But wasn’t that not too big a component of their earnings? I don’t remember how much exactly.

I am personally quite suprised that it continues to fall. Does the market know something we don’t? Else I don’t see a reason to correct so much!

But wasn’t that not too big a component of their earnings? I don’t remember how much exactly.

I am personally quite suprised that it continues to fall. Does the market know something we don’t? Else I don’t see a reason to correct so much!

techno launched.pdf (576.9 KB)

techno electric launched for hyperscale data centre

Good to have a separate entity on data centre. But on ground, we need to understand when the Chennai data centre will start business. it has been delayed multiple times. On railtel DCs also, there is no clarity - they keep talking about at very high level.

Having said that TECHNOE core business has good probability of doing well over the next couple of years. Need to watch cash flow very closely.

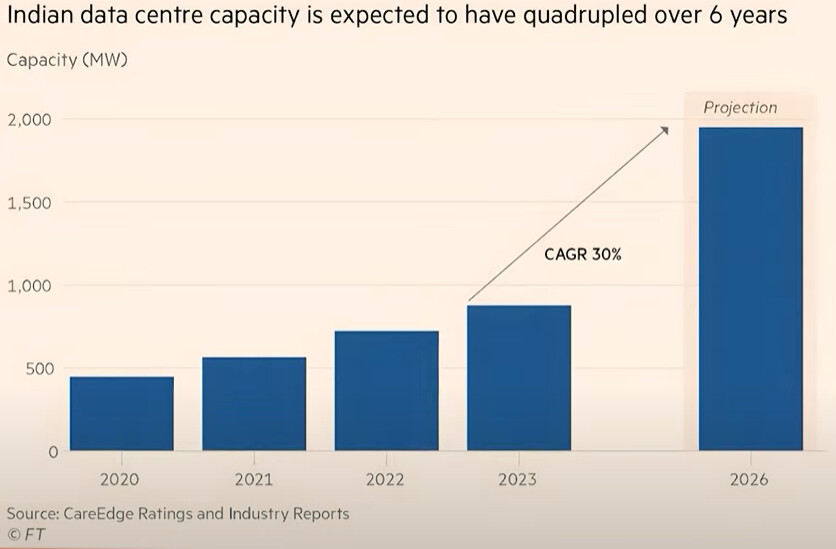

According to the article-does 100billion$ is new investments in datat centre or 100-60=40billion$ in 2027?

