I dont think that there is discrepancy in the audio call and the transcript. I have gone through the Audio Call which was about 80 minutes and glanced through the transcript. the transcript is 27 pages long and not 18 pages. Can you please confirm which point is missing?

While this comes as no comfort to the share price, it does come as some comfort to me as a shareholder in that the possibility of fraud is ruled out, as also the possibility that Tejas’ payment was withheld due to some issues with their product.

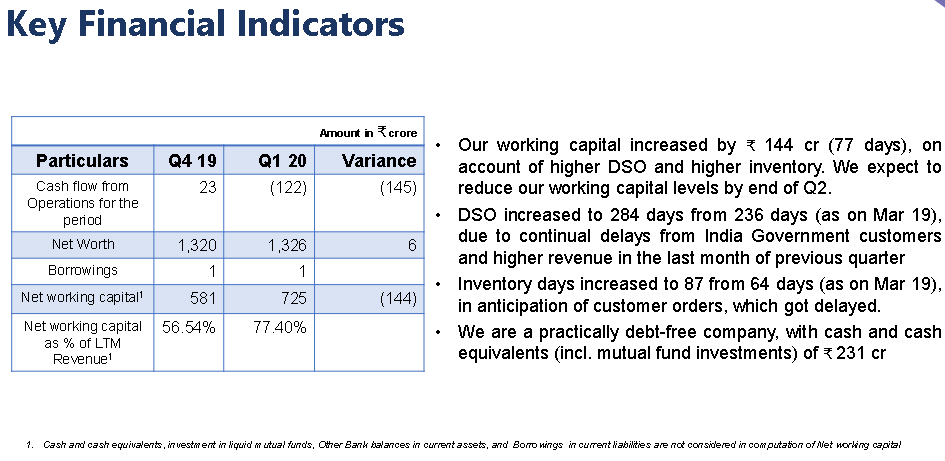

- Q1FY20 profit tumbled by 87% to Rs 5.77 crore compared to Rs 45 crore for Q1FY19.

- Total revenue also declined by 32% to Rs 162 crore.

- EBTIDA fell by 61% YOY.

- OPM contracted to 4.2% in Q1FY20 from 19.5% in Q1FY19. A fall of nearly 78%.

Stock hit lower circuit yesterday & tumbled 15% so far today.

All this mayhem happened due to deferment of spending on government projects, as government business accounted for 15% of the total revenue. To de-risk the business, they now aim to increase international revenue contribution to at least 50% of total revenues in medium term.

Disc. On Watchlist.

Reducing dependence on government is the right move (from 55% in FY18 to 15% in FY19) but the challenge is going to be increasing Private India Sales along with International sales…

If BSNL capitalization gets further delayed, the problems can get heigtened.

Bias: Interested and tracking.

There was a block deal yesterday where some funds sold their holding and HDFC Mutual fund bought 30 lac shares.

The results are certainly disappointing. The international business especially from USA is the hope because company stopped OEM based revenues in favor of direct sales. That had an impact on international revenue. On top of that, in last quarter, the government based revenue also stopped. Going forward, if they can increase sales in US successfully then that would reduce reliance on the government orders which are always lumpy.

FY19 AGM Notes

Chairman’s Address:

- Maiden dividend declared

- India Data usage to show 2x growth YoY

- De-risk the biz model by increasing the sales contribution from International to 50% of overall revenues

- Total Addressable Market: USD 18 billion

CEO Address:

- Walked through their Investor Presentation Slide deck

- 100% YoY growth in data consumption for next 3-5 years in India

- Cell Tower growth to be 10x of current levels.

- Fixed broadband access to increase from 20 Million to 100 Million mainly driven by Small and Medium Business (SMB’s).

- Most important competitive advantage is the software IP since the conribution of S/w in the final equipment is of magnitude difference compared to 20 years ago where h/w contribution was dominant

- Tejas Software-defined solutions provides flexibility and scalability to the customer and reducing their capex intensity.

- Core+Metro: TJ1600, Access: TJ1400

- Requested us to have a look at their products which were showcased during the AGM

- International business contribution increased from 13% to 19% with 70% YoY Growth.

- Reduce dependency on Indian Govt orders

- 475,000+ Deployments/Installed base

- The GPON device released 3 years back was the most advanced among its peers and remains competitive even today

- Best Access+Aggregation portfolio

- Their go-to customer approach is to showcase how their differentiated products are the best solution for their requirements.

- Mention of their alienwave/dwdm solution being best in the market.

CFO Address:

- R&D (gross): 13% of sales (P&L + B/S)

- R&D (net): 5.8% of sales (P&L)

- Guidance on Operating Cost: Will maintain around 14-15%

- Operating Costs are quasi-fixed mainly due to manpower for R&D and Sales.

- R&D expenses: 23% 3year CAGR

- S&M expenses: 13% 3year CAGR

- No collection risk on receivables of BharatNet Project due to demarcation of the funds.

- 25+ Tier 1 customers

- Mgmt continues to be confident that they will get additional BharatNet orders in the future as well.

