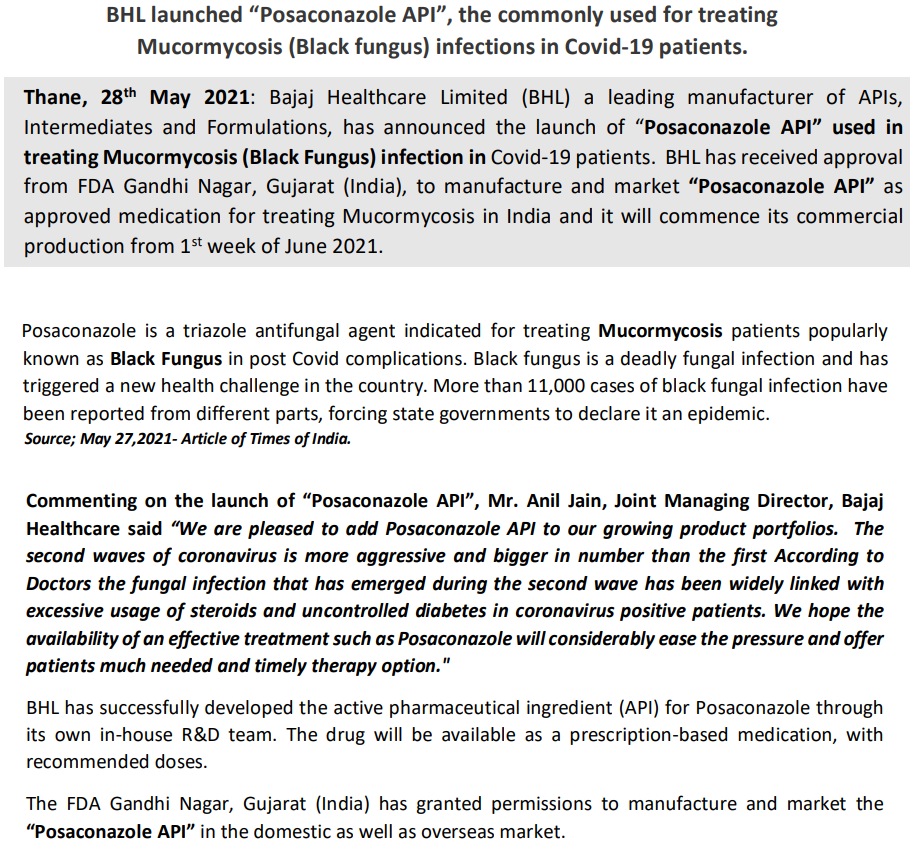

Yes, I did find mentions for this co and checked out the background. It seems not that great quality but maybe worth a small sized punt. What turned me off was the fact that the co did a complete turnaround within 2 weeks, from sending announce for completion and expected start of new plant to then saying that the foreign engineers were not available for final startup.

They have repeatedly, over many years, said they will get cheap raw-material supplies from fertilizer co, that is finally looking to come true. Also they have done good sized expansion. These two seem baked into the current price, given good Aluminum cycle which will last for some time.

Further, their investment in middle-east is also looking promising, to may provide more growth. It may turn out to be an ok bet, bit risky IMHO.

No change, just a very small addition (0.3%) to Shakti pumps just before the results date.

Results are still pending for about half of the stocks in folio.

