Dear Vikas ji,

What’s your opinion on Zen Technologies now after the not so good Q3 results.

Regards

Dear Vikas ji,

What’s your opinion on Zen Technologies now after the not so good Q3 results.

Regards

Check order book : Very dismal — Even margins have come down. Other income has contributed to earnings.

In Anti drone h/w - Zen tech is just assembling. Imports from Taiwan and possibly don’t even own embedded software. Ideally u should prefer an innovator.

Also the R&D team - check LinkedIn profiles around the RD staff - all tier 3 colleges i guess less on experience. Which collaborates the fact that they just assemble and tinker the assembled hardware and software. The CEO is a Bsc grad and great at marketing on TV channels.

I am still holding in profit, lumping of government contracts is a valid concern, nothing extraordinary for the business.

Vikas ji any new picks in the dip or portfolio remains unchanged

Hi Vikas Ji, Any changes on the portfolio.

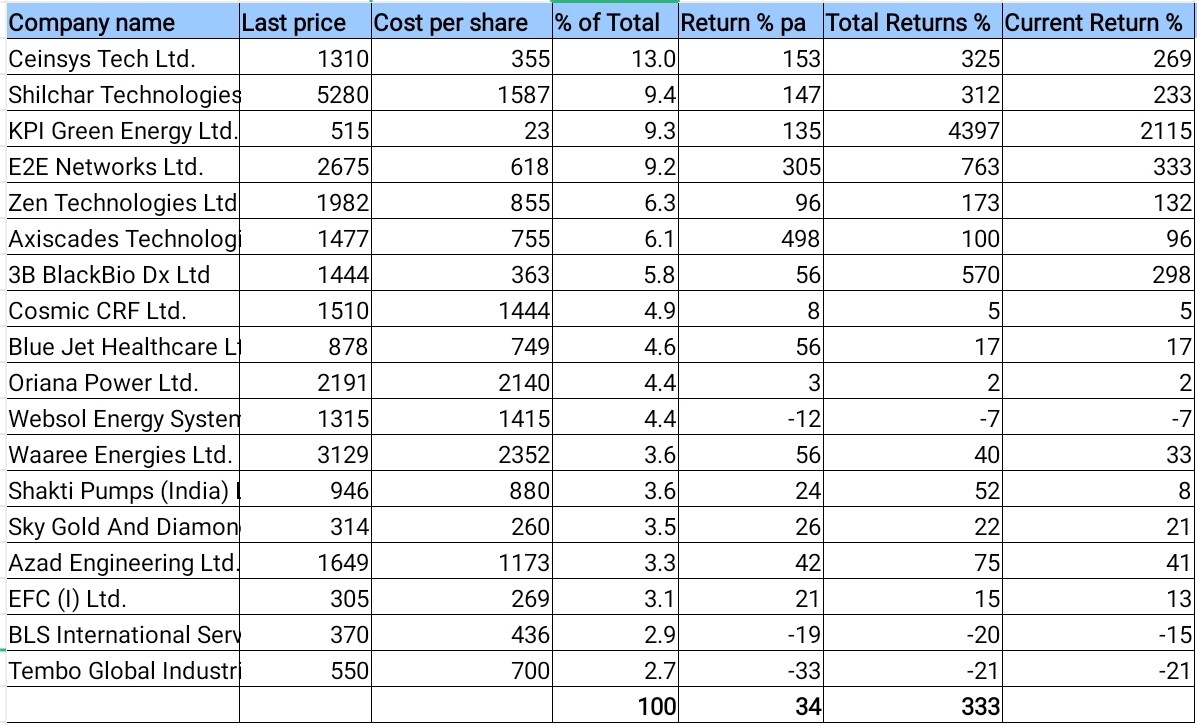

Latest folio status:

CAGR approx 34% since inception, 7 years ago. Currently about 10% below peak. Calculations are considering the withdrawn amount too. 15% up in past year. Total 18 stocks.