- Cash and Bank Balances: 106 crores

- Deposit with Financial Institutions: 160 crores

- Investments: 86 crores

Shareholder Queries:

- Patent Valuation - They do not see patents as something which they would want to sell. The intention is to showcase them as a competitive advantage and evidence of company’s innovation ability to their customer base. Moreover Valuation of Patents is complicated. They will consider the possibility of highlighting it as a non-Ind AS measure. 350 Patents filed (288 semiconductor IPs) but 107 granted.

- Use of surplus cash for buyback: Not useful since it is immaterial to the intrinsic value of the business. Better served by having the cash in hand to fund business growth.

- Average time of execution of the order book and composition of the order book: Majority of the order book is Indian Govt related which typically takes 24 months (40% current fiscal and 60% next fiscal). International orders typically range from 6 to 16 weeks.

- How much of the 475000+ Installed base were retained or churned? None.

- Average Customer Retention Ratio over last 10 years: Typical industry average is 7 to 10 years while Tejas have been able to maintain and grow their existing customer relationships over last 15 years.

- None of the competitors have launched a similar product to their Ultra-converged access product launched in Mobile World Congress in Barcelona which Tejas has claimed to be world’s 1st.

Some unanswered queries of mine:

How many Tier 1 customers were there 3yr, 5yr, 10yr and 15yr back?

How confident and ready are they to face patent litigation challenges in future? Why have we not faced any patent litigation so far?

Other Observation:

Overall management remained upbeat and did not seem overly concerned about the poor Q1FY20 results.

Was my first AGM ever. Any discrepancies with the actual statements are my mistake.

Others who attended, please free to add or correct where necessary.

Disc: Invested and added further on Friday. Not a buy/sell recommendation. Not registered with SEBI. Please do ur own due diligence.

Investor Presentation - Q1 FY20

https://www.bseindia.com/xml-data/corpfiling/AttachLive/122ceedd-8054-4ef0-9e45-eccf70ceac39.pdf

9 Likes

Thanks for the detailed AGM info crazymama.

Price has dropped drastically for this stock recently. Is there something I am missing here? Book value which is mostly cash + receivables is only so much higher than the market cap and the company is debt free.

Is the market thinking that the company will not be able to get the receivables & discounting it? Management seems good in terms of profile of people & the quality of the annual report. Not sure why the market is punishing it so much for a bad quarter.

Welcome to ValuePickr forum, @alexander

Apart from the receivables issue, the drop in revenues from Govt is causing additional worry. For me it is actually a positive and provides additional incentive for the mgmt to put more focus on growing their International - Direct revenues.

Maybe Mr. Market thinks the company will not be able to scale up the international biz sufficiently this year to offset the loss of revenue from Govt. Of course there is the added anxiety of policy mistakes leading to a policy paralysis (akin to UPA2) which has got the market worried. Either ways I think IMHO it is a temporary problem assuming the company maintains the momentum in International segment growth.

https://twitter.com/CNBCTV18News/status/1154261259547582464

2 Likes

Business and all is okay but are you not concerned about the fact and the way employees were selling shares since last 3 months…

I mean…I know employees can do it whenever they want but it all seems fishy when this selling is just before fall…that too a big one

1 Like

Fiber Optic Network Solutions sector is one of the brutally competitive spaces.

US company Infinera , used to trade at $10 per share dropped all the way down to $3. This has been symptomatic of this sector’s wealth destruction.

Ciena is the leader in this space and doing well. Rest of the names go thru high competition not only from multinational US European companies but also from Chinese names as well. Given this back drop, why would a name like Tejas Network do spectacular is way beyond comprehension. It’s a waste of time to even track this and it’s a joke (btw knowing this sector competition backdrop, I still thought earlier that an Indian solution provider is something to be proud about and local players will support a desi company to sustainable levels, but I have been proven wrong)

4 Likes

I can think of one possibility.

Employees have much longer term vision and higher conviction than average investors about the capability of its Employer. Suppose they know that the future is bright. And they also are aware of the Govt deferment (insider info) and possibly assumed that market will react significantly (as it often does with smaller companies with fewer reputations). I wouldn’t blame them if they see this as an opportunity to sell at higher price and buy back at a lesser price. In fact, market became more suspicious because of this activity and fell more strongly.

If my hypothesis is true, we shall see the same employees buying shares before a quarter when the situation normalizes.