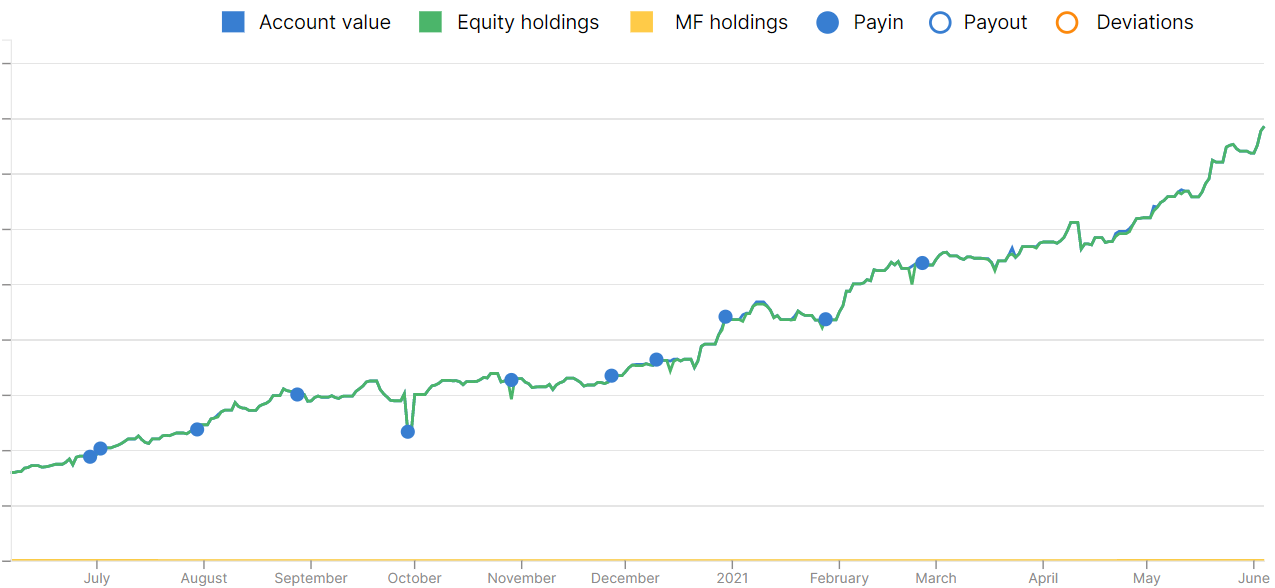

PS: The last pay-in is when I achieved atma-nirbhar/financial independence status. The processing/paper-work took a while, the intent having been declared 2 pay-ins before that

650% return in a year is extraordinary, Vikas. Congos. How were you able to achieve it? What made the difference. Are you entering stocks based on triggers and exiting after the trigger. I guess you are entering and exiting fast like in 6 months, not going for very long term. I have few stocks from your list.

Thanks, Pankaj!

I have corrected myself, it is 5x (gain of 400%), sorry, got carried away with the horizontal lines on the graph, which I used for rough computation (happens to me all the time ).

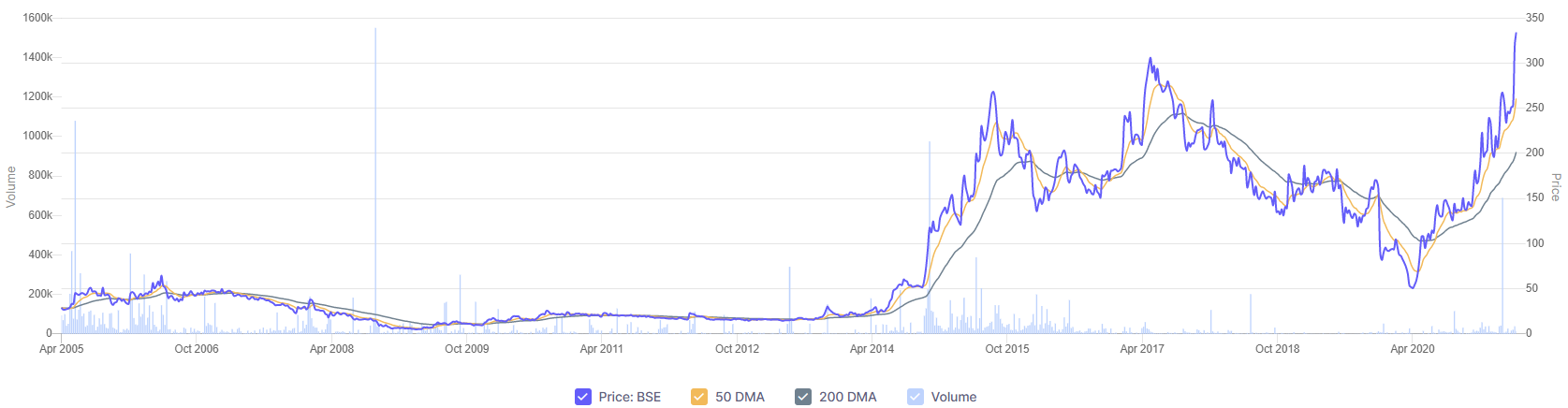

What helps is choosing the start-date for comparison. Till 1st week of June the stocks had been beaten down a bit and bullish recovery/reversal was yet to start.

Yes, I did choose to make exits soon enough, not really longish term value-investing style. I evaluated the valuation triggers and the time-line in which they would play out, and hence the price-gains v/s time. If the stocks seemed to be slowing down considerably and the risks tending to show a possible back-slide or stagnation, that means I would look to cash-out and try to find a better alternative.

Made some mistakes but bull market is very forgiving

Only Laurus struck me as having such great potential to be a value-pick for a long term, over-riding short-term gains mentality. Thanks to Hitesh bhai who keeps educating us with his ready wisdom

I have been trying to find at least some medium-term quality plays like Kopran, RACL, Pix, which can sustain decent valuations while having longish growth runway. Thanks to Rajeev Jawahar who keeps posting info on such gems

@vikas_sinha

Cement prices are likely to sustain at such high levels !

