial supplies will be for 155 mm M107 and 152 mm variants only.

• The above volumes exceed the present capacity of the company but there is already a plan in place to increase the production capacity beyond from the 360,000 per annum from internal accruals.”

If supplies are expected to start from April 2026 and company alread planning for increasing the production capacity beyond from the 360,000 per annum from internal accruals, then can we assume that the purchase order (PO) should have already been received by now or there must be some concete commitment from the party to proceed fruther? However, there has been no communication regarding any confirmed PO.

Alternatively, could this initial supply be meant purely for evaluation purposes? But in that case, the MoU also mentions:

“155 mm M107: 30,000 units per month in ‘Ready to Fill’ condition for a period of 5 years

152 mm: 10,000 units per month in ‘Ready to Fill’ condition for a period of 5 years.”

Given these numbers, it appears more like a production-scale arrangement rather than just evaluation supplies.

I am therefore trying to understand whether the company has already completed the evaluation phase and is now moving towards deliveries, or whether the evaluation process is still ongoing.

Would appreciate your thoughts on this.

1 Like

Indeed, as you observe, the amount of details shared should mean that the evaluation phase is done, this is reasonable to expect. And the order is finalised, or almost. Technically speaking though, only MoU is mentioned, experts say this is legally different from a binding supply order.

2 Likes

Any idea why Ashish kachodia reduced stake in this for Mar 26