Consilium acquired 0.11% more stake - link

From a pure product-wise, it is difficult to differentiate with existing players.

What I understand from Tejas AR & other presentations is that differentiating in the market they are choosing to compete and also how they acquire new customers.

They want to be in Tier 1 players in developing markets and Tier2/3 players in Developed markets.

Acquire at a lower margin and then build on the same. For a new customer, as per Tejas, their offer looks similar or better compared to competitors.

Now, this is as per Tejas, we don’t know how competitors responding! There is enough market and with good sales force, Tejas can capture. Whether they are able to do is what numbers will tell over next 2-3 qtrs

2 Likes

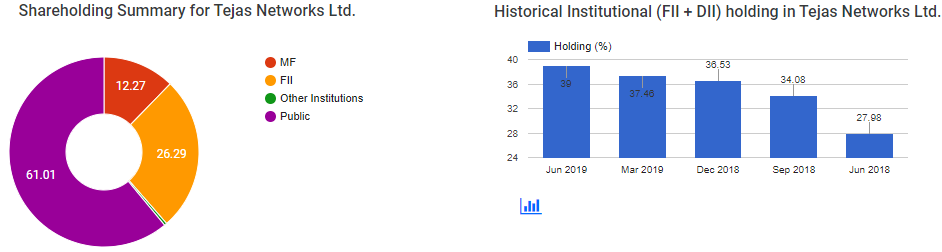

FII/FPI/MFs have kept on buying while price has been falling in past year

40% of shares are with Institutional holders.

src = Latest Shareholding Pattern - Tejas Networks Ltd.

2 Likes

From their AR -

‘In July, 2017, the Income Tax Department initiated proceedings under

Section 132 of the Income tax Act, 1961 and had issued a restraint

order on certain bank accounts and deposits of the Company and later

the restraint order was withdrawn. The Company and its officials fully

co-operated with the Income Tax Department. As on date, there is no

demand raised by the Income Tax Department.’

Anyone know the details of this ? This is all that they have mentioned … View pls

I don’t think this has been asked (I might be wrong). You can ask them in the next con-call/AGM if you have time. They are generally very straightforward and will answer

1 Like

Tejas Networks launches World’s Largest Disaggregated Packet-Optical Switch at India Mobile Congress 2019

1 Like

Very bad set of Q2 results. Not sure if this is priced in (Link)

Investor Presentation (Link) - Good to see cash balance has increased

This year will be the new base for the company for future years.

Related news on BSNL/MTNL merger and revival plan (Link)

Disclosure: Invested

CNBC interview

important points from interview ,

- BSNL/DoT started clearing the payments. 220cr pending payments. Received 20cr in Q2 FY20.

- Confident of achieving 500cr sales in H2 (Sanjay looks unconfortable with this question but just says he is confident as 2/3 of revenues are from H2 in the past)

- Cash on books 290cr , will use this for R&D and international sales instead of speding on dividends or buybacks which he sees as short-term confidence building measures for supporting stock price.

- 100 cr business from govt. companies (Utilities,Railways) is not impacted.

Cash on books + BSNL receivables = 510 cr and mcap is 672cr.

Disclaimer : Invested @peak (400+) and will not sell as it will acts a reminder for me whenever I get tempted by the low valuations of govt. companies or the companies that depend excessively on govt. for sales.

3 Likes

Hello,

You could sell and keep a token amount to remind you of the losses. I have myself collected a number of such stocks (BHEL, opto circuits…) and kept a token amount to remind myself of my amazing stock picking abilities ![]()

2 Likes

As per latest holdings,

src: https://trendlyne.com/equity/share-holding/54898/TEJASNET/latest/tejas-networks-ltd/

FII+DII = 40% (22% is Foreign)

And of the rest some 44% is divided among various Foreign non-institutions.

So, majority is foreign owned.

Maybe they know something we do not?

Only 8% is really Indian “public” individual holdings.

Good point. I have worked in the chip manufacturing sector, with the fabrication equipment makers, one core product. The company had 90% market share, with only 2 other Japanese competitors.

Being the Highest-Tech we had gross margins of 60-70% and net of 40-50%. The biggest expenditure was R&D, we were the top spenders in Europe, much more than Shell, Unilever but less than EADS, Thales or Airbus. And of that of course the biggest factor was paying the people/D&E staffing.