Mid cap cement stocks gaining momentum have look at sanghi cement as techno funda. Bet…

Please share ur views on that…

Yes, @Kuldeepjadeja very good point, cement is severely constrained by capacity, prices will be high. But I see this already priced in and we should only pick stocks with fresh capacities coming online soon. Not studied much actually.

Got interested with the company as they just completed an expansion project at Sanghipuram, Kutch. The expansion included 10000TPD clinker unit, 67 MW Thermal Power plant and a 2 MTPA cement grinding unit. The new unit commenced production in Febrary’21 behind schedule by a year due to covid related delay. With the new expansion project can the cement company post great results?The company has a price/book value of 0.78 and CWIP of 1262 cores as on Sept’21. Are we going to see the end of company’s production woes with the current expansion?

Tips, post-demerger is/will be a much simpler biz than Saregama. Tips library gets more monetization than Saregama as analyzed on its thread. I find more valuation upside in Tips, and their biz decisions seem better, in terms of content purchase, highly subjective, for a habitual skimmer of info such as me. Management quality wise Saregama seems bit better, but Tips may be catching up and not that bad, again bit speculative judgement.

Indeed that is the risk, but we have to consider the fact that the monetization of content will grow at a good pace to sustain valuations and provide upside for years. This will be a secular trend, easier to play than cyclicals etc. Should maybe always have a decent premium valuation. Demerger should kick this up and technically it was just retracing from ATH levels.

Good find! Expansion seems to be 25% of current capacity, very rough estimate. Also depends on the entire industry capex cycle. Infra push may help this along, but it depends on the particular company situation, this one seems good actually!

Company’s locational as well as raw material advantages.

The company has its plant in Gujarat and 80- 85 % of the sales comes from Gujarat. The other two major states include Maharashtra and Kerala. SIL has an integrated cement production facility with easy access to high quality raw material, viz., limestone, at its captive mine about 3 km from its plant. Further, it has access to other raw materials like laterite, silica, clay and fly ash in the region with captive mines available for most of them. SIL has its own source of power with its 61.5-MW captive power plant (CPP) located about 10 km from the clinker plant and 2 km from the cement plant, adjacent to its captive jetty. The captive jetty allows SIL to directly import coal/pet coke for operating its CPP as well as for its cement operations. In terms of its fuel mix, it has the option to switch fuel source to lignite/imported coal/pet coke at both its CPP and clinker units, offering it the flexibility to control its energy costs depending on market conditions. The western India is traditionally a strong market for cement. Due to the captive jetty available the company is also exploring the possibility of export of clinker with the added capacity coming on stream. Company has also signed an agreement with Zuari for using its bulk terminal facility at Kochi port for packing its cement for usage in Kerala markets. Proximity to port can be considered an additional advantage for the company when it comes to export and reaching new market close to ports. SIL has also completed dredging activities at its jetty facility for enabling higher capacity ships/barges to voyage directly to the jetty.

Capacity Utilization

The company’s capacity utilization has been pretty poor (less than 50 %) in the past may quarters. Operational issues were one of the key factors, however, even during such dull quarters company was able to clock very good EBITDA/ ton close to 1000 due to good raw material management.

Debt

The company’s debt has moved from 771 crores in FY’19 to 1256 crores in FY’20 mainly due to the very large capex undertaken. Moreover the company has issues NCDs worth 305 crores for private placement on 23rd February for redemption of NCDs worth 256 crores issued in March’18. The NCDs carry a coupon interest of 14-16 %. In such a low interest scenario it’s not pleasant to see the company going for such high cost debt. The debt will be for a tenure of 6 years. The earlier debenture were at 10.5%.

To conclude it can be seen that the company has almost doubled its clinker capacity. The enhanced capacity has come on stream in Q421 when the country is seeing increased demand after covid unlocking, However the demand may have flattened with the 2nd wave. The company has advantages in the cost side due to its integrated nature of operations and proximity to raw material. The company has captive limestone mine, captive power plants etc. Also captive jetty will aid the company in imports of pet coke etc. and export of clinker as well. Digvijay cement has a similar market and had a revenue increase of 22 % in Q4’21 over Q3’21 with increased OPM margins. The capacity utilization along with debt reduction will be the key factors to watch out for.

Key risk:

The very high debt along with high cost of debt can be disastrous for the company if demand/ capacity utilization doesn’t pickup

Very well tracked company on this forum thanks to Balki and others. I prefer companies with disclosure/interaction with the retail, so con-calls, presentations etc. The pedigree is now impeccable, and that gives lot of traction for growth. That has yet to materialize, hence optimistic about management projections (with a pinch of salt, of course). The valuation is comfortable, and value sharing via periodic buybacks is good idea, they price them right also. Likely they announce a dividend policy soon.

).

).