Mirae AMC and Aditya Birla AMC are meeting Tejas management next week. Looks like fund houses are waking up to the potential of this company…(after one good quarter… ![]() )

)

US Rip & Replace program will benefit Tejas Network in the coming years!

It says “After getting initial partial funding, telecoms companies face deadlines to remove, replace, and dispose all Huawei and ZTE communications equipment and services ranging from May 29, to Feb. 4, 2025, the FCC said.”

Tejas Networks

Proxy to: Telecom, Data Centres, AI, Utility, Infra, BFSI, Defence, Railways & Metro, etc.

Through Saankhya Labs, they have secured approval under the Semiconductor DLI scheme to develop a cuttingedge System-on-Chip (SoC) - a critical advancement in electronics, enabling the creation of powerful, efficient, and compact devices across a wide range of applications

Vessel Tracking Network, powered by Saankhya Labs’ award-winning SDR chipsets, signifies advancement in Indian coastal security and the safety of fishermen. With 2,500+ vessels already benefiting from its capabilities, there is an ongoing planned deployment of over 50,000 additional boats nationwide.

Over 60% of workforce is into R&D!

International Partnerships

FibreConnect partnered with Tejas to successfully deploy an end-to end optical network in Italy

Tejas signed a strategic partnership with Telecom Egypt to replicate the Bharatnet (Rural Broadband Project) and NKN (National Knowledge Network) projects in Egypt.

As a percentage of net revenues, the services expenses in FY 2024 decreased to 3.7% as compared to 9.5% in FY 2023.

As of March 31, 2024 they have filed for 446 patents of which 335 have been granted

Company has received 32.66Cr from the PLI scheme and total PLI accounted for stands at 156Cr

Majorly B2B, so quarterly fluctuation in numbers is normal

Order backlog of over 8200Cr in FY24 - Company expects to recognize revenue of around 93% within the next one year and the remaining thereafter.

Disc: Invested

Tejas Networks Mr. Arnob Roy attending the India-US Initiative on Critical and Emerging Technology (iCET) industry roundtable, including Ajit Doval National Security Advisor India & Jake Sullivan National Security Advisor USA

Seated besides him Rajesh Pankaj Rajesh Pankaj - Greater Philadelphia | Professional Profile | LinkedIn previously EVP InterDigital & ex Sr.Vp Qualcomm

The USAID is also being involved and helping with the funding for the development of 5G & ORAN

For list of participating entities refer below article

Also they have setup an office recently at IIT Madras Research Park as their entire core wireless team was from Midas Communications which was an incubator based out of IITM

