What is the value of the marketable investments the company has.The annual report says around 295.41 crores,whereas screener says it is 528 crores.

As long as they dont buy back a huge number of shares,things should be okay.I mean they have a profitable business and a good amount of rcurrent investments.

Results…

https://www.bseindia.com/xml-data/corpfiling/AttachLive/26ec82c1-f817-4f88-bfdd-ed75cb4b7160.pdf

In Brief:

1 Like

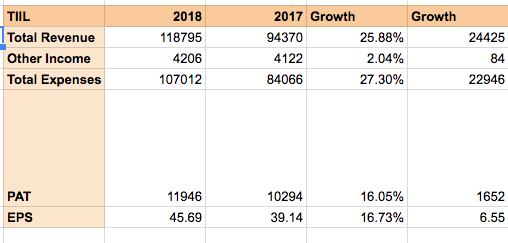

Results are very good. Scaffolding business is matching the drum closures division with a good return on capital.

Tailwinds for textile ( weaker rupee, import duties ) might help and make it ripe for a demerger hopefully

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=c6e78de5-174a-4a57-a3ca-298326c46c6e

2 Likes

I was going through the Company. Though the diversification in Yarn business is a concern , i have found more interesting things :

- Nutricraft Products Private Ltd formed in 2015 is a private company of promoter involved in Production, processing and preservation of meat, fish, fruit vegetables, oils and fats. The E-mail and Address of the company is same as that of Technocraft.

Possible contender of including this business into Technocraft in future for more diversification at high premium. - Dynasty Brewcraft Industries LLP incorporated on 13 October 2016. It is into Manufacturing of food products and beverages… Again Same Email and Same address.

- BMS Industries Limited involved in Manufacture of Basic Iron and Steel. Same address and Same Email.

- Technosoft Engineering Projects Limited : It is a Subsidiary Company which is registered as a Software publishing, consultancy and supply and documentation of ready-made (non-customized) software, operating systems software, business and other applications software, computer games software for all platforms. Don’t know what actually this subsidiary Company is for.

- Paithan Eco Foods Private Limited incorporated on 31 May 2016 having same registered address and email as of Technocraft.

- Ashrey International Trading Private Limited is a private company of promoters registered on Same address as that of Technocraft but not mentioned as Promoter. May be not holding any Shares.

- Hochstein International Trading & Consulting Private Limited incorporated on 20 October 2016. Again a company registered on Same address but do not form part of Promoter Group. Possibility of No Share Holding in the Company.

- M. D. Saraf Securities Private Limited involved in Activities auxiliary to financial intermediation, except insurance and pension funding. Not a part of Promoter group but again registered on Same address as that of Technocraft.

No doubt company recently shifted the registered address of the Main Business.

.

