Interview of Vijay Kedia on TEJAS networks

Love to hear from him on the opportunities 4G, 5G 6G and so on ………

https://twitter.com/cnbc_awaaz/status/1671392726531854338?s=46&t=MxMxfNuyq6s4fya08o2PwA

Interview of Vijay Kedia on TEJAS networks

Love to hear from him on the opportunities 4G, 5G 6G and so on ………

https://twitter.com/cnbc_awaaz/status/1671392726531854338?s=46&t=MxMxfNuyq6s4fya08o2PwA

Boost for Indian companies - tcs led Tejas networks

While result is below average, AGM had good foresight about what is likely ahead. Aim to be among top 5 Telecom OEMs means min market cap of 10 billion dollar in years ahead. 5G rollout will life many SMEs highly too like Frog cellsat, Kore digital , invested in all 3 for long term…

At 44th minute of the concall the management of Tejas networks replied about tie up with Renesas Japan for semiconductor sector.

They explained that they have increased inventory to complete the 4G deployment for BSNL on timely basis.

Th concall gives fair idea of future prospects.

Concall of Tejas networks ![]()

Many insights from management.

During the call, someone mentioned about the exchange filing by ITI about their share of advance purchase order of Rs 3889 Cr for 23,633 sites in the west zone. Attached is the relevant filing. They have mentioned that the purchase order will be issued by the BSNL circles. In the call, Tejas too mentioned that purchase orders will be issued by the respective BSNL circles and once they receive it, they will share it with the investors.

ITI filing.pdf (568.4 KB)

Disc: Largest holding

Would be interesting…!!

Now the time for execution of order

On a positive note - management has stressed on execution. Erstwhile leaders though stressing on delivery, used to fall short every other quarter, whether through their lack of vision or due to Acts of God, read as Covid, or SemiConductor shortage.

The luck factor on the side of the company, was that, it was not capital intensive - sometime ago they mentioned ~200 crs (per year?) was enough to meet operational expenses - so the receivables getting stuck was not a big negative.

About 2 years ago, recall how markets kept punishing the MCap due to BSNL dues not budging. This time around the bright spot is that, TCS is the customer who then collect from BSNL.

New Tata management would be keen to bring motions in order. And TCS is rich in cash. They should clear dues promptly. This is a national project where the Government is keen to show the technological prowess into next 25years of India’s growth. Plus, my belief is Tatas got a fair trade for taking AirIndia out of Governments books.

In ~1.5yrs, if 7K crores get executed then each quarter revenue should be ~1200 crores (7.5Kcr / 6Q ). Much higher than ~200crs per Q now.

Plus there’s ‘several thousand crores’ worth of maintenence beginning in 3Y and stretching to 9Y (3Y_fwd_9Y_bond). Plus 5G, as per management.

Failed to understand why the newscasters at CNBC interview above, didn’t do a rough calculation - but kept asking, management.

Edit: perversely my thoughts are that, this is a better EMS play than a pure route. Hoping for another few baggins-of-wealth. A few of us I know, held and added through a lot of pain - so this kind of seems like a reward.

TCS got contract for 15000 crores…out of that about 50% has come to Tejas for supply of equipment.

Tejas mngt in the last concall has said that they will be supplying equipment for ITI too…so out of ITI contract of 5000 crores, Tejas may get 2400 crores order for equipment.

That will take the total 4G equipment order to 10000 crores…if they execute this in next 6 quarters, then quarterly topline should be 1830 crores…of course the Q2 will be when there will be some starting troubles…but from Q3/Q4 onwards the pace of execution will pick up and the peak execution will be in 2024 as they will start upgrading to 5G…after that there may be some good international orders for 4G and 5G

