Hi Vikas, I had a question on NSE. I saw that it is quoting at < 25 pe in grey market. I have heard the buzz of its ipo that it will have huge subscription. I am a new investor with almost no knowledge of grey market. Wanted to know your opinion on why nse trades so cheaply. Is it because of the colocation scam ?

No clue about NSE valuation, superficially it’s very cheap compared to BSE. Generally I don’t track well discovered stories, unless there is a dramatic re-rating or turn-around kind of development taking place.

1 Like

Hello @vikas_sinha

Wanted to ask you about Ujjivan Financial. Now that there is more clarity on the reverse merger, and valuation of the bank has improved quite a bit, how do you plan to play this.

Thanks for your time ![]()

Hi @sarthakkumar19_ I am reducing allocation slowly since top is still some time away, may be 2 years approx. It’s about 20% of my folio, and more than 5x for me, all long term so tax efficient to book for occasional liquidity needs. Valuation is quite comfortable due to merger currently.

2 Likes

You make it sound so simple and easy, thats the beauty when one understands himself as investor and to top it, has the required skills as well. Cannot stop admiring everytime I read your posts…

6 Likes

Hi Vikas, any changes/trimming in your portfolio after the recent rally.

Have you added any new stock, Please share your watchlist as well.

2 Likes

Hi @Shakti_Srivastava no change since last status update, tracking satin credit since interested in micro finance nbfc and ujjivan seems to be moving away from the sector.

Update:

25% of folio churned, with 2 full exits and 8 fresh additions.

Trying to change the theme, it’s been good years recently but have to stop pretending to be a serious investor ![]() size now offers comfort to take risk more. Missed so many sectors, pipes, cables, rail, defence, EMS, PSU so on. A more diverse bet would likely pick up some of these early which can be pyramid on up or milked occasionally but position kept (since sell triggers often an up swing

size now offers comfort to take risk more. Missed so many sectors, pipes, cables, rail, defence, EMS, PSU so on. A more diverse bet would likely pick up some of these early which can be pyramid on up or milked occasionally but position kept (since sell triggers often an up swing ![]() ). Maybe results overall wouldn’t be much different, this diversity bug bites me every other year, and then I slowly consolidate the winners.

). Maybe results overall wouldn’t be much different, this diversity bug bites me every other year, and then I slowly consolidate the winners.

Some small caps reach a point of inflexion where even though their exponential profit graph flattens but real long term strength appears. For not so agile investor, it can be a point of entry. Indian manufacturing exports are booming, with true domestic value addition like auto.

Added Sharda motors, it’s supplying mainly emissions control systems with one of largest market share in India and now started exports to US, bit slowly, decent value buy, tie-up with kinetic for some BMS etc.

Added Satin credit since interested in micro finance nbfc and ujjivan seems to be moving away from the sector 🤷🏽♂

Added E2E which is selling cloud infra, GPU focus with growth likely due to AI.

Added Ceinsys which is doing geospatial studies and recently took over auto design company based in US. Maybe just superficially cheap.

Also added Shilchar which is making transformers with exports growing, new capacity under construction, 1 more year wait required with max capacity reached. Transformers shortage globally, scaling production may take 5 years approx.

Added All E tech which is just Microsoft solutions provider but apparently it’s in a sweet spot to grow.

Added Beta drugs oncology drugs maker, with exports to developing countries mainly, doing well in India also, addition of dermatology products recently.

Added Roto pumps which is making non centrifugal pumps, major exports, growing faster due to China+1 and Europe+1 theme. Looks like they are expanding capacity.

Fully exited Redtape and Best Agro.

I don’t understand much about fashion brands ![]()

Reduced Kilpest and Ujjivan financial by half.

Also reduced from Gujarat Themis, Shivalik bimetal, KPI green, RBL, Tinna in that order. Kilpest doesn’t seem to have the strength to grow that fast and my position was about 10% of folio, bit large, with 350 average buy. Gujarat Themis is showing slow progress in capacity addition, one year more for sales to start. Shivalik bimetal capacity rampup will take time depending on global macros, electronics sales, ev growth story, 30% cagr for few years is mostly priced in. Rest booked had grown 3x and needed diversity IMO. Best agro was loss booking for saving taxes. ![]() Also total holdings are 19 now, bit large but then I don’t study that well to make concentrated bets! My effort is to follow GARP strategy

Also total holdings are 19 now, bit large but then I don’t study that well to make concentrated bets! My effort is to follow GARP strategy ![]()

All new positions are roughly equal size, each about 4% of folio

11 Likes

Vikas, Any research around All-E tech? I know this was covered recently in IAS2020 but I didn’t subscribe to it.

