I agree to @phreakv6 that this doesn’t really call for long term growth stock. With only low-cost differentiation and customized solutions, you cannot become top vendor in this industry. What is required is significant R&D to create really disruptive product which can create performance

differences.

But Tejas being a very small player and with tiny R&D investment cannot do that.

But what I do see a few positives for the company are,

It remains the only true Indian company in the telecom network space. I know from inside circles that Tejas top folks are involved in most of the Indian telecom discussions. There has been a discussion that Govt has plans to allocate funds to Pvt companies to develop solutions that are India specific. So if and when Govt telecom picks up, Tejas benefits. But it is definitely not the only thing to consider for investment.

2nd point I see is the company has been able to survive for 20 years in the cut-throat telecom market and know how to survive. The management is ethical and have passion to build a business in this space. They don’t know any other business. Their focus will be on sustaining and growing.

Also, today the market is matured as said by @fundoo and no new players want to enter this market.

At the current price, it seems like quite a discount and matches Graham’s net-net approach.

Over the next 6-12 months how the company fares on Pvt business matters.

But with current product capability, sustained growth over the long term with a focus on only pvt business seems really tough. The company must get significant support from the Indian government because this industry especially companies in hardware telecom needs govt support.

Disc: Invested.

Agree with @Prash, they are never going to be the next Huawei. But they are able to fill a niche gap in the market, are able to retain customers and are playing in a huge growing global market where all they need is a single digit market share. I came to know that the line of credit that Modi is promising to lots of African countries, Bangladesh and even Russia can only be used by these countries to buy indian equipment. Apparently Tejas is making a play for that also. If they are able to get into few global telecom accounts, and the brand gradually builds, they can do well.

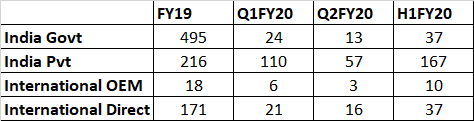

If we see H1FY20 segmentwise results then India Pvt has increased significantly from 216 in Full year in FY19 to 167 only in H1FY20. International sales have not done well. We should not expect anything from Govt Business significantly in FY20. This leaves us only one segment to grow which is International Sales and I dont think this segment will give the kind of growth given last year which was 70% last year

On the product side what Tejas markets as a strength is the telecom customer does not have to invest upfront in the equipment and he can increase its equipment’s capacity as and when required as the business grows. This gives the advantage to the customer on the expenditure he is going to make on Capex side. For example if 48Tbps Aggregation eqpt needs to be replaced by other OEM then the Telecom Operator has to invest upfront for the eqpt and the cards in it, but in case of Tejas he can start small and upgrade the eqpt as his business requirement grows. Will need to check the validity of this point.If @vikas_sinha or other members can verify this it will be good.

Disc: Holding. will wait till next quarter if situation improves.

“SW defined HW” is over-sold. They are just trying to “turn the weakness into strength” ™. Any hardware gets obsolete, with time.

HW Upgrade cost-benefit is usually good. HW gets (rapidly) cheaper with time, so the same money buys you more processing power. More processing is required for greater capacity or higher performance/more complex telecom protocols (higher xG, generation number)

There is practically limited scope to reuse old hardware for new, higher level tasks.