Next 18 months may be exciting time for Tejas investors…

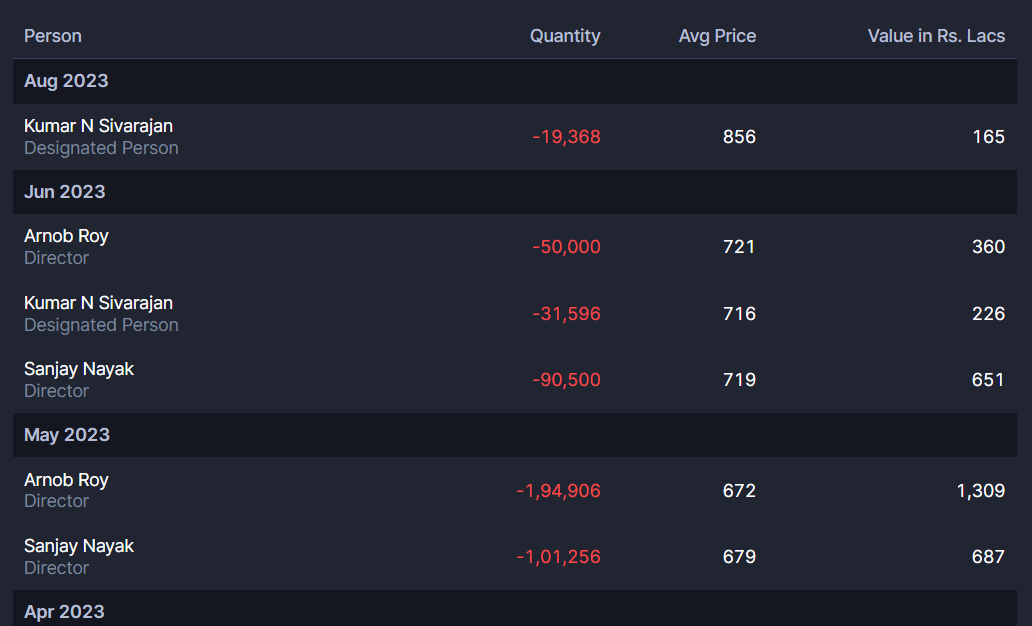

[New to Tejas Networks.]

The company’s Mcap is 14.3K cr.

and the order book seems close to 10k cr. ( 7500cr from tcs for bsnl + ~2400 that will come for ITI )

and this 7500 cr will be in the next 1.5years.

Now, my query is,

why are the kmp & director’s selling it all off?

there is an inventory buildup of 354 crs and recievables of 169 crs.

and anything regarding the dilution of equity done for 1500crs in 2 years?

edit* : inviting views, just the selling part seems a bit off since, kmp would want to hold onto even higher number of shares, they why are they selling so much that to month on month as the prices sore.

Despite BSNL order for next 18 months, Tejas is not cheap by any stretch of imagination. Don’t expect huge margins here.

By the way this level of selling is normal. They too are humans like us who need money.

There are 2 new opportunities which are not unfolded yet. First is semiconductor and 2nd is DDaS.

![]()

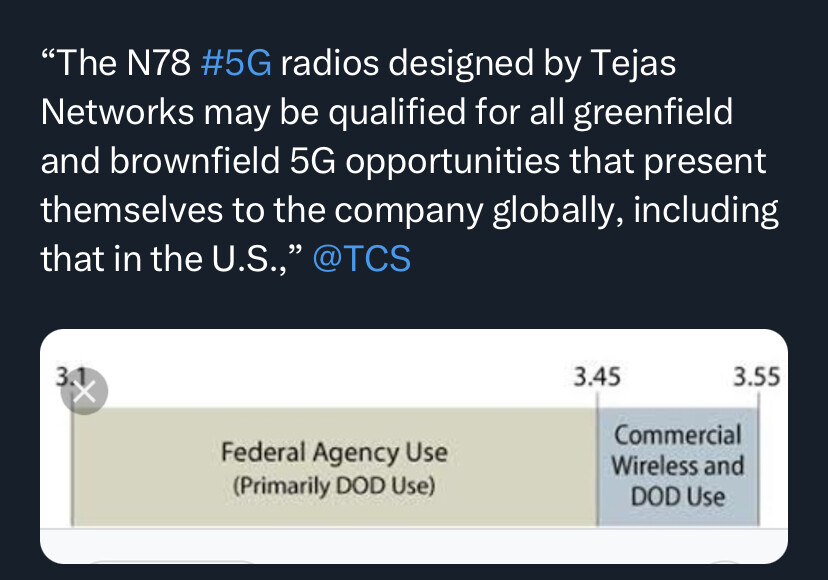

A very big opportunity could open up for Tejas Network due to recent Bharat 6G Alliance, Next G Alliance between US & India

Read more at:

Moreover the U.S. Rip & Replace program which started in 2020 is a very big opportunity for Indian Telecom Equipment co’s

Under this Program all the existing Chinese equipments from ZTE & Huawei are to be ripped apart & replaced with trusted equipment similar to what just happened in India.

Not just US even Europe is doing the same.

Although there are existing & established players like Ericsson & Nokia etc., but the cost of their equipments are quite high

As a result the $1.8bn Bugdet Set by the US govt. has already been breached to $5bn & the program has slowed down as service providers are unsure whether they will be able to get support from govt. or not.

Major issue is with the smaller ISP which Tejas is already targeting from few years

As these smaller ISPs cannot afford high cost equipment from the European Co’s

This is where opportunity for Indian Telecom Equip. co’s opens up

The cost of Indian equipment will be far lower than those of Nokia & Ericsson

Not to forget the New Ceo Mr.Anand Athreya is quite well versed with the US market having served with Juniper Electronics & the BSNL 4g project will be a testament to Tejas’s Capabilities.

US and Europe opportunities for TEJAS Networks

Telecom Minister says that now BSNL 4G work is launched only in 4 districts…it will be launched PAN India from Diwali…i.e 14th November onwards

So there wont be much impact of BSNL 4G order in Tejas Networks Q2 result…therefore, brace for lacklustre Q2 results…not so impressive numbers…and in case of very bad result…the price may go down to 780 once again

But long term prospects are very good. Implicit in the ministers speech is that there will be big export opportunities for Tejas in setting up 4g and 5g networks in other countries. The earstwhile Non Aligned countries would be a good market for Tejas 4G network.

Also the best performance of Tejas maybe from March 2024 onwards.

