The crux of the matter is to establish 3-4 things -

Quality of Tejas’s products vs competition like Huawei, Nokia, Ericsson, Ciena etc. Are the products completely non-starter or at least are they at par for latest - 1 generation products with cost advantages?

With Huawei forced to exit Indian and RoW markets, how much business can Tejas win realistically?

Given Macro tailwinds and most of the Telco stress getting sorted out, can implementation/fiberization pick up pace over next 3 years?

Understanding level of indigenous tech as claimed by JIO. Is JIO going to make optical products on its own?

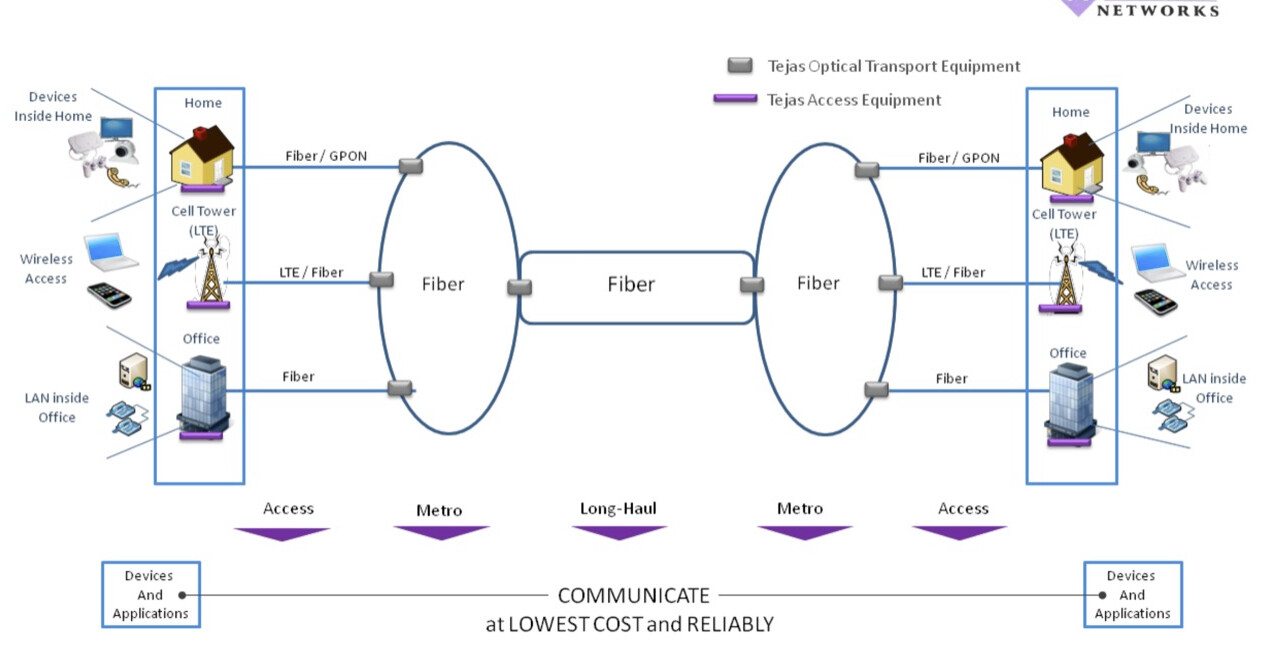

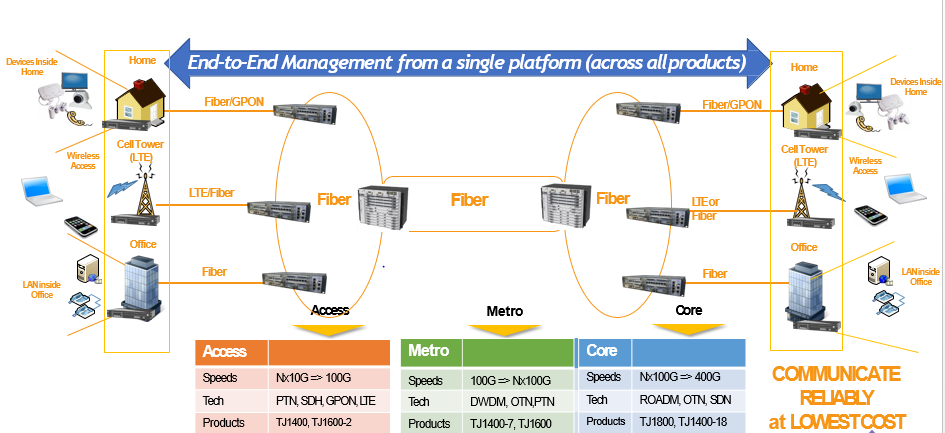

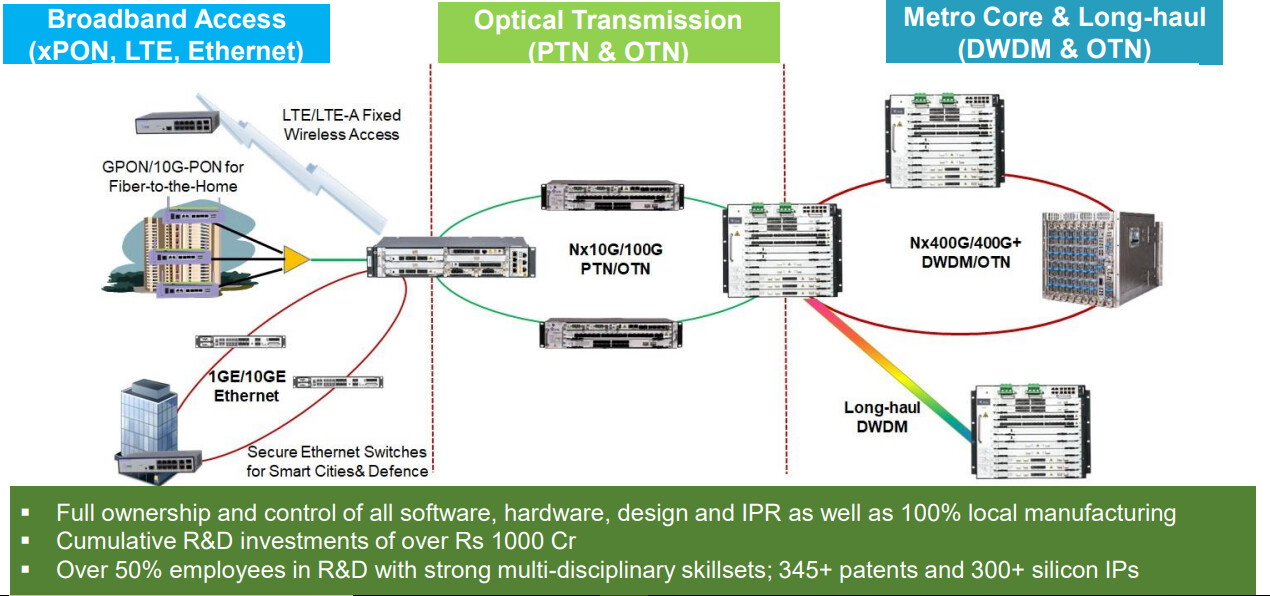

PRODUCTS

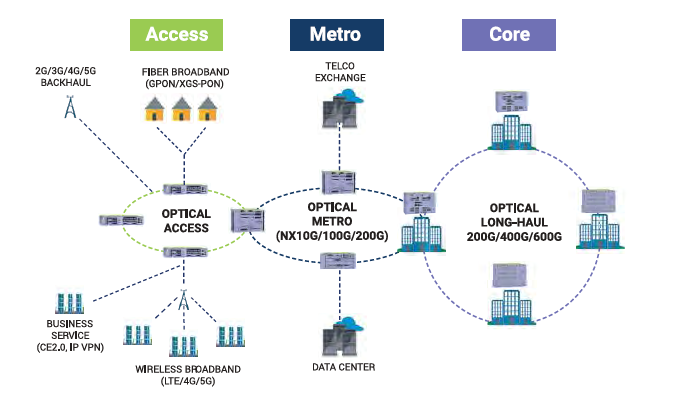

To put it simply - Tejas makes optical products (switches) that are used in networks. The products are broadly categorised into 3 categories -

Access (switches at the edge of the network where users access the network)

Metro (Backhaul capacity building)

Long Haul

Following simple diagram gives pictorial view of network and products -

FTTH: There are < 10mn households in India that have fibre to the home (FTTH) connections in the India. Some reports from DoT/TRAI project aggressive targets of 100mn households etc. in next 3 years. The capex spend for telcos per customer is around 20-30$ per connection. Even if 10mn FTTH connections are to be added, that opens market opportunity of 1500-2000 crore. Fibre ARPU is 600 Rs vs ~150 Rs for mobile data and hence it probably makes sense for Telcos to invest in FTTH. Also to use 4G/5G, you need devices that have modem to use 4G/5G. Many devices like smart TVs/Laptops do not have modem and Wi-Fi (with fibre connection to tower) remains the easiest way to consume data.

