This is interesting and I was not aware that ecommerce delivery is not profitable anywhere in world. Any insights why is it so? Is it still in investment stage even in US/Europe/China etc or in race to gain market share as is ecommerce websites in India?

E-commerce specialized logistics players e.g. Delhivery, Xpressbees typically offer aggressive prices to e-commerce companies with the objective of eventually gaining scale to an extent where the per delivery cost becomes very low. Eventually, the tradional players who focus on a per shipment profitability loose out in pricing.

Secondly, to serve e-commerce companies, which are increasingly focussing on Tier-2 cities, logistics players need to invest in infra (dispatch centers, return processing centers etc.) to reach these pin-codes. Many of these routes might not be profitable for the logistics companies hence ROI takes time.

Also, the low share might also be a factor of inability of the company to deliver on the service parameters of e-commerce giants - on-time delivery (2-5 days), end-to-end trackability of shipments - which would be much better in e-commerce logistics specialists.

2 Likes

One of the reason E commerce is not profitable is - Bulk buyer with huge volume (i.e. E commerce companies) who also have their own delivery arms, giving them better bargaining power with transporters.

Also, reason for TCI gaining marketshare even during slowdown is - their major competitor Gati is going through financial and operational troubles and losing market share ( As evident from their results)

3 Likes

The article looks very tricky and doesn’t seem to conclude in any one direction.

Well, in terms of business model, I think they are doing all the right things as of now. This is quite evident in the robust results in terms of revenue growth, margin expansion and cash flow generation where almost all other industry players are bleeding.

Gati is almost at the verge of collapse, even strong player like Blue Dart is struggling to keep market share and profitability intact.

Now, directionally incremental capex is also smart thing to do - where they are focussed on increasing sorting centres, branch expansion and strong IT + grievance redressal mechanism. Essentially all the right things that asset light player should do (see what UBER and OLA does in similar way for personal transport). Infact, the branch network will cross that of Blue Dart if I remember the figures correctly.

However, concerning area is that PE money has also understood the opportunity size and scope of this space in huge country like ours (where 90% market is still unorganized) and they have started aggressively funding startups like Rivigo (who have similar revenue but huge losses, thanks to their aggressive pricing to capture market share).

We saw similar trend in diagnostic space where huge PE money stalled the growth for existing organized players since they funded regional players to gain volume and market share.

This space will be interesting to see how competitive intensity pans out in short to medium term but surely there will be consolidation and displacement of unorganized share it looks like.

Disclosure: Tracking position

6 Likes

I have created a semi-automated peer comparison sheet for most of the companies in the industry.

Logistics Industry Data.xlsx (724.1 KB)

You can find comparisons of more industries here:

1 Like

Q3 results

My thoughts on current situation with respect to industry in general and TCI Express in particular.

I think logistics industry will take some time to pick-up. In general I would categorize this in medium impact zone. Though, any economic activity to pick-up (for that matter even transporting FMCG or Medicines), we can’t live without logistics.

Migration of labour can be another layer of problem, where there will be limited trucks running and industry might need to pay premiums to drivers to carry-on the activity. On the other hand, they might be also able to pass-on this extra amount to customers.

If we think about this sector, it’s mainly proxy of GDP (with some factor of 1.xx) and probably we are going to hit bottom of GDP cycle due to lockdown situation. So, it’s fair to assume that we are at the bottom of the whole cycle. Any increase in GDP can lead to incremental growth for the sector.

Now, specific to business model of TCI Express - thanks to asset light business model, it has following advantages:

- They might not incur much of salary cost except backend support staff as they don’t own trucks

- They will not face any interest cost like other logistic players who have taken loans for vehicles

- Cost is more variable so they have greater capacity to suffer if things don’t work well

It’s kind of anti-fragile business model, where competition is more likely to bleed and TCI Express can come out much stronger relatively. Unorganized to organized shift in the sector will also further accelerate. TCI Express has almost zero debt so that adds a layer to capacity to suffer and survival in near term.

Key monitor-able would be to watch demand of underlying sectors which it caters to and how fast the lockdown measures are lifted for these industries.

16 Likes

Though this is behind paywall.

3 Likes

Hi,

Since fuel prices and jet fuel prices have both gone down this should help with margins of TCI exp, but what sectors which they cater to do you see recovering quickly post lockdown?

Ecommerce is hardly 5% of their revenue and will take time to grow. TCI investor ppts say that 50% of their business comes from SMEs. Do you have any idea on the breakup of the same?

