This is the engineering division website

Scaffolding website with aait usa

http://scaffolding.technocraftgroup.com/

E commerce website

https://tdf.drdo.gov.in/project/development-dual-flow-jt-cooler

Can some seniors have a look at this what is the defence product awarded to technocraft industries lf any info pl share

1 Like

A recent interview by Mr Sharad saraf

Textile division restructuring is happening but demerger will take time

New capex 400 cr to add 500 cr topline in fy 24 and margin on conservative estimate at 20/25

Textile is still challenging alluminium form work is coming up new products in drum closure.

Let us wish a honest industrialist luck.

1 Like

I attended Technocraft AGM on Sep 27, 2023. Here are my notes -

Scaffolding

-

Prospects in US : We did about $48 mn of sales in US in CY22. US business continues to be quite strong and growing. In CY23, well on track to do around $65 mn. Next year CY24 should be able to increase it further to $80 mn. Have expanded distribution setup in US. Recently opened new distribution centre in Miami. Overall we have five different distribution location across the US. We are now the largest scaffolding distributer in US. Prospects are quite good.

-

Competitive Advantage : In scaffolding there is not much of product specialisation. It is more of a commodity product. Unlike drum closures there are 1000s of cos worldwide making scaffolding, primarily in China. Our competitive advantage in scaffolding is sales distribution. We cut across the entire distribution chain and keep stock in countries like US, Australia, NZ, Europe, etc and sell directly to the end user. The competitors in local distributors here get their products made in China whereas we have our own manufacturing facilities so we are able to provide better quality, better reliability and end-to-end service. Also able to command some premium pricing.

-

It is well known that steel is more expensive in India than China. We have disadvantage of 15-20% over China. Also the tariffs are gradually pulled away from US. Inspite of these we are able to sell our products at good margins because of our bandwidth, our distribution channel and also China+1 strategy that is going along in the US and other countries

-

Europe Sales : We are not well penetrated in Europe yet; it continues to be small market for us for now. We addressed this by hiring a very senior sales head in Europe in our Poland office from competition. We have little setback in Europe right now because of economic crisis there and market is right now quite dull. We expect this to improve. By end of this year, we will have certification in place for our scaffolding products in Europe. This will be a major breakthrough for us to increase our sales there. By next fiscal year FY24-25 we should see significant pickup in Europe sales and I think Europe market in FY24-25 and FY25-26 has the potential to be as large as the US market for us. So prospects are very good. Currently the Europe is only about $5-6 mn but it has prospects to be at least 10 times the present size based on we getting the certification which we will get by end of this year and market picking up.

Formwork

-

Formwork is far more specialised product than scaffolding. Formwork involves precision engineering, fabrication and site support. The kind of work we are doing in infrastructure in India is very high end Engineering. There is competition in formwork but part of the reason we are putting Aurangabad plant with backward integration of aluminium extrution is to put in place entry barrier. That by itself is quite a significant entry barrier. We will be first co (in India) to have our own aluminium extrusion plant with forward integration of aluminium formwork. Our specialisation is we cater to niche high end Engineering sector like infrastructure.

-

Capex and Timeline : 350 cr new capex in Aurangabad, primarily for formwork. Will be fully completed by end of next year 2024. Production will start by Feb ’24 in stages. The entire aluminium extrusion plant will be fully commissioned by end of 2024. We should see the full benefit of new plant in FY25-26 and we will see some benefit in FY24-25 as well.

-

Sustainable Margins : 15-20% in formwork business is doable in the segments we play. This will increase by 5% to about 20-25% once the Aurangabad aluminium extrusion plant is up and running, specifically for aluminium formwork business. Overall 20% is quite a sustainable margins for formwork business.

-

Export Plans : We do have export plans. Currently we do very limited formwork exports in Middle East. As we increase capacity in Aurangabad we plan to increase formwork exports. US is definitely going to be key market for us, so is South America.

-

Construction growth is strong in India. In India, we are primarily selling formwork, not scaffolding. And that is the reason why we are doing capex in the Aurangabad to increase the capacity to cater to increasing demand in India.

Scaffolding + Formwork

-

Sales breakup : In Fy23, export was 62% and domestic 38% of business segment sales

-

Export revenue breakup : North America 70%, Europe 13%, Australia + NZ around 8%, South America 3%, Middle East 1-2% and Asia 1-2%.