4G/5G: Only 20-25% of the towers in India have fibre in them, rest use the old copper/coaxial cables. With rising data consumption, old copper cables can not support increased bandwidth requirement. So these towers would need to move to fibre which presents an opportunity. In India, even 4G (LTE) itself has not been used to its potential and 4G itself would require massive fiberization.

5G technology is few years away in India as most telcos do not make enough money in 4G itself. As and when 5G comes, it will result in network densification e.g. to provide 5G coverage over same area 10x more towers than 4G will be needed. All these additional towers would require optical products. Also to support 5G products, backhaul speeds need to be increased multifold from 100G → 400G → 800G. So as and when 5G catches on, it will result in massive requirements of optical products.

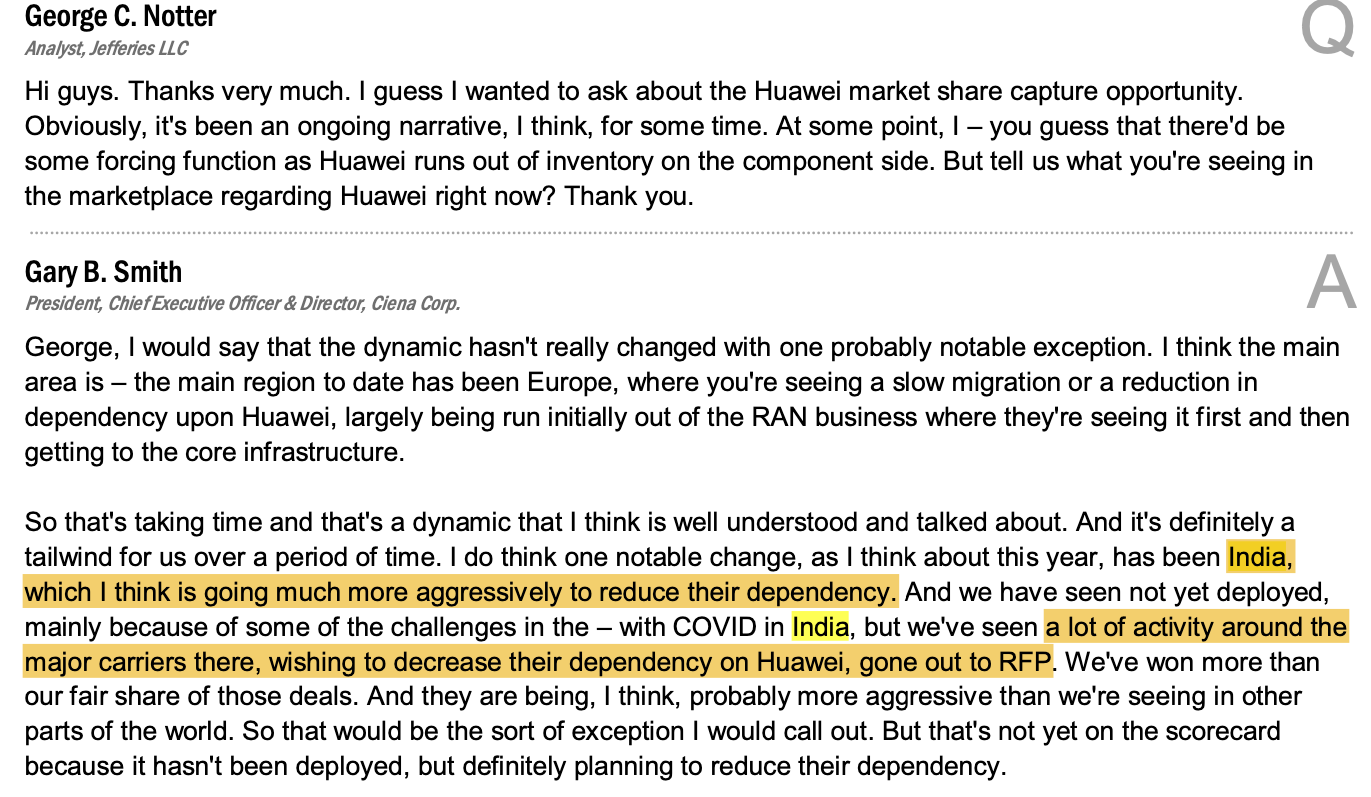

Huawei: This is probably more near term and most important potential tailwind. Huawei had 36% market share (As per Tejas DRHP) in the Indian optical network market and with all the issues with China, Huawei is forced to vacate the market. Can a decent chunk of this business come to Tejas?

