Any impact on book value if they lose this case? CMP is below the book value.

I think management indicated max impact of 31 cr in one of the earnings call if they lose.

Still not able to fathom low valuation of this R&D based tech product company with PE<10 where even a shrimp company trades at valuation of 1.5 times Tejas.

Dont you think 134 debtor days is very high?. Also, 0 dividend and very low tax ( This may be ignoble though. They may have got some tax exemption.)

Let me write some off topic. About 10 years I visited them to attend an interview. The hr guy asked me to wait for a few mins as the interviewer was busy. After that nobody spoke to me. They didn’t even offer water. I waited for about 3 hour. He then comes and tells he will call me some other day. He didn’t even apologize. I never heard from them again. I dont know if this was a one off.

BSNL fails to pay its employees; and BSNL is the organization from which Tejas Networks dues are high.

Cannot see a good reason for receivables coming down this Quarter.

Could somebody here elucidate the bear case for this stock? Aside from the current non repayment issues with BSNL, is anything else wrong with the stock?

1 Like

Two cents.

Company is heavily dependent on Government orders. Bharat Net had significant contribution to initial growth of 2017. This is one risk in case government orders stop coming in or dry out. Then there are other issues which comes with this reliance on gov orders like delays in orders (thats why they missed guidance for two years in row), delay in payments (higher working capital), politics etc.

Policies of current administration have been very favorable to smaller players like Tejas and it is reflected in the fact that 8 out 10 bids for some smart cities have products of Tejas. That is, the private bidders have chosen products of Tejas as part of their bids. This is partly because of policies favoring Indian small players and Make In India campaign of current administration. One risk is that if the administration changes after the elections these policies might change and favor multinationals ( personally, I wish that doesn’t happen  )

)

Other risk is that for some products, competitors of Tejas Networks are chinese giants like Huawei which can give tough competition to Tejas. I remember reading a management interview recently where the CEO said that bigger giant companies are giving away some products at extremely cheap prices as part of their larger overall strategy to get orders from private telecos. These giants have products and offering range which is much bigger and wider than that of Tejas and therefore they are strategically selling some products at very low prices and according to management these products are competitors to Tejas which can affect their top line. The CEO also mentioned that these giants are lobbying strongly and many state/departmental government policies are created unfair to smaller players like them in spite of strong measures from Central Gov.

This was mentioned in an interview. and other way to interpret this is that management might be chickening out from the guidance that they have been giving about catching up on 20% CAGR. For two years that management missed 20% growth guidance, they have been saying that orders are simply delayed and they will catch up on the guidance, so they maintain their earlier guidance. With such negative comments I am concerned about it.

Having said that, they seem to have better products technically and it would be interesting to see whether that fructifies into big orders from private telecos. Private capex in telecom industry is also expected after recent consolidation and it would be a big success for Tejas if they can get an entry into big customers. Another trigger could be from USA where they have started marketing products under their own brands. Earlier they were manufacturing for other companies. This shift had a negative impact on their top line and it is understandable. However, if they can get enough customers on their own then it would be advantageous for the company. Also, they have some advantage over Chinese counter parts in USA because recent bans on Chinese hardware.

Coming year should give much better clarity about the company so need to monitor next few quarters closely.

Disc:

Invested

7 Likes

Have u observed management purchased shares from open market in month of FEB. MD CFO and director purchased the shares.

that may be a positive sign.

Anyway this quarter results will be announced on monday. Lets see what the management says

Yes, management bought significant amount from lows. But at the same time many employees have been selling their shares in open market consistently.

This quarters result should be really good if we go by their guidance. Let’s see how it comes

1 Like

Results has been declared today. Overall it seems ok.

One point is bothering me. Receivables increased from 257 cr to 600 cr yoy. Any view on this?? Is it a red flag which can be serious or a normal thing in government projects??

On first look, the results seem to be good.

It is good that their direct international business is showing growth. Winning few big clients can also be very big for the company. I am excited about USA especially. It is also good that management is focused on reducing the reliance on government and PSUs.

About high receivables, I think it is not a big risk as they are mostly from Government and BharatNet where delay is expected, understandable but risk of non payment is low. We have to accept that this the nature of their business. Clients and orders are few and big and that can result in such delays on revenue front as well as payments front. I would be curious to know how they did in domestic private telecom sector.

Disc.

Invested

2 Likes

I am not so sure that the large receivables were ‘expected’ or ‘acceptable’. This is because the management had during the last quarter stated that the bump up in receivables should be resolved soon as the Bharat Net payments historically have been paid without much delay. So the question then was - why the delay now.