I spent some time studying it but at surface I couldn’t find any moat that any run of the mill IT companies doesn’t have. My back of the envelope assessment of IT service companies goes like this. Calculate revenue per employee and see how they fair in comparison.

For All-E tech, 2023 revenue is 88 Cr for 331 employees (as per AR). This comes to 26 lakhs per employee. This is no different than others. In fact it is less than lot many mid size IT companies.

So why?

1 Like

Hi,

I’ve been tracking Shilchar from 1200-1400 levels and has moved all the way upto 2800 levels. Just wanted to understand what is your thought process to add the stock when it’s 6-8x up already this year. Would love to understand your reasoning.

Almost no research, this one kept popping into visibility likely due to their IPO this year and indeed trigger was the coverage in IAS. Yes, I wrote it’s just run of the mill, it does have a sufficiently long track record, so could be growing into a strong stretch going by results. It’s quite small sized, not even close to mid tier, yet. Just figuring in my bottom 3 holdings ranking by size. May get flipped quickly!

2 Likes

Found more growth here and coverage on this forum too, bit cheaper side compared to peers, only interested in the specific sector. The stock can still move perhaps after a quarter or two, 5x this year to be precise. Very nice fixed assets turnover here. Chart looks good for entry. It’s just bottom 4 by holding size ranking in folio, not making big bets in overheated market indeed! Especially with limited research!

4 Likes

Latest folio status:

God has been kind ![]() maintain 30% cagr since inception in October 2017.

maintain 30% cagr since inception in October 2017.

| Company name | Last price | Cost per share | % of Total | Return % pa | Total Return % | Current Return % |

|---|---|---|---|---|---|---|

| KPI Green Energy Ltd. | 1468 | 377 | 12.4 | 151 | 307 | 289 |

| Ujjivan Financial Services Ltd. | 565 | 140 | 9.6 | 135 | 575 | 304 |

| RBL Bank Ltd. | 279 | 110 | 8.6 | 77 | 177 | 154 |

| Ugro Capital Ltd. | 270 | 184 | 7.8 | 25 | 39 | 47 |

| Tinna Rubber And Infrastructure Ltd. | 568 | 166 | 6.7 | 231 | 259 | 242 |

| Arman Financial Services Ltd. | 2438 | 2239 | 5.8 | 28 | 9 | 9 |

| Caplin Point Laboratories Ltd. | 1356 | 807 | 4.7 | 92 | 69 | 68 |

| Phantom Digital Effects Ltd. | 434 | 489 | 4.5 | -35 | -11 | -11 |

| Sharda Motor Industries Ltd. | 1307 | 1233 | 4.2 | 42 | 6 | 6 |

| Satin Creditcare Network Ltd. | 240 | 256 | 4.1 | -95 | -6 | -6 |

| E2E Networks Ltd. | 658 | 614 | 3.9 | – | 7 | 7 |

| Ceinsys Tech Ltd. | 355 | 355 | 3.9 | -3 | 0 | 0 |

| Shilchar Technologies Ltd. | 2535 | 2378 | 3.8 | – | 7 | 7 |

| Beta Drugs Ltd. | 1470 | 1508 | 3.8 | -70 | -3 | -3 |

| Gujarat Themis Biosyn Ltd. | 257 | 123 | 3.6 | 61 | 171 | 109 |

| Kilpest India Ltd. | 790 | 354 | 3.6 | 55 | 284 | 123 |

| Roto Pumps Ltd. | 421 | 410 | 3.4 | 41 | 2 | 3 |

| All E Technologies Ltd. | 238 | 256 | 3.2 | -97 | -7 | -7 |

| Shivalik Bimetal Controls Ltd. | 551 | 152 | 2.7 | 65 | 341 | 262 |

| Total Stocks | 100 | 30.4 | 128 |

Due to tax, mainly from the recent large churn, the folio value will be 1% lower. The tax amount has not been debited from folio yet, historical losses have reduced taxes a little bit.

Currently 1% below ATH. 110% gains since start of the financial year. 3x since starting my financial independence journey in March 2021.