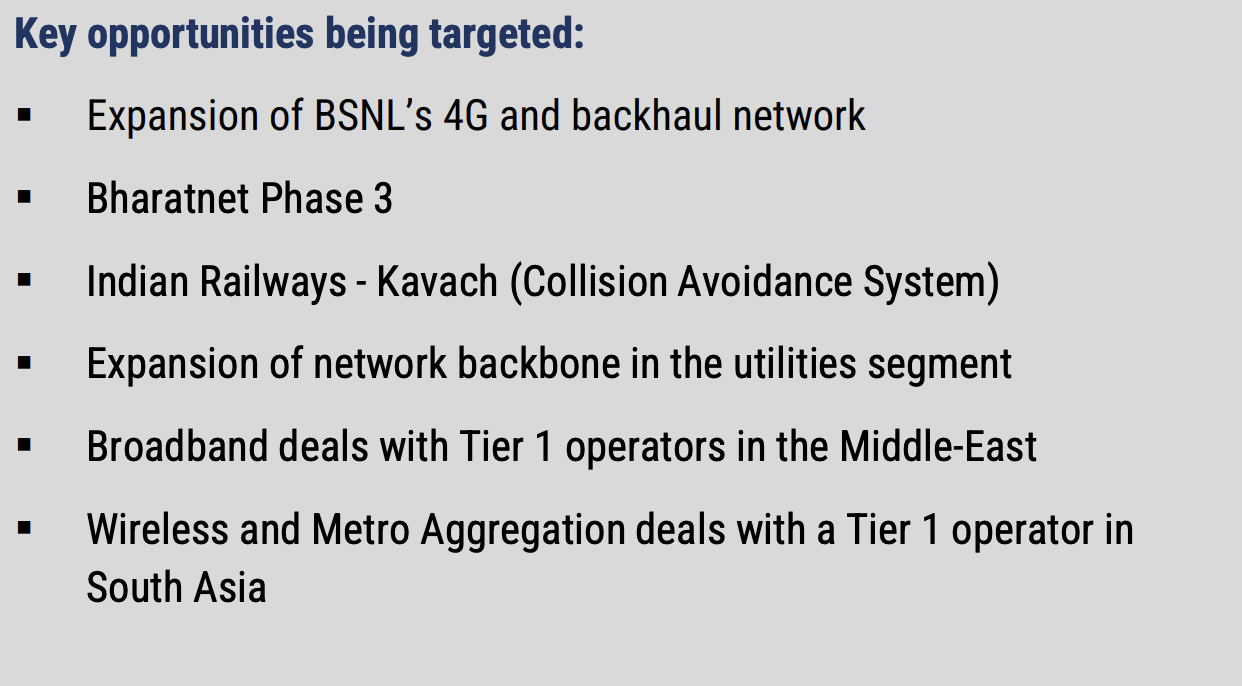

Also the BharatNet Project Phase 3 could be due in a month or two with some orders to trickle down further to Tejas

Tejas AGM video. They plan completing the TCS/BSNL order this fiscal year. They might also get a reasonable order out of Rs 65000 crore BharatNet phase-3 tender, and US Rip and Replace program will definitely benefit companies like Tejas.

They have added Kavach as an opportunity under their radar.

Indian Railways to roll out tender for 10,000 km of 'Kavach' - BusinessToday.

Looking at the contract of ₹280 crore for 260 km that HBL bagged in 2022, of which HBL’s work share is ₹206 crore, we can say that it will be a significant order. If Tejas wins the contract, their order book will also look impressive.

Q1FY25 Concall Notes:

- Best quarter ever.

- Order book 7091 Cr (6831 Domestic and 260 International)

- 2 business segments : Wireless and Wireline

- Wireless:

- 4G and 5G RAN installation for the BSNL.

- Significantly scaled up manufacturing capacity for the RAN equipment.

- The company has made releases for the additional equipment for the bands which are used globally - band 3(800MHz) , band5(850MHz), band41(2500MHz).

- Engaging with multiple players for POC.

- Wireline:

- Won a strategic deal with a tier-2 operator in the US.

- Got into a deal with a telecom operator in South East Asia for broadband operations.

- Getting repeat orders from the existing clients.

- The equipment which were delivered for BSNL order in the last quarter are under installation.

-

Previous quarter had PLI incentives (other income) of 156 Cr, compared to the current quarter 76 Cr.

-

EBIT for Q1FY25 is 167 Cr compared to 258 Cr in Q4FY25. But in Q4FY24 there was a big impact on other income (PLI, which was total of FY23 & FY24). If we remove that then EBIT for Q4FY24 is 101 Cr and Q1FY25 is 100.

-

Inventory and receivables increased due to ramp up in the shipment.

-

Borrowings have increased from 1744 Cr to 2844 Cr.

-

Generative AI, Data Centers, VR, AR, Gaming, Streaming etc. are key growth drivers for the expansion of the 4G-5G networks & broadband network, which is the area where Tejas operates.

-

BSNLs 5G tender for nation-wide build out is expected.

-

The upgrade from 4G to 5G for the existing site costs hardly any fraction, it is not a big jump as such. However, setting up a new 5G site costs higher than a 4G site.

-

The management avoided answering a question on the cost advantage that it may have over other players like Nokia, Ericsson etc. (which also have RnD and manufacturing centers in India). The similar question was asked by one other participant subsequently to which management said that a lot of the equipment manufactured by them are integrated equipment and hence results in the cost savings for the clients.

-

Doesn’t have a direct role in the data centers as such but it’s more of a high speed connectivity required for the data centers - Data Centers Interconnection.

-

The switches that the company manufactures find application in campus or buildings - that is enterprise level. It doesn’t have applications in the data center as such.

-

Significant opportunities in the US in terms of modernization of the existing networks and also network expansion in the rural areas.