Change in fuel prices does not affects TCI express. They work on a vendor system wherein the contracts are fixed at the start of the year for next 12 months on per kilometer basis.

Also management had once mentioned that in case of very large movements in fuel prices they do allow change in contractual prices which is a pass through to its customers.

Either way, retail fuel prices has not changed materially in India as the government filled the vaccum of low oil prices with additional taxes.

9 Likes

Here is a list of parameters against which “logistics”; especially “Express Cargo” services are evaluated

Another big one is last mile delivery and TCI says -

Efficient Last Mile Deliveries:

With the continuous increase in the number of e-commerce companies, the provision of efficient last mile deliveries is experiencing a major upswing creating differentiated services amongst competitors. As a result, logistics companies are making significant efforts to offer efficient last

mile deliveries, thereby boosting the growth of the sector.

2 cents on last mile deliveries - Last mile contributes a massive 41% of the overall logistics cost . Its contribution increases to 53% when it comes to the overall shipping cost .

source- 6 most effective ways to reduce last mile delivery costs in your business

Once we have gauged where TCI and its competitors/other players stand (1) w.r.t the parameters and (2) the prices at which they are selling (lower is better), we would have gathered a good amount of knowledge & information so that we can go forward and try to establish whether TCI has got competitive advantages(entry barriers) when compared to others. If there is, what is it and how strong it is!

2 Likes

And this is what TCI mentions in its annual report

What technological advancements ? We need the details

1 Like

Short Notes

1.TCI Express started in 1996 as a division of Transport Corporation of India Limited (TCIL), catering to Express delivery. On 1 st April 2016, this department split from TCI as a new company TCI Express in the share market (Demerger).

2.TCI Express has adopted Uber / Ola’s Asset Light Business Model. It does not own trucks, but mostly enters into long term rental agreement with the Truck owners. This results in a high ROCE Business(35%-45%) in a brutal sector. The company is reducing its debt through its high earnings.

3.It has plans to invest Rs.400 Crores(mostly through its own earnings), over 5 years, primarily into establishing and automating its sorting centers, which would definitely strengthen the network of the company in future. As a matter of strategy, the company wants to own its sorting centers (at least in future). Currently 8 of its 28 are owned, rest leased.

4.TCI Express is a family owned company.

Mr. Chander Agarwal is the Managing Director of TCI Express Company. He is the younger son of D P Agarwal, who is the Chairman & Managing Director of Transport Corporation of India Ltd.

5. Among the various interests of Mr. Chander Agarwal, one includes printing his own interviews(in third person) from his profile in Social Media.

He once had a habit to remind himself after a few months that he is the precious gem behind TCI Express’s success. Eagerly waiting for his 2020 article.

https://medium.com/@chanderagarwal

6. In one of his exclusive interviews to himself, he has told

“Talking about his personal life, he is one of those persons who even after touching newer heights in his career with each passing day, is one of the most down to earth person. His down to earth nature is the reason for his success, all his decisions are made keeping in mind his nation, customers, employees, family and the community he is living in.”

7. It thus comes as no surprise when the remuneration of this down-to-earth person’s crosses regulatory limit of 5% of Net profit of the company. His remuneration includes 4% of Net Pofits of the company, in addition to a pocket money of around Rs. 15-25Lakhs per month.

To be fair to him however, he has decided to give up his 3 months salary due to Coronavirus, while ensuring rest of the company get their normal salary.

A small video made by me on the company. Hope it does not break Valuepikr rules.

https://youtu.be/etswGRxmU5E

4 Likes

Article on Transport sector post Covid by MD of TCI : https://www.linkedin.com/pulse/supply-chains-india-post-covid-world-vineet-agarwal?articleId=6667407481595138048#comments-6667407481595138048&trk=public_profile_article_view

1 Like

1 Like

I am trying to get a list - as “COMPLETE” as possible…

anyone willing to help me ?

Please kep in mind :

1. The logistics industry has further subdivisions. One may take a look at the following link to learn about the various sub sectors Logistics Sector Skill Council

2. TCI belongs to “Transportation” sub category

It will be best to compare TCI with other “Transportation” logistics companies than just any other logistics company - imho