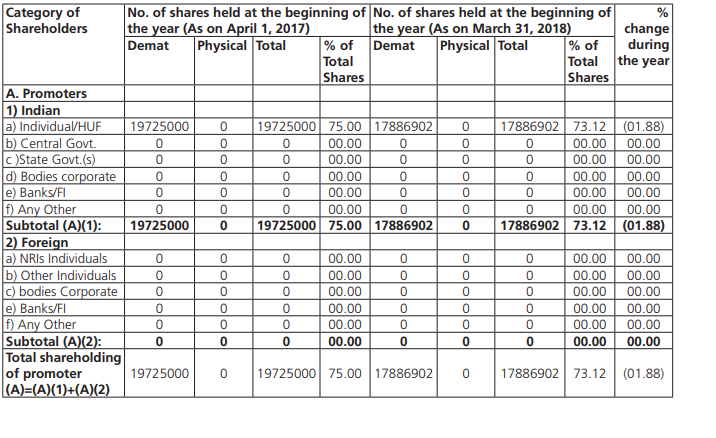

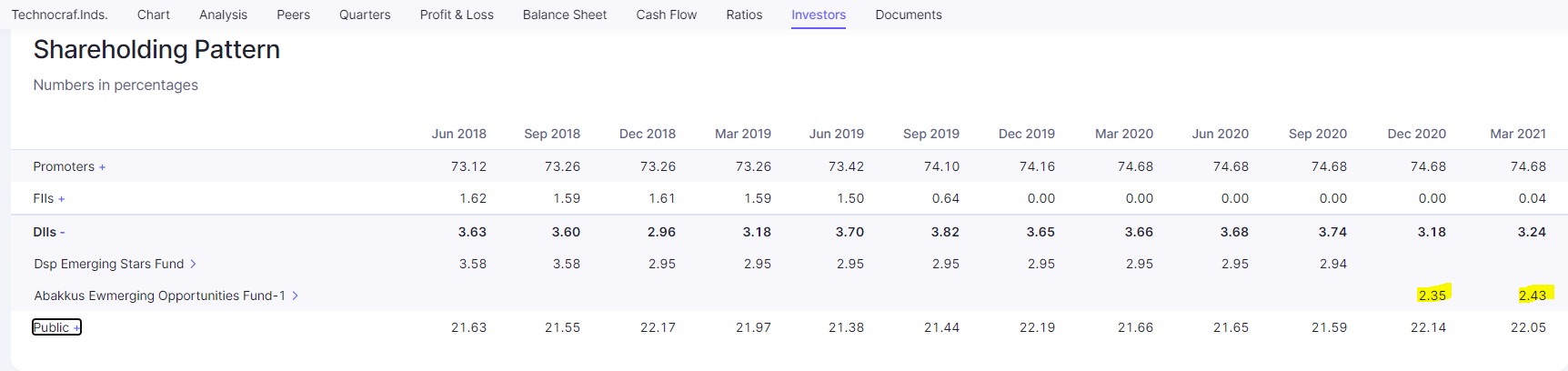

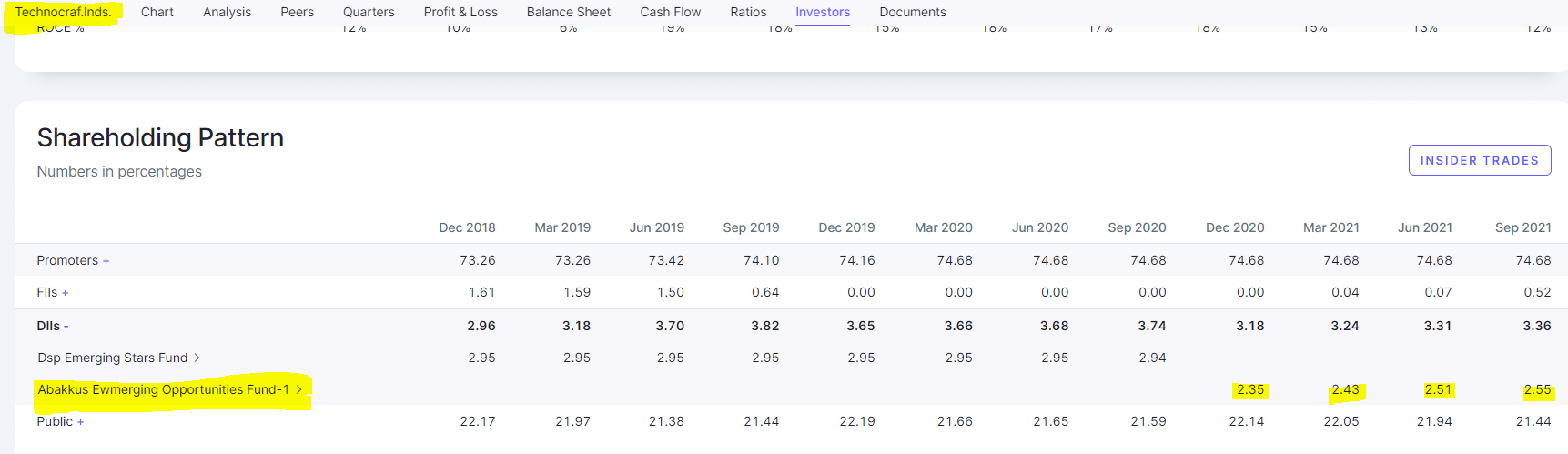

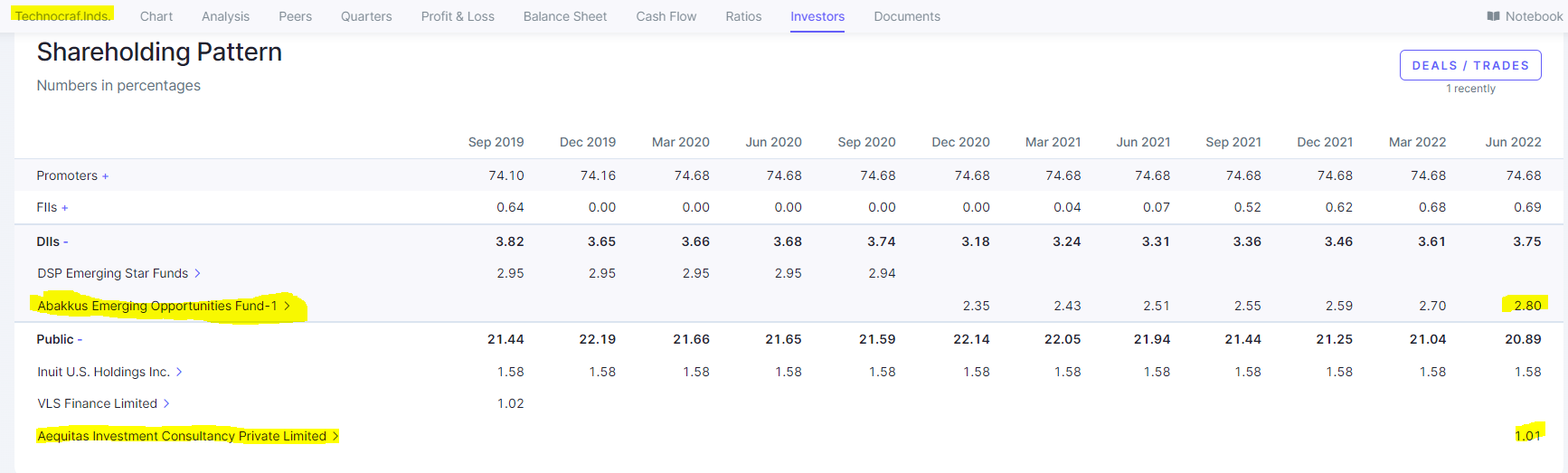

There is one more interesting thing i am unable to understand. The company has done buyback of equity shares last year and shares have to