-

The current order book of 7091 Cr is expected to be completed in FY25 (No guidance on the EBITDA margins as such).

-

The company works on the asset light model where majority of the manufacturing is outsourced to the EMS players and the company mainly focuses on assembly and testing.

-

There is no clear visibility of the order post FY25 (though management is saying that there is good demand and is bullish about the future and hence has done significant ramp up).

-

The wireline and wireless businesses have similar kinds of margins. The margins over the long term can increase as the contribution from the international business increases.

-

The overall tender for the Bharatnet Phase-3 could be somewhere around 4K to 5K Cr.

-

The WC intensity is likely to increase because of the execution of BSNL orders and thus the debt to service the WC is also likely to go up.

-

The international opportunities won’t be as big as BSNL, but the number of opportunities could be higher.

-

The number of sites that may need to be covered for Kavach is around 15K to 20K sites. This is overall size and not specific to Tejas.

-

The execution time for the BSNL 4G to 5G upgradation and the BharatNet (whenever it starts) would be around 18 to 24 months.

-

The initial size of the orders/opportunities for 5G network would be focused mainly on the metro cities, where the population is ready to pay higher for using that technology, but the orders would be relatively smaller. However, over the longer term the orders would be of bigger magnitude as more and more geography will be covered and also the cost of the equipment would be higher.

-

As per the management, there won’t be a big competition from the chinese companies doing JVs with Indian companies.

-

The company is putting more sales and marketing focus on the developed economies such as the US, however these are long dated cycles which usually take a lot of time and hence the company is going to focus on the Indian business in the meantime.

Some of the points to ponder upon are:

- There is no clear visibility of the growth post FY25. Though management has listed following optionalities, the quantum of these opportunities look relatively lower as compared to current BSNL order.

-

Optionality 1: The Kavach system. As per the management, this contract/order could be of 15K to 20K sites. If we compare this with the BSNL order then it is hardly 1/5th. Meaning it can translate into orders worth 2K to 3K Cr.

-

Optionality 2: The BharatNet Phase3: As per management the total equipment required for this could be somewhere in the range of 4K to 5K Cr. Also the chances are this tender could be allotted to more than 1 player.

Above both orders will have to be executed (if and when it comes) in 18 to 24 months. Thus revenue contribution from these orders would be not more than 2 to 3K per year.

Optionality 3: International business. The management has categorically said that these orders would be much lesser than the BSNL orders. There can be number of orders but the size would be relatively smaller.

Moreover, the company is currently doing POC with the international clients, which are long dated ones and hence it will take some time for the actual orders to come in.

The management has avoided commenting anything on the orders post FY26 and have also avoided commenting on the pipeline as well.

- Another concerning aspect is the increasing debt because of the stretched WC as they deliver more and more equipment for the BSNL. Already debt increased from 1744Cr to 2844Cr in a quarter and management has indicated that it will increase even more going forward.

Disc: Invested.

Well written summary of the con call. Thanks!

Management not commenting on orders post-FY26 should not be a matter of worry. They are a conservative management and do not make such long predictions about their business.

Regarding the ‘another concerning aspect’ of their working capital, ICRA has assigned the company a rating of A+ Stable for it. The company follows an asset light model of business, under which it is unavoidable to take short term loans for working capital during execution of large projects such as the BSNL 4G project. They explained it in the concall.

Disc: Invested

In both cases of Bharat net and Kavach profit margin will be higher compared to BSNL 4G. If revenue you mentioned comes true in those 2 opportunities then I will be more than happy for company to achieve more profit in these projects than BSNL 4G

Intel’s decision to cut 15% of its workforce could significantly impact its telecom business, particularly in the Open RAN segment, where key customers include Nokia, Ericsson, and Huawei. Intel dominates the chips market, holding a 99% share of all virtual RAN deployments as of early 2023. This workforce reduction could weaken Intel’s stronghold in the Open RAN market, valued at around $40 billion in 2023. This situation could create favorable opportunities for Tejas in the coming years.

https://www.lightreading.com/open-ran/an-intel-crisis-is-a-crisis-for-open-virtual-ran

Presentation for the investor/ analyst meet