This seems to be old article dated May 28, 2010

1 Like

Poor set of results for tatva chintan.

Y on Y sales down from 123 cr to 90 cr. Op profit down from 35 cr to 11 cr . And net profit down from 32 cr to 7 cr.

Consistent q on q decline in net profits since Sep 21 quarter.

Stock price still holding firm inspite of many poor quarters.

One of the reasons could be low retail holding at 6% with promoters holding 79% stake and rest held by DII/FIIs. In fact DIIs have consistently raised their stakes in past few quarters.

I remember similar excitement post listing in advanced enzymes, where market participants were excited a lot and results did not come through. Stock price corrected and has not rewarded shareholders till now. Here too FIIs stake has gone up from 11% in Dec 2019 to nearly 22 % as on Sep 22. And the big fund raising stake is Nalanda India fund. Nalanda stake was 4.74 % from Sep 2020 to Dec 21 post which they kept increasing stake each quarter and now it stands at 8.91%. Stock price consolidating above 61.8% retracement level (at 252) to the previous rally from low of 98 in March 2020 to a high of 503 in May 2021.

28 Likes

Tatva chintan Q4 & FY 2023 concall highlights:

Results:

Q Sales of 124 cr. Rise of 22% yoy, yearly sales of 423 cr, a degrowth of 2%.EBITDA margins at 13% vs 22% in q422.

My take: poor show continues despite management’s earlier forecast of good growth from q423. Reason being stockpile of high cost inventory and low demand for SDA which was further aggreviated by drop in RM cost leading to drop in realisation.

Product wise performance & forecast:

SDA:

Contributed 30% to revenue, a decline of 43 % yoy.

Entire old inventory will be consumed by may end(this made me believe that Q1 should also be lackluster). SDA demand to improve from H2fy24. Submitted commercial trial order to large customer for 4 different applications. Expect full scale commercialisation from jan 2024.

PTC:

Grew 46% yoy( as sda demand was almost zero in q2, q3, they sold more ptc).

Electrolyte salt:

Now contributes 4% to revenue compared to 1% during ipo. This year many customers will go for trial order and full scale commercialization from fy 25.expect revenue to double by fy25.

PASC:

In q424, all three products using continuous flow chemistry (1.product for metal extraction. 2.dehydrated monoglyme for battery. 3.agchem intermediate which is key RM for many advanced agchem intermediate) to go into full scale production so expect exponential growth from q4.

BFR:

got commercial approval from 2 large customers. More approvals are in progress. But due to sudden drop in bromine proces and low demand, customer uptake is verylow. Initially we will go for low margin base products and then move to more advanced, higher margin FR.

Projections:

Will grow 20% in value terms fy24 with 18-20%

(Their ideal margins are 22-26 % but as current FR are low margins, they will consume some gain and secondly new capex is adding to cost as currently plant is running at very low levels. It will run at optimum levels only from q3/q4)

margins. Actually in volume terms, growth will be much higher but recently, realisations have dropped by 18-20% due to fall in key RM prices. So taking this drop in realisation into count, we will grow 20%.drop in revenue will not have any impact on ebitda margins.

Expect to grow by 75-80% in fy 25 from current levels.

Segment wise fy 24 growth forecast:

SDA: In value terms, it will be flat due to low realizations. Might be some volume growth. Euro 7 norms will increase demand for SDA.

PTC:likely to be flat.Have submitted for new applications. If that materializes, might see some growth.

Electrolyte salt:will see growth close to 100%.

PASC:management did not mention but my take is it will show good growth as this is rhe only segment that has shown consistent performance.

BFR: Sales can be near 50cr.By fy25, expect sales of about 200cr.

My take:current poor performance is not likely to last long . It appears to be a case of good company in bad times which is what i look for. But valuations are stretched. At cmp there is no margin of safety even if company beats management forecast for fy24. So for me its wait and watch.

Disclaimer: I do not have any holding in company as of now.

9 Likes

Tatva Chintan reported sales growth in June quarter and marginal improvement in operating margins. But its below the line items like depreciation ( related to higher capex) which are acting as a dampener on the results at net profit levels.

This company is a classic example of a hot stock in a hot sector. When chemical sector was the rage, this company was touted as a company with competitive edge, and entry barriers etc. These terms are very important to understand and apply. By themselves they are not a license to pay crazy valuations. And Tatva Chintan began its listing journey enjoying crazy valuations. When its valuations were at peak,

I guess peak market cap was around 6500 crores plus. And sales were a mere 400 crores. A lot of extrapolation was done about capex coming on stream by X number of years and sales figure being double that of the sales at that time. And then margins were also extrapolated based on management guidance. And based on that, a lot of experts predicted that at ABC valuations, it would be justified to buy this company.

