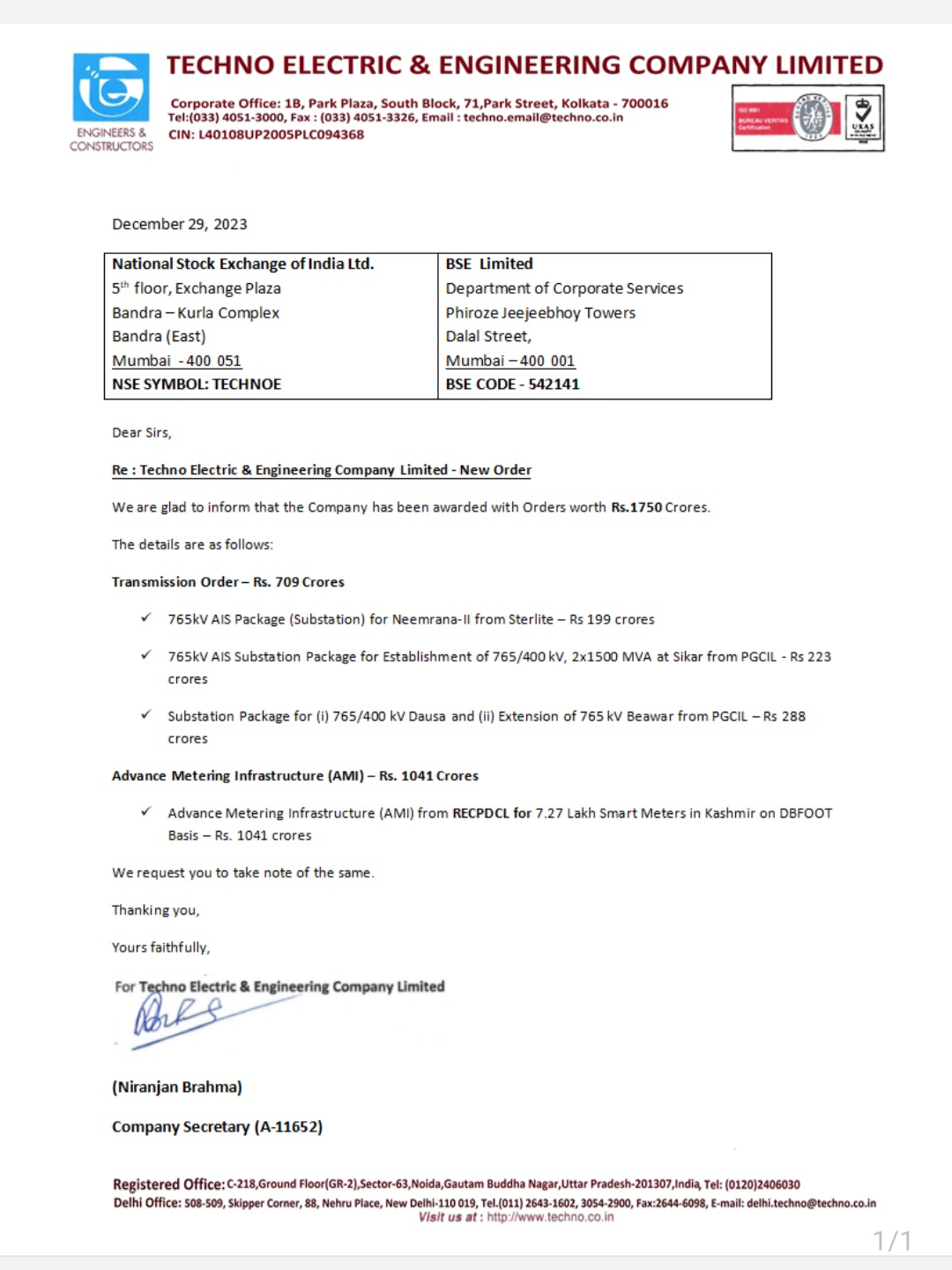

Techno wins 1750 Cr. Orders

4 Likes

Query - is this T&D segment competitive or complimentary to Skipper Ltd?

complimentary to skipper !!

Skipper might be supplier to techno co.

Can you help break down the difference and explain how it Skipper be a supplier ?

Trying to understand how Techno Electric is setup.

Techno is EPC player.

Company wins tenders from Transmission companies to implement the project like Powergrid.

As part of contract, either transmission towers will be given by Power grid or will have to be sourced by techno .

Skipper is one of vendor company which is manufactures Towers. That’s why, skipper is vendor to Techno.

4 Likes

FY26 guidance

Revenue : 3000cr

Profit : 500cr+

FY24 revenue guidance 1800cr

In 765 kv power segment, techno electric has market share of 50-60%

5000cr order book

Out of which 1000cr will be executed in this and next quarter

Expecting another order of 1500cr in near future

So should end this FY with 5000-5500cr order backlog

2 Likes

Huge underperformance in topline growth but margins holding up is great.

1000cr revenue guidance in Q3 and Q4 combined doesn’t look possible now.

Also they will raise 1250cr not sure why.

Let’s see what they say in the concall ![]()

Disclosure : Biased

6 Likes

I did a thesis post on Techno’s data center business on X yesterday. Here is the content:

Techno Electric is among India’s best power EPC companies by capabilities, having market leadership in 765Kv transmission, and a very good standing in smart meters, FGDs and other power EPC. But it’s their data center business plans that I am most excited about!