Indian spending on optical equipment is projected to be 1bn$ per year. Even Ciena (world leader) talks about India in its conf calls and it is important parameter for them to deliver on growth guidance.

These are the things I really want to take to industry expert and start conversation.

A few things about Tejas business in itself -

It had large dependence on government (B2G) orders (BharatNet, RailTel etc.) for its revenues. Given the lumpy nature of these orders (+ Telco stress - AGR being latest one after JIO pricing war), Tejas really suffered in receivables and also in P&L in last 2 years. As investor, I can wish that they do not do the government business at all - but government business is what made Tejas to the company it is today. So, we will have to deal with it.

I do really hope that International reaches 50% of sales as per management’s ambition over next 3 years as it is better DSO and margin business. Also Telcos will start spending monies in a little bit more consistent fashion as no new shock (other than 5G auctions) is on horizon.

In terms of value addition/IP, the business in itself is much higher up in value chain (vs say Dixon/Ambers of the world) as company is designing its own chips.

If the tailwinds lifts the Tejas boat, the operating leverage can be quite strong as employee costs and R&D costs will not scale proportionately.

Order book of 680cr, growth in international business, products wins with Airtel/JIO are encouraging signs in recent past.

In this post, let me talk a little bit about company history and few issues -

Tejas was founded in year 2000 by 3 founders - Sanjay Nayak (CEO), Arnob Roy (COO) and Dr. Kumar Sivarajan (CTO).

History

2000-2005

Cumulative revenue > $20mn

First order from Tata power, helped build India’s first DWDM network in Mumbai

Executed RailTel’s first pan-India network

2006-2010

Cumulative revenue > 400mn$, 80K products shipped in 25+ countries

First wins with Airtel, Tata Comm, Power Grid, Oil India, GAIL

Executed first OEM agreement with Nortel

2011-2015

Cumulative revenue > $750mn, 250K products shipped in 50+ countries

Signed OEM contract with vendors from USA/Japan for packet-optical products

2016-2020

Cumulative revenue > $1bn, 500K products shipped in 75+ countries.

Selected for optical and broadband product supplies for world’s largest 4G network by subscribers (JIO)

The company has survived and thrived in last 2 decades. Government/PSU business have had a large role to play in the scale up of the company.

Winning Airtel in 2006-2010 and then Jio in 2020 shows that product quality is at least acceptable. Winning wallet share of Indian private customers is now next stage for India private business.

In DRHP, company had said that it has 15% market share in total Indian optical networking spends (diagram in first post). We need to understand the market share just in Indian private operators. As per same DRHP, Huawei had 36% market share (of total) and I think some part of this MS is up for grabs. What do Indian operators think of Tejas and its positioning (in terms of technology and pricing) w.r.t. other competitors like Ciena/Ericsson needs to be understood.

The company also tried the OEM business where it did some contract manufacturing for Nortel/Cienna till FY19. But in recent years, this business has gone to negligible levels.

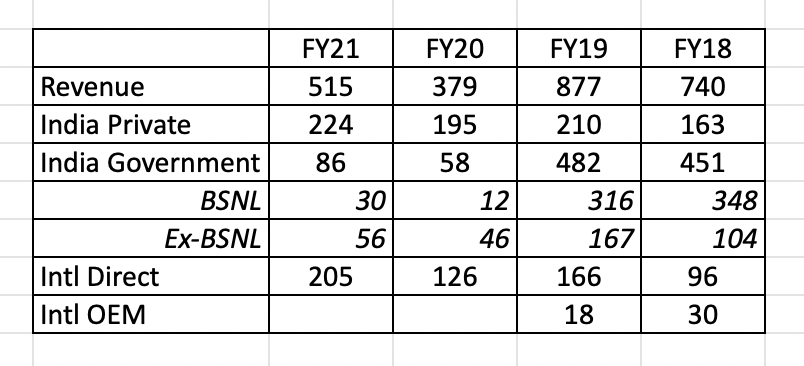

The company had sales of 900cr in FY19 and it fell to 391cr in FY20. This is largely because of India Government business falling from 55% share (495cr) to 15% share (59cr). This is because of election year and other delays at government level. In FY21, India private has remained at 17% of revenues but revenues have grown from 391cr to 527cr (growth driven by India private and International). I will write another post that shows revenue split between different segments.