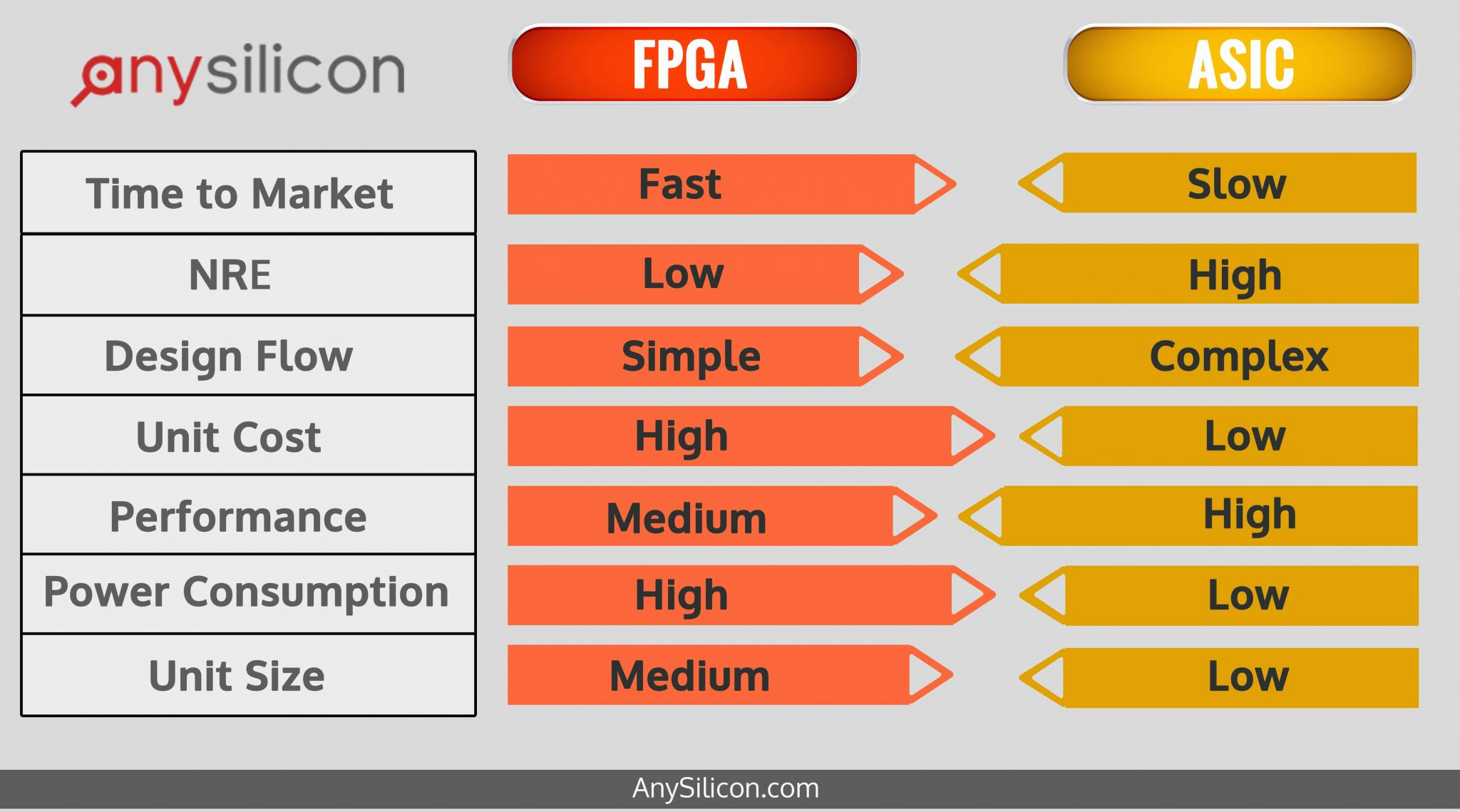

It would be difficult to match performance specs with patching using old hardware. I do not think it should be a big consideration in costing of networks. As it is, an FPGA will be several orders of magnitude slower than ASIC used by higher volume/bigger-sized competitors. As explained earlier by a more domain knowledge guy in this thread @alexander .

Network for Spectrum is a Defence project (by BSNL) where spending is likely going to be half of the BharatNet costs. I am saying they should bounce from here but I am not sure of their longer term play.

@nityanandparab Are you sure your numbers are correct? Below is an excerpt from their Q2 earnings presentation

Sales Update

• Government business during 1H was weak (YoY decline of 88% for 1H), resulting in significant revenue decline.

• As anticipated, no new business expected from BSNL for rest of FY. Government critical infrastructure projects will

result in strong bookings, but some revenues will slip to next FY.

• India Private: Strong YoY growth of 67% for 1H

• For full FY, we expect YoY growth to be similar to last FY.

• International: Strong momentum; we added 5 new international customers in Q2.

• In addition, we closed techno-commercial discussions on 6 new customer deals (2 in Asia, 3 in Mid-east/Africa, 1 in

America), each of which are expected to result in multi-million dollar orders in 2H. • Overall we expect international YoY growth to be similar to last FY • Run-rate business (India-Private + International) grew 28% YoY for 1H

As per management when it comes international sales, what is changed now compared to last year is, increase in company focus by adding sales force . The expectation, 2nd half of the year to close some deals. But most telecom sales cycles are long, hence majority sales can spillover to last quarter. My guess, next 2~3 quarters crucial to know how international sales happening or not

Sorry to butt in here again

I would like to say that ANY supplier can do what they are doing (program and re-program etc. FPGAs, even engg students do that) but they do not do that, I assume, preferring ASIC. Or maybe the other suppliers do, since even smart-phones have some FPGA parts, such as for cameras (not their main feature), I observed on youtube in some deconstruction video. But they DO NOT advertise this as their best/selling feature.