-

Raw Material : Steel is our main raw material for scaffolding. We buy hot rolled coil steel. We have our own ERW tube manufacturing capacity. So we roll the steel into tubes. We don’t sell tubes at all (used to sell long time back; have come out completely). All our tube product is 100% captive consumption, in making scaffolding. The other raw material is aluminium extrusion used for making formwork panel which we will soon in Aurangabad start making in-house as well, for that the raw material will be aluminium scrap.

-

Revenue from aluminium formwork in Fy23 was about 188 cr which is about 20% of Scaffoldings business segment reported revenue of 889 cr.

Textile

-

Investing in new mill in Amravati; capital outlay of ~150 cr. Govt incentive : Generous benefit in Amravati; co gets 25-30% capital subsidy. In process of complete shutdown of yarn mill in Murbad as it has high cost of operation (power, wages) causing bleeding in textile division. Will continue to be producing fabric in Murbad because have process house there and affluent treatment plant which cannot be shifted is also there. Out of the capex plan of 150 cr in Amravati, we have already spent 108 cr. We expect to start the production within couple of months. No immediate future plans of more capex in textile .

-

Demerger: No talk of demerger as of now. We keep getting proposals. The board will decide as and when appropriate time comes.

China Capacity for Drum Closures

- In China we have 18 mn sets capacity that is on one shift basis of 14 hr. China capacity is fully utilised as of now. China capacity can be expanded if we increase the shift hours. May expand as and when needed.

Defense

- It takes lot of time. So far we have total order worth 20-21 cr. In future defence may pickup at faster pace

Technosoft Engineering

- This business is doing very well. We are seeing strong growth in FY24. First qtr was not just the one-off qtr. We will see similar or better qtr going forward in each of the qtr this year. We expect FY24 to be very strong year. And going forward for FY25 the prospects for this business is quite strong in US, UK and in the European market. Post covid even the small and mid size manufacturing cos are very open to outsourcing large part of their Engineering work which earlier they were not. We are also expanding our sales staff in US, we got very senior VP of sales who has joined in US. We are expanding and are now entering into larger accounts. Overall the prospects are quite good.

Disc: Invested. No transactions in last 30 days.

33 Likes

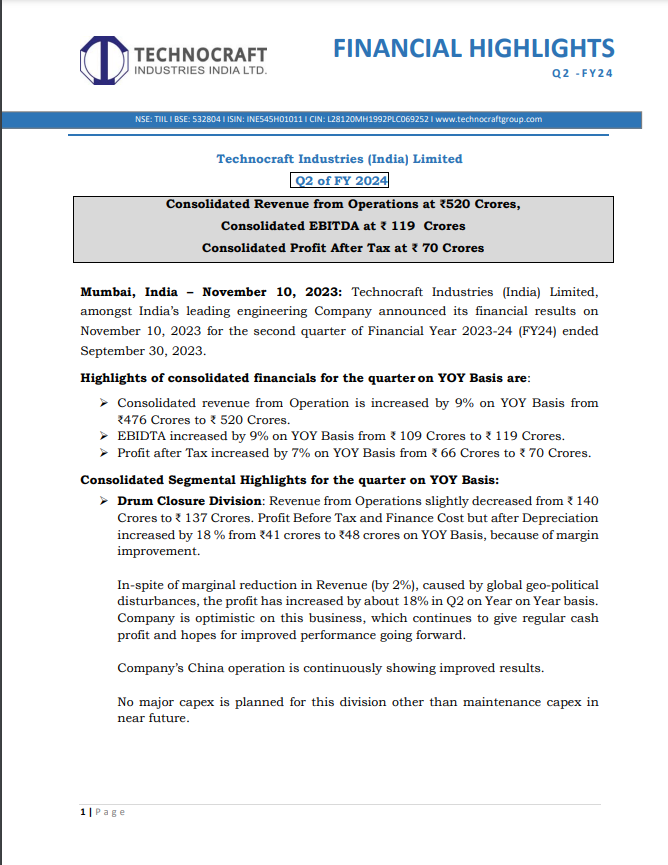

Technocraft Industries has reported its financial results for the second quarter of the fiscal year 2023-24 (FY24)

Financial Performance (Consolidated) for Q2 FY24:

- Revenue from Operations: The company achieved consolidated revenue of ₹520 Crores for Q2 FY24, representing a 9% year-on-year (YoY) increase from ₹476 Crores in the previous year.