Another issue has been that receivable days went up - 134 (FY19) → 252 (FY20) → 351 (FY21) primarily due to delay from BSNL and reduced revenue base vs. FY19. As of Q4 FY21, total outstanding from BSNL is 122cr (out of which 70cr is retention money).

There is possibility that India government business might come back strongly in FY22. When asked about receivable days for this potential business - following was management’s response in Q2 FY20 -

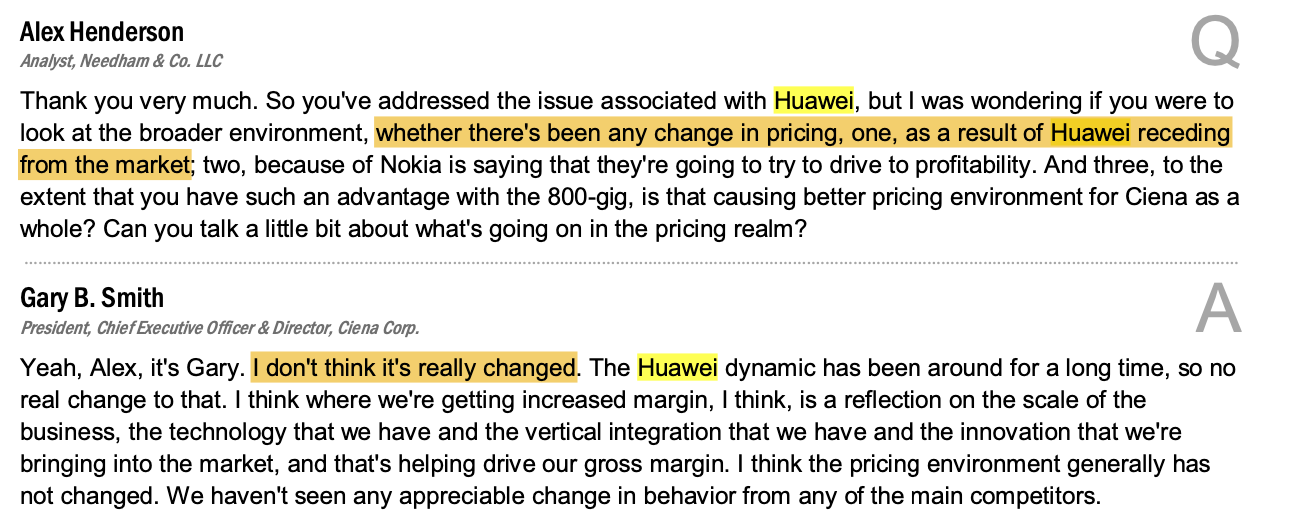

Quality of Tejas Products against Huwaei, Nokia, Ericsson, Cienna: At par with Huwaei and Cienna. For Cienna they used to do some contract manufacturing also. Nokia and Ericsson do not really compete with similar product offering.

Strength: I would say good R&D team, they hire from decent colleges and manage to get good talent because there are very few Core ECE jobs opportunities are there in India.

Cost Advantage: Apart from Cheap R&D, the products are made up of low cost ingredients. What i mean is the product would be designed using cheaper DD2 RAMs while everyone in the industry would be using costlier DDR3 RAMs. It doesn’t mean the quality is inferior, Tejas manages to tweak the built using codes. They work on FPGA platform which is reprogrammable and hence the tweaks can be improvised time and on.

Growth Opportunities: They did manage to win few deals in South East Asia and Africa through competitive bidding in 2012-16. If the Internet infra opens up in African region then the company can win further more orders.

What didn’t work: Company had invested decent amount of time and effort in few projects like Defense and EV batteries which never materialized during 2010-14 which led to de-growth. Between 2010-16 they managed to win very few orders

Huawei Exit and competition: The company has been pleading for preferential market access to Indian companies from a long time. If that happens it would be strong tailwind for sure. But Huawei offers complete network access unlike Tejas which predominantly operates in L2 (Switching). L3 is where routing happens is a more lucrative opportunity. But previously we have seen Telcos preferring companies with complete network access that is why Airtel preferred Huawei post 2010.

Expanding product portfolio with Innovation & R&D. ICICI Securities has ranked Tejas as a top-3 R&D spender (as a %age of annual revenues) amongst all publicly listed companies in India. Tejas is the only information technology company to make it to this top-10 list.