Disc. Tracking

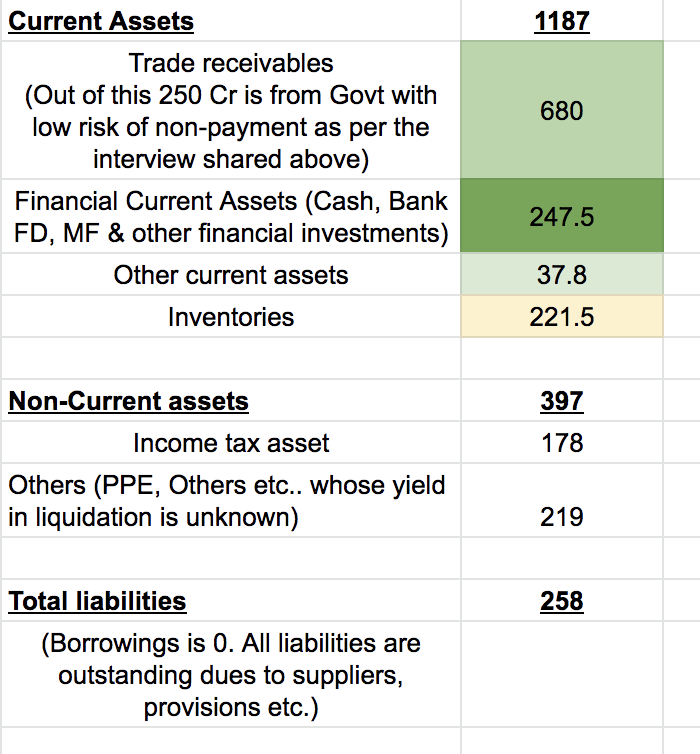

What you are saying maybe true. But below are the numbers as they stand and they make a compelling case for further investment in my view.

Current Market Cap of Tejas = 775 Cr

Trade receivables + Financial current assets - Total liabilities = 707 Cr

The company has no pressure of going bankrupt & is consistently profitable. No debt to speak of.

Below is the summary of the balance sheet -

Link to the full balance sheet - https://www.tejasnetworks.com/main-control/download/Consolidated%20Ind%20AS%20financials-2019-2020-Q1.pdf

Disclaimer - I have invested in this already at a higher price & now considering further investment due to this fall

1 Like

Valid question. But my thoughts are more in line with Sujay’s.

If you analyze the Insider Trading the employees have been selling since July 2017.

- There are overall 466 disposal transactions from 70 employees.

- Out of 70, only 5 employees (including 1 KMP) disposed of their entire holding.

- While 4 employees had also acquired shares.

- This is offset by the promoters and chairman buying significant quantity during the Feb drawdown.

- Prima Facie, it would seem the employees are cashing in on their vested options. Reasons can be many. Would be fruitless to speculate.

It comes down to how much weightage one gives to this point among many others for and against investing in this company.

My own view is that lots of employees (especially engineers) are generally not keeping in mind the big picture/business prospects. I know the type of people Tejas mostly hires - good E&C engineers focused on tech but not on business (they used to come to my college for campus placement). Hence not giving a lot of weight to employees cashing their ESOPs at whatever price.

I would give weightage to the senior folks who bought the stock. Looks like the CFO bought Rs 69L worth of stock at Rs. 169. Now, he is someone who would understand the business a lot better. He is an ex-Infosys guy & an IT industry veteran

Any other strong negatives I am missing apart from below?

- High receivables (primarily due to BSNL)

- Bad quarter (Government not spending due to elections)

- Employees selling stocks a lot (unknown reasons)

- International expansion is tough (due to competition & lack of strong brand name)

- High dependence on government especially Bharatnet spending which is lumpy

Locally, the company faces competition from Chinese players like Huawei. They give really high discounts for some products to strategically win orders which involves many products. It works for them because their portfolio is very wide.

Government business is lumpy and private capex hasnt picked up properly yet.

Internationally, Tejas used to earn good amount of revenue from OEMs but last year company decided to stop selling through OEM route and started selling with it’s own brand name. This resulted in drop on international revenues. Market is probably worried about uncertainty around this. However, I personally think this is a good step and can improve profitability in long run. In the USA, Indian companies have some advantage over chinese players because of recent woes around security.

Many employees who receive ESOPs sell them immediately and cash in. In previous correction when stock price had corrected to around 120 rs, the chairman and some more top members had bought significant amount of shares from the open market. This is around February this year which is not much far.

Disclosure

Invested and bought more on Friday

5 Likes

Agree with you their products are not comparable to Huawei and others who offer better solutions at competitive price.

Wonder what is the commercial viability of their patents. These patents may justly be marketing gimmicks nothing more. They are worthless unless they give some competitive or price advantage.

Exactly this is the main thing I am not able to understand. Promoters instead of buying in February (when they already know that this quarter is bad) could have done it later … I mean do they want to support stock price by showing their intent or they wanted retailers to buy seeing promoter buy…

They can definitely buy at lot cheaper as they say even next quarter they are not expecting government business.

I think they read the market reaction wrongly. Sanjay Nayak in every interview tells the market to not evaluate them on Q-o-Q basis but look at the financials yearly. They might have thought that the market would agree with them (?). Even on the investor day in May, they highlighted the same thing. So they were probably not expecting such a negative reaction from the market in my opinion. If you look at their sales before IPO also, it is similar due to dependence on government.

I think it is a good company run by people with high pedigree & even if it doesn’t become a multibagger due to lots of competition, it will not end up bankrupt / lose more value due to fraud etc. I am going to accumulate more on Monday.

1 Like

Apparently HDFC mutual fund has picked up a stake @ Rs ~84

1 Like