Your PC can read and play DVD like your TV/DVD player. The difference is that the PC is re-programmable (behaves somewhat like FPGA) where as the consumer electronics usually have ASIC. But the difference is getting really small these days. Between using hard-wired chips/ASIC and SW running on General purpose chips (something similar to FPGA).

Phones did not use to get updated but now they do. Even my set-top box gets updates.

Maybe telecom does not really require super-duper performance and millisec delay is fine in place of microsec.

But if there really is an advantage in selling using FPGAs then ANY BODY can do that. Since SW is always written separately and is “compiled to silicon” i.e. chip is designed, only for reasons of better performance (speed, power), mass-production i.e. lower costs.

ASIC is only used when mass selling is required. Because “chip-designing” costs (little) extra and the design is sent to the actual chip manufacturers who only make chips for big orders.

Maybe Tejas have taken an obvious niche that nobody cared about or noticed. I have my doubts.

Strong buying for the last 2 days in the counter. I can’t see any news flow around this. People who are tracking Tejas if they can throw some lights then would be very helpful.

Couple of days back I was contemplating the decision to increase my holding further and was looking at Technical Analysis to enter at right price point. But now I will wait and watch.

Disclosure: Invested at 78 (average price). Among the top 5 holdings in my portfolio

Not aware of any news about the business but this is very typical for market to beat down the price significantly well before worst results for few quarters. By the time the worst results comes, smart money has sold off and retail investors starts to panic based on results and sell off at wrong valuations. At some point after this, price of business gets below the intrinsic value and that’s when smart money starts buying again and retail investors feel left out.

Management has said that coming 2 quarters are going to be good so might be that market is looking ahead. Management has been wrong in the past about government business though. Management has also said that bsnl payments will be received by end of the year.

Performance wise FPGA will never match equivalent ASIC (Application specific IC). For chips produced in massive volume for any application , any company will go for ASIC.

FPGA are used for cases where the market is small so that it doesn’t justify the high costs of designing an ASIC.

So aslong as Tejas is doing FPGA & not climbing in the value ladder to ASIC , they will never be another Huawei or intel.

DISc: Not invested .ASIC engineer for a US based MNC

In the conference call and other latest interviews, management has said that they will be able to do apprx 750 crores of revenue for this year. In best case scenario, even if we take it on face value and assume that it will be achieved and PAT margin will be around 14%, then the PAT would be around 105 which means at current valuations, the PE of Tejas would be around 9 after the year.

Current PE is 12 so its not really cheap wrt earnings of entire year. Unless there is a PE re-rating which is very unlikely in absence of significant business development or great new unexpected orders, the price may not move much for a year.

So bottom line is that considering the foreseeable future earnings potential in medium term, the valuation is not attractive.

For longer term, it is hard to know how things will pan out because

Government business is not coming back soon with BSNL in trouble. This will change if we get to see significant development from gov on BSNL and pending Bharat Net phases and smart city projects.

There is not enough evidence to say that international business will turn out to be great success, this is also something which will become clear in future but can’t be predicted now. In fact @vikas_sinha@arunjacob have pointed out gloomy picture about their product.

India private business is also not having any tailwind with most of the players in telecom struggling.

So in short,

current valuations are not attractive wrt near term future of 1 year

there is not enough evidence to judge long term future because of reasons mentioned above.

Considering all this, I felt that current rise in stock price can be used as an exit opportunity. If such dramatic 40% rise would have not come, I would have probably held my position and waited cause negatives were in price and now possible positives are in price. I had averaged at around 80 so that helped somewhat. I decided to bite the bullet and booked loss yesterday at around 100.

I will closely monitor coming quarters and business development. Given the current situation, I don’t think things will change dramatically and I will get opportunity to get back in at reasonable price if at all things starts looking better. I did not want to hold on to a business with less potentiality purely based on hope at current valuations. If things turn around then we can always get back in.

@vikas_sinha and @arunjacob can you guys throw some light on how does the products of Tejas compare with that of Ciena which is major competitor? Also it would be helpful if you can compare the business models.

On a side note for me, lessons learned from this investment…

Do not trust last 2-3 years of numbers of a recently listed business and never allocate significant position to them unless it is definitely a quality business. Most companies do window dressing of last 3 years of numbers before IPO.