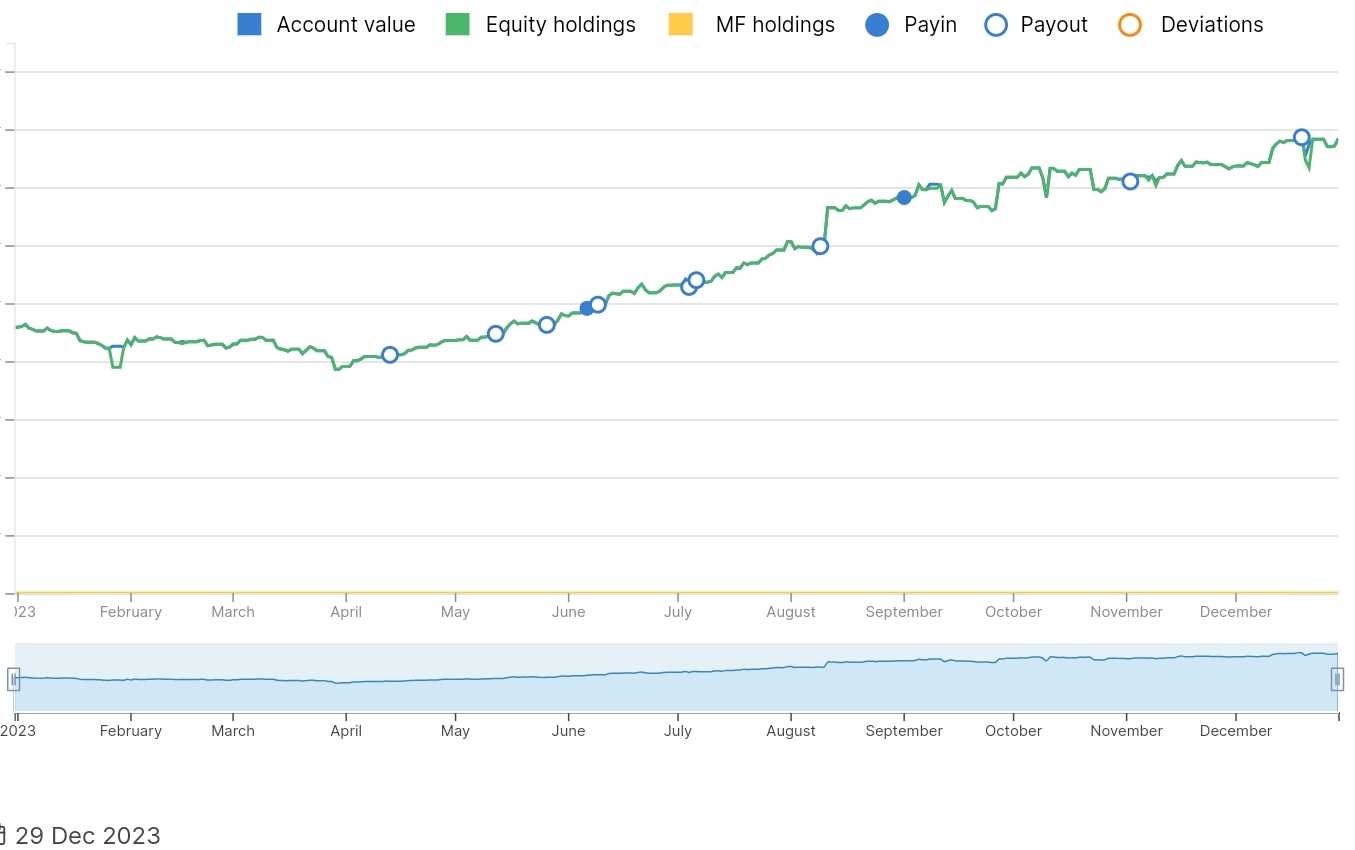

Past year graph: (courtesy zerodha)

Flashback:

One of my first punts was in solar panel, Moser Baer, when my demat was just opened. Rest 2-3 picks were all bluest of blue chips, ICICI Bank, Tata motors etc. Indian subsidy policy was terminated due to trade dispute raised by US, and politics was unfavorable too. Only good study helps in markets. ![]()

Many thanks to value pickr folks! ![]()

28 Likes

Dear Vikas,

This thread is very useful and i have been silent reader.

How do you view collection efficiency of Ugro. Last 2 quarters it is revolving around 91% and deteriorated from 94% levels an year ago

Also like to know your overall views on this counter.

