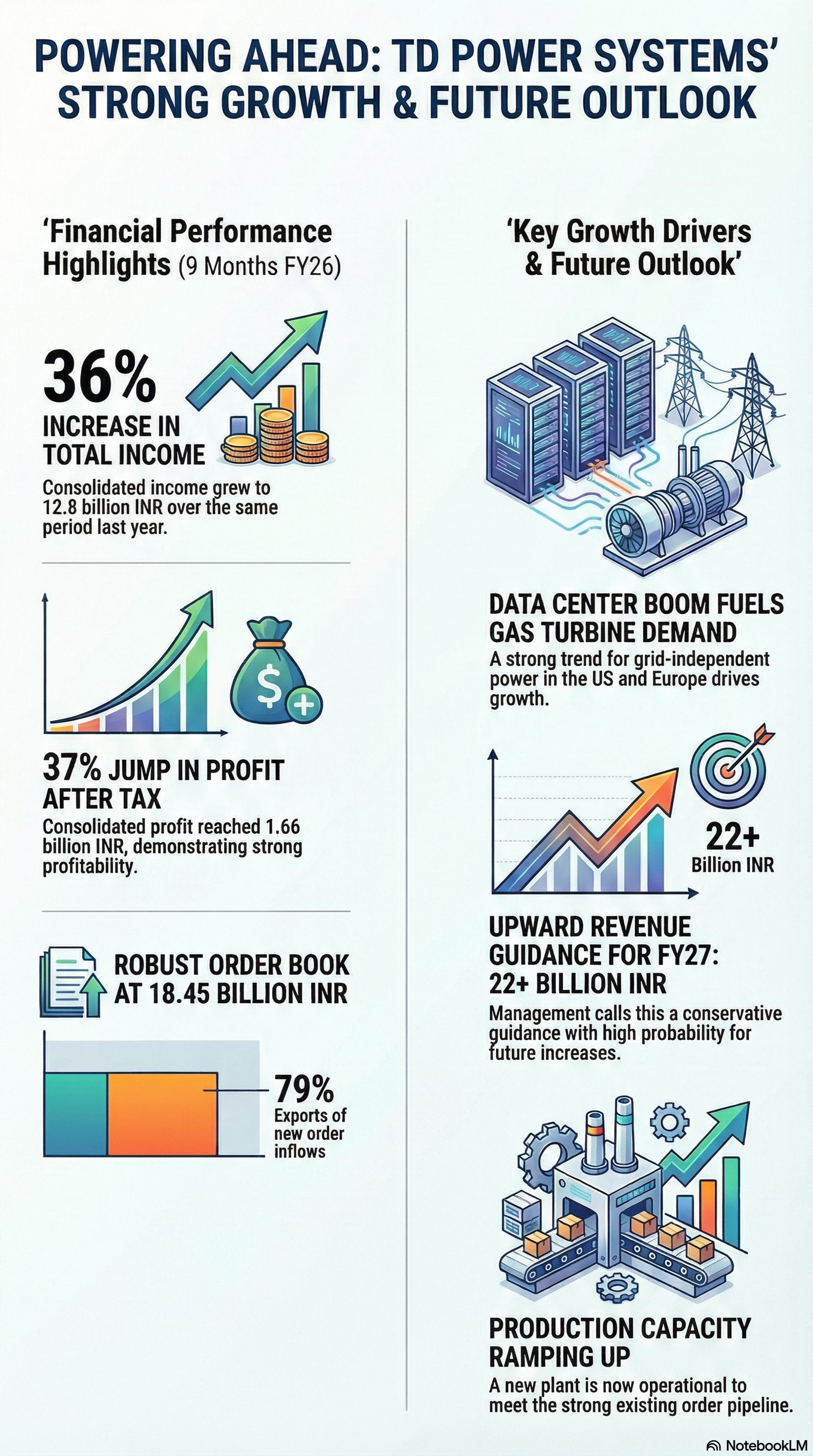

US gas-fired turbine wait times stretch up to 7 years; costs jump sharply: A tailwind for TD Power?

The US gas turbine market is seeing a massive demand spike driven by data center growth (AI, cloud), manufacturing expansion and broader electrification. Some key takeaways from S&P Gloabl 500 report:

-

Wait times are stretching to 5–7 years for certain models, as global OEM order books hit record highs. Even the shorter lead times are now 1–2 years depending on the turbine frame.

-

Costs have risen sharply. Building a new GE H-class combined cycle facility is now ~2.5x more expensive than just a few years ago, with EPC, equipment, and materials all inflating.

-

OEM backlogs are at historic highs i.e Siemens, Mitsubishi, GE Vernova all reporting strong bookings. Siemens’ gas services just recorded its highest ever quarterly orders.

-

Data centers are a key demand driver. A single hyperscale campus can need 1 GW+ of capacity, which gas-fired turbines can efficiently deliver.

-

Mitsubishi and Siemens confirm demand will stay very high for at least the next 3–5 years.

Why this matters for TD Power Systems (TDPS):

TDPS manufactures and supplies generators for large turbines. With global OEMs like Siemens, GE, Mitsubishi facing swelling backlogs, they need reliable supply chain partners.

Long-term, the “gas + renewables” mix remains critical for stable grids, meaning steady, structural demand for turbine-generator sets.

Rising costs and bottlenecks for OEMs can actually strengthen TDPS’s positioning; if they can execute on deliveries efficiently, they become an even more valuable supplier.

This demand cycle is not a short-term spike but tied to secular themes like AI/data center power demand, grid stability and industrial growth.

In short: Global gas turbine demand is entering a multi-year upcycle. For TDPS, which is closely tied to this ecosystem, it represents a strong structural tailwind.