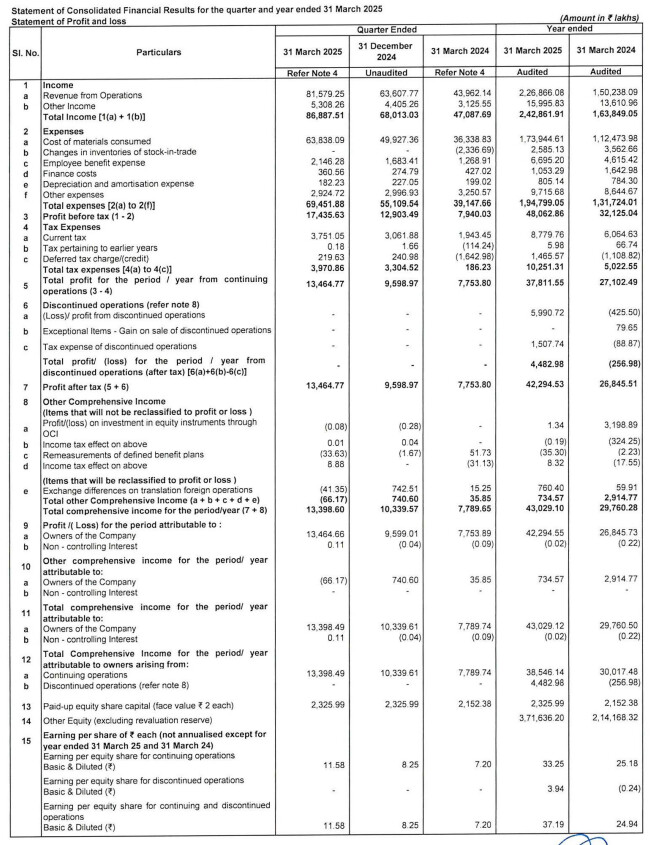

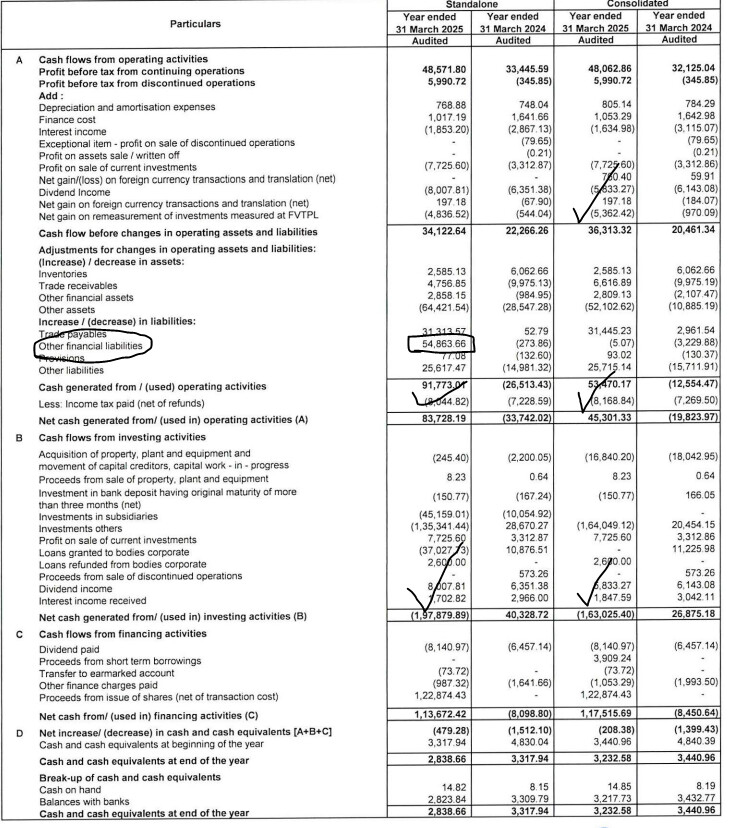

what is included in Other Assets? That seems to have gone up significantly, while Other financial liabilities have also significantly gone up.

RailTel Corporation of India Ltd. has awarded a significant domestic contract to M/s Techno Electric & Engineering Co. Ltd. for establishing a 10MW Data Centre in phases at Noida. The selection was made through an open tender process, with Techno Electric appointed as the Managed Service Data Centre Partner.

![]() Key Highlights:

Key Highlights:

How Will FGD Relaxation Impact the EPC Order Book of Techno Electric?

The government’s recent decision to relax the 2015 mandate on compulsory installation of flue-gas desulphurisation (FGD) units in thermal power plants could have a serious bearing on EPC players like Techno Electric. Around 79% of thermal capacity now stands exempt from FGD rules. So what does this mean for Techno’s future?

Let’s unpack this.

Is the ₹98,000 crore FGD opportunity shrinking fast?

Techno has already executed FGD projects worth nearly ₹1900 crore and was aiming for an annual FGD order inflow of ₹1000 crore. With only plants near million-plus cities, in polluted zones, or using imported coal now needing FGD systems, the remaining pipeline could shrink sharply.

What happens to the ₹319 crore Bokaro A project and others in the tendering phase? Will we start seeing order cancellations or indefinite delays?

What does this mean for margins and topline growth?

FGD jobs tend to be margin-accretive and form a key part of Techno’s growth narrative. If this segment dries up, how quickly can the company reallocate resources and bid more aggressively in other verticals like transmission, data centers, or renewables? Can the EBITDA profile be sustained?