Now we see that the number has increased further. What worries me is that there was a news report in ET in which a high ranking govt official had stated that the Bharat Net roll out was delayed due to issues with one of the Vendors (Tejas), which the company has refuted. So am worried that the payments are not heldback/disputed because of the ‘issues’ mentioned by the official. So we need to ask the management about it.

1 Like

As far as products go, Tejas Network is not offering the complete bouquet of products. It is offering just a part of product / requirement and that’s the reason users prefer company like Huawei as it offers better range quality and is a better brand although a but expensive. With whatever information I could get from one of the users (he is in sify) tejas is a mediocre firm. It’s not a preferred vendor and will never be in near future.

1 Like

First of all, let me admit that based on the last 2-3 quarters, Tejas is a not an easy company to own! I was unable to join their conference call today, and if anyone did, could they kindly summarize the key points for us please?

Results:

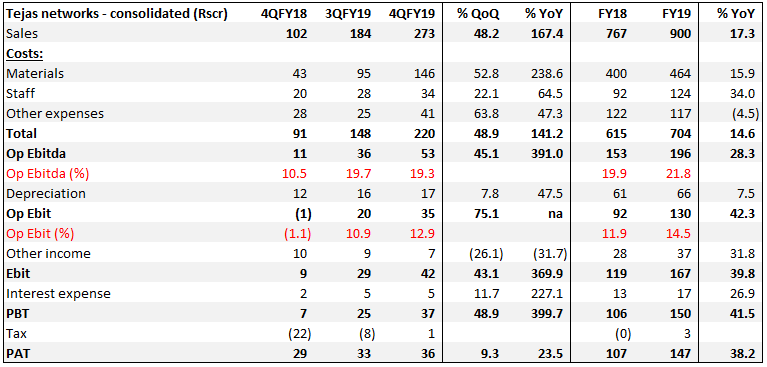

Tejas has missed its full year revenue target of 20% growth, as actual growth was 17.3% YoY. It however did manage to perform well on the margin front with Op Ebitda margin at 21.8% vs. 19.9% in FY18. PBT rose 41.5% YoY and PAT by 38.2% YoY. Since the Company management insists that Tejas is NOT a quarterly analysis type of the company, will not meander on those results here.

The biggest disappointment, despite the stellar results, has been on the debtor front, with receivables at an high of Rs622 cr (~70% of the operating revenues of the Company). This is not a defensible or acceptable number. Some course correction on this front is clearly needed.

The worst case assessment of this would be that the Company’s sales number is not genuine. However, this would not be fair given that the company has identified the party from whom a significant portion of this debt is pending. Also, while not a guarantee by any stretch, the presence of industry veterans on the Tejas board gives me some comfort that the sales number is genuine.

Coming to whether BSNL is ‘punishing’ Tejas for the alleged delays caused by their product. This may be possible, but even then it is unlikely that BSNL will simply not pay the firm. It is also entirely possible that Tejas has been an easy scapegoat for some government official to pin his inefficiency on for the delay in BharatNet. In either scenario, can a case be made for Rs600 crores worth of debtors going bad? It is possible, but is it likely? It is my guess that it is not.

While I do not have access to customers interpretation of Tejas products, I think its a bit harsh to call them mediocre. A mediocre product would not command a better than industry standard gross margin, or an improving trend in Ebitda margins (from 18% in FY15 to 22% in FY19). The product itself works on standards, so no company can come up with a totally unique offering in any case. Its successful foray in the international market also supports that at least Tejas is offering a standard product, if not a better one. Of course, the base assumption underlying this is that the financials are believable! Additionally I believe the government will continue to prefer Tejas as the Indian vendor to its products, versus buying from Huawei which would have security concerns, and political concerns.

So the key question to ask is, are these hurdles temporary, teething problems faced by any true technology driven company, or are they unfixable. For example, if Tejas were to announce next month, that it has recovered Rs600 crores from its debtors, would people view this company in a favorable light?

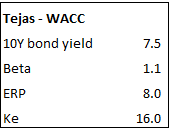

Now how does one value this Company? Tejas has Rs370cr in cash on books, indicating that the net of cash Mcap is Rs1290cr. Assuming a 20% PAT growth for FY20 (3Y PAT Cagr has been 72%), Net Mcap is trading at 7x PE. EV/Ebitda is about 5-6x (assuming 20% revenue growth, 20% Ebitda margin). So the valuations appear to reflect these justified concerns to an extent.

