Thanks for sharing the snippets, it clarifies the point i am making  and why i am linking inventory to forecast system. The primary aim of a good forecast system is to avoid both out of stock situation and inventory write-off while having optimum inventory since inventory is essentially cash which cannot be put to use.

and why i am linking inventory to forecast system. The primary aim of a good forecast system is to avoid both out of stock situation and inventory write-off while having optimum inventory since inventory is essentially cash which cannot be put to use.

If you read through first reply they are mentioning that most of the business is done on basis of forecast system and not contract but if you look at the forecast horizon they are talking about current year and next year, it is more like an estimate at very high level, i would not call that forecast. And Dhruv makes exactly the same point which Mr. Shah has explained that they keep high inventory because they are not sure which supplier will get the order, understand there can be deviation from forecast but not sure whether one gets an order or not, i would not call that as forecast based replenishment. It is more like made to stock in supply chain parlance. Dont wish to split hairs but it seemed dichotomy to me Nonetheless the business seems to be in quite good shape, valuation is for each one to make their own assessment. Thank you.

I see, you have some apprehension about the inventory days. But is it way out of line from industry standard ? I looked at some of the top of mind recall specialty chem companies and this is what I get. Doesn’t tatva inventory nos. seem more or less within industry norms ?

Company name: FY21 Inventory days : Exports Contribution

Aarti Industries : 190 : 44% (Spec chem is 83% of revenue )

Clean Science : 156 : ~75% (With ~30% of it to China)

Tatva Chintan : 174 : 70.58 %

PIIND : 149 : 72%

Did you get your hands on what’s the %age of export to China ? I might have missed it. I know it’s very high for Clean Science at close to ~35%. Not sure about Tatva.

Yes it is inline with industry, my comment was with reference to forecast system only. As per RHP China sales is around 17-20%.

TATVA CHINTAN Q2 : Cons. Net Profit Up 826 % (YOY), Up 41 % (QOQ)

Revenue Up 106 % at Rs 123 cr (YOY), Up 16 % (QOQ)

EBITDA up 477 % at Rs 35.8 cr (YOY), Up 39 % (QOQ)

Margins At 28 % V 10 % (YOY), 24 % (QOQ)

Invested

Devil in detail, good margin is because of inventory gains, QOQ revenue is up 16% but COGS is up 30%, seems RM pricing pressure, otherwise stupendous result, will provide some relief to valuation unless it goes through the roof on Monday

A very good and detailed report by JM Financial (available in public domain )

I have the following questions, if someone can please answer them:

- How much % of TCPCL’s PTC production is in captive use for SDA manufacturing?

- What can be the potential % contribution to sales of electrolyte salts in next 3-4 years?

- What are some of the key raw materials and whether RM prices are generally very volatile in nature?

Thank you.

Disc- no holdings but researching and tracking closely

Dont have idea on 1st and 3rd question but Management has guided that as new applications emerge then Electrolytes can be a significant contributor

Q2FY22 Conference Call

https://www.tatvachintan.com/pdf/Financial%20Results%20Q3FY22.pdf

Q3 results - YOY has increased by 30 % 104 Cr ,but compared to last quarter its down by 15% .

Earnings Call is sechduled for 18th Jan at 4PM

https://services.choruscall.in/DiamondPassRegistration/register?confirmationNumber=4410450&linkSecurityString=11b6fff9b6

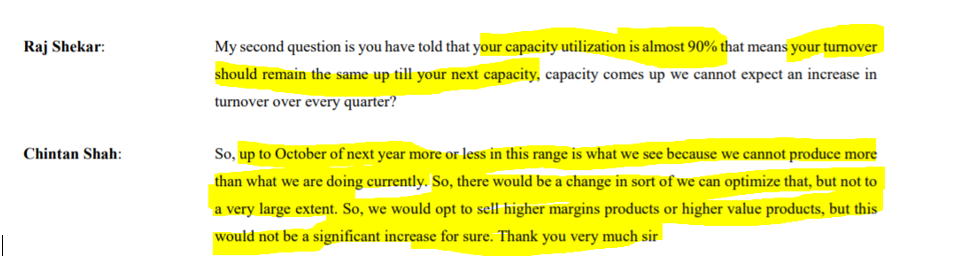

I like the company but is trading at a nose bleed valuation. Here is an excerpt from Q2FY22 concall.