Is there a second-order benefit here?

The cost savings from not implementing FGDs may free up capital for state utilities and private players. Will this eventually boost spending on other infra segments where Techno already has competence? Could we see an uptick in orders for T&D infrastructure instead?

Could there be a pivot to lower-cost pollution control solutions like ESPs?

Electrostatic precipitators cost just a fraction of FGD systems and are gaining policy traction. Does Techno have capability here? Is management already thinking of this shift?

How much of the FGD risk is priced into the stock already?

Bottom line

The FGD relaxation is clearly a setback, but whether it’s a bump in the road or a structural drag depends on how Techno responds. Order visibility, pivot speed, and capital allocation strategy will be critical to track over the next few quarters.

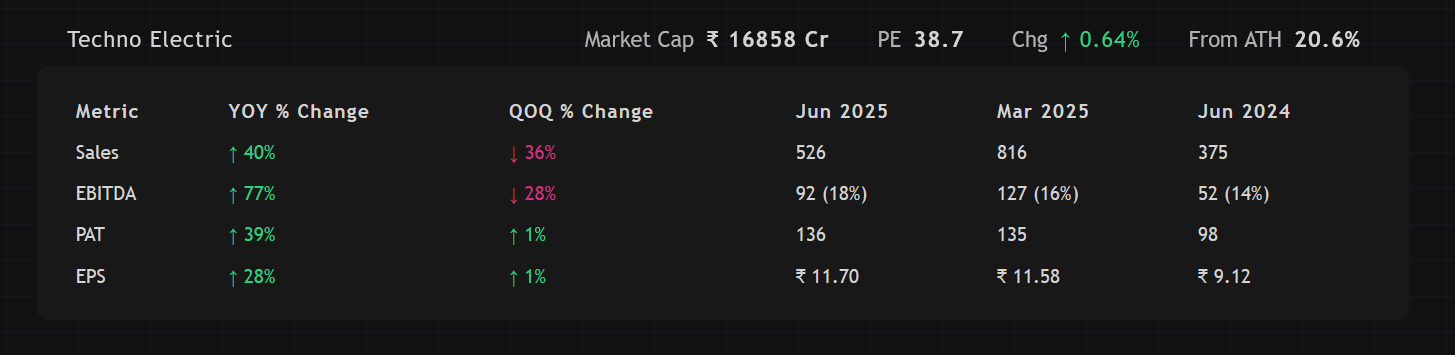

Q1 FY26

Performance:

Concall Notes:

14% plus/minus will be the benchmark, as I have always guided and we have achieved consistently. The further improvements will happen only by our data center business now happening and somewhat out of the AMI business, which are the asset-based businesses of the company. So club together, you may find some improvement year-on-year.

80 gigawatt of additional thermal capacity is planned by 2030 to meet the peak demand of 400 gigawatt, focus on ultra-supercritical and supercritical plant technology, which means lesser coal consumption and also emission thereby. The EPC scope as a balance of plant will continue to be there. We’ll have a scope to deliver at least the grid connectivity part as well as the electrical elements for auxiliary systems. The estimated EPC opportunity is about INR80,000 to INR1 lakh crores over 7 years, out of which we intend to make around INR500 crores per year.

Guidance:

Maybe it will be more visible from INR100 crores to INR200 crores next year. And this year, we are in the process of building up of the capacities like Gurgaon, Bombay, Chennai. So these 3 facilities will be ready for deployment. So I will say conservatively INR25 crores, but maybe more.

Shareholding:

Disclaimer: Invested

Good read on the FGD landscape in India

Do they provide revenue breakup between EPC, smart meters, FGD & data centres?

They do not provide revenue breakup in my understanding. But you can derive the numbers from the order book breakup.