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): The consolidated EBITDA for the quarter reached ₹119 Crores, reflecting a 9% YoY growth from ₹109 Crores in the corresponding period of the previous year.

- Profit After Tax (PAT): The consolidated profit after tax stood at ₹70 Crores, indicating a 7% YoY increase from ₹66 Crores in Q2 FY23.

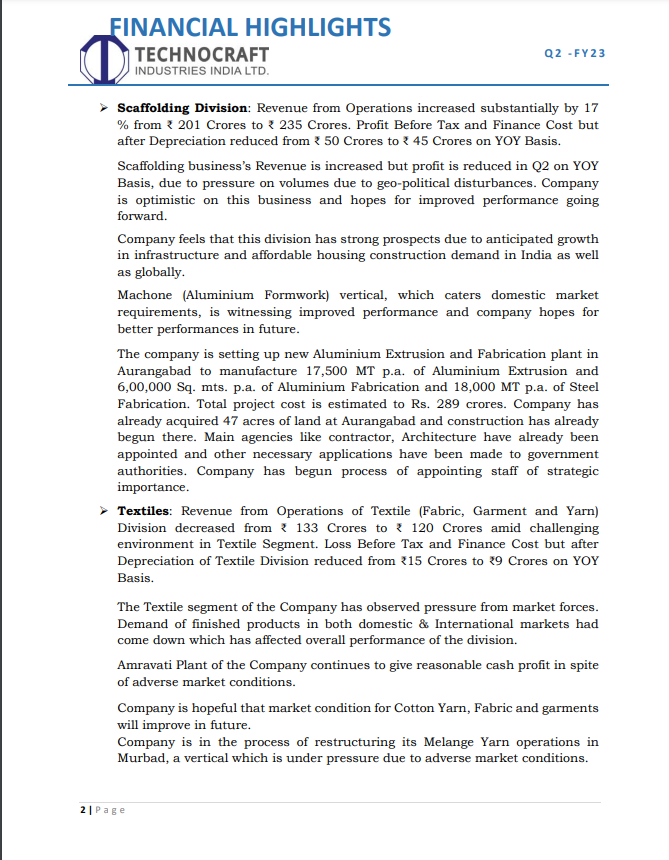

Segmental Highlights (Consolidated) for Q2 FY24:

1. Drum Closure Division:

- Revenue from Operations: This division’s revenue slightly decreased from ₹140 Crores to ₹137 Crores in Q2 FY24, a 2% decline.

- Profit Before Tax and Finance Cost: However, the profit before tax and finance cost, but after depreciation, increased by 18% from ₹41 Crores to ₹48 Crores YoY due to margin improvement.

2. Scaffolding Division:

- Revenue from Operations: The Scaffolding Division experienced a substantial 17% YoY increase in revenue, rising from ₹201 Crores to ₹235 Crores.

- Profit Before Tax and Finance Cost: In contrast, profit before tax and finance cost, but after depreciation, decreased from ₹50 Crores to ₹45 Crores on a YoY basis.

3. Textiles:

- Revenue from Operations: The Textile Division reported a decrease in revenue from ₹133 Crores to ₹120 Crores, primarily due to challenging market conditions.

- Loss Before Tax and Finance Cost: The loss before tax and finance cost, but after depreciation, reduced from ₹15 Crores to ₹9 Crores YoY in the Textile Division.

4. Engineering Services:

- Revenue from Operations: The Engineering Services Division saw a significant 59% YoY increase in revenue, rising from ₹33 Crores to ₹52 Crores.

- Profit Before Tax and Finance Cost: The profit before tax and finance cost, but after depreciation, increased by 38%, growing from ₹9 Crores to ₹13 Crores on a YoY basis.

Key Observations and Outlook:

- Technocraft Industries reported growth in consolidated revenue, EBITDA, and PAT in Q2 FY24 compared to the same period in the previous year.

- The Drum Closure Division saw a profit increase despite a marginal reduction in revenue, attributing the growth to margin improvement.

- The Scaffolding Division, while experiencing increased revenue, faced profit pressure due to geopolitical disturbances affecting volumes.

- The Textile Division witnessed revenue decline due to challenging market conditions, leading to lower profit.

- Engineering Services showed strong growth, with increased revenue and profit, driven by cost restructuring and a global delivery model.

- The company is optimistic about the growth potential in its various divisions and anticipates improved performance in the future.

- Technocraft Industries is actively focusing on expansion, as seen in the setup of a new Aluminium Extrusion and Fabrication plant, with a total project cost of ₹289 Crores.