Tejas should be able to compete purely because of cheaper Indian talent base.

Also, optical is the future.

With 4K TVs and everything on the Cloud, people just stream a lot of data. Everything is data and streaming. Music, voice, entertainment, surveillance etc. Networks will have to scale. Europe is slow and expensive and needs to catch up. US is still running at a good pace. I picked this up from Sterlite thread. EMEA area can support growth.

PS: The company I mention was sold off by Philips because a decade ago there were several such companies and they thought making money was simply impossible.

Things are still scary in the business, very prone to cycles of big-investment. 2008 led to 50% contract staff fired. They keep staffing out-sourced as much as legally possible.

If you look at the DRHP, you can see that Samena Spectrum acquired majority of its 13.98 million shares from pref allotment at Rs.120 (5.6 million shares) and a bulk of it, about 3.9 million or so around $1/share from sycamore networks (high-flying dot-dom entity to currently bankrupt entity). Overall all these FPIs have acquisition costs roughly around Rs.60/share on avg from 2016. They sold 25% of their holdings at Rs.250 in the IPO covering their costs. Samena Spectrum sold further and everyone else has too, to some extent above Rs.250 making it an overall profitable position for themselves.

When I was researching I came across this piece from 2013

Take some of the optimism from Deshpande here with a pinch of salt, as he still had stake in Tejas when the piece was written. It is also strange how most of the excuses still remain, from increasing international business to competing with the Chinese on cost and so so on. The problem here is that Sycamore, Alcatel-Lucent etc have all ceased operations because this sector itself is hard to make money in. So the question to ask yourself is if you want to be in a business with poor economics and commodity nature. If they move from govt. orders to private businesses, who are these going to be? Are Airtel, Jio and Vodafone-Idea in any capacity to incur further capex for 5G in their current state?

On top of this they have keep spending around 100 Cr avg on R&D costs every year, roughly about 13% of their topline which doesn’t seem to provide any inherent advantage in terms of margins. Benefits if any, are being enjoyed by the Customer with no benefit being accrued to the business and its shareholders. This is akin to Buffett’s powerful loom example. Some businesses have to jump so many hurdles just to stay in business!

All this said, at around 500 Cr market cap (Rs.60/share) it could look attractive to a Graham style value investor.

9 Likes

They are very comfortably placed for sustenance …

- 0 debt and good amount of cash

- Flexibility to scale up and down quickly - how many companies can have 50-60% volume decrease and still almost breakeven…

- Niche player in a Huge and Growing markets where they operate giving a lot of runway

- Very high retention among existing customers (almost no churn )

- Any government investment from time to time is a huge bonus

Downside Risks from this point seem very very less…

This is a cigar butt worth investing in my view

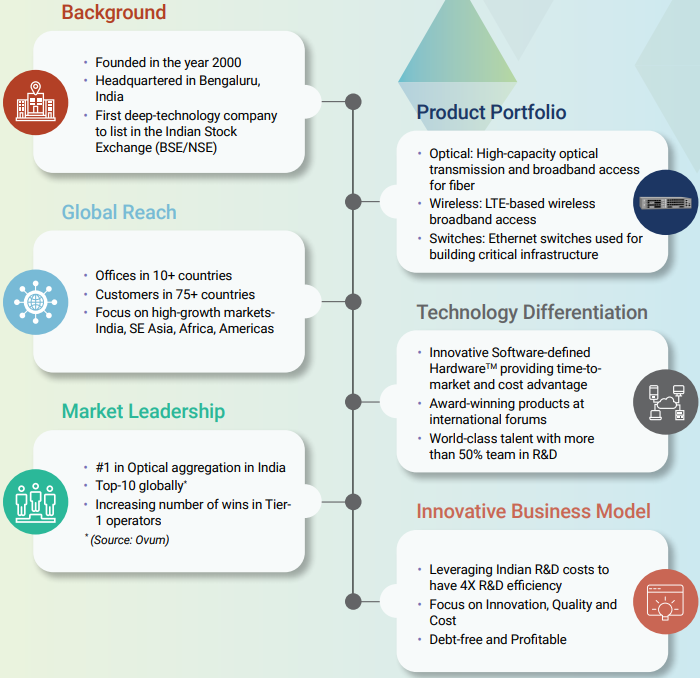

What you see as weakness, they project as strength, their R&D. (see the bottom right boxes)

Sycamore failed mainly because of not upgrading the tech.