Kaynes and Macfos sold out since last update about the liquidation for house buying funds. Added Axiscades, Blue jet tracking @phreakv6 mainly.

About 40% of funds are used in 3 house assets. This has reduced my interest in the markets, which was declining anyway, not that it was much to begin with. Overall market sentiment is also bit boring.

Past 3 years performance curve as per zerodha:

Explanation here:

Absolute value curve for past year.

Portfolio:

Please advise selection criteria of stocks and also at what technical point you try to enter

Exited BLS International and bought Raymond realty, wanted to book losses and find something else cheap to buy, Raymond realty has been demerged recently and facing selling from institutions who have to stick to various rules for their holdings. BLS was the smallest holding, have mistimed it twice now, something looked disturbing about its decline. Realty cycle seems to still have some growth left.

Disc: unqualified to advise, hence please do your own research.

Interesting pick in Realty. But doesn’t the leadership of a documented thief like Gautam Singhania who got the board of Raymond to sell prime mumbai houses at sub par rates worry you. Real estate is a notorious for poor governance and even more poor morals.

Yes, interesting pick is how I would put it! Yes, promotor is a very doubtful character. That is the big risk in this one. Real estate is like you mentioned, consider it part of the game. I mostly don’t like realty, judging also that it’s cycle may have peaked already. Position sizing is such that I don’t think much about it. Technically, price action looks like the bottom, which was the attraction here. Mumbai realty focus is also interesting.

how do you catch the bottom? I am not that sharp in technical analysis

@vikas_sinha are you still holding E2E ?, last quarter results were not good.

Still holding, wait for good results is taking more time than expected by me. This is a very asset heavy business which might be a good reason to not like it. Depreciation is astronomical too, and not just on paper. Still feel that the numbers should improve now, sooner than later, hence the patient approach.

Disc: not qualified to advise, hence please do your own research.

I see that for E2E quarter after quarter promoter holding is reducing which in a year has reduced from 59% to 40%. Is it concerning

Sold off Azad and Cosmic crf, bought in equal amount SJ logistics, Rajesh power and Freshara agro, dealing worth 10% of the folio.

Azad was too high quality and expensive, seems it required lots of waiting. Cosmic growth depends on the takeover deal which likely gets decided tomorrow, too much risk on the one event stuck in nclt appeal

All new ones are SME so risky and cheap in current market. Cosmic was SME also.

Azad is supplier of turbine parts to top manufacturers, unfortunately many deals were confidential, and timeline for the projects quite long because of the complexity such as manufacturing Indian jet engines.

Freshara Agro is pickles exporter, recently in a takeover of Spanish olive and pickles producer, seems well managed to get decent growth.

SJ logistics is shipping provider, again bet is on the promoter, it has recently started leasing own vessels rather than just managing cargo.

Rajesh power is transmission and distribution contractor, overall solar supply needs to increase distribution, it’s mainly working in the solar area of Gujarat, Rajasthan and Madhya Pradesh, similar to Viviana, Kay Cee.

Disc: not qualified to advise, hence please do your own research.

If i had just copied your ideas as and when you post it , i would have done immensely well in the bull market (2021-2024). wishing you better returns with the new bets. I might take a look at SJ logistics though i hold delhivery

what is your Stoploss or Drawdown strategy in the companies you invest? or do you play the momentum?

What is the reason of such low valuations of SJ logistics, in your opinion ?

I too think it’s because of the reasons discussed on the company thread here

Also logistics business has a very low moat typically and exposed to global trade, shipping etc conditions.

I like to think that I am a pure value investor, but it might be the case that momentum attracts me to a situation or stocks. So I don’t keep any stop-loss or drawdown strategy.

The whole point of being a full time investor for me is to avoid getting a job and make minimal efforts. So I am just coasting along without any special efforts or strategy, given enough cushion is available to absorb most of the shocks.