- The company expects increasing demand for its services in the Engineering Division due to its offshore global delivery model.

10 Likes

Hi , where can I get technocraft industries agm recordings or agm minutes

1 Like

The company will start the commercial production of aluminium fabrication which has even more realisation compared to Steel formwork/Scaffolding now

5 Likes

After long time they have done a concall

Revenue top line guidance of 20 percent growth in all verticals and in textile a turnaround to positive because of shifting out of Mumbai and additional capex benefit to start from august full effect in 25/26.

And last answer about the defence product R&D looks interesting but it may take time to materialise

2 Likes

Technocraft Industries (India) Ltd Q4FY24 Concall Notes

- Management Guidance

(Management Tone: seems confident and bullish led by new capacities)

- Drum closure business will be steady in FY25 (supported by good growth in China), Scaffoldings business will see strong growth due to the Aurangabad expansion (full effects will be visible in 2025-26), Engineering and design service will also grow strongly and textile business will also see better performance for both the spinning and garment unit (due to shift from Bombay).

- FY25 Consol guidance- Revenues will grow by 25-27% in FY25 and 20-21% in FY26 , Margin- Likely to expand to 19-20% in FY25.

- Business

- Capex done for the two new plants (Amravati and Aurangabad) has been progressing well and will help the company to get out of the bombay circuit. Amravati is fully operational and Aurangabad (new aluminum formwork facility) has started trial production which will scale up gradually and reach optimum utilization levels by end of FY25. Expansion in Aluminium extrusion is for captive consumption (1500tpm will be required for 60k sq m of aluminum formwork production). Finished product is Mach One.

- The benefits from these new capacities will be visible from FY 24-25. Total Capex required will be 280cr (phase 1). Company has already spent half of that.

- The decline in the overall volumes of Scaffolding and Formwork division in FY24 was due to -

- Slowdown in the European market which became prominent from Q3FY23 (October) as a result of the Ukraine Russia crisis. Scaffolding plant was operating at 70% utilization levels and output was restricted to 2000 tpm (peak volumes were 3000 tpm) due to decline in these markets.

- Slowdown in the infrastructure formwork segment in India, led by delay in execution of projects. Even though the business was sitting on strong order books (which they still are), they were impacted by the slow cashflow cycle between the govt and the contractors who are TIIL’s customers. This business was averaging about 700 tpm but now is down to 200-250 tpm (peak volumes for steel formwork division was 800 tpm)

-

Things have turned around in this business since February. The European market continues to be slow but there has been a strong uptick in demand from the US, Middle East, Australia and India. From April of this year, the business will be back to 3000 tpm. June onwards this output will increase to 3250 tpm. Mach one continues to be strong and the infra formwork division is steady at 250 tpm but management expects it to pick up post election results.

-

Mach one has done well. 100% of sales is from India and capacities are fully utilized. Volumes used to be 20k sqm per month and currently they are doing 30k sqm per month. Plan is to add another 30k sqm per month in Phase 1 of expansion. Production will start from August and the full effect of this increase will be seen next year. Peak revenue which will be seen next year from mach one will be 850cr (New facility will add about 450 cr). Total order book for aluminum formwork is 2 lakh sqm.

-

Mach one is also seeing demand from South America, US, African countries, and the Middle east. Management has not started tapping into these opportunities fully because of capacity constraints. Post commissioning of the Aurangabad plant, they will also start tapping into these opportunities.

-

The end use of the product Mach one is residential developers (mostly) and construction contractors. The life of standard aluminum formwork is about 3-4 years. Project specific formwork (about 35%) will have a life of one project and will be scrapped. Scrap realizations of aluminum formwork is 30%.

-

The realizations of aluminum formwork per sq m is Rs. 10,000 rs and steel formwork is about 1.05-1.1 lakh per sq metric tonne.

-

Sustainable margin for the scaffolding division is 20% and for formwork and Mach One division is 15%.

-

Majority of the company’s export for scaffolding is to the US (75%), Europe is 5-10%. The US continues to see good demand but problems in other markets have dampened the show in cumulative revenues. This business is majorly an export business with 95% revenues coming from exports.

-

The company has recently hired a sales head for europe. Waiting for a certification to start supplies of scaffoldings in Europe. Will come in 3-4 months.

-

Drum closure business will have a market share of 55-60% (varies between 40-60%). China contributes to 15-20% of the drum closure revenues. Chineses drum closure facilities are running over 90% capacities and will see some expansion.