1 Like

Dear James,

Thanks! Ugro performance on recovery front has indeed been concerning. My point is that they are currently focusing first on growth and this shows in the risky book. Positive being that data which doesn’t look good is also disclosed, rather than massaging the numbers. Overall if the NPA numbers are good and steady given their lending profile, till then it’s a case to remain invested. Being in top 4 holding by size, it’s not likely I am going to add to the position though. Or atleast wait for earnings to catch up. This earnings growth rate provides comfort to stick around and keep watch.

3 Likes

Quite a bit of churn in the folio, sold 12% of folio from banks, Ujjivan financial totally sold off and RBL reduced by half, reduced KPI green by 8% of folio, also pruned Beta drugs, Caplin point, Phantom digital, Ugro, Arman, Tinna altogether by 5%.

Put equally in 7 new buys with 3% allocation each Indraprastha medical, Zen tech, Kotyark, Interglobe aviation, Godawari power, HBL power and RBM infra only 1.5%.

Banks will rise slowly, were oversold when bought, still have 4 financial sector stocks. KPI green is running ahead of fundamentals, it’s just a solar EPC mostly in few places in Gujarat.

Indraprastha medical is just a cheap hospital stock, growth has come back inspite of it being an Apollo joint venture with Delhi govt, medical tourism is growing faster. Indraprastha medical has only 2 hospitals, no addition since 2009, Delhi govt may be uninterested in the business, Apollo hospitals too can go it alone. Central govt can obstruct state govt plans. It’s cheap, can be the only positive thing if any growth trigger comes true.

Zen tech is making defence simulators for tanks, rifles, trucks etc. it’s also making anti drone systems now. Looks promising but it’s expensive🤞 simulators can be difficult since end product can face rejection even after long development time, but track record looks good, govt contract payment issues and lumpy nature makes quarterly results highly variable. Anti drone systems can become commodity due to developing competition. I think they have got good connections. Anti drone popularity can grow fast.

Kotyark is SME stock, only listed purely bio-diesel player, they collect used cooking oil and after some processing mix with diesel and supply to oil companies based on tenders. They won lots tenders recently, should be doing 3x business soon. Margins depend on tender competition and government/PSU is the only customer.

Godavari started to rise just when I sold it few months ago, iron ore is still trending strong, while global growth issues can be a problem. They expect clearance from govt to increase production 2.5x by March. Project will still take 1 year to execute. Maybe get 3rd time lucky ![]()

Indigo is survival of fittest, while oil price should remain low, competition is lower as market keeps growing. People are valuing it a bit cheaper due to issues with airlines. Actually margins are better for IndiGo with more efficient use of lower number of aircraft, so capacity issues work both ways.

HBL power, more hi-tech and stable growth expected from railway and defence electronics and batteries, but very expensive ![]() may need to wait few months to see growth.

may need to wait few months to see growth.

RBM infra is maybe fraud kinda but working like subcontractors in jamnagar refinery construction boom, Russian crude oil is processed by reliance and rosneft, and the Indian petrol, diesel sold to Europe.

Ujjivan merger is delayed now till April, bit slow working style. Also 36% allocation was too much in financial sector. Need to reduce further perhaps by 3%, will do that when thinking about next buy decision, or tax amount withdrawal etc.

Total number of Holdings increase from 19 stocks to 25.

4 year anniversary of starting this thread, zerodha has now increased the time duration of folio graph to 4 years. ![]()

140% growth in past year, including withdrawals, and 10x since 4 years, with 20x from market bottom in April 2020. Many thanks to value pickr folks! ![]()

57 Likes

Latest folio status:

CAGR approx 33% since inception, 6.5 years ago, on the better days! Currently 2% down from peak.

Total 28 stocks.

| Company name | Last price | Cost per share | % of Total | Return % pa | Total Return % | Current Return % |