As of now valuations have nearly halved ( still not there, but just about there. ) And still no clear light at the end of the tunnel. While it may be one of the better chemical companies with some kind of moat, or competitive advantage, the key take home learning for us is that it was a " Hot stock in a hot sector" … A classical example of what Lynch preaches in his book.

Maximum money is made when a company is bought at cheap (read commodity type company valuations) valuations, and it reports growth and profits that are expected from a speciality or niche company. Majority of the money is made from re rating, and the other big chunk from actual growth.

Now apply exactly reverse logic to above paragraph. Imagine a company bought at 100 PE (according to screener this used to quote actually at 100 PE or close to it), delivering negligible growth, and swift contraction in valuations to sub 40 ( as seen during April 2023) . The key thing to note here is that even if the company starts delivering growth at a reasonable clip, one cannot expect valuations to reach levels of 100 PE…

The other tell tale sign was an extremely appealing IPO happening during sectoral fancy. One needs to beware of these kind of IPOs. We have seen this kind of history being repeated off and on … In 2006-2008 era it was infra and real estate companies. In the run up to 2015 pharma peak it was pharma companies. Nowadays its railways, defence, power etc. And these things will keep on repeating with old wine in new bottles.

So starting valuations matter a lot while evaluating a company. For a time being they do not matter in a hot sector and a hotter stock. But after market wearies of lacklustre results, prices tend to correct or go sidways. Either case the capital invested does not produce any return.

