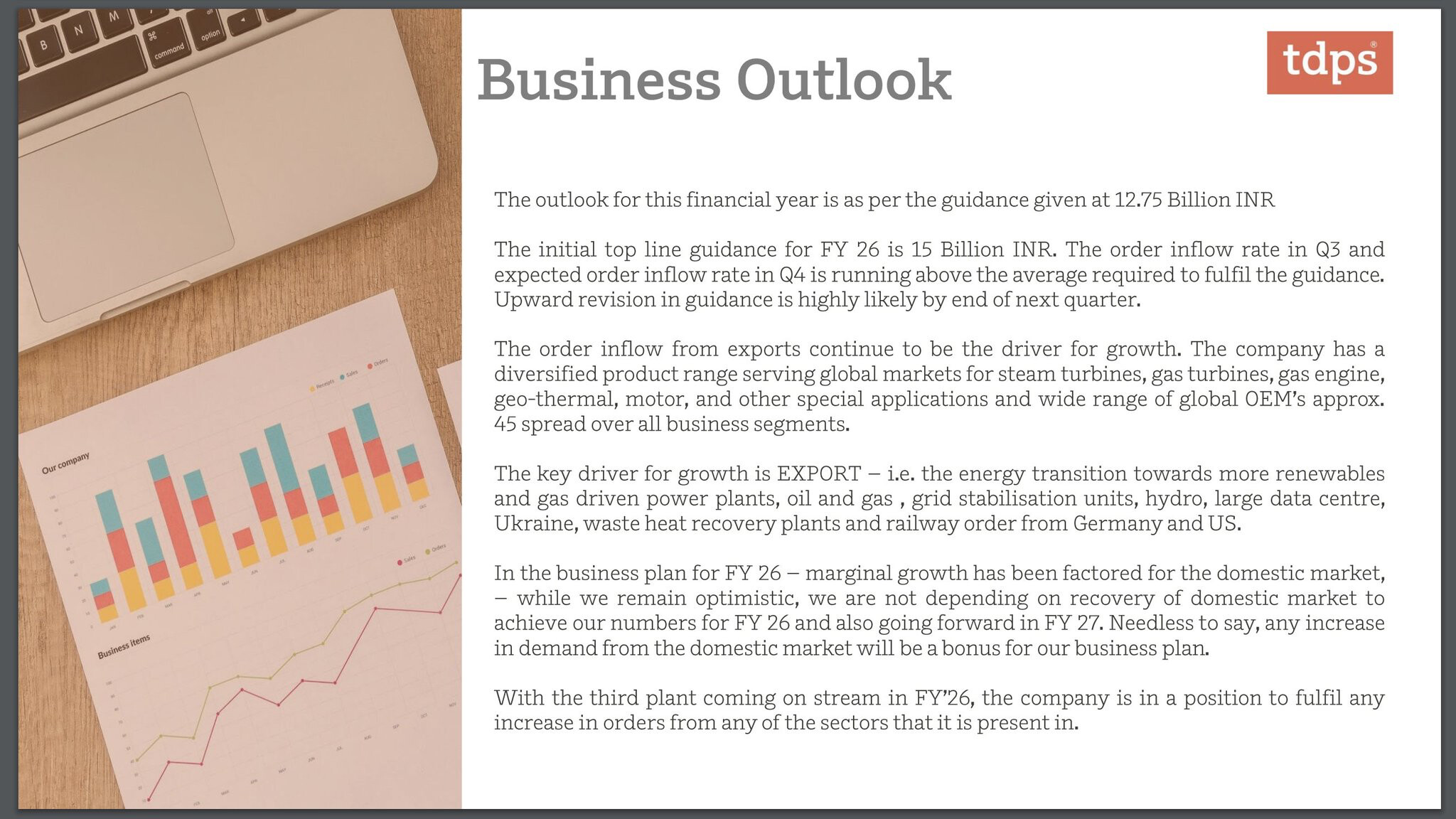

Management provided a revised top-line guidance FY25, Rev b/w 1250Cr and 1275Cr

Representing an overall growth of ~ >25%

Operating leverage : Margin growth anticipated to be 2-3% more than sales growth

Order Flow : 41% YoY increase

Company expects order inflow in Q3 to exceed that of Q2.

Management is expecting new tenders from the railways. TD power is gaining greater market share due to increased acceptance of their products

Gas Turbine and Gas Engine Business

Structural demand for gas turbines and engines, coz of rise of AI Data farms, which are projected to require b/w 200 to 500 GW of power. This demand cannot be met by larger gas turbines plants alone, as they are booked out for the next 3-4Y. Instead the smaller units (20-50MW) are expected to fulfill a significant portion of this demand.

There is definite surge in orders due to increased activity in Fracking and the ongoing need for gas supply in Europe, particularly replacement of Russian gas. US is major supplier to Europe, which is further driving demand for smaller gas units.