Just curious on a few things at the starting level. if you can help us understand better the capabilities/support available in deployed/current gen Tejas products

How is SDN (Software defined Networking) supported in all products - for remote operability and control?

How is ALOPS (Artificial intelligence based operations) supported in all products - for predicting failures, impact analysis and preventive maintenance automation?

How/What Open standards architecture for Hw and Sw are provided?

Scalable hardware supporting Open standards? Please elaborate

How existing products support Netconf open flow standards - router/switches configs

Support for ONAP supporting Orchestrator - for supporting Alops based deployment, configuration?

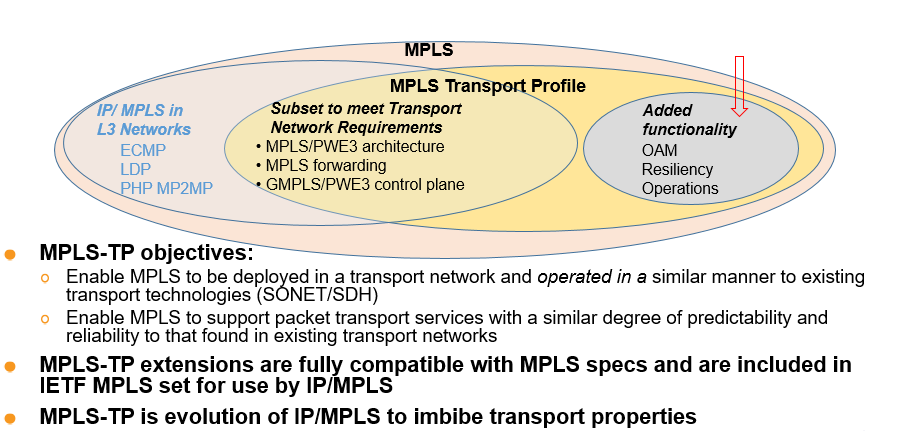

GMPLS based support in DWDM products - for switching paths on DWDM optical routes/ports/wavelength switching

India and major Indian operators are going aggressive on reducing dependence on Huawei. Cienna has won decent business, I hope Tejas also can gain some market share here.

