Sold off PFC and Hazoor multi project. PFC was mostly a cash parking space. PSU, large caps are not my favourite areas, bit conservative that way.

Hazoor seems to depend on corruption in road contracts and growth was nothing special, mauritius based FII heavily bought preferential issue so could be money laundering too, not worth the risk. Thanks to the value pickr thread for this info.

Bought permanent magnets, it’s a difficult investment, very close compared to shivalik bimetal, they use some electronic parts and make larger product, possibly start making bigger magnets, good management. What happened to Shivalik also hit them, EV subsidies have been reduced at several places worldwide and so inventory reduction is going on, demand should slowly start picking up in next few months, hence the difficult part of waiting and watching. Thanks @phreakv6 for the💡

Bought Azad engineering, simplistic pre IPO calculations were pessimistic because they didn’t account for debt pay off, this simply boosted PAT by almost 2x, since there were huge interest payments. Now it’s just fairly valued for a high tech company. Given growth triggers lined up, perhaps on the cheaper side.

Azad engineering is mainly 80% exporting turbine blades to Japan, US and Europe in that order. For use in power plants and now aircraft engines too. IPO happened about 2 months ago. They used the money (and also some debt to equity conversion, thanks for the correction @Prdnt_investor!) to pay off almost all the debt (270 out of 300 Cr), while prospectus only mentioned plan for payment of 138 Cr.

They also make other metal parts, but focus is turbine blades which have a special shape called aerofoil for optimum conversion of fluid dynamics (velocity and pressure) to/from mechanical energy. So from super hot steam to run generator for electricity or super hot kerosene flames to run aircraft turbofan engine. Aircraft engines is a recent entry for them.

Capital goods sector can be highly cyclical, but turbine need regular preventive maintenance and blades are replaced before failure which can cause huge damage. Due to Russian gas and renewable energy issues, coal and nuclear power plants are back in focus.

As their huge debt burden shows that they bet large to get to this position. Apparently it takes 2-4 years to get parts approval to most of the biggest turbine makers of the world.

First started reading in some detail from IPO review by Dilip Davda. Found something here on twitter (thanks to @arjun0s), haven’t read it though, except some lines at the end about valuation. Rolls-Royce defence aircraft engine order kicked up the stock. Company concall transcript and presentation are good.

Hello Vikas sir, been following your thread for some time. Just curious, why so much diversification suddenly 12 to 25? Is it to preserve gains already made or you see the new positions as better opportunities?

Yes, you make valid points Diversification, if done right ofcourse, is meant to cut down on volatility and risk. Indeed, I think I see better options to invest hence the alternate buys, though I might have made a mistake or two.

I have only sold off two banks, Ujjivan and RBL, since I wasn’t paying attention while making 36% of folio weight in financials, with 6 companies. So, sectoral rotation happens, they gained lots rapidly, and financial sector can be bit complicated to understand. Now it’s just 12%.

No company or sector should be more than 15% roughly for a balanced folio, they say. Ujjivan and KPI green had exceeded to about 20% weight each.

The major reduced one is KPI green, to about half. Ceinsys, Shilchar and E2E networks have matched the growth, almost double since past 2 months, where the money was deployed.

Sharda motors, Phantom digital, Sanghvi movers, All E tech, Caplin point have all done well. Most others are doing ok too.

I think a small mutual fund kind of folio will also do ok, given bit less expectations. Overall market conditions are also not giving valuation comfort to go big on concentrated buying.

Sold off Roto pumps, exports focused business can face issues due to shipping rates increase. Also I need to sell in order to buy.

Bought Time technoplast, it has been selling off weak parts of it’s global business, promising to reward share holders with the money and pay off debt partly. Mainly just bulk plastic containers and more recently composite gas cylinders, cng, lng, oxygen as of now, maybe even hydrogen. Doing some capex too. Demand has been strong with 80% capacity utilisation. Seems bit on cheaper side since natural gas prices are at record lows and composite cylinders are safer and lighter than steel, other businesses are also doing ok.

Added Exicom tele-systems.

It’s mainly lithium batteries for telecom, faster growth is EV charging. Lithium battery price is falling, can be possibly used for grid scale energy storage.

Exicom are related to HFCL, maybe part of 2g scam, they teamed up later with videocon, and also did some dubious transactions in share market leading to a ban by SEBI for some time.

They were likely not charged for 2g scam, they did help Reliance get into 4g.