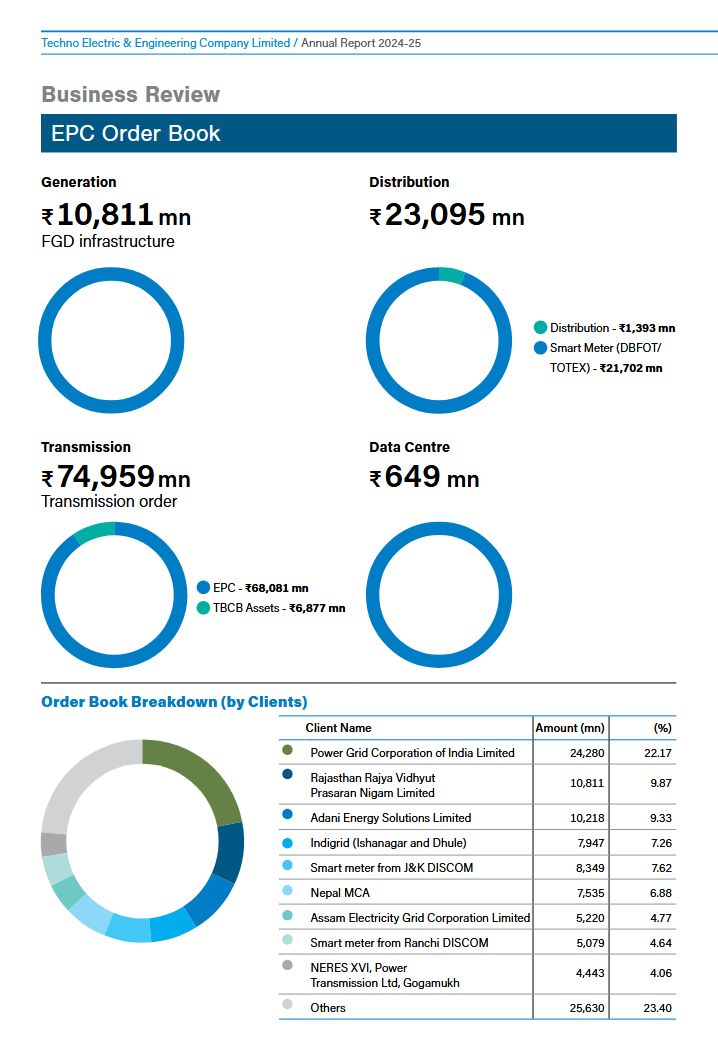

Transmission: 7495 Cr

Distribution: 2309 Cr

Smart meters (within distribution): 2170 Cr

FGD: 1081 Cr

Data centres: 65 Cr

But the proportion seems to be changing every year. How come data centre orders were 422 Crs in FY23 end but only 62 Crs now. Did they execute any orders?

I am not sure about the source of 422 crores of data center orders which you are referring to.

They have given a long term guidance

A vision to build an interconnected network of hyperscale and edge data centers across India, with a planned investment of $1 billion over five years. The goal is to achieve a cumulative data center capacity of 250 MW by 2030.

This was the last data center order win by them:

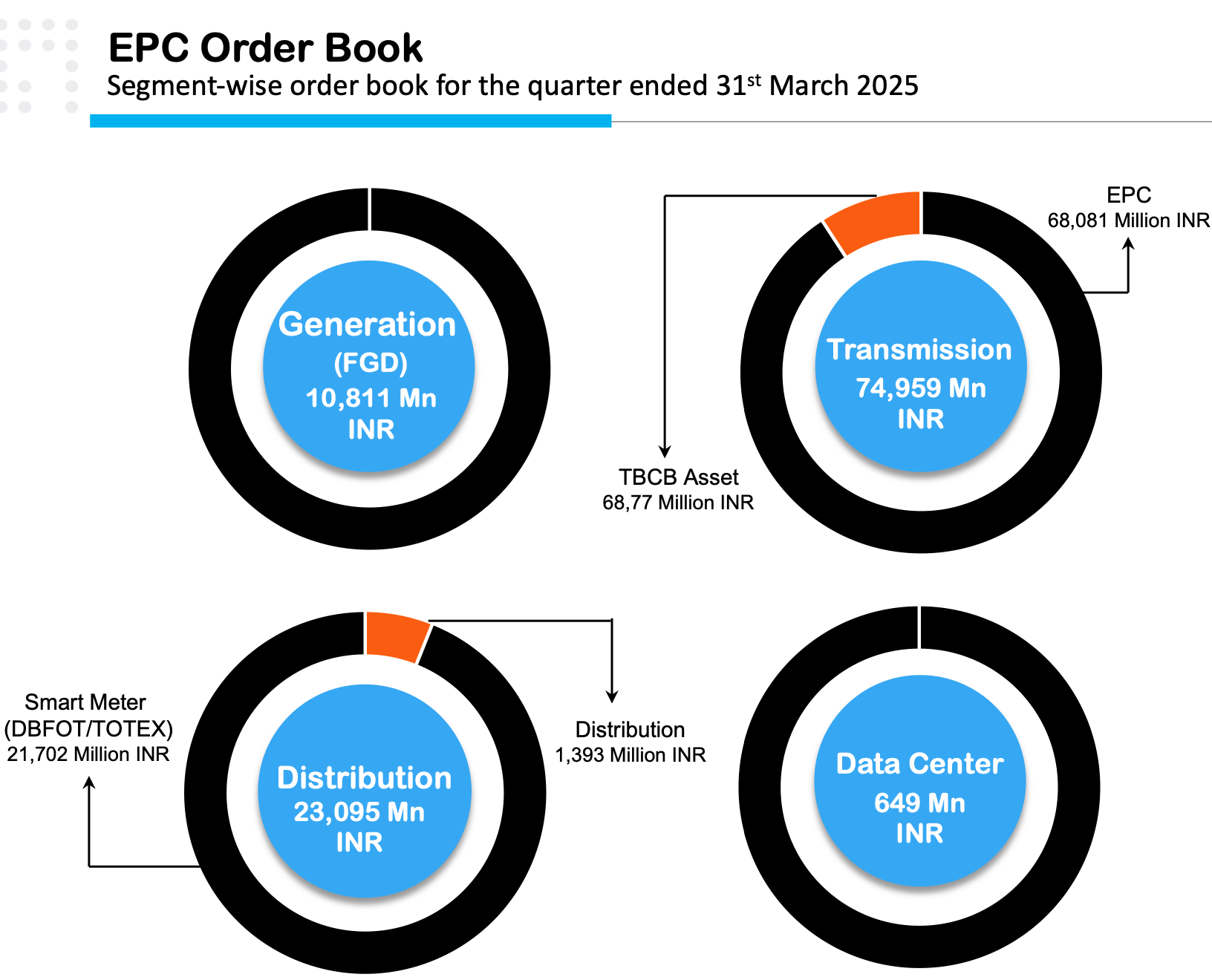

Snapshot of the current orderbook:

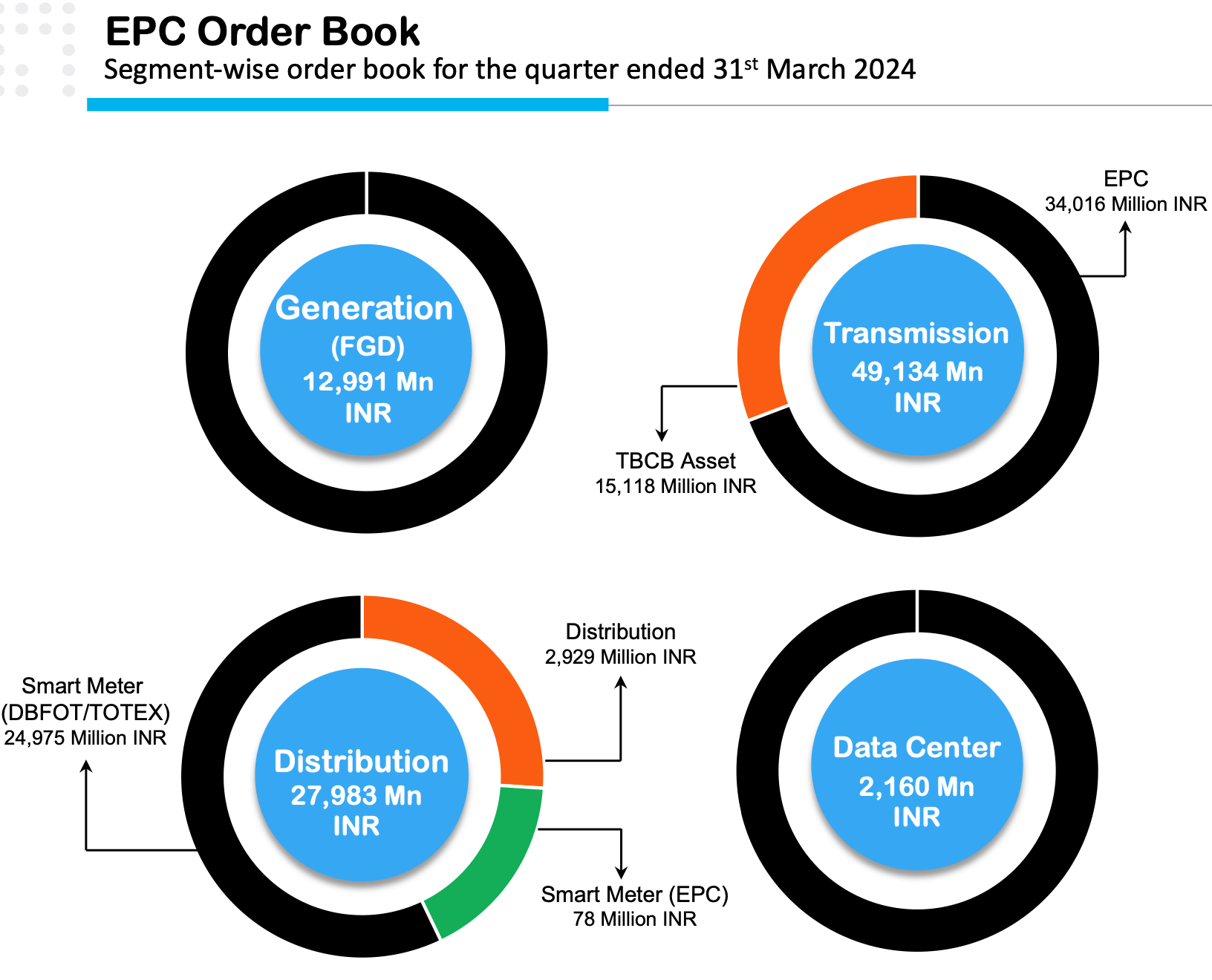

This is their order book over the years-

Data centre orders have reduced from 422 Crs in FY23 to 65 Crs in FY25.

Techno’s data centers are not typical EPC projects but rather asset-based businesses. This means that instead of receiving a contract from a client to build a data center, Techno is setting up and will operate these data centers on its own balance sheet. Therefore, the value of the work done on these projects is not classified as an “order book” in the same way as their EPC contracts.

In the 2023 annual report, the ₹422 crore data center order book mentioned likely refers to the company’s investment in the Chennai hyperscale data center.

Therefore the decline can be attributed to the company classifying the capital expenditure as work-in-progress and capitalizing it as the asset gets closer to commissioning, rather than it being a contract that gets executed as revenue. As the projects progress, the value of the order book decreases because the work has been done and the capital has been deployed. This is just my understanding and I might be completely wrong.