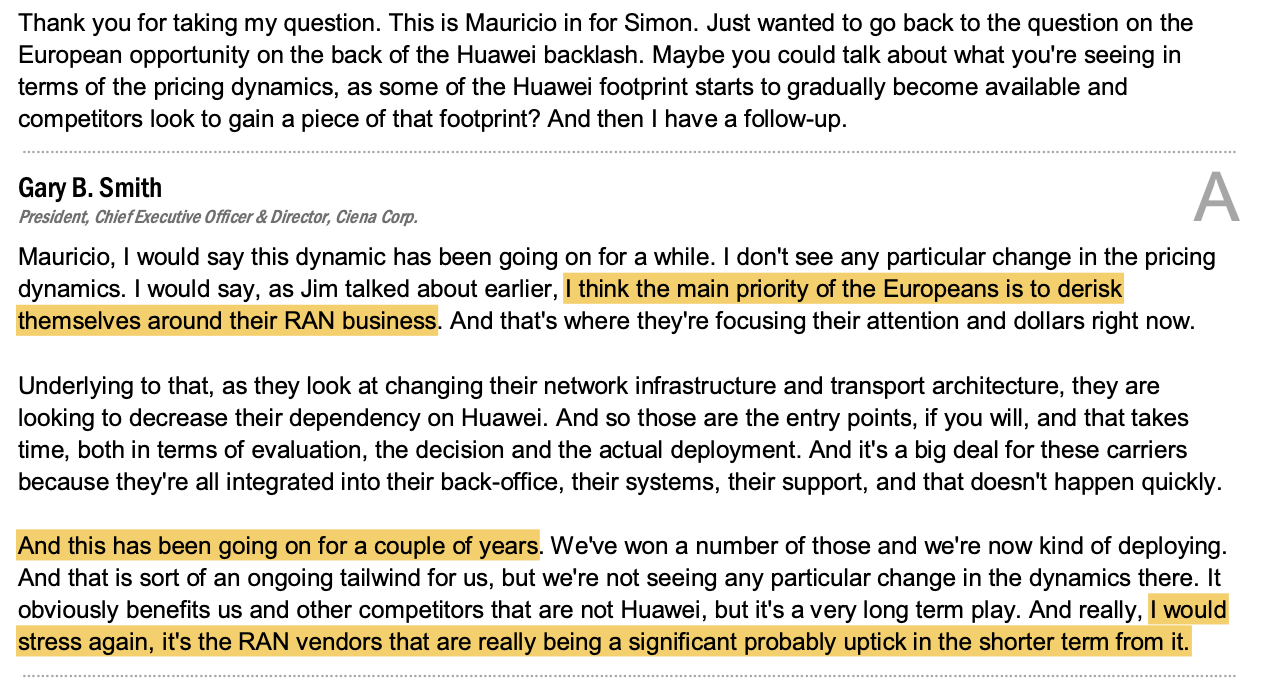

Tejas has talked about trying to focus more on Europe business and following para gives more context in terms of Europe and Huawei. In near term, RAN vendors would have business wins from Huawei and but over medium term optical vendors would also be able to win Huawei business.

As mentioned before, India government business fell off clip from 482cr in FY19 to 58cr in FY20.

It is good to see run rate of 200cr business with India private. With some order wins and Huawei exit, we need to see if this business can double in size in next 2-3 years.

International business has also reached the size of 200cr+ in FY21 and management expects this business to growth faster than other businesses to reach 50% of the revenue. International business has bettor DSO and better margins.

Company used to do International OEM business till FY19 but that business has gone to zero now. Scale up in International direct business is exciting.

The order book at the beginning of FY22 is ~680cr and management has guided that 50% will get executed in FY22. If I find the order book split in above segments, I will update.

International and India private orders get delivered in 8-12 weeks and hence orders executed within same quarter do not show up in order book.

