Yes but expecting it to be a stable compounder not trailblazing growth. A 25% cagr grower over the next 2 years. Waiting to see how the Tractions business shapes up with higher margins and the new capacity to come online. Not complaining, the company delivering what it said but I guess its priced in.

8 Likes

The company is demonstrating robust growth; however, its 5-year CFO-to-PAT ratio is only 45%, and FY24-25 CFO/EBITDA is at 20%. What might be driving this low CFO conversion? Could it signal potential future QIPs or debt raises to support working capital needs?

4 Likes

The management of TD Power Ltd has clarified that the company has secured a healthy inventory of copper and special steel at attractive prices, anticipating a future rise in commodity costs. They continue to maintain a strong cash position of over ₹200 crore, which indicates no foreseeable issues with capital requirements. Furthermore, all ongoing capital expenditure is being funded entirely through internal accruals. As discussed in their concall today, the company has also made good progress in recovering outstanding receivables as at March 31, 2025 and they said 80% of o/s receivables are less than 90 days.

7 Likes

slight decrease in topline from Dec to Mar. should we be concerned about this and is order book getting thinner?

2 Likes

Q4 FY25 Concall Summary

- The current manufacturing segment’s order book totals 1366 crores:

- 1012 crores for regular manufacturing business

- 316 crores for railway business

- 11 crores for states and aftermarket

- 29 crores for Turkey business

- Highest quarterly order inflow of 413 Crores

- Domestic market is dormant with only 4% growth mostly driven by captive power plants and select green/brownfield investments. Hydro refurbishment can help them deliver double-digit order growth if their bids succeed. Indian railways orders are currently muted.

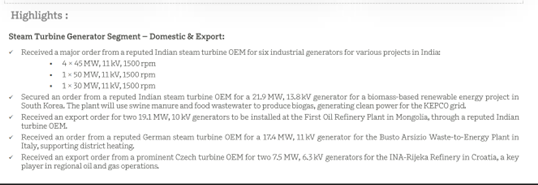

- Exports is the primary growth engine for them with strong growth in order books of gas turbines, engines, motors.

- For their Traction Motors segment, Prototype deliveries underway for Germany, US, and CIS and they have firm contracts for FY27 and they expect good volumes of order, with impact in FY27.

- They have secured business for 40-45 MW sets in large data center farms which unlocks a TAM equivalent to their current market. They see huge market potential from FY27 and could be 25% of their total revenue.

- They received an order in Turkey after a pause, but the local regulations and guidelines is making Turkey operations unsustainable and they are planning to shut the plant post this order completion. However, they are a known brand there so they will likely export in the market.

- They believe they can sustain 36% as the gross margin with slight deviations. Also, they clarified that staff costs are not being capitalized.

- Increased net working capital days which affected the operating cash flows. This was due to:

- They built their inventories by buying significant quantities of copper and electrical steel when prices dropped due to the tariff situation.

- March is invoicing heavy time which lead to higher receivables

- They expect significant improvement in their cash flows from Q1 as they utilise the cheaper raw material and collections from March will be realised in H1.

- Tariff Implications:

- The demand is very high and the OEMs are passing the cost to the customers.

- AI related machines are imported from Europe in US, so if a trade deal with India comes out faster that can give them an advantage over their peers.

- As long as tariff rates for imports from India and Europe remain comparable, there shouldn’t be a significant advantage for US customers to choose one over the other.

- Design Center in UK as talent pool for larger machines (up to 100 MW) is concentrated in the region. It will also help in improving the existing designs and to enhance their technology for larger machine.

- The new plant’s commissioning is on track, with its financial contributions expected to materialize in the second half of the fiscal year.

- What happened in Spain and Portugal:

- The blackout was triggered by a sudden and significant drop in renewable energy production (wind and solar) across the region.

- Since there was insufficient immediate backup power to compensate for this loss, the remaining grid became overloaded which lead to a domino effect and lead to progressive grid collapses.

- This has opened another tailwind as governments are now looking at gas power to stabilize the grids more seriously.

- Historically, the company has executed around 60-70% of its annual order book as revenue. However, last year saw high execution rate of approximately 110%. The management acknowledged the current guidance suggests a similar 110% execution and such trend to continue.

- Dividend payout is not a priority and they are investing in growth by conserving cash and fund any initiatives using internal accruals.

- The primary competitor for NPCIL orders is BHEL. The current order is for replacement motors for existing Russian equipment in the nuclear power plants. The execution timeline for the current NPCIL order is within the next 12 months.

