If you go through the last conference call, management acknowledges the difficult last 7-8 years and finally the tide has turned favorable with strong tailwinds. If anything the past has taught them to be more conservative and they are diluting and raising capital cushion probably at the right time.

While discounting business performance and capital allocation track record we should also be considerate of the operating environment and challenges thereof.

Disc: Invested from lower levels, booked partial profits in the 1400-1500 range.

It was good to finally see some tangible updates on the plan for the Edge DCs and progress updates on the Chennai and Kolkata DCs in their presentation! They seem to be on track. Of course this is just the cherry on the cake.

An article on the demand requirement for Micro Data centre ( Edge DC ) . India requires 10k Edge Data centres as per this. Techno recvd a contract to build 100 Edge DCs from Railtel…

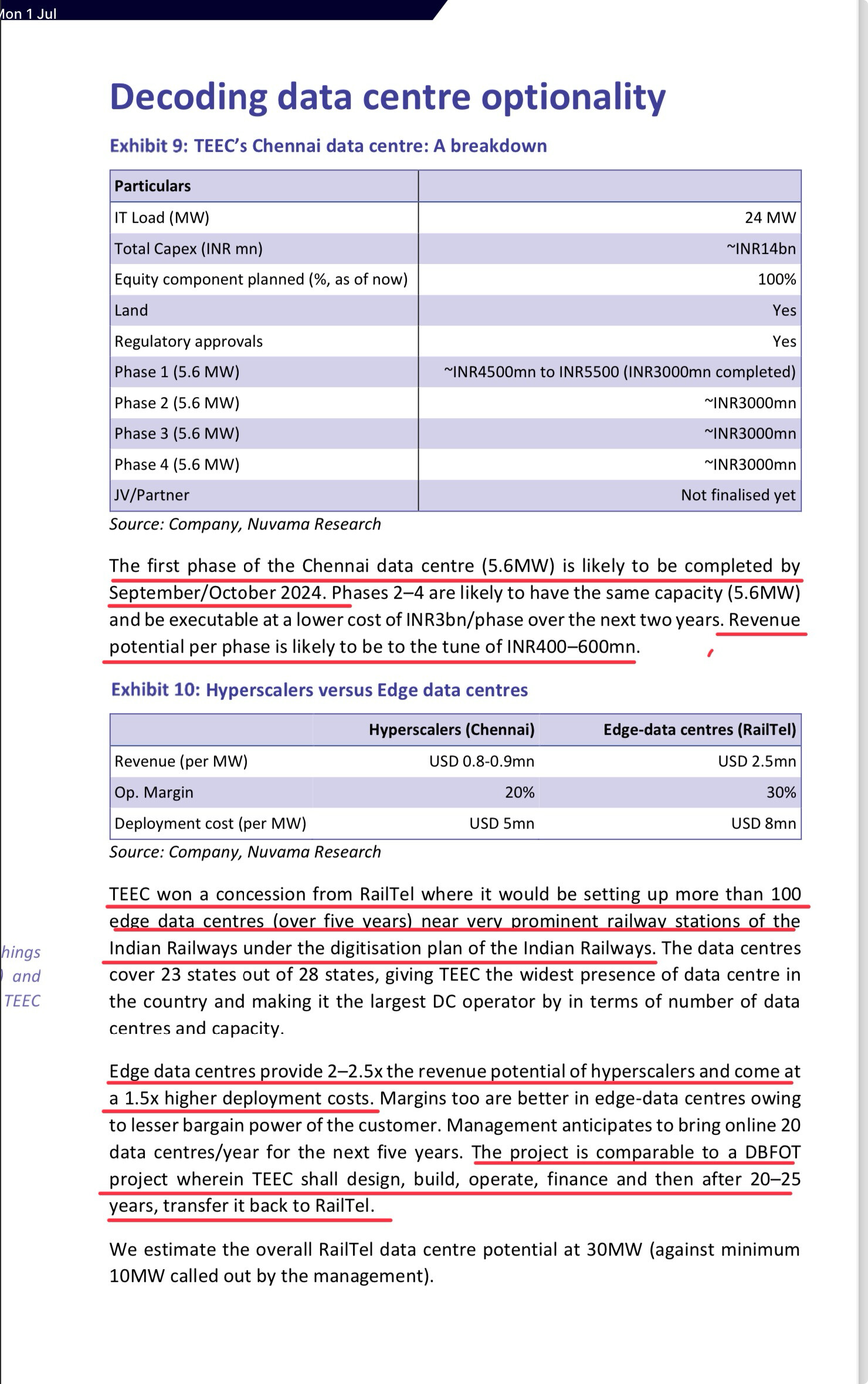

The above details are from a Report by Nuvama Research. This has answers to most of the questions on the Edge DC order. In case of the Railtel order the Land is provided on lease to Techno ( confirmed in con call) .

They were targeting 500 Cr annual revenue from FGD business in the coming years. As of Sep 30th, FGD order book was 1200 Cr out of 9500+ Cr. To that extent, it will impact their revenue.

More importantly, Q3 results are critical to understand a couple of things -

Management said H2 will be ~1600 Cr revenue against ~900 Cr in H1. We need to see how it pans out. Anything less than ~650 Cr in Q3 will raise doubts about meeting FY25 projection of 2500 Cr.

Status of Chennai DC - Original go live for phase I was September 2023. Got delayed to March 2024 and further to late 2024. While we can give management benefit out doubt on a pilot DC launch, even as of October they were not able to give firm date, which is a bit worrying.

More clarity on EDGE DC. In the last concall, management could only explain at very high level - something like 20 DC/per year. Also, if taking up EDGE DC moves out some dates for Chennai DC, management needs to be clear in communicating that.

In general, they tend to over promise in con calls. Already stock price is cracking (below 40W EMA this week). If they dont walk the talk, market may not be too patient, especially given the current market mood. This is my sense - I could be wrong.

Valuations are correcting across the board in small and mid caps space. Stocks commanding 60/80+ p/e were bidded up just because of very high liquidity and not necessarily because of fundamentals. Too much cash chasing a few fancied stocks can expand their multiples in a way that may not be justified by earnings or business models but in euphoria of bull run, retail investors find a way to do that.

Now liquidity has been slowly disappearing from market in general and small/mid caps in particular, we have seen valuation corrections to the degree of 30-70% in some of the stocks that went up 3-8x in no time.

Nothing wrong with company though. Stock has been a multibagger over the years. It’s just that buying a stock at any price, ignoring valuations, in bull market can sometimes cause a bit of pain. So unless all that liquidity comes back (which I highly doubt), we’ll have to contend with earnings to do all the heavy lifting on price action.

PEG ratio differs person to person ,

PEG= PE/CAGR Growth anticipated in next 3 or 5 years in PAT

in this case PEG in screener is calculated based on previous 5 or 3 years growth , which is not a correct matrix in this case, because techno has changed its past strategy a lot and is being guiding for around 5000cr sales in fy 27 its like 3 to 4 times of current revenue, on that basis you can find the PEG very low even today

Surprise to see techno falling so much, the reason why its falling so much is purely due to deepseek developed by china but what people forget to see is out of the total orderbook of about 10800 crores only 330 crores is related to data center its not even 3% of the total order book

Whatever guidance management has given for fy26 and fy27 for 50 and 75 eps still looks achievable…need to see management commentary post results i dont see much downside from this levels if they stand to there guidance