High level story:

A super conservative man like Mr Gupta who has been hoarding cash on the balance sheet for years is talking about taking on 5000cr of debt by 2030 to make an investment of 15,000cr to develop 250MW Tier 3+ and Tier 4 data centers suitable for hyperscalers. I sense he smells a seriously disproportionate opportunity.

The present estimate:

The construction of a 24MW data center in Chennai is underway and phase 1 is near completion. In the last call, they mentioned bringing in a person from Silicon Valley for the data center business, who will probably help them broker a deal. Similar deals have been happening at 100-150cr/MW globally. So conservatively if this sells at 100cr/MW, we have a 2400cr sale right there.

Now Techno spends somewhere between 40-50cr/MW in development. If they are able to sell close to 100cr/MW, thats a very high RoE capital gain. Going forward, they will likely fund a part of future investments with debt, increasing the RoEs even more!

The analogy and model:

There should be significant demand for Tier 3+ and Tier 4 data centers. Mr Gupta has not been very clear on whether they plan to build and sell / build and lease themselves, or if they want to use this first project to prove capabilities and then take on high end data center EPC work. If it’s the former (I hope it is), I’d think of this business analogous to a high end real estate (high RoEs) developer where only a few players can compete and demand is not a problem. If it’s the latter, then it’s analogous to a specialist high margin construction / EPC company in a booming construction cycle. It could be a monstor of a business if they are serious about the 250MW plan over the next 5 years. It could dwarf the existing EPC business in scale and valuation.

Their right to win:

Robust and reliable power infra is one of the main competencies needed for hyperscaler data centers as downtimes are not an option for Tier 3+ and Tier 4. Techno has this covered better than anyone else I would imagine. The other competemcies like internal connections, cooling systems, rack reconfiguration etc are probably easier to master with the right investments is my understanding - happy to learn more about this from domain experts.

Valuation and risk-reward:

This when the entire company is at 6500cr EV with a rapidly growing and profitable EPC business which they are guiding will do sales of 2500cr (~40% growth) in FY25 and 3200cr in FY26. So the EPC business alone is valued at 2 times EV to FY26 sales, for an industry leader in a sector experiencing massive tailwinds. The story will obviously come down to execution, and this is the main risk.

Please do your own research. I am invested and biased, and as you can see, I’ve done a lot of projecting and guess work. I could be completely wrong in my assumptions.

Disclosure: Invested in the last couple of weeks with a mid sized allocation for now (5%).

28 Likes

Hi @nandan_ganatra ji, can you please suggest me the last how many concall i should read to understand about Data centre and company guidance, as I am very new to this sector and really gratitude towards your constant sharing of wisdom on this company and sector.

Thanks.

- If you want to read about data centre, then go through this article - which is very well written

Also there is techno electric video available on youtune on data centre which is a must watch, as it gives in depth details about industry functions ![]()

- To understand Techno electric business ( EPC+ DC ), you should read atleast last 3-4 of their concalls to get to know about how management is progressing in their business. And it will also help you understand in future weather management is walking the talk or not.

11 Likes

Hey Nandan, saw your analysis very helpful, i am stuck at understanding one thing, help me understand it better , i went through the management interview of techno by B&K where he states that, “data centre cost is around 40 to 45cr per MW in india which is not very different from USA or other countries” , source : YouTube Transcript - read YouTube videos

so what incentive does outsiders have to setup their data centres here in india ? apart from “data stays in country” and “low latency” any other advantage they have ? or did i miss- understood something on the cost side ?

anyone can answer studying this sector.

2 Likes

Data center are classified under Tier 1 , 2,3,4 and accordingly cost varies depending on the category of Data centre being build up. India can offer itself as one of the reliable cheap data center partner.

2 Likes

Apropos the discussion in their latest con-call, about the ‘Edge Data Centers’ they are building for Railtel. The business model was not very clear. If they are building these for Railtel on the Railways property, using Railways’ fiber (they specifically alluded to that), wouldn’t the DCs be owned by Railtel? But Techno Electric management spoke of these edge DCs as if they were extensions of their own DCs.

Does anyone have some insight into this please? Thank you!

2 Likes

Intersting. I posted this morning on data center by Railtel.

You may like to watch if it helps !

1 Like

Agreed, another company is moving towards high Kv transmission products and will be the only one in the country to manufacture such products. So yeah, it seems like the transition to Higher Kv lines is on track.

In fact, the way I see it, it seems to be a very good investment idea just based on the electricity EPC part of the business. The Data center piece would be icing on the cake.

2 Likes

Techno is raising funds from Market by the way of QIP at the floor price of Rs 1506.58. The offer price is 0.7% premium to the last closing price. Their release did not mention the quantum of funds to be raised from the market. They are debt free and hold a cash kitty of Rs 1200 crores. Unable to understand the reason for raising further funds from the market.

Discl: Invested

1 Like

Funds are for their data center vertical. They have committed around 1.3billion usd for this vertical over next 5 years to be funded through cash kitty, future cash flows and qip funds.

5 Likes

Massive lineup of fund houses despite the allotment price.

2 Likes

https://x.com/mukesh634/status/1814703252950429720

Different prespective of Techno Electric’s past. Will the future be different?

Disclaimer : Invested from 400 levels.

4 Likes