- They feel that they can achieve 20-25% of their revenue from US in the next 2 years.

- Guidance:

- The initial guidance for FY26 is set at 1500 crores with potential for upward revision due to sustained order inflow and the new third plant becoming operational in the second half of the financial year. Margins are expected to be in the range of 18% to 18.25%.

- They also believe that with strong demand and order execution of traction motors they can achieve 1900-2000 crores revenue in FY27.

- Revenue growth up to 2200 crore will be achieved by optimizing the efficiency of their existing capacity. No new capacity addition is planned until the revenue reaches this level.

The management sounds confident/bullish about the future.

Let me know in case of any errors

Disclaimer: Biased, do your own diligence

31 Likes

Considering the potential future trade implications between India and Turkey due to Turkey’s alignment with Pakistan in the recent conflict, do you foresee any mid- to long-term impact on TD Power’s plant in Turkey and its associated business operations?

2 Likes

I think if you will read the con call they have mentioned that they will close their turkey operations due to regulations

7 Likes

Yes, they mentioned in the concall. Looks like well thought out decision in hindsight.

4 Likes

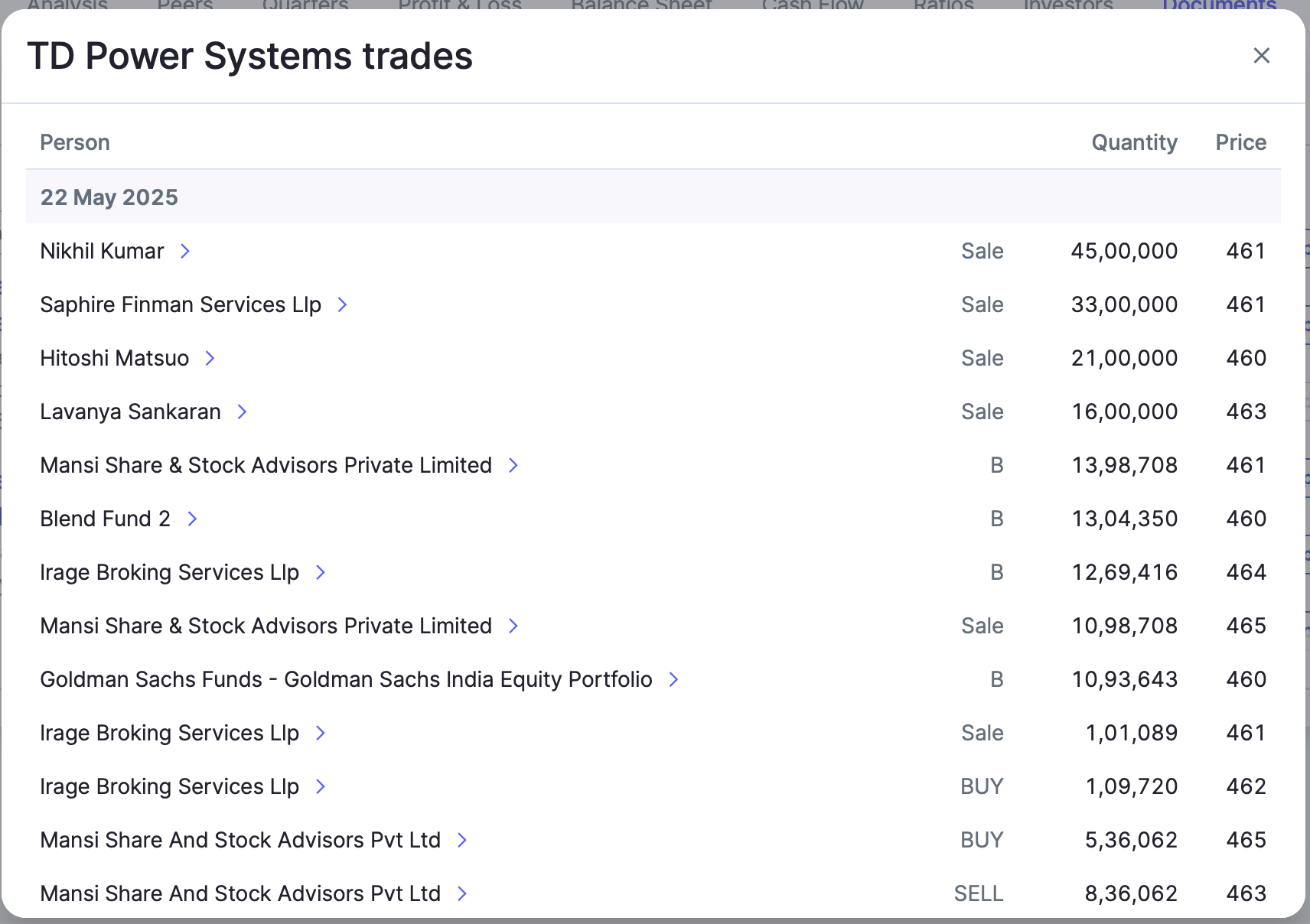

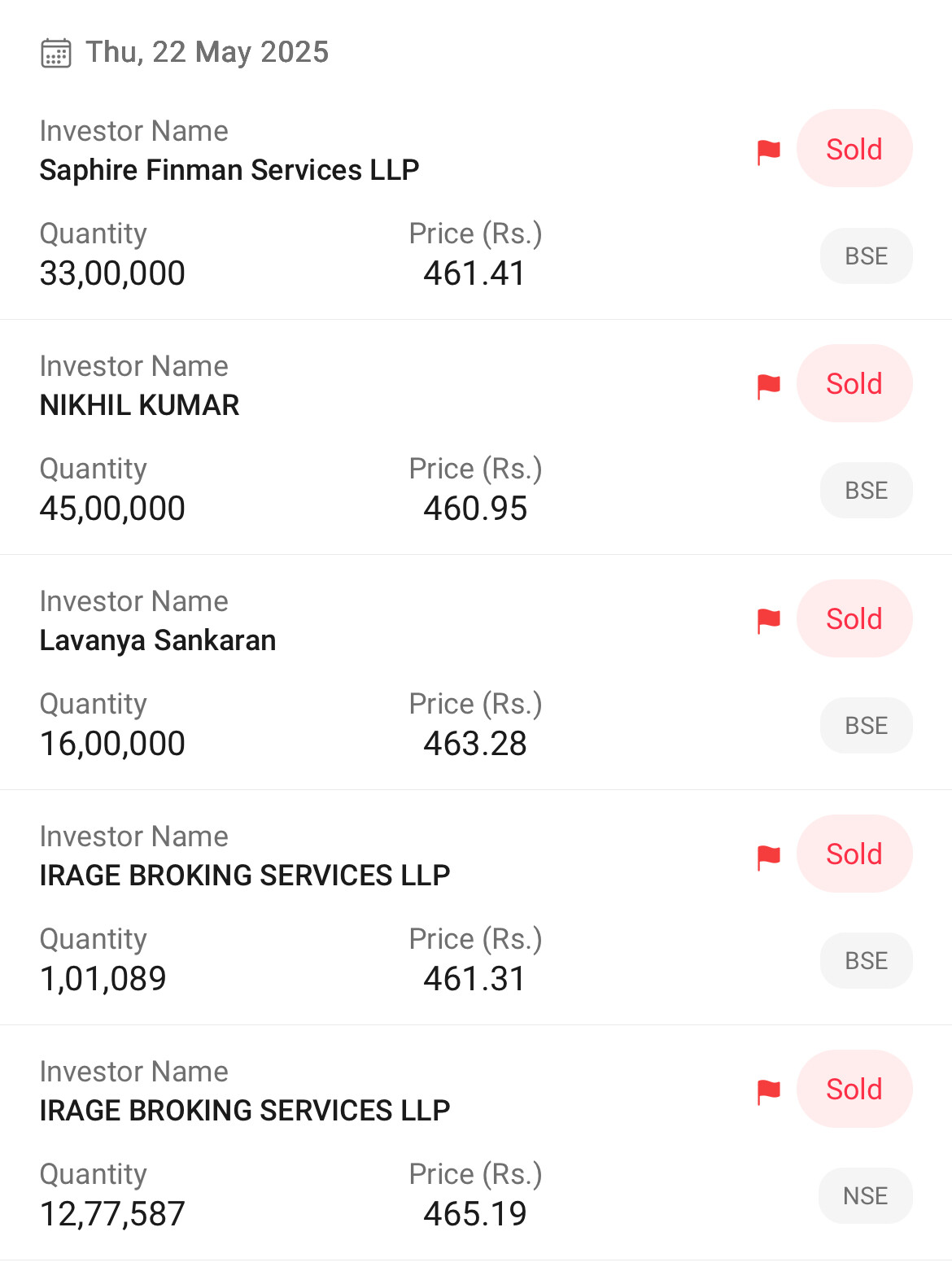

Promotor and CEO have sold 250+ cr worth of shares today. Apparently they mentioned in a concall that they had no intention to sell…

How do we make sense of this, especially following a bullish concall with clear hints of upward revision to estimates?