-

Share of drum closures in Europe is ⅓. It has gone down due to war, shifting of chemicals out of Europe, etc. Company trying to make the shortfall by focusing aggressively on other markets, hence no fall in sales this year.

-

Company has added a new range of plastic closures which will start showing results in FY25. Plastic closure is a higher margin segment but low volume.

-

Drum closure business is built on long term relationships with customers, so the repeat business is very high (90%).

-

Textile business spinning operations have been shifted from Mumbai to Amravati, where the spinning division will see good cost benefits. Yarn has shifted there already and did 12-15% margins last year and will do 10-12% ebitda this year. Similarly, the garment business also shifted to Amravati (1.5years ago). Total proceeds from the sale of the Mumbai facility will be 27-28 crs. Garments business did sales of 50 cr last year, will touch 80-90 crs this year with ebitda margins of 15%. Fabric segment has been under stress due to the global scenario. But now the US market is picking up with buyers like Walmart and Target. Next Q onwards this division will also start doing well.

-

Will receive subsidy of 50cr from 150 cr of investment for the new capex done here. (earlier received 35-40 cr for capex done for another 120-130cr). No plans of incremental capex in Textiles.

-

Engineering and design segment has done well. No abnormality in margin fall. Demand is quite strong specifically from the US, UK and other western countries. This division has strong long term relationships with repeat business of 50%.

- Risks

-

The Red Sea issue led to a rise in freight cost. This has cooled down from a month.But, management is able to pass on these costs in the price of the product sold.

-

Lost some share to Chinese players in the drum closure segment which the management will get back.

Disclosure: Invested. No recommendation to buy/sell/hold

10 Likes

Hi,

Can anyone explain their interest costs. Their int costs for FY 24 is about 40 CR, but when I look into the balance sheet, the long term borrowing is only 127CR. Even if I take the total borrowing of 675 CR, at rougly 9% rate the interest should be some where close to 60 CR. Not sure what am I missing here.

2 Likes

Concoll notes for Q4(Taken from screener)

Scaffolding Division:

- Saw a decline in volumes due to slowdown in European market and delays in infrastructure projects in India.

- Output in October 2023 to February 2024 was at 2000 tons a month, dropped due to market conditions.

- Currently back to 3000 tons a month with increased demand from US, Middle East, Australia, and domestic markets.

- MACH ONE business saw an increase in volumes.

- Sustainable margin for Scaffolding business is about 20%.

Margin Expectations:

- For Formwork and MACH ONE business, margin is around 15%.

Export Markets:

- Majority of export for Scaffolding is to the US (75%), Europe is around 5%.

- US demand remained strong, while other markets experienced a decline.

Textile Business:

- Shifted operations from Bombay to Amravati for cost and efficiency benefits.

- Expecting improvement in garment sales and EBITDA margin in the coming year.

- Fabric business impacted by global retail segment standstill, expecting recovery post US market pickup.

- Historic negative EBITDA issue addressed by shifting operations to Amravati.

- Received capital subsidy for capex, no plans for further capex in spinning.

- Expectation of positive EBITDA to continue in upcoming financial years.

Drum Closure Business:

- Market share in Europe is around 30%.

- Dependence on chemical sector in Europe, affected by capacity shifting to China and India.

- Continuous expansion in China, running at over 90% capacity.

Aluminum Extrusion Plant:

- Capex of INR 280 crores for the plant.

- Expected to double the output of MACH ONE product with additional capacity.

- Backward integration for captive consumption, but will also contribute to additional sales.

Market Strategies:

- Focused on aggressive sales in other markets to compensate for the decline in Europe.

- Bullish outlook for Europe with certification in progress.

- New capex in Aurangabad to increase top line as per previous statements by management.

Expansion Plans:

- Trials for additional top line to start in July, fully operational by end of December.

- Production to start in phases this financial year, with full effect seen in '25-'26.

- Incremental revenue from MACH-ONE to be around ₹450 crores in '25-'26.

- Aurangabad plant to contribute to growth in scaffolding and formwork division.

Engineering and Design Services:

- Revenue and profitability increased by 40% last year.

- Strong demand from US, Western Europe, and UK markets.

- Margin slippage in last quarter not abnormal, demand remains strong.

- Turbulence in logistics due to Red Sea crisis, freight costs have now stabilized.