2021…2022…2023…thats like 3 years of consolidation…3 years of sideways price movement…for investors the reward will be backloaded…only in 2024 and 2025 when 1 lakh BSNL 4G towers are set up.

Till then shift your money elsewhere or sleep over your Tejas holdings till March 2025 and open your eyes to see Tejas @3000+

https://x.com/aigetoachq/status/1709504247489003699?t=dXyBxZaziuBkN359k0d4Xw&s=08

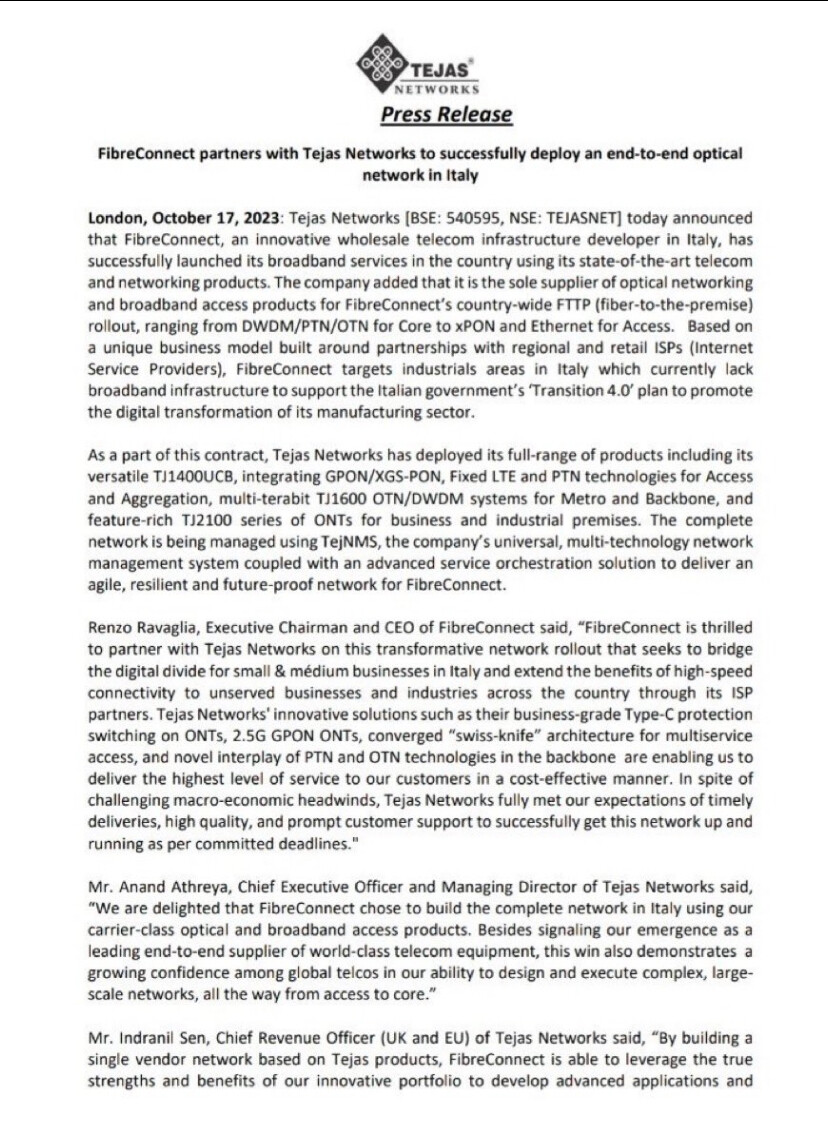

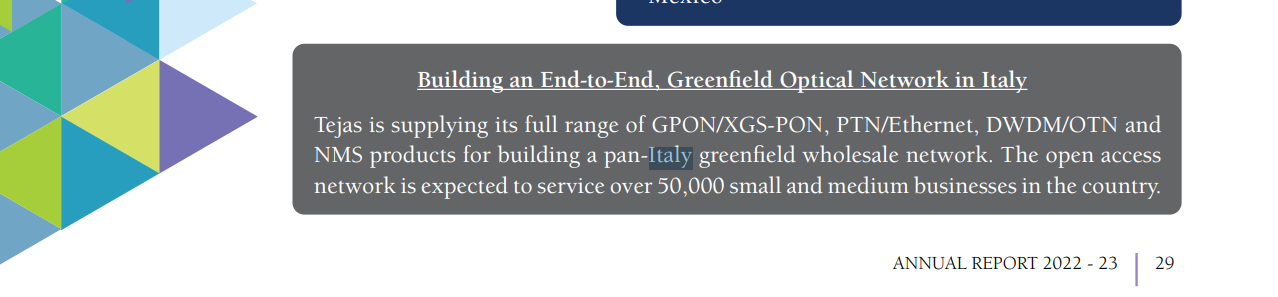

This is not a new order per my understanding by reading through the news. It’s to let the market know that Tejas has been successful in deploying the end to end equipment for Fiber-Connect. Market also though that this is a new order but i can see from reading the AR for 2023, it was mentioned (snip below) that Tejas is supplying the full range of equipment for network service provider based out of Italy. The market also realised that this is not a new order win and hence the intraday run up in share price got subsequently corrected.