18 Likes

Don’t know how to interpret. May be it will unfold in next few days. But one thing is assuring to see that Goldman Sachs bought shares worth 50 cr in the block deal. So it can’t be negative.

9 Likes

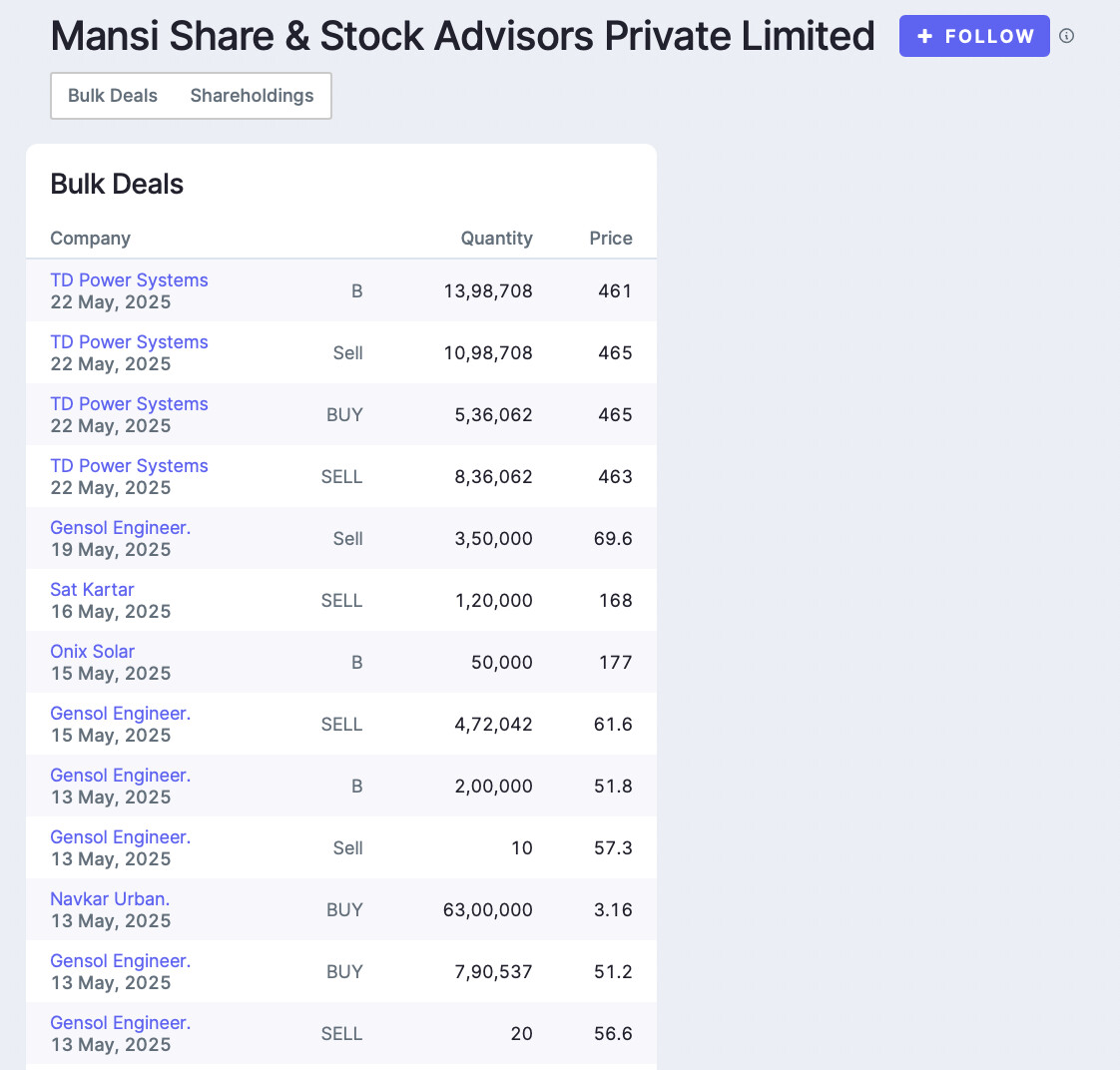

Started tracking and reading this business few days ago. The thing that bothers me is not promoter selling, it is that 5 different people accounts have sold their stake. It is not as if they had 70% ownership anyways. Another thing, One entity “Mansi Share and stock advisors pvt. ltd.” appears in the list. Going through other investments of this firm, not even one seems to be a normal company. It’s filled with- Gensol, MTNL, Zee media, etc. Attaching some screenshots.

