Has there been any impact on the company’s Turkey plant due to the unfortunate earthquake ?

I don’t see any press release from the company or public announcement.

Has there been any impact on the company’s Turkey plant due to the unfortunate earthquake ?

I don’t see any press release from the company or public announcement.

Please go through their conf call recording. You will have all your answers.

Regards

Raj

Disc: invested

Thanks, @raj1968

I couldn’t attend the call, and just saw they uploaded con call few minutes back. Will read up!

Interesting development here regarding the recent event of a promoter selling via block deals:

The company filed a disclosure almost immediately claiming no knowledge of any behind the scenes agreement between Mr. Mohib Khericha and Mr. Vijay Kirloskar.

The matter is sub judice at the Karnataka High Court. I hope there is no fraud here, especially after such a stellar turnaround by the company in the last 5 years. Anyone here with some inside knowledge?

The company stated in concall of Q1fy24 :

the high court has passed anorder saying that the shares – the captured shares, which are at 2.5 crores shares arerelated to a single promoter entity – single – which is Sapphire Finman and not related toother promoters. So this is a very welcome development as far as we are concerned. So,we would expect the entire sales team to just one promoter entity and not for the other – does not relate to any other promoter shares. Plus the notifi cation about the website --the High Court website today or tomorrow will be put up on the exchange. And we willkeep all our investors informed about the developments. The next hearing for this case inthe High Court has been scheduled for 28 August and we’ll keep all of you informedabout the progress.

We have been alerted to the fact that you have been putting links to your Twitter/X account in various threads, after putting up some pretty ordinary mundane details.

If this continues, we will have to block your ID.

Kindly take note of above friendly nudge.

This is a forum for learning, not littering posts with Twitter/X links.

Before mentioning the details it would have been great if you could have pointed out the mundane link which i posted.I am not sure if VP member believe in writing long essays to prove a investment thesis , i just feel human mind better works in images and if a business is showing a change in trend then it is better represented in images than write a 2 page note about it.

I had a interaction with another VP Moderator on this and below is the screenshot of the message and if you still feel these messages are mundane or creating nuisance among the community i will happily stop doing so.

P.S:For everyone who is thinking good investing is something to do with high intellect then markets will time and again show you that it is doing the “Mundane” and “boring” stuff right with high Emotional quotient.

We do not encourage external links and encourage boarders to post whatever they post on VP platform itself. What you posted in a series of posts on various topics comes across as an attempt to post a link to Twitter. Hence the above nudge.

If you notice, wherever the external links have not been posted, the posts have not been removed. That should give you a direction of how to go about on VP. rgds.

Promoter decreasing their holdings 58.43% to 34.27%

Its bought by FII and DIIs …

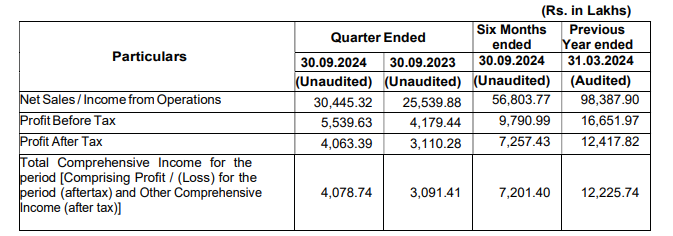

Q2 results came out on 29th. Decent numbers at first glance

Investor presentation

https://www.bseindia.com/xml-data/corpfiling/AttachLive/8b974ee9-a349-4a31-a824-676747e991dd.pdf

Concall held on 30th Oct

Top line guidance for current year 1250 to 1275 cr. With 580 cr done in Q1 and Q2, that leaves a run rate of 335 or 350 cr per Q, in Q3 and Q4…1250 will be a solid growth of 25%. Margin growth will be 2-3% more than the sales growth, as per guidance. With the kind of order book they have and the way, factories are utilized, this looks very much feasible. Risk is of course, a lot of dependence on exports, rather than domestic. That said, TD is in every possible sector feasible in this field and that includes sunrise sector like clean energy.

Disc…invested

TD Power Systems -

Q2 FY 24 results and concall highlights -

Q2 outcomes -

Revenues - 309 vs 273 cr, up 13 pc

Gross Margins @ 36 vs 33 pc

EBITDA - 58 vs 47 cr, up 25 pc ( margins @ 19 vs 17 pc )

PAT - 41 vs 33 cr, up 26 pc

Orders received in Q2 @ 360 vs 256 cr ( up 40 pc YoY )

H1 outcomes -

Revenues - 586 vs 494 cr, up 18 pc

Gross margins @ 36 vs 34.5 pc

EBITDA - 107 vs 86 cr, up 25 pc ( margins @ 18.5 vs 17.5 pc )

PAT - 77 vs 59 cr, up 29 pc

Orders received in H1 @ 657 vs 493 cr ( up 33 pc YoY )