be tendered in equal Proportion i guess.Then how come the promoters holding got declined despite the fact that there was no selling by the Promoters throughout the year except in Buyback.

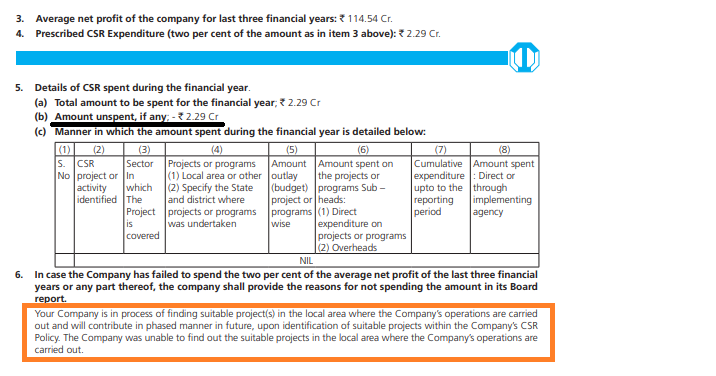

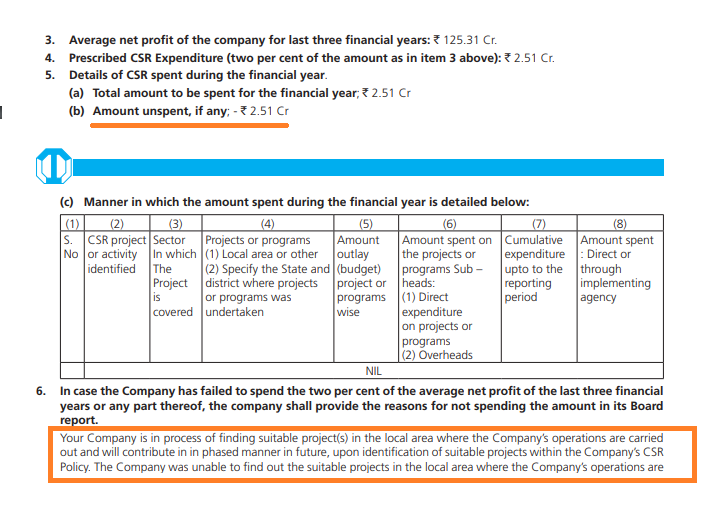

AR 2017 : CSR Expenditure is Zero.