13 Likes

13th May, 2025 “No plans to sell shares right now”

Proceeds to sell 207 crore worth of shares after 9 days.

529 Cr worth of total shares were sold on 22nd May, out of which Goldman Sachs bought 50.31 Cr and Blend Fund bought 60 Cr. 419.43 Cr worth of shares are not disclosed. Probably HNI / strategic investors bought in multiple smaller bulk deals which do not meet the criteria of public disclosure.

10 Likes

There was an ownership dispute between Kirloskar and TD power promoters.

I think they are in hurry to dispose before any adverse ruling comes on that front.

Paint a rosy picture….Sell someone’s silver.

Just a hunch.

13 Likes

Amazing Export performance by TD Power so far in Q1FY26. The first two months have shown good performance YOY. April and May months are up more than 2x compared to last year. If this trend continues in June, the Q1FY26, could end at par or very slightly lower than Q4FY25. Given that Q4 is generally the best quarter in such companies, TD Power is showing tremendous growth in exports. Top buyers are still the two European countries, Austria and Germany. USA is their third largest buyer. Domestic traction needs to be tracked, in order to estimate their topline for Q1FY26, if someone has any information in that regard, please share here.

20 Likes

Can you share the excel file for the export data please

Note:

Holding tracking position.

Hi , from which site you got export data ,i tried to check on importyeti.com but data is not available , are you using any paid service ?

Yes sir it’s a proprietary data, that our team tracks. I think it’s against the forum’s guidelines to share proprietary/paid data as it is, so that’s why I just posted an update on the exports performance.

15 Likes

Manit - Just wondering if it is just a co-incidence that which all companies you have commented in past few months, 1 thing is common - their exports have been phenomenon ![]()

3 Likes

I won’t say it’s a co-incidence. It’s a well planned screener. Our team filtered stocks where revenue from exports was relatively high compared to peers, and they sold a high margin, high entry-barrier product. Filtered a few names in this process, with reasonable fundamentals and now we actively track them. I feel it’s good to update the VP forum with this data as well, so I try to post the updates whenever I can.

28 Likes

Q1 FY 26 Concall Notes

Business overview

- 36% increase in revenue YoY; and 40% increase in Net profit

- Order book for manufacturing – 14.67 billion;

- Generator and motors business comprises around 10.8 billion.

- 3.8 billion from railways

- Order inflow: 32% increase YoY to 3918 million

- 66% is from exports and 34% is from domestic

- Demand from US & Europe is very high. Expecting good uptick in orders.

- Strong export outlook and demand

- Macros for power generation in US, Europe, etc have been strong and favourable for us

- Witnessing shortage of power generation equipments across the world

- Data centre, AI, etc driving demand in US

- Power generation equipment – very little manufacturing in US. Mostly European and Japanese companies. We are an outlier – only non-European, non-Japanese player

- 45 to 50 cr capex for FY 26 – 20 cr is replacement capex and rest is for growth

- Promoter selling – No current plans for reduction in stake for next 2 years

Segment wise

- Hydro – Received a big refurbishment job last qtr. Order values are very large.

- Railways – have orders for US, Europe, Russia and India. Expecting significant uptick in India business next FY

- Domestic market in captive steam turbines - 10 to 12% steady and broad based growth

- After market – mainly coming from hydro business. Participating in lot of tenders and expecting good orders. Its 5 to 6% of sales and will be maintained

Tariff impact –

- 15 to 20% sales from US

- 75% export to US (indirect export) –routed via the OEMs in Europe

- 25% direct exports to US – that production might be moved to Turkey. Already producing in Turkey. 15% duty in Turkey

- Will assess by end of the month. If 50% tariff were to continue in September, will have to shift manufacturing in another country, to mitigate the impact.

- No delays in customers placing orders, etc owing to tariff concerns

Production in Turkey

- Already present there for 7 years.

- Don’t expect issues in manufacturing a small no. of machines – needed to meet US demand. Production qty is manageable and doesn’t cross the pain threshold of re-routing vis Turkey. If the issue persists, might explore other geographies for more efficient production

- No labour related concern as we only need 6-10 people. Currently have 5 employees

- After re-routing via Turkey & with 15% duty – takes care of forex exchange and would be competitive

Guidance & outlook

- As of now, maintaining guidance of 1500 cr for this FY. Margins will largely be maintained. Likely to exceed guidance

- By next quarter – will give detailed guidance for FY 26 and tentative guidance for 27

Disc: Invested with a tracking position

18 Likes