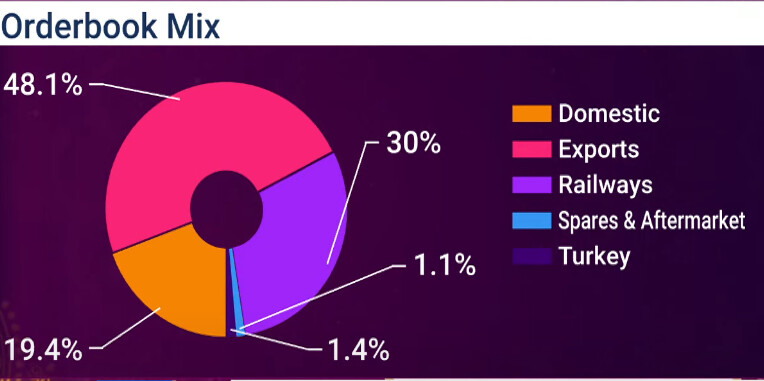

Current status of Orderbook -

Domestic orders - 239 cr

Exports - 594 cr

Railway Orders - 370 cr

Others ( including spares and after market )- 30 cr

Company’s products -

Generators - Over the years, TDPS has established itself as an international market leader in A.C generator manufacturing delivering a wide product spectrum from 1 to 250 MVA. Our machines cater to all prime movers including steam turbines, gas turbines, hydro turbines, wind turbines, gas engines & diesel engines

Motors - Company manufactures synchronous and induction motors designed to suit various industrial & irrigation applications - delivering high performance with greater reliability and efficiency. Their traction motors power complex propulsion systems that drive freight locomotives and passenger transit vehicles

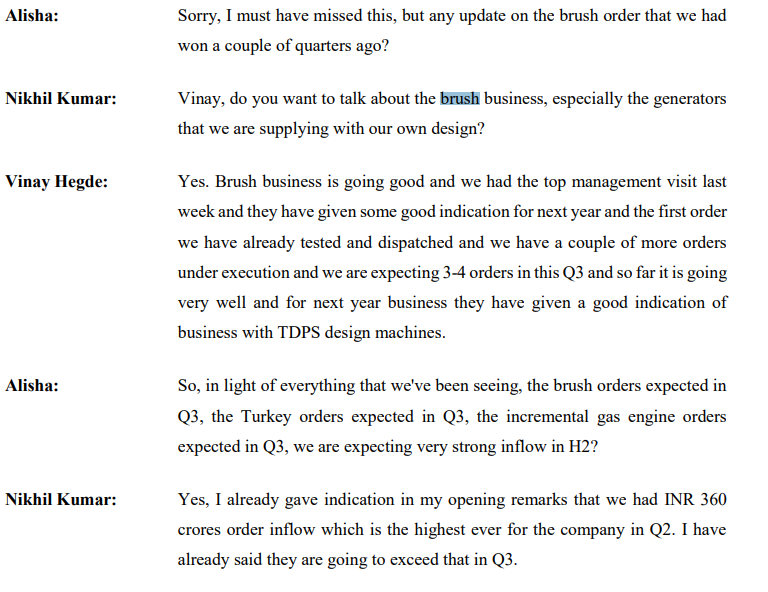

Company expects the order inflow in Q3 to be > Q2 order inflow ( which was @ 360 cr )

Guiding for a topline of 1250 - 1275 cr for FY 25 ( which is a 25-27 pc YoY growth ). Expect EBITDA margins to be around the 19-20 pc mark for full FY 25

Steel and Cement sectors are in the Capex mode and continue to order generators of sizes around 100 MW ( to set up captive power plants ). This is driving the domestic demand. Ethanol, Sugar and Chemical sectors are not showing growth but are maintaining base level demand. Domestic order flow has been flat in H1 vs H1 LY

Expecting 2-3 large orders from railways in coming months. Their execution may happen in FY 27

International markets are showing very strong order book growth for gas turbines, gas engines and motors. Export orders in H1 were @ 478 vs 236 cr YoY which amounts to > 100 pc YoY growth. Exports and Deemed exports orders now constitute 73 pc of company’s total order inflow

Most of the export demand is driven by demand from sectors like - fracking, AI server farms and grid stabilisation ( in case of renewable energy grids )

Company’s capacities are running 3 shifts, 7 days a week. Their customers have asked them to be ready for further growth in next FY

GeoThermal plants are another area of huge growth potential. Company has signed an order for supply of 3 X 43 MW generators for a large geothermal plant in US

Have signed a 5 yr contract with an international major for supply of traction motors. There is another such project in negotiation stages and the company hopes to win the same in Q3/Q4

Orders from Hydro electric power projects continue to be strong. All this demand for Hydro projects is from international mkts

In the motors business, company expects to do 80 cr business this FY and 160 cr in FY 26. Most of the demand for motors is coming from India and ME

Company expects good order flow to resume from the Turkish mkts by next FY ( after a long hiatus )

Company will start hiring people wef Q4 so as to start training them so they are ready by the time company’s new plant is ready in next FY. This new facility is going to be housed in 3 big buildings. They will be commissioned + operationalised one at a time ( as and when they r ready ie in stages )