I found the idea from write up by @akash_das, though I am being contrarian here.

So it’s like HBL power, except they mainly do lithium batteries while HBL just started working on new project to make them, EV charging looks ok which can grow faster.

Reduced mainly KPI green since it’s likely peaked for a while, also from Ugro and the other financials Satin and Arman etc.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor, please do your due diligence before investing.

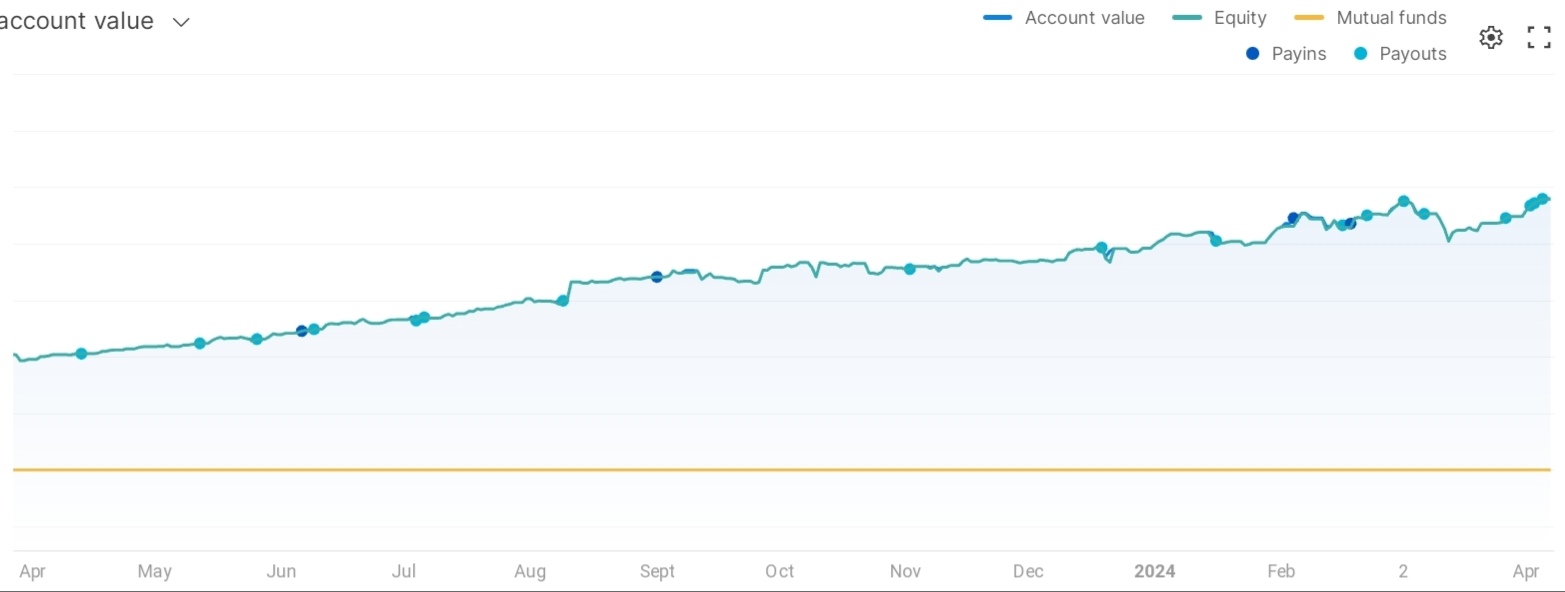

Latest folio status:

CAGR approx 33% since inception, 6.5 years ago. Currently 3% up from previous peak. 165% up in past year.

Total 29 stocks.

Average cost of share data is only correct technically as per FIFO method for taxation of gains computation, where bonus happened older shares have higher cost and which get sold first, it is making average buy price look artificially low, such as for KPI green, Tinna etc.

Financials are having issues mainly from sectoral rotation, bargain sale is on since fundamental story is fairly intact. Phantom digital is facing the angst regarding competition from AI. Several have high expectations backing them, the ride is bound to be volatile in names like RBM infra, Kotyark, HBL etc. Beta drugs is mostly a mistake, not in hurry to exit, position size is very small.

Started to increase withdrawals monthly to build a safe fixed income pool like bank deposit or debt fund etc, likely make it around 5-10% of folio size over next 2-3 years.

