The Domestic Steel Price Plunge

In the surprising turn of events for the past 3-4 years, domestic steel prices in India have fallen to a 45-month low , despite a strong underlying demand. For a nation like India which has a goal to achieve 300 million tonne per annum (mtpa) steel-making capacity by 2030 , might derail its ambitious goal in the steel industry. Let’s decode what is happening in the sector.

What’s happening?

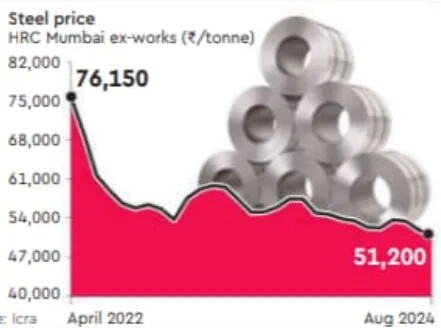

Over the past few months, steel prices have taken a steep dive, reaching ₹51,200 per tonne in August 2024, down from ₹76,150 per tonne in April 2022. This significant drop comes even as India witnesses strong steel consumption growth , which rose by 13.4% year-on-year in FY23.

So, what’s driving this decline?

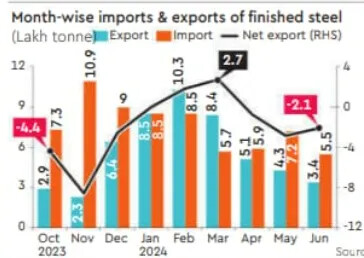

One of the primary reasons behind the price plunge is the growing imbalance between steel imports and exports . In the past, India was a net exporter of steel, which means it exported more steel than it imported. However, in recent times, this trend has reversed. India has now become a net importer of steel, with imports exceeding exports by 0.83 million tonnes (MT) in FY24. In FY24, imports grew 38%, where as exports rose just by 11.5% over FY23.

The reason behind this is cheaper imports, especially from countries like China and South Korea, have flooded the Indian market. According to steel ministry data, China contributed 30.5% of India’s total imports during the April-June period, compared with 28.4% a year ago. The increase in China’s Steel exports by 24.7% year-on-year for FY24, has resulted in significant drop in export volumes of Indian steel Companies. This has affected the pricing dynamics within the Indian Industry.

Analysts have given three main reasons for the worsening of steel trade balance which are mentioned below

- Weak global demand mainly due to tightening monetary policies and geopolitical tensions.

- Low priced imports from steel surplus countries obviously, China.

- A slowdown in Chinese economy majorly due to the real estate crisis, to which steel is the basic raw material for the real estate sector.

What does the experts say?

TV Narendran, CEO and MD of TATA Steel Ltd ., quoted that “These prices aren’t sustainable. We expect the trend to reverse in the next few weeks.”

“Indian steel prices have fallen to their lowest levels in over three years, largely due to shifts in the global market. A notable slowdown in China’s economy has triggered a correction in global steel prices, with Chinese export prices dropping to a four-year low. This decline has led to a surge in HRC imports from Vietnam and China into India,” said Dhruv Goel, CEO, BigMint.

Domestic firms also allege that the Indian steel sector is in a structural disadvantage due to various taxes, duties and levies. Other exporting countries like China, Japan, Korea, ASEAN, etc. are not prone to these taxes.

Conclusion

India’s journey towards becoming a steel powerhouse is fraught with challenges, but with the right policies and industry support, it’s a journey that can still lead to success. As the country moves forward, balancing the dynamics of steel sector will be crucial in ensuring that its steel sector remains competitive and capable of achieving the ambitious targets set for the coming decade.

Your thoughts and views is highly appreciated.