Capex planned for current FY is @ 80 cr

Company will give out a guidance for FY 26 in the Q3 concall. However, a 17-18 pc topline growth can be assumed to be a conservative tgt for FY 26

Company expects orders for generators to be used in GeoThermal and Hydro power plants from the Turkish mkts. The quantum of orders should be around 25-35 cr for next FY

Company is able to command good Gross and EBITDA margins because of improved product mix hand high capacity utilisations

Company has got a trial order for 17-18 cr from a multinational company operating in the CIS region. If all goes well, company is expected to get business worth 60-70 cr from this company for next 5 yrs. There is another opportunity of similar magnitude in the pipeline with an existing customer. Company intends to obtain the orders before the Christmas holidays or latest by Jan 25

The margins in the GeoThermal generators are > Hydro Electric generators due greater degree of sophistication and complexity involved

The new plant that the company is putting up should cost them around 120 cr and they should be able to do revenues of aprox 400 cr from the same

Turkey is one of the largest GeoThermal mkt in the world as they have multiple sites where these plants can be set up. They have those reservoirs. It’s a gift of nature. Now with stabilisation of their currency and moderation in inflation, Turkish mkt is showing signs of revival

Company has had deep conversations with their clients wrt the sustainability of this strong demand that they r seeing. The feedback that they r getting is that the unmet demand from new Data Centers, Wind and Solar farm stabilisation, GeoThermal energy is likely to be long and strong. Plus the demand from India has been tepid because of the general election. That is also expected to pick up soon as India is expected to double its GDP in not so distant future. Plus there is the Motors division, which has now started to contribute. Basically, it seems that the company is in a really sweet spot

Company believes that their Motors business is going to double in FY 26 ( from 80 cr currently ) and grow very fast in FY 27 as well. They believe, the motors business can eventually be as big as the Generators business !!!

The new capacity’s phase -1,2,3 are expected to come up in June, July and Aug respectively

Once the incremental orders start to pick up for the traction motors, company will also put up a completely new facility for traction motors as well. These r not as bulky as their generators. So - a smaller site, smaller building should suffice. Should come up in 5-6 months

Company is mostly getting its order for Waste 2 Energy generators from Japan and Singapore. The W2E plants are mostly supplying energy to Google’s Data centers in Japan and Singapore

Company has been supplying generators to hydro and gas based power plants for about 20 yrs now. They are also seeing good replacement demand for the equipment installed long back. They are also getting demand for replacement of equipment installed by the competitors

Disc : initiated a tracking position, management commentary and business prospects look rosy, biased, not a buy/sell recommendation, not SEBI registered

Special Opportunity - Small Nuclear Reactors

In the Q2FY25 concall key takeaway -

"They said, they are signing PPA with geothermal. This big geothermal opportunity I talked about. The PPAs are being signed by guys like Google, Microsoft, Meta and so on and so forth. So, they are putting their fingers in geothermal. They are putting their fingers in small nuclear there. But today their requirement is being met by gas. And so they are talking about

changing the mix in the future. But these technologies and scaling up to the

level that they want is going to take some time. They want everything to be

done in the next five years or seven years, right? So, I don’t see things like

small nuclear and everything really affecting the medium-term demand from

our point of view even if it does become a success and I hope it does become

a success, because they are talking about unit sizes of 75 to 80 MW. TDPS can

make these generators. So, if this technology does become widespread, that

small nuclear becomes a commercially viable thing. Then it’s a huge new sector

of demand for TDPS because we are right there in this 80 MW range and we

will deliver those machines then for the next, I don’t know, 20 years."

–

Market Opportunity : The SMR market is emerging, with estimates suggesting a $150 billion market by 2040 .

Holding.

Vishwanath Hangari - The Head of Design and Development

TR Krishna - SBU Unit head

Why are they consistently offloading stock?

Anyone have any insight on this?

Client worth studying are Alstom BRUSH(baker hughes)

Turkey - in the past they did think of exiting the turkey operations to avoid losses. Gov revised incentives for locally made generators and made it attractive. And this revived the whole sector benefiting TD power which is a power shortage country

Captive demand for power will remain high in countries for sure. Domestically this is also picking up.

Railways - supplying electrical motors and this is also a big segment for them

What are drawbacks you see here. Either in execution or in demand. Any chance of US demand going down with new administration,

Disclosure: Recently Invested.

Don’t Hope so looking to the capex in renewable energy

Order book

Growth Opportunities:

In a global setup, u need leaders like Trump who tend to focus on resolving/ending geopolitical tensions atleast which disrupt USA. So TD power can do well in this term.

BRUSH orders for TDPS : BRUSH Power Generation | Baker Hughes

Ques in Q2 concall from Envision capital

Our factory is running seven days a week, three full shifts and we are

completely full and customers have asked us to be ready for further growth

next year and we have had detailed discussions with them on allocation of

capacity and load plans. FROM CONCALL ![]()