AR2018 : Again Zero Expenditure on CSR

The website of the company mentions the CSR activities , have to again look at Next year AR ![]()

5 Likes

- Drum closures business going from strength to strength

- Less focus on the Textile business going forward. See disclosure below :

2 Likes

Technocraft is potentially a thematic stock. Globally dominant player in 2/4 segments. Unfortunate that most people get distracted by other 2 segments, of which 1 was always making small money (Technosoft) and the other might finally be turning around (textiles). Net-net, 10 year RoE is 15%. Leverage might be another distraction, but its growth engine, i.e. scaffolding does require working capital, as it is all about owning the distribution entity (now largest in the USA) and maintaining multiple SKUs/ inventory. 18-20% RoCE business, and now known as a dominant player in multiple markets. Drum closures too they are global leader, used in chemicals packaging.

2 Likes

They invested a large amount of capital on the Yars business why not dispose it off? The working capital cycle is almost a year since 2017-2019? Is there an issue with the debtors/inventory? Suddenly the collected a lot of cash in H1 20202 to pay down the leverage.

1 Like

Lets hope for a change P. Hope (Hold On Pain Ends) is all we have!

Demerger of Textiles business and buyback of shares. The fact that SuSi has entered, taken a large position in the company, something could be in the offing.

2 Likes

Long Term Techinical Analysis of TIIL. ( not a buy or sell reco)

TIIL (Technocraft Inds) - Weekly Line (log) chart. Double Inverse Hns. Restest of Smaller (Green) Inverse HnS done. Both multi year formations.

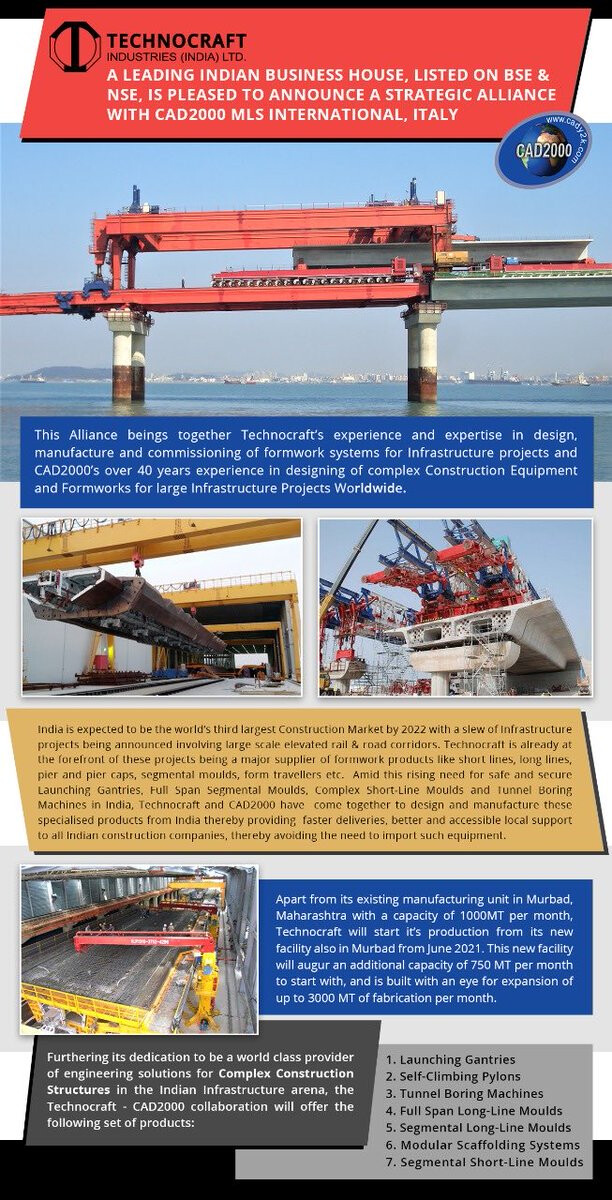

Technocraft Industries (INDIA) Ltd., a 50 years old ₹2000 Crore Indian Business House, listed in BSE & NSE, is pleased to announce its Joint Collaboration with CAD2000 MLS International of #Italy

Abakkus - Sunil Singhania further increases stake in the company.

2 Likes

1 Like

This time the drum division has shown a very good growth on comparable basis from precovid 2019 to 2020 more than 20 percent growth on the revenue and profit the scaffolding is an interesting theme with very interesting product portfolio but the margins are fluctuate from 12 to 22 percent however the revenue has grown very well to more than 600 cr with various geography. The yarn division which was a major drawback has shown a turnaround. However the important thing is the drum closure division growth has come back and scaffolding has a good future. ( They have forayed into some defence manufacturing in a company called technocrats defence pvt ltd even mr saraf mentioned in a old interview but not verified) the technical engineering division has a very good potential and doing around 100/120 cr with 22/25 cr opm.