Revenue and Capex:

- Total revenue from MACH-ONE product line to be around ₹850 Cr in '25-'26.

- Order book close to 2 lakh square meters in aluminium formwork.

- INR27-28 Cr expected from the sale of textile assets in Bombay.

Defence Business:

- Successfully developed Joule-Thomson coolers for missiles and equipment for mass moment of inertia measurement.

- Expecting growth in defence business with government spending.

- Considered as an investment for future growth opportunities.

Plastic Closures and Other Opportunities:

- Developing rapidly in plastic closures with good margins.

- Facing resistance in the US market, but growing in other markets.

- Engineering design services division expected to show double-digit growth.

- No active pursuit of new lateral opportunities, focusing on existing verticals for growth.

3 Likes

Technocraft Industries -

Q4 and FY 24 concall and results updates -

Company’s Business segments, FY 24 revenues, EBIT margins -

Drum Closures - 543 vs 534 cr YoY, operated @ 34 vs 30 pc EBIT margins YoY

Scaffolding and Formwork - 1032 vs 889 cr YoY, operated at 18 vs 26 pc EBIT margins YoY. This is likely to reverse in FY 25

Manufacturing of Cotton Yarn, Fabric and Garments - 491 vs 534 cr YoY, operated at (-)4 pc vs (-) 7 pc EBIT margins YoY

Engineering and Design Services - 198 vs 135 cr YoY, operated at 19 vs 20 pc EBIT margins YoY

Company’s new Aluminium extrusion and fabrication plant at Aurangabad with a capacity of 17,500 MT and 6 lakh Sq Mar has gone live in Mar 24. As this facility ramps up, results from this plant should be visible in FY 25 ( in Q4 - basically, full effects will be visible in FY 26 ). Total capex required here should be around 280-300 cr. This should result in incremental revenues of 400-500 cr for the company ( most likely in FY 26 - after the full ramp up )

Seeing strong demand uptick in the Scaffolding and Formwork business from US, Middle East and Indian Mkts in Q1. Company is ramping up capacity to meet the increased demand. Expecting further acceleration in Indian demand after the election uncertainty is over

Sustainable EBITDA margins in Scaffolding are around 20 pc and 15 pc for Formwork

Company has shifted most of their Textiles business from Mumbai to Aurangabad. Aurangabad is a low cost destination wrt doing business. Plus there is a global recovery ( post COVID led overstocking ) in the Textiles business. Company feels that a turnaround in their textiles business should only be around the corner

Most of company’s Scaffolding exports are targeted at US ( 90 pc of exports ) vs only 10 pc of exports to Europe. Company lacks a key certification that’s required to sell in Europe. If that certification comes through in next 3-4 months, company can ramp up their European business as well. If this happens, the EU business can be as big as their US business

Also expecting descent growth to continue in the engineering and design business

Company has not even started tapping the export demand for Aluminium formwork from geographies like - Africa, LATAM. Will venture out there once the new Aurangabad facility comes fully on stream

Guiding for a topline growth of > 20 pc for FY 25 and FY 26. Also guiding for an EBITDA margin of 19-20 pc for FY 25

Other players are also putting up Aluminium formwork capacities in India. However, the demand is outpacing the supply. Also, Technocraft is one of the few companies that are also backward integrating into Aluminium Extrusions. This should give them a competitive advantage

Company has also entered into plastic drum closure business. Margins here are similar to steel drum closures. Also, the application areas of steel and plastic drum closures are completely different

**Company has developed a special device used to cool down the seeker head of Air-Air, Surface - Air missiles (cools it down below (-) 150 degrees within seconds). Company is the sole Indian Producer for this device. Supplies should start shortly.**Although wrt company’s size, this may ( at present ) not be a big revenue driver

Disc: holding, biased, not SEBI registered

6 Likes

Please have a look at shareholding pattern… some fund reducing stake…

Why sudden buying interest in this company?

Almost 20% up in 2 days- Any institutional buying.

Not that am complaining- Invested and biased😀

2 Likes

Technocraft Industries (India) Limited (BSE:532804) announces a share repurchase program. Under the program, the company will repurchase up to 288,889 equity shares, representing 1.26% of the issued share capital, for INR 1,300 million. The shares will be repurchased at a price of INR 4,500 per share.

The company has fixed August 27, 2024 as record date for the offer. As of August 9, 2024, the company had 24,461,687 shares issued and outstanding.