Profits will be lumpy, governments will pay, SA or India (very rarely do they go bankrupt), eventually.

Yes, WB is right, the business is tough. Boeing 737 MAX disaster is an example of how tough.

My work-life started with an IIT-D start-up in telecom domain. It did not survive selling to Defence and Airtel.

But I still believe make-in-india will survive in this domain.

source: AR 2019 page #4.

Yes, Samena has sold off 5% (between june-sept 2018) and other individuals have sold off 5%, absorbed by Institutions. Indian Mutual Funds have bought 12%.

Samena was an initial PE investor with 20% stake reduced to 15%.

And Mayfield reduced its 10% to ~8%.

So, 25% of their equity was diluted to raise funds through IPO.

Some others exited. So, yes they are there in the ride for “free” but of course capital opportunity costs are there.

source: https://www.vccircle.com/tejas-networks-files-ipo-frontline-pe-intel-capital-sell-stake/

Companies go bankrupt in this domain simply because the R&D expense is too big. Also why India is the out-sourcing capital.

But ultimately Tejas have to sell products. Also their receivable days have doubled in past year, to 9 months now.

Sycamore failed because the dot-com boom was 10 years ahead of its time. That might be true again.

Thanks to @phreakv6 I have exited this today. Happy Diwali!

I understand the Foreign holding is due to Deshpande of Sycamore.

Reckon Tejas was Sycamore out-sourcing house till it went out of business in 2013.

This business has had 20 years to scale and it never did. I do not see why it will grow now. Even in 2008 it had sales that it has currently, not inflation adjusted! (the link shared by phreakv6)

Its AR 2019 shows nothing exceptional, only scary things like majority dependence on huge government spending. Only because of reducing this do the sales to others show some growth. (% effect)

FPGA based dev is more for prototyping than large scale deployments.

It is not even in the top 10 of vendors worldwide.

Multiple sources quoted here by IEEE:

It cannot even sell in India beyond 15-20% share. And most telecom spend is going to face a slump, drastic in India and little moderation worldwide.

The stock was likely prepped for an IPO and we fell for it.

BharatNet optical gear vendors also included L&T ECC, so Tejas is not exclusive even here.

Stage 1 is complete and Stage 2 will be much delayed and split over various agencies. It was supposed to be complete by March this year and has not even started by the looks of it.

PMI (preference to make in india) policy is not implemented by most procurement agencies.

1 Like

CMay I know what was your acquisition price?

At this juncture (and price point), as mentioned by alexandar, i don’t see much downside risk to the stock given traction and focus on international business.

There is no disruption to tejas products that suddenly it will go away out of business. In fact, the demand for optical networking equipment is going to grow only and Tejas can capture some of it specially in the emerging markets where the biggies will not come (because the market is too small for them).

I agree that it may not be a Sustainable long term bet but at this price point risk reward looks to be in the favor. I see this year as a transition period for the company.

Biggest risk is obviously no pick up in the international business as guided by management.

We can’t compare this scenario with 2000 dot com bubble where lot of optical start ups came into the picture suddenly with exorbitant valuations and a bubble was created. Only the fittest survived the bust.

Currently, the market is very much matured globally. No new companies are coming in optical space so i don’t forsee any signs of bubble here

Disclosure: Invested from 80s level. Adding more to the position. This is not a recommendation

3 Likes

Doesn’t matter what the buy price was, it had been averaged and could have been a good thesis at this price point (throwing good money after bad). But I decided not to stick around. In the current scenario I see many good opportunities than a risky, cyclical bet like this.

Lots of big established players already.

I follow the Sterlite thread and there is doom and gloom about fibre optics (just the mileage aspect at least).

Even BharatNet is a bit of a mess. So phase 2 is being re-structured. I do not see much money left in telecom. It has been a disaster, seen my friends laid off over the past few years.

Yes, it will probably will not go any lower. And if my luck/stock selection is the usual then perhaps may bounce even. ![]()

3 Likes