Do not ignore the risk of client concentration especially if its government agencies.

For a company like Tejas which has been in business for 20 years and having significant expertise, getting ASIC based solution won’t be really difficult.

But why should they do or what is consequence of doing?

IMO, One huge investments required, 2nd you will have to chase market where other big players already established 3rd, you run the risk of huge Capex year or year with dependency on fab manufacturing

In that way I think Tejas has chosen a market which is fine with FPGA solutions.

Not not every car buyer can afford or wants the the performance of BMW…Many are fine with Maruti. Similarly Tejas is targeting a market who are fine with performance of FPGA with lower cost.

Need to explore if this is by itself a sizeable market for the company size of Tejas to grow year on year.

I am sure they will have to migrate to ASIC sometime in the future. But expecting Tejas to become Huawei/Intel is too much of expectation

For the kind of solutions provided by Tejas, FPGAs are the industry standard platform. All competitors use FPGAs, only in specific cases ASICs are developed. Reason is that requirements keep changing, easier to fix any issues without re-spin, number of units being sold, backward compatibility. ASICs once made can’t be modified to add a new features or even fixing a bug, R&D cost being way higher than FPGAs.

But here, Tejas has to compete with global players. Note: I work in communication industry but not invested in Tejas.

My whole point is about the market size . FPGA are made for small markets where the number of units are small .

May be Tejas has a niche in a small market , but fpga are so easy to design , you just need to burn your code into the FPGA chip (FPGA is a predesigned chip which can be configured & are supplied by xilinx or Altera).so there is moat here .I have done this back in college.

Actually ASIC are cheaper if made in huge volume . Also performance & power are less for ASIC .

The only application where FPGA are used is when markets are very small & performance & power doesnt really matter . In this case FPGA is cheaper

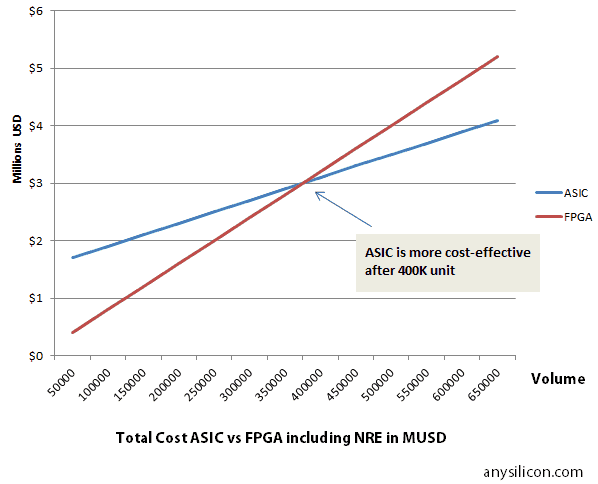

The below is a rough chart for how many units ASIC or FPGA will be cheaper (it varies for each technology node) (this is a rough graph i got on google search)

I have no idea about cienna . But as far as i know CISCO & huawei are the major players in the international markets & both of them have ASIC design teams which makes their product cheaper than their competitors and with better spec

All I repeatedly said is that choice of tech (FPGA vs ASIC), it seems, is not special to Tejas. It is mostly dictated by volumes, top among other factors.

It’s likely that the OFC device sales/chips used in them, are not big numbers, around half-million mark, where FPGA/ASIC choice is not big thing.

Tejas by choosing FPGA, stays cost competitive and has customized its products to be highly-reusable. This is the “moat”, if at all. Cheapness even at low volumes by selling re-use. Bit of a hard-sell, IMHO, since FPGA is obvious choice below volume threshold anyway.

If Indian govt spending and preference to make in India both work-out then there is a definite market. Our net speeds are quite low, maybe infra spend is needed, but is the govt going to be an (big) actor in the market? Doubt it. Modi wanted solar-cells to be made here but lost in WTO and now we just make panel-frames for chinese PV, having almost zero PV cell production of our own.

Their overseas sales seem to be in part from some sort of inter-govt sponsorship, maybe special funding grants are involved which make Tejas competitive.

Tejas does seem to try and have some specialized products, private Indian players sometimes buy their “metro” links (devices aggregating data from multiple different kinds of sources).

They did supply OEM overseas, formed a decent part of sales, before selling under their own brand.

This is a tough, competitive market and Tejas is not even in top 10. They are trying to leverage cheap Indian R&D. Will it scale? I chose not to bet.