@vikas_sinha - Firstly, congratulations on achieving 33% CAGR over almost 7 years, that quite an achievement. Do you mind sharing why you think Beta Drugs is a mistake? Would like to understand your anti-thesis on it. Per me, it has the following things going for it:

Strong R&D setup in place

Indian Oncology Drug market is on the rise

It is a net debt free company

High ROE and ROCE business and steady operating margins of 18-19%

It’s expecting 290cr+ revenue for FY24

And I also believe you have been tracking Arman Financials for a while now, what according to you is the hold up with it? Is it the recent increase in NPAs or is there more to it? It’s been consolidating for a year now, which I think is good. But when it comes to triggers which will make it regain its upward trajectory again, what do think those are?

Well beta drugs looks to me just one of the weaker positions compared to the rest, I bought it at the absolute peak too, might have waited for 1300 levels atleast. Your projection is correct, that doesn’t provide immediate growth trigger for the stock and I am not that much of a longer term investor. It’s releasing half yearly results only and hardly sharing info with investors. Regulatory action can impact profits, also I don’t trust the high valuation of pharmaceuticals, just my opinion, better for margin of safety.

Arman financials is not out of sync with the market action the entire sector is facing. Yes, I too hear of elevated NPA, it’s just one of the scares that happens with faster growth, I mainly trust their solid background. It’s expensive based on great performance and expectations, and for such tiny caps price movement can be bit exaggerated. Yes, strong growth seems to happen in yearly cycles, so the consolidation phase may just be getting over.

@vikas_sinha Have been following this thread for long while now. It’s impressive to have 33% CAGR since inception and quite an achievement. Congratulations on this feat and continue providing value to the community.

I wanted to understand the rationale behind how you profit book on your investments over a period of time. Do you have set rules for example, every 40%, 100%, 130% return on the stock do you partial book your way up or book a certain percentage of the allocation and rest let it be till there are flaws in fundamentals.

Also curious to know how exactly you are going about this? As in, How do you maintain set portfolio size/ allocation on stocks while you increase withdrawals/payouts moving forward?

@Arjun_Pillai thanks!

I have targets, which depend upon developing situations also, so like a moving target. When prices approach this target, and margin becomes less, I start booking, in stages. Sometimes momentum carries it over the target while I keep booking.

Mostly I have 100-150% kind of targets over 1.5 to 2 year time period.

It’s a very slow withdrawal rate, on a monthly scale, I just book a bit randomly. For bigger withdrawal, indeed it is sometimes simpler to just take out equally from most constituents of folio.

@prav.br

I don’t have any special thesis for Arman, mainly it’s just that I have a weak spot for financials, so was holding Ujjivan, IDFC, RBL, Satin, Ugro, even PFC, about 6-7 stocks, aggregating about 35-40% of folio, until about quite recently. Financials I guess are an easy proxy for overall development cycle, and if you can find them cheap before a rising cycle then all the better.

Specifically you can maybe spot a tendency leaning towards micro finance. So I am still holding Satin. Also holding Ugro for its MSME focus. So its more a basket approach, preference overall is for NBFC targeting the underserved sector. Arman has good track record, some good metrics and is still quite small to grow faster than others, for which it seems to be on track.

@Prakash_Kumar transformer and power sector will see very good business, for a considerably long term. Transformer demand supply gap is huge with international and domestic growth, supported by renewables which have picked up pace. Power overall is just close to teens growth rate, even doubling in 5 years means just 15% yearly growth, just basic growth rate. So I am not that interested in just generic power label. But few specifics like renewables, energy storage, wind EPC etc are far more interesting.

Hi @HarshVijay frankly I don’t have much idea. Had looked at it due to recent IPO earlier but gave up since had just picked up Shilchar in the transformers domain. It’s looking more diversified than Shilchar but I would be little wary of marketing terms used like solar and wind transformers as if they are somehow speciality types. Ignoring any more details and what looks like increase in gross block. At the end of the day capital goods are very cyclical afterall so bit risky.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor, please do your due diligence before investing.

Thanks a lot for pointing that out @vikas_sinha . I delved deeper into whether the tranformers are really different for both the different types of energy sources or is it just a marketing gimmick and here’s what I found briefly:

while the basic principle of operation remains the same, transformers for renewable energy sources have distinct design considerations to address the unique and specific challenges and requirements of integrating these variable and intermittent sources into the electrical grid.