Now let us look at it from another perspective. Lets assume that, the steady state Ebitda for the business is Rs171cr (average of last 3 years Ebitda). The cost of Capital for the business (or required return is 16% (Tejas is net cash, so cost of equity is cost of capital):

Note I have taken Tejas Beta from this link: https://www.edelweiss.in/quotes/equity/tejas-networks-ltd-35619

Therefore, the value of its steady state business is (171/16%) = Rs1070cr. Hence, the PVGO (present value of growth opportunities) implied by its Market Capitalisation is Rs 1290 - 1070 = Rs220 crores. (if I were to assume Ke is 20%, this number would be Rs435 crore).

Now the question to be asked to self is this, “Does Rs200-400 crore fairly reflect the value of the telecom opportunity runway, that lies in front of Tejas over the next several years?”

For perspectives sake, let me highlight that Rs200cr is roughly a quarter’s revenue for Tejas.

This is just my 2 cents. I own Tejas, so I may be biased and everyone should do their own research. And finally, all this is academic, the real boss is the market, and if tomorrow Tejas is down 20%, that is the only value that matters! ![]()

Again, please do put the conference call salient points, or the transcript if possible.

7 Likes

I read bit of BharatNet-I and it looks like things are not very good. You can look it up here, here, here, here and here. It does look like BSNL/BBNL are looking for a scapegoat and Tejas Networks has already been blamed. With senior officials responsible for the project transferred by DoT due to delays, the receivables IMHO look dicey. How dicey - you can assign a probability and discount it.

If I were to value this company, I will do it this way. This company has had long DSO - around 240 days on average if you look back last 5 years. This has been mentioned in their DRHP as well. If you apply their cost of capital on the receivables, respecting the time value of money, you will have to reduce about 10% of 600 Cr receivables from their PAT which will bring their PAT down to about 90 Cr for FY19 (You can see what this can do to their margins, notionally). It is roughly about 15 P/E net of cash at this point which appears to be fair value. This is assuming they collect it completely, but after 240 odd days on average. If you take a pessimistic view and discount the receivables further, current levels are probably not attractive. This is just a rough mental model I use for discounting receivables and giving additional advantage to companies that have better cash conversion cycle, all else remaining same.

2 Likes

This is actually reassuring for me. I agree with you that Tejas may have been a victim of scapegoating by some babu. However, the transfer of officials suggests that the new officer at DoT has taken corrective actions by effecting transfers of such officials. Also, there is the practical aspect that even if we assume that Tejas may have had some part to play in the delays, the Indian government can hardly complete the Bharatnet project with chinese equipment. The political and security implications may outweigh any past delay concerns. The fact that Tejas has actually won more orders in Bharatnet Phase 2, and also from Indian defence services, is also comforting and supports the thesis that past delays were not due to Tejas. (as an aside, I wonder if Tejas can be looked at as a defence play as well. If Indian forces modernise, they are likely to pick and Indian technology partner or at least make it part of offset agreements).

I really liked the way you translated the higher debtor days to a cost number. If I may suggest a refinement, it would be this: The standard payment terms for a company would be 90 days (3 months). So let us assume that when Tejas prices its products, this 90 day period has been taken into consideration. In other words, if debtor days were 70-100 days or so, it would not have been a concern.

So the extra 160 days is the concern. So Rs622cr * 16% * 160/365 = Rs43cr is the hidden cost, and revised profit would be Rs104cr.

It is worth noting that this is a conservative number (ie cost on on the higher side,profit lower) for 2 reasons:

-

The funds that are caught up in debtors may have been made up by borrowing, and the current profit of Rs147cr already reflects this interest cost.

-

The average debtor days for Tejas has never been 90 days, but 160 days. In FY18 it was 134 days. Assuming that this was the level of debtor days that the market had priced in, the revised calculation of the implied cost of debtor days would be: (6220.16118/365) Rs32cr, and revised profit would be 115cr.

4 Likes

From Tejas’ recent conference call. As I suspected, they were trying to scapegoat the company, but dont seem to have succeeded.

Another interesting point, on how growing security concerns vs. Chinese players may help Tejas:

1 Like

How interesting. I missed the call so didnt realise. Is there anything that stood out during the call for you that is missing from the transcript? thanks.

I was listening to it in the background, after I had already made the decision to pass on the investment, so I wasn’t taking notes nor really paying much attention. Stock Adda has a 1.5 hour recording that I plan to listen to sometime: https://www.stockadda.com/concalls/viewmedia/1429-tejas-networks.

1 Like