4 Likes

Technocrat Industries -

Q1 FY 25 results and concall highlights -

Revenues - 620 vs 556 cr, up 11 pc

EBITDA - 146 vs 145 cr ( margins @ 24 vs 26 pc )

PAT - 84 vs 91 cr

Segment wise revenues -

Drum closures - 151 vs 127 cr, up 18 pc

Scaffoldings and Formworks - 334 vs 274 cr, up 22 pc

Textiles division - 104 vs 139 cr, down 25 pc

Engineering and Design services - 49 vs 42 cr, up 18 pc

Segment wise EBIT -

Drum closures - 55 vs 40 cr, up 38 pc

Scaffoldings and Formworks - 53 vs 77 cr, down 31 pc

Textiles - (-) 12 vs (-) 4 cr

Engineering and Design services - 8 vs 9 cr

Company is hopeful of an improved performance in the Drum Closure division. No major capex ( except maint capex ) planned in this division

Company is confident about a margin revival in Scaffoldings and Formwork division because of anticipated growth in infrastructure and housing led demand in India. Company’s 02 plants in Aurangabad to make 17,500 MT of Aluminium Extrusion and 6,00,000 Sq Mtr of Aluminium fabrication has commenced production in Q1 ( a reason for lower EBIT in this segment due higher depreciation ) . They will be ramped up over the course of FY 25

Expecting the demand for engineering and design services to remain strong due to the strong acceptance of their offshore global delivery model

Company is the second largest drum closure manufacturer in the world, currently exporting to 75 countries. Company is guiding for single digit growth in this segment but the margins will sustain in > 30 pc band

Because of commercialisation of the Aurangabad facility, company expects incremental topline of 450 cr and EBIT of 80 cr for FY 26. For FY 25, incremental topline and EBIT should be 60 cr and 10-15 cr respectively

The scaffolding business continues to be soft in Europe. However, demand from US is descent

In the textiles business, company has commissioned a new spinning unit in May. Revenue from that will start to flow in Q2 whereas the expenses started to come in Q1. From Q2 onwards, company sees a descent uptick in the textiles business. For full FY, should add around 130 cr of topline to the yarn business. All textiles divisions combines ( Yarn + Fabric + Garments ), topline should be around 650 cr

Also expecting the textiles division ( Yarn + Garments + Fabric divisions ) to be EBITDA positive for this FY ( EBITDA percentage in the range of 8-10 pc )

Company is still awaiting - B certification in Europe for its Scaffolding business. They are expected to get it sometime in Sep

Aluminium formwork’s demand continues to outstrip supply ( despite having local and Chinese competition ). Local demand is so good that the company is not even able to export this product. Company’s current Mkt share in India is around 10 pc or so

Company’s steel formwork business did witness softness in demand in Q1 - because of the elections. Should pick up going forward. However, company’s main thrust and bulk of the business continues to come from Aluminium formwork. ( Steel formwork is mainly used for Infra projects while Aluminium formwork is mainly used in Real Estate sector )

Company sees very good demand outlook for its MAK-1 - aluminium formwork business - both from domestic and export markets for next 2-3 yrs

LY, company’s scaffolding + Formwork division did revenues of 1030 cr. This yr, company is expecting to do around 1250 cr and next year, they are expecting to do > 1800 cr from this segment ( because of the new capacity coming online )

For engineering services segment, expecting to do 20-25 pc CAGR topline growth for next 2-3 yrs

Expecting to touch a PBT of 500 cr for FY 25

Disc : holding, biased, not SEBI registered, not a buy / sell recommendation

7 Likes

Is there any news about Technocraft that I am missing,

mprice has corrected from 3100 levels to 2500 levels in a week. At this levels it looks attractive.

Disc: Tracking closely to enter.

1 Like

There was a buyback with price of 4500. After that its one way street

Company moved from PE of 10 (10 yr average) to 23 today… as profits doubled the price went up multiple times…

now with no further growth PE will contract to 10 again !! I think retail investors should exit and let the institutions buy…

1 Like

TIIL is the first Company outside Europe to have been awarded this Certification.

Until now, TIIL was only selling Props in the Polish market but with this B Certificate, it will

now be able to sell its Ringlock Scaffolding to customers across Poland. This will lead to an

enhancement of the customer base and increase in overall sales both in volume and value.

This Certification will also make it easier and faster for the Company to obtain similar

Certifications in neighbouring European countries wherein the Company decides to offer its

Ringlock System.

3 Likes