So capacity utilization is at 90% which realistically leaves very little scope for topline expansion. In order for them to increase the bottom line quarter on quarter from here on they will need to increase the share of high margin SDA even further. Last quarter the revenue share was SDA at 62% already. The additional 200KL capacity will come online by Jan 2023. Given these constraints I am not sure how much more the stock can fly, but given the markets are forward looking one never knows. Maybe the next couple of quarters might provide a better entry point.

Disc:- Bought a couple of shares for tracking purposes.

agreed, part in Q3 concall management mentioned that they cant accelerate further until the new venture is established and it is insisted that the SDA utilization demand is low due to semi conductor issue and this will take a while to ramp up. additionally the split between SDA utilization with respective to auto & non-auto is 80:20, with this ratio observed that demand for SDA is capable to meet combining both factory utilizations. and it is expected that we could see the similar result in Q4 as following to Q3. I believe the growth will stable for few next quarters, the only trigger point would be announcement for new client win, as the discussion in progress, we may hear the deal win in near future and that claims 7 out of 7 top OEM companies into TATVA client list.

Initiating coverage by Nirmal Bang

A detailed report by ICICI Securities - An insightful read!

20220421_TATVA_ICICI Securities.pdf (440.8 KB)

Tatva Chintan came out with results. Below is the investor presentation.

Q4 has been bad to say the least. YoY decline in revenue, margins! Attributed to increase in freight and fuel cost. The new plant to commence in Dec’22.

Quite a few product launches planned over next 22 months!

Disc-invested

And a good one

Concall: Tatva Chintan Pharma Chem Earnings Call for Q1FY23 - YouTube

Investor PPT: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5605c8a3-6517-4977-b734-c11ac57ad8bd.pdf

My notes on Q1 FY23 concall:

SDA

- Elephant in the room - Drop in SDA demand for Q1 (52% in FY22 vs 7% in Q1FY23) and Q2 was advised in Q4 concall.

- This is a temporary demand problem mainly due to semiconductor shortage and geo-political issues, further increased due to COVID lockdowns in China.

- Despite SDA tanking, achieved 83% of YoY numbers meaning other segments are quite strong. PTC + Salts + PASC showed 60% YoY growth, expect better through to Q4 due to 1 new product in PASC gone into commercial sales now.

- SDA is high margin segment so lower EBITDA margin in Q1 is due to loss of revenues from SDA segment

Guidance for FY23

- Renewed demand seen. Q2 to be marginally better than Q1 with Q3 onwards full scale demand expected.

- Carrying higher inventory now mainly due to expected demand uptick from Q3 onwards.

- So, realistically expect to achieve 90% of FY22 numbers. Mainly due to delay in order for 1 large customer in China which should come in by Dec '22.

- SDA based zeolite catalyst in waste recycling already developed and ready for commercial sales.

PTC

- PTC showed historically highest quarterly revenue of 40Cr, growth of 79% YoY. TCPCL continues to be leader in PTC segment and has increased market share in Q1 (by how much?)

Guidance for FY23

- More PTC can be sold due to lower captive consumption by SDA segment in Q1. Additional capacity of PTC should be online by Q3FY23 so now full potential of PTC can be realised without hampering SDA pipeline when SDA demand returns.

- PTC demand in Q1 higher due to 1 Europe customer whose 80% demand was serviced by TCPCL due to better logistics than other supplier.

Electrolyte Salts

- Showed historically highest quarterly revenue of 6.9Cr, entire FY22 was 5.7Cr.

- Formal approval from new customer on energy storage device application is in and commercial sales have begun. 2 more customers in pipeline for approvals.

Guidance for FY23

- Robust future for this segment in coming years. Previous guidance is 4x-5x over FY22.|

PASC

- PASC 34.5Cr, strong growth of 28% YoY. 1 new product has begun full commercial sales.

- Monoglyme - Pilot stage equipment will be in place in Q2. For another product (Which one??), equipment is in place and trials underway with commercial sales Q2-Q3FY24 onwards.

- New product in metal extraction is approved and commercial sales to begin in Q4FY23 (1 of the 4 ones in R&D in Q4). At full scale, 30-40Cr revenue potential.