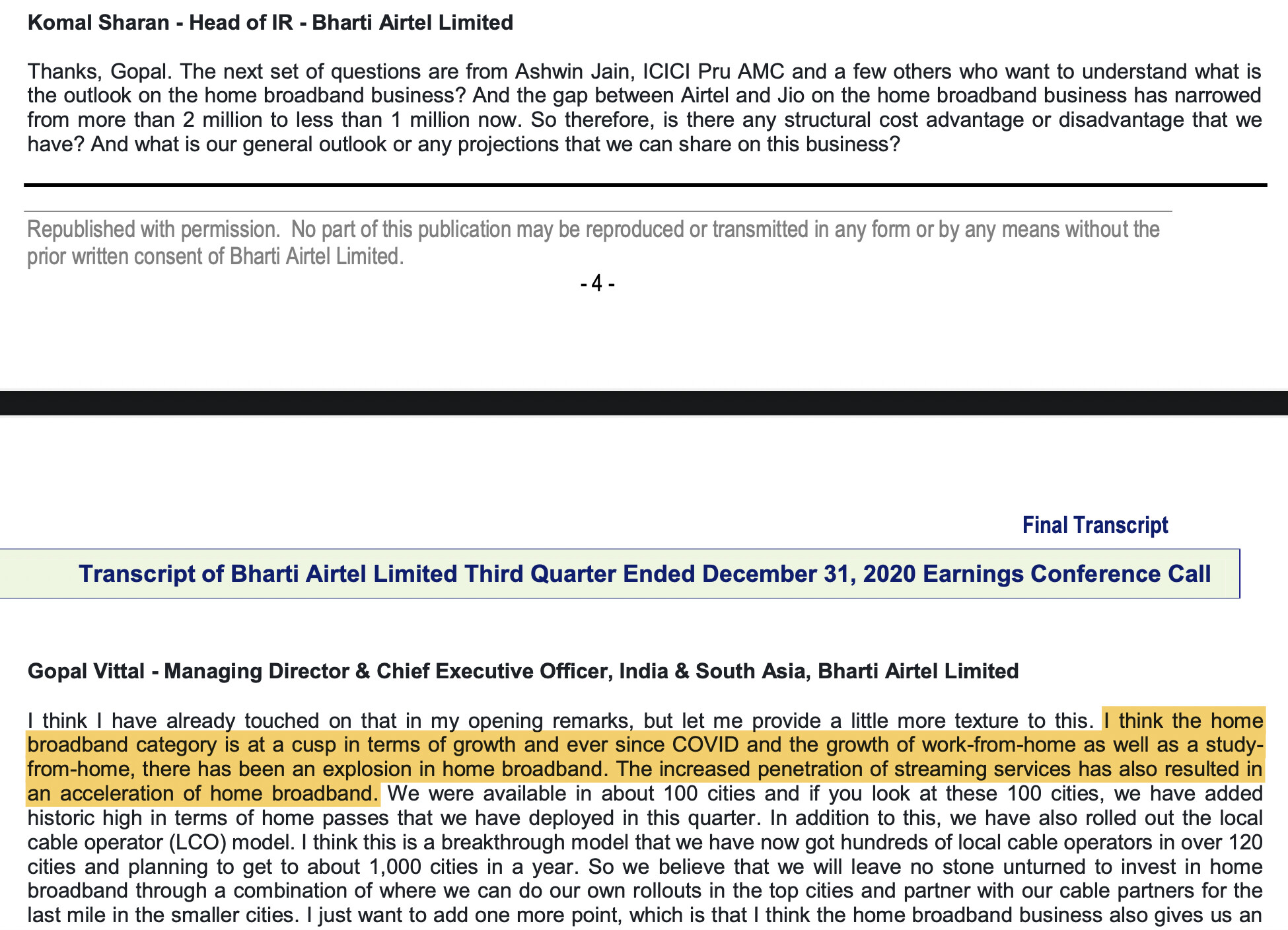

Let me talk a little bit about FTTH business now.

From Airtel Q3 FY21 Conf Call →

In home internet business, entire copper infrastructure will be upgraded to FTTH. How big of an opportunity is this?

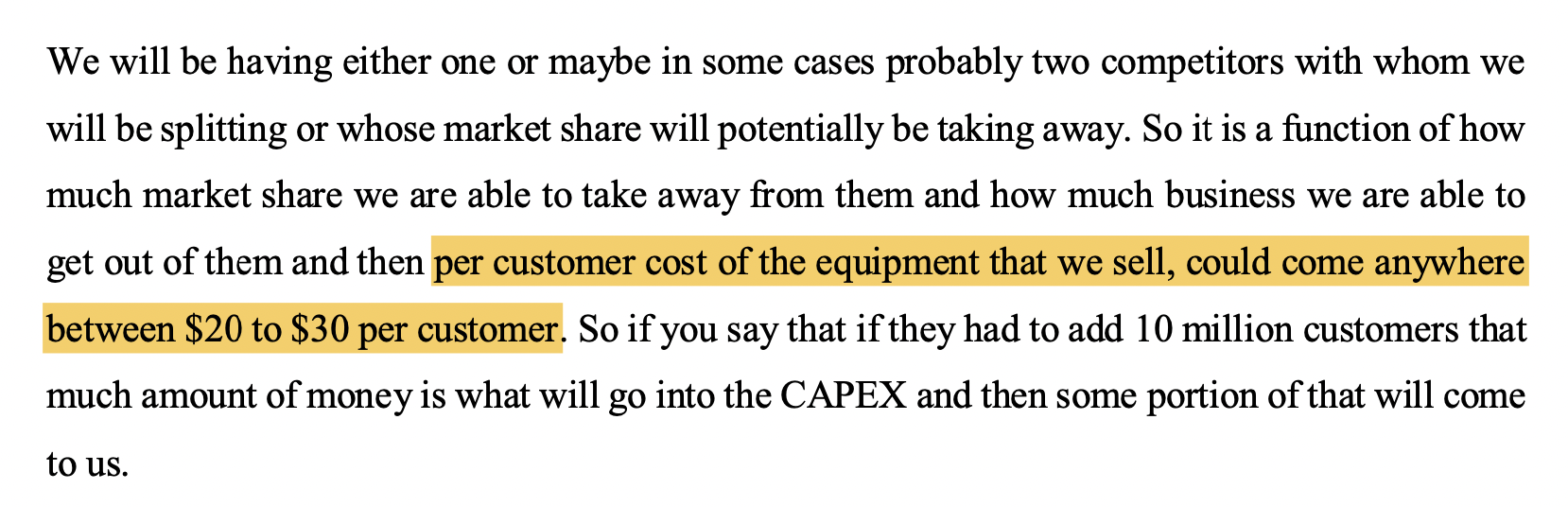

Tejas Q2 FY21 Conf Call, per customer equipment that Tejas can sell in FTTX is 20-30$ per customer. If 10mn customers get added over next 2-3 years, opportunity size comes to 200-300mn$.

Larger operators usually buy customer premise equipment directly (like Jio Fibre) and hence smaller opportunity size for Tejas. Smaller players buy both - infrastructure as well customer equipment from Tejas.

Let me pick the last one first. GMPLS based support for DWDM products. As reported by industry sources Tejas supports MPLS-TP based products for PTN networks, Mobile Backhaul for example. See below picture just to understand relationship between GMPLS, IP/MPLS and MPLS-TP.