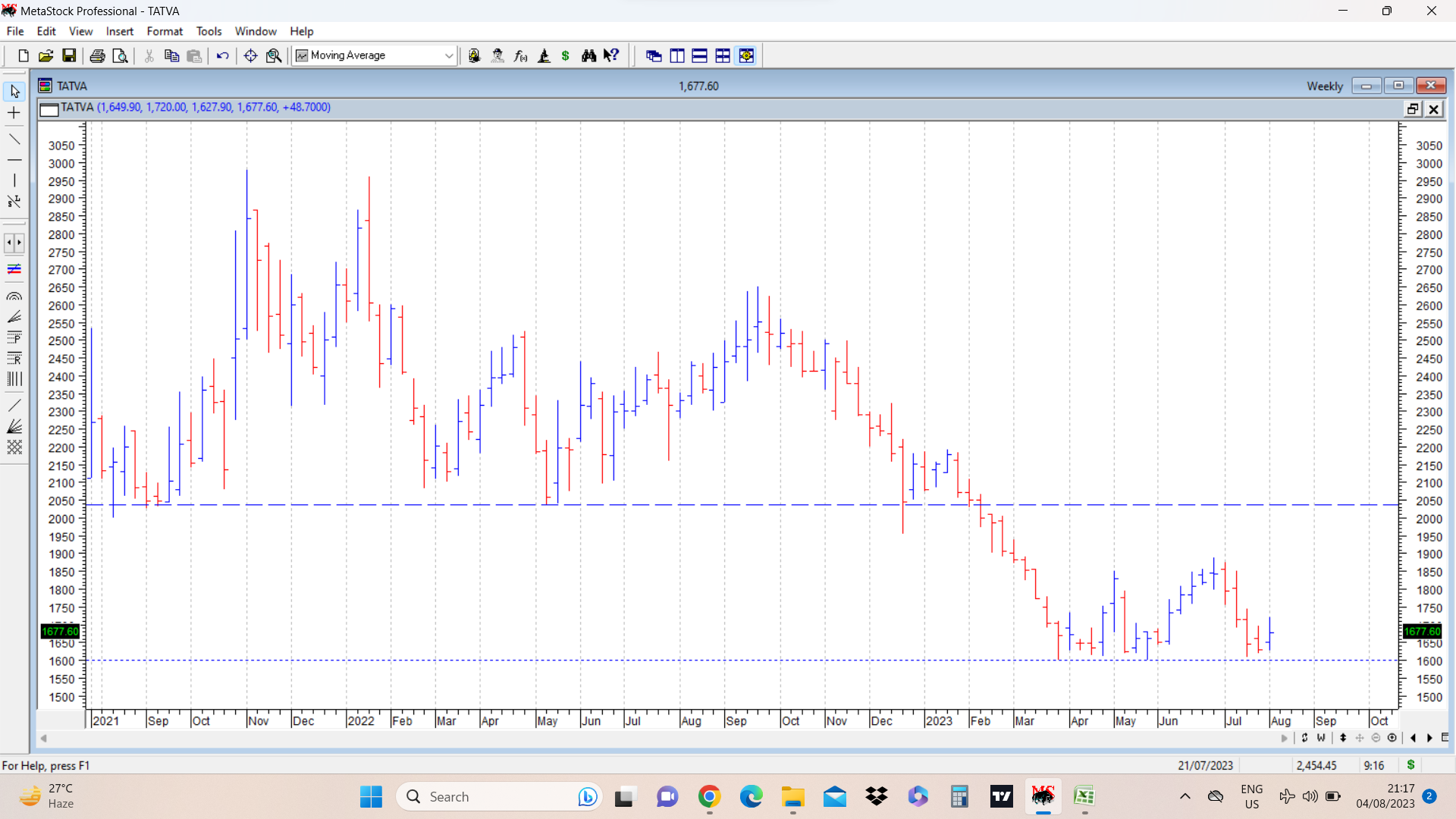

Attaching a simple chart where breach of post IPO lows was an indication to exit. That level was around 2000. After that stock price has not gone close to those breakdown levels. New next level to watch is level of 1600 or thereabouts. Just for record, stock listed on bourses in July 2021 and its more than 2 years since then. Folks who bought post IPO and listing, considering this as a company with moat etc are still sitting in losses and their capital has not produced anything for more than 2 years, and while a lot of other stocks have doubled or tripled or more.

22 Likes

@hitesh2710 may I know view on this technically, please? Seems to be forming a bottom at around 1620?

Disc: taken positions at 1620-1650 levels.

As of now there is no evidence of change in trend, (stock is in downtrend.) Need to see if recent bottom holds and any rally materialises. I think level of 1600 remains crucial . One also needs to review fundamental prospects of the company.

5 Likes

Can’t agree more with @hitesh2710 sir on valuations. No doubt tatva has differentiated products that are not easy to manufacture.I have liked the company because of its technical expertise, technocrat promoters and expanding product portfolio but did not enter due to crazy valuations. Margin erosion led to decline. Main reason for erosion is low demand for SDA’s.Although now demand has stabilised to an extent, but their current SDA’s find use mainly in auto emission control. Auto being highly cyclical, i think such margin erosion can repeat. They are trying to add non auto application but it will have limited scope.

On positive side, if management guidance of 100% revenue growth from next year onwards with stable margin holds true, i feel company should rerate.

Disclaimer: Have a tracking position at 1486.

3 Likes

hi folks! haven’t seen you all discussing the stock quite much in recent times.

I came across this stock when it IPOed but I didn’t invest although liked its characteristics.

I recently bought the stock at around 990rs.

Why now? Let me introduce you’all to my thought process

I have an experience of around 3 years in the markets, and when I started in the markets at that time the hot stocks were pharma and chemicals, so invested a lot of money there and on net levels didn’t make any return.

Things I learnt from my first sectoral cycle :

1.Valutions matter

2.Brokerage reports are sales reports

3.Never invest at peak margins, peak earnings, peak valuations (even if its a structural business, look for temporary headwinds to invest so that you can get a good valuation multiple)

“Its the earnings that break or make the narrative. I like to be placed in a stage where the earnings start the narrative. and its the narative that gives you speculative returns alongside earnings growth” ~ me ![]()

Lets apply my learnings to Tatva Chintan while looking at some ratios:

- The business is trading at 3.25x Price to Book , Average ~ 7x

- RoCE less than 10% for 2 years now.

- OPM (17%) lower than average ~ (20%)

Now it clearly shows that the stock is going through an earnings downcycle and the stock is falling continuously but I believe enough pessimism has been built enough around it. I have made a tracking position.

How I think differently from the market at this point is:

- I think the revenue has bottomed out in FY24 (0.9x asset turns, 2.6x asset turns bull times on a much smaller asset base)

- I could be completely wrong with the first point so let’s check survivability - the business has no debt (due its recent equity dilution xD) and lil cash too so I think it can survive in one year of downturn.

Now lets look at optionalities :

- A large part of revenue can come from the other part of business (PASC - molecules commercializing) in next 1 year (biggest and only optionality for me) (management has guided for next 6 months but I have also taken a cushion of another 6 months in my assumption), one must note that in the previous bull run of the stock it was the SDAs (major part of business) which gave a splendid performance. it would be a blue-sky situation if both PASC and SDAs do well from here.

- Euro 7 norms to tentatively start from next 1.5 years.(good for SDA business division)

- China’s GDP showing signs of lil recovery. (GDP growth and Commercial Vehicle sales are correlated) (good for SDA business division)

Risks:

- The working capital cycle is very baddddddd. (which makes me not be a permanent owner of the business) (I just want to play out the cycle in this business)

- Change in end use of the application (I am unaware on this, neither the management has told me anything about it. sus)(still let’s hope for the positive)

- PASC molecules do not commercial (I will sell immediately)

I have used simple principles of a cyclical investing approach for this business because I know my circle of competence. I cannot understand the chemical business because of their complexity.

fingers crossed, I am optimistic about the stock performance ![]()

11 Likes