|---|---|---|---|---|---|---|

| KPI Green Energy Ltd. | 2008 | 124 | 9.9 | 190 | 2152 | 1519 |

| Tinna Rubber And Infrastructure Ltd. | 666 | 129 | 5.9 | 234 | 477 | 417 |

| Shilchar Technologies Ltd. | 4077 | 2378 | 5.5 | – | 71 | 71 |

| Ceinsys Tech Ltd. | 472 | 355 | 4.6 | 563 | 33 | 33 |

| Ugro Capital Ltd. | 266 | 191 | 4.6 | 23 | 54 | 39 |

| Sharda Motor Industries Ltd. | 1535 | 1233 | 4.4 | 66 | 24 | 24 |

| E2E Networks Ltd. | 800 | 614 | 4.3 | 485 | 30 | 30 |

| Arman Financial Services Ltd. | 2300 | 2237 | 3.8 | 5 | 3 | 3 |

| Satin Creditcare Network Ltd. | 246 | 257 | 3.8 | -26 | -4 | -4 |

| Phantom Digital Effects Ltd. | 472 | 487 | 3.7 | -10 | -5 | -3 |

| 3B BlackBio Dx Ltd | 820 | 354 | 3.3 | 54 | 292 | 132 |

| All E Technologies Ltd. | 278 | 256 | 3.3 | 73 | 9 | 9 |

| Kotyark Industries Ltd. | 1189 | 1247 | 3.2 | -86 | -5 | -5 |

| Caplin Point Laboratories Ltd. | 1518 | 806 | 3.2 | 94 | 123 | 88 |

| Gujarat Themis Biosyn Ltd. | 330 | 124 | 3.2 | 73 | 303 | 166 |

| Roto Pumps Ltd. | 436 | 410 | 3.1 | 36 | 6 | 6 |

| Indraprastha Medical Corporation Ltd. | 192 | 188 | 3.1 | 132 | 3 | 2 |

| Zen Technologies Ltd. | 826 | 858 | 3.1 | -71 | -4 | -4 |

| Godawari Power And Ispat Ltd. | 755 | 762 | 3.0 | 1 | 1 | -1 |

| Interglobe Aviation Ltd. | 3094 | 3199 | 3.0 | -76 | -2 | -3 |

| HBL Power Systems Ltd. | 552 | 581 | 2.9 | -96 | -5 | -5 |

| Sanghvi Movers Ltd. | 1098 | 1034 | 2.9 | 83 | 6 | 6 |

| Anuh Pharma Ltd. | 205 | 204 | 2.7 | 187 | 1 | 0 |

| Power Finance Corporation Ltd. | 435 | 430 | 2.4 | – | 1 | 1 |

| Shivalik Bimetal Controls Ltd. | 545 | 152 | 2.4 | 61 | 337 | 259 |

| Beta Drugs Ltd. | 1229 | 1509 | 2.2 | -71 | -21 | -19 |

| RBM Infracon | 635 | 667 | 1.4 | -95 | -5 | -5 |

| Hazoor Multi Projects Ltd. | 382 | 399 | 1.4 | -100 | -4 | -4 |

| Total Stocks | 100 | 32.2 | 137 |

Note: there maybe something wrong with KPI green calculation but Trendlyne portfolio auto synced with Zerodha reports exact same numbers as the value-research folio service that I update manually. I entered stock in August 2022. Don’t understand how average buy cost could be 123.

A more than 5 digit number is shown as - for “Return % pa”.

Churn continues, sold off RBL bank fully, and reduced some from Ugro, Satin and Arman, my remaining financial stocks. Rest some put into PFC.

Bought Sanghvi movers, it’s proxy for wind power sector, cranes operator.

Also bought Anuh pharma, is getting more serious about growth, doing capex, selling more to developed markets, introducing new products, so margins are better and some revenue rise is helping growing profits, could almost double in a year, still value is on cheap side.

To balance health sector weight, reduced Gujarat Themis and Caplin point. No sector more than 15% now.

Punting little bit on Hazoor multi project, used to be housing company but failed and new promotor has started road works, purely in Maharashtra, growth is good, still it’s relatively cheap but this sector is severely cyclical, infra work may be slowing, especially road works.

16 Likes

Hi Vikas, Pls explain why PFC? Its valuations have already runup quite a lot!

At 1.5 P/B Vs 10 yr avg of 0.7; so more than 2X!

What makes you bullish at this stage? Do you anticipate the volume of projects financed growing by more than 2X in the next few years?

Yes, I anticipate strong growth so historical average can be a misleading statistic sometimes.

PFC is getting into infra finance, power is growing, power now needs double the normal investment trend since renewable, mostly solar, only works in sunshine hours, so thermal, nuclear etc need same amount of backup capacity. In addition, you need pumped storage or batteries for some balancing.

1 Like

Absolutely, am still learning this and realize that it can be tricky since it requires much more deep technical/industry knowledge, in contrast the Reversion to mean strategy is easy to follow.

Had a few shares which i was contemplating selling due to the rise, but looking at the new areas you listed above, looks like there is growth still. Thanks!