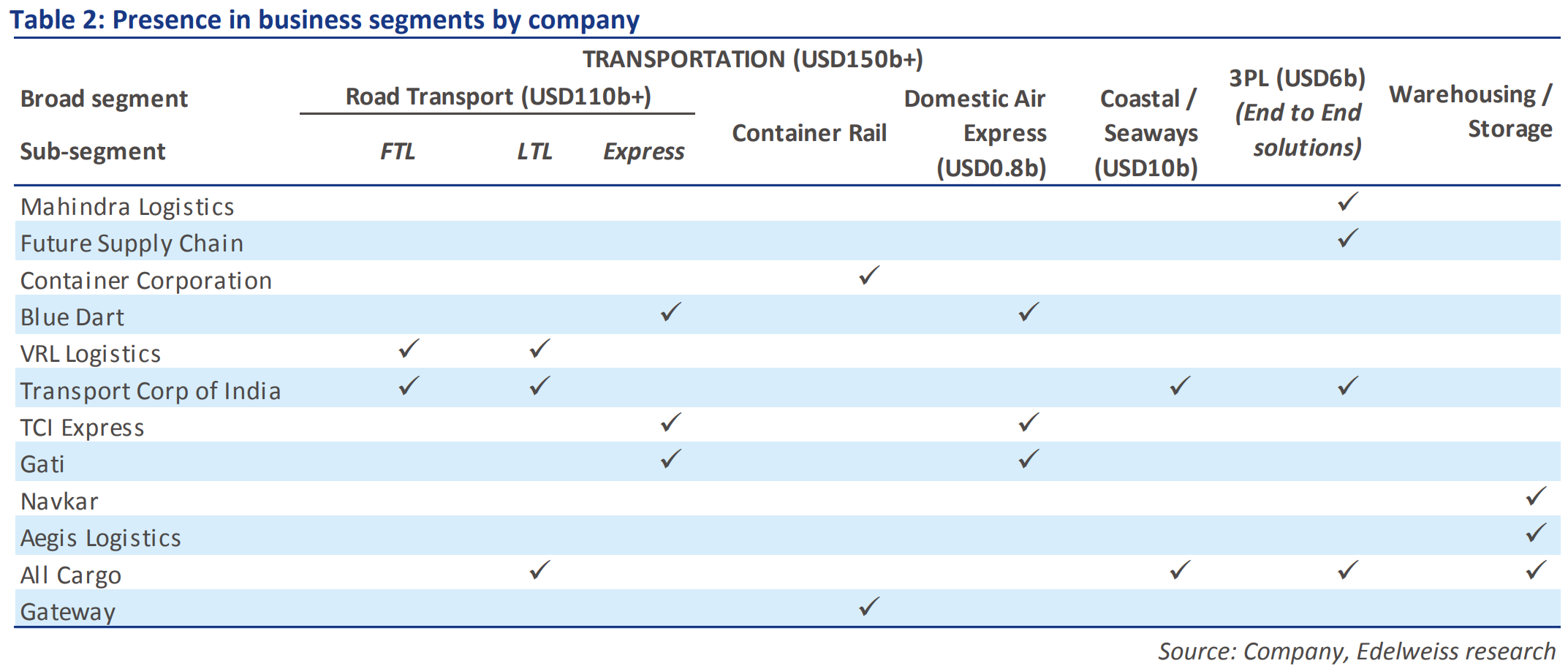

The Edelweiss report on India Logistics has a nice list.

4 Likes

Bluedart and Gati have faced plenty of challenges and werent able to do well due to absence of moat. What makes TCI Express better positioned? They have plenty of competition from unorganized and unlisted players.

The parent, TCI Ltd is has moat in 3PL. Businesses who require regular transportation of goods cannot (well, mostly) do it in-house. They have to rely on a transport service.

Auto sector is a huge component of TCIs revenues, around 56%, and as the sector picks up so will the business of TCI… but for TCI express there is no such clarity. The state of Bluedart and Gati is less encouraging.

As per my understanding,

-

Gati & Bluedart suffered the most due to their strong focus on eCommerce. Most of the PE funded logistics players are eCommerce focussed due to strong volume visibility.

-

Bluedart suffered due to its focus on Air Express which is less profitable compared to Road Express for obvious reasons.

TCI Express did the following:

-

Focussed on B2B mostly. Branding in logistics works best in B2B.

-

Focussed on Road express which was benefited the most from GST implementation.

A joint survey in 2011-12 by the Transport Corporation of India and IIM Calcutta revealed an annual loss of about Rs 27,000 crore to the economy owing to detention to road vehicles at checkposts and en route for documentation, physical checks of vehicles, drivers and cargo by RTO/police, and payment of highway toll and taxes, as well as harassment and corruption. The on-road stoppage expenses including illicit payments amounted, on average, to 15% of total trip expenses. Additional fuel consumption due to delays and slow speed of vehicles led to annual costs of Rs 60,000 crore.

They may have done many things better but the above seems to me the main differentiators.

7 Likes