Guidance for FY23

- No major callout for PASC. Previous guidance of strong growth of 40-50% expected over FY22.

Flame Retardants

- Pilot trials completed, Full scale plant trial to start now. Current plant of 5000 MT vs global market size of 160,000 MT. No competitor in India, only 3 known MNCs.

Guidance for FY23

- No major callout, revenue potential towards Q4FY23.

General

- Capex for Dahej as per schedule and should be ready by Q3FY23 (Nov '22) despite 3 weeks of construction strike. Increase reactor capacity from 200KL to 400KL with potential to double revenues in coming years.

- Minor capex of 3Cr towards special tanks for storing flame retardants done in Q1FY23.

- Until FY22, 100% tax exemption for Dahej plant. Next 5 years, 50% tax would be applicable. Overall tax rate should be 18-20%.

Guidance for FY23

- No major capex after Dahej expansion until EC clearance for acquired land comes in.

- Sustainable margins - 23-27% EBITDA margins

Estimates for FY23 based on above commentary turn out to be not too bad actually. With non-SDA segments, growing 60%, if they manage to get ~200Cr from SDA (10% degrowth), you are looking at ~20% topline growth and ~30% bottomline since SDA is high margin. Now that Dahej tax holiday has ended, bottomline will come down a bit and needs higher SDA share to alleviate that. With Q2 to be marginally better for SDA, overall numbers might look subdued until Q3 when additional capacity, renewed demand and new product revenues kick in. I see this as temporary pain for 2 quarters which will hopefully bring TCPCL down from stratospheric into reasonable valuation range.

Disc: Not invested. In my watchlist to invest when valuations are reasonable.

I am trying to search the applications of Structure Directing Agents. As per company they are saying it is mainly used in vehicles and as Euro5/6 norms are effective and emissions need to be controlled.

a. Will this be used as a quoting material in Engine- If this is the case then it will be required in each and every vehicle which will have Euro5/6/7

b. Will this be used as agent in gasoline- If this is the case then it will need to be mixed in gasoline and will be in continuous demand

Can anybody throw some light on the applications?

In Automobiles SDA usage is in Catalytic Converters .

SDAs are the key building blocks for manufacturing high-precision zeolite which is used in automotive emission control, petrochemicals, continuous flow chemistry,

Dont think its used in gasoline .

**Q1FY23 - Commentary **

-

anticipating a drop in demand of SDAs for Q1 and Q2 FY2023. Due to semiconductor chip shortage coupled with geopolitical issues, which again was further enhanced by COVID lockdowns in China.

-

The other three product categories PTC, Electrolyte Salts and PASC together contributed a revenue of ₹ 818 million in these three categories showing an overall growth of nearly 60%.

-

On the full year basis FY2022 the total revenue was ₹ 4,336 million out of which only the SDAs contribute ₹ 2,248 million. an average the quarterly sales of these three categories together was at ₹ 515 million against this during Q1 FY2023 achieved a revenue of ₹ 818 million.

-

During Q1 FY2023, export stood at ₹ 564 million, contributing around 64% of the total revenue. Export declined during the quarter mainly due to drop in the sale of SDA which is our major export contributor.

-

The ongoing capacity expansion of setting up additional facilities at our existing Dahej SEZ is as per schedule and we target to commission the facility by end of Q3 FY2023.

in overall the revenues for Q2 expected to in a similar to Q1FY23 or slightly better, as the SDA revenues are continuous to be in downtrend it is likely that revenues are stable in Q2. And SDA revenues are expected to grow starting from Q3 and brought back to normal run rate from Q4. Expecting the major trigger kicks in with the new capacity launch in Q3 and the SDA normal run rate, currently in a tracking position and add subsequently post Q2 results or in a down trajectory.

- TATVA Chems are largest producer of Glymes in the world, and third largest in India. Glymes (called “glycol ethers” )-The U.S. Environmental Protection Agency announced in July that it plans to clamp down on these little known ingredients used by a broad array of industries. More on (https://www.scientificamerican.com/article.cfm?id=green-chemistry-benign-by-design) typically used as solvents in manufacturing.

- Though speciality chems contribute 25% revenue there is very little disclosure from mgmt which is not encouraging?

- Though SDA are used currently in automobiles, with transition to EV, unless ES business catches up, SDA will go down.