Geothermal and Hydro Business

Order for 3 units of 43MW for a geothermal power plant in the US and is in discussions for a potential 1000MW order in phase II. Geothermal projects yield better margins compared to hydro projects.

TD signed a PPA with major IT companies too.

Traction Motors

5Y contract for traction motors, this business can goto 60-70Cr per year

Something to watch out from this space. Significant order might be incoming

Increase in inventories and cash flow : ramp up in prod required securing raw materials to avoid disruptions. Coz of capex and hiring in Q4 we might see some increase costs.

I’m fairly new to this company, going through their presentations and concalls there is little to no information on the realizations, unit economics, Revenue share of their products. Also if any of the experts here can tell who their competitors are for various products and what exactly is their competitive edge. Also if there any reports that discuss their Opportunity size across products globally. Thanks in Advance!

Current guided Revenue growth for FY 25 - 25%

Revenue FY 25 - 1250 cr and PAT would be 160 cr

Estimated Revenue FY26 (18% growth) - 1475 cr and PAT (taking current profit margin without mentioned increase of 2-3%) would be 189 cr

Exit PE of 50 → FY25 gains could be from current price of 399 → 28%

FY26 gains could be 52%

Gains could go higher in case of guidance revision as mentioned by promoter in concall that guidance for FY26 would be revised in Feb 24.

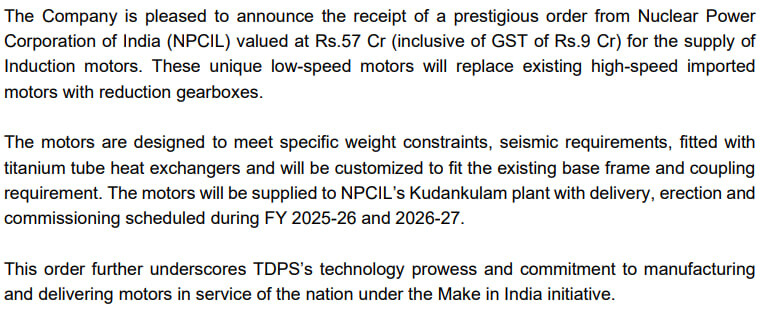

Segment : Nuclear Power (Induction Motors)

Great order win - very prestigious

Some benefits of the replacement being carried out apart from the import substitution angle the guys here were trying to allude to.

Gearboxes introduce energy losses due to friction and heat. By replacing high-speed motors with low-speed motors, energy loss in the gearbox is eliminated, resulting in improved overall efficiency.

Removing the gearbox simplifies the system, leading to lower maintenance requirements and downtime.

President Trump’s elect US Energy Secretary’s fracking company is investor in Fervo [customer of TDPS]. Geothermal produces 99% less carbon vs fossil fuel. Cleaner source of energy which has started to be used by hyper scalers for AI power generation.

Simple thesis: Given renewable energy [solar/wind] can’t reliably meet demand to power data centres, whichever energy source [Gas/Geothermal/Small Modular Reactor] is used, TDPS has a product play there

The only red flag, for now, is the heavy insider selling. Counterintuitive - and in fact, this & the business potential, are on opposite ends of an indefinitely long stick.

Maybe because it is not a major concern for others, is the business longevity and opportunity size a concern? The promoter laid bare the future plans, what if tariff gets applicable, Turkey, 3rd plant getting operational, inventory etc etc.

I wouldn’t have been too concerned about promoter selling if it were just one or two individuals. However, in this case, multiple key leaders, including department heads and even the Managing Director, have been consistently offloading shares. It seems unlikely to be a coincidence that all of them require significant amounts of cash at the same time - especially when the company is at such an interesting juncture with promising future prospects.

Folks rate the promoter selling so highly that they forget the whole thesis

Possibly a weakness with set templates floating around where u become ultra bullish when promoter buys and u become pessimistic when promoter sells some qty.

Saddened to se so many folks contributing to the promoter selling thing with their opinions and no one talking about the guidance upgrade and commentary on the concall.

put a line or two around the quality of earnings and cash they are still holding.

Have not you or your acquaintances sold shares during the market crash in past 2 months to lock in profits ? All the guys listed are employees …senior or otherwise . They get stocks in ESOP etc. and they can sell for just the same reason too .Even promoters can do it …and they did do it a year and half ago when the prospects were equally rosy as they know it in advance … That did not stop the company from posting good results or the stock getting costlier .

Give us a good reason why the selling in 2023 was OK (not a matter of any opinion since we know company did just fine after that ) and this one is not ?

Sometimes insiders have to sell when their ESOPs / RSUs are vested and on exercise, they need to pay taxes (can go up to 39% of the vested value). To cover the taxes upfront, selling is done. Most of time, insiders selling/buying is executed through a trading plan.