So this year around fy 21/22 440 ebitda with other income it is trading at around 5 ev to ebitda debt is 435 cr catering to WC on the higher side above 150 days whereas they have cash around 80 cr and 300 cr investment and an property which fetches rent valued at 30 cr. Most of capex looks in the scaffolding side the new plastic division was also opened closer to the old plant.

With the kind of growth shown will the market value it at historical EVEBITA of 8 which should fetch a market Capitalization of 3500 cr or why it is still at 5 EVEBITA is a interesting point for discussion

Can the seniors have a look please .

Disl invested a small qty at lower price and have added recently and hence could have confirmation bias

4 Likes

better to wait for Q1 results.

1 Like

The scaffolding division is presenting a good opportunity

Existing Indian player like MFE BLS and even the international players local sales like LAHER PERI ULMA shows that there is competition in the business but each player has a niche product.

As far Technocraft is concerned there MACH one is a very good product and they are present in all the areas of scaffolding and formwork.

But if we observe we will notice that scaffolding is a capital intensive in nature which is reflected in high inventory we’re they have to maintain SKD kits at dealer end.

Now they have tie up with COATSMAN India for scaffolding and even there rental income scope has increased

They have also tie up with CAD2000 MLS in this area.

They did nearly 200 cr exports to AAIT USA there subsidiary previous year in scaffolding and some exports to Europe and Latin America and Africa. Now company is doing some major work in India in scaffolding in some major infra projects.

Whether the anticipated recession will play some dampening has to been seen.

As for drum closures with Europe and usa facing problems there competition like Tri-SURE whether it will be affected which will give some advantage or whether steel drums manufacturers will be affected has to been seen. But with a market share of 35/40 percent and projected market of around 3000 cr in 2030 there is improvement chances, which is mentioned in the CRISIL ratings of sep 2022. Now they have entered into plastic closure business which is also seeing some traction.

The engineering services business is not major but a reaonsable growth can be expected from the electronic design section of technosoft inc

The textile division has shown a turnaround but a wait and watch there garments is DANUBE fashion has ladies children and mens knitted garments.

Very honest decent but conservative promoter IIT GRADUTES and second line is in place with there sons taking charge has over 1300 permanent employees. Never diluted there equity nor pledged.

Even the balance sheet on a whole if see the investment is 420 cr ash 101 cr which will offset there DEBT. But even in the debt short term debt is around 440 cr which is majority in packing credit.

Three yr OCF is above 500 cr even after increase in the working capital.

We have an EBIT of around 360 cr for the working capital of 1400 cr (with investments) without investments and textile into account it will be 270 cr for 900 cr working capital.

But the market has identified the company under steel sector and hence low PE whether it will be categorised as a multiproduct company and get a 15 PE is left to the market dynamics

But with the present price correction it is avalaibe at less than 8 PE and around 5 evebita looks like an interesting bet.

DISCL bought holding qty with long term intentions

6 Likes

**

In this list Technocraft is only Indian exbitor from India in scaffolding and form work

But the Europe largest is PERI with a turnover of more than approx 1600 million euros with Germany facing power crisis whether PERI group and its subsidiaries will face any problems which will TIIL any added advantage

This is a point I am not able to find out if any Body could throw some light it will helpful

Since peri is not listed the other listed is laher sa in Poland which has turnover of around 225 Plm ie I think around 500 cr inr which is trading around 13 PE.

This is just a weekend info collection not to be taken as any recommendation

With Europe facing power crises, construction work itself will shrink a lot, thereby denting demand of scaffolding itself.

That is point I wanted to understand with PERI facing problems and comparatively TIIL has a price advantage in the market non Europe area it is just a thought may be confirmation bias also. But yes with 80 percent sales coming from export the demand could be an issue

1 Like

This is the scaffolding work peri gmbh subsidiary peri India is doing here

Still technocraft was able achieve such a growth

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=d854df7f-9135-4393-8b08-46d6183b7539

This qtr bottom line looks like having some inventory profit from the consolidated side already trading above the buy back price

Again the textile is a major draw back which is draining there capital and profit overall there is more than 100 cr loss but still they are building capex in textile sector

Since it a love of a father for the son I don’t think they will demerge it

Other wise looks very good whether the scaffolding division can grow at the rate of 15 to 20 percent and maintain the present ebita is a factor

Disl invested

1 Like