Tata power is more than renewables right now. Valuations are combination of different businesses right now.

Renewables is one

Distribution and privatisation of power in metro cities is one more advantage which tatas have

Plus the EV charging points is a great revenue stream. Rest tata’s would always want tata power to grow profitably as that benefits the tata motors ecosystem too.

1 Like

EV charging points are already part of the renewable portfolio for which BlackRock is coming.

This is a welcome news for TATA POWER

1 Like

One more step hinted towards debt reduction plan by Tata Power management and better than earlier planned Invit.

The management is firing from all sides to become a global leader.

Per above Bloomberg article - 4.5 GW capacities ( current + in progress) will deliver approx 3400 cr EBDITA, I.e. approx 750 cr per GW. For revenue of 12K -14k cr.

Tata power plans to reach 20 GW in next five years( reason for this fund raising), I.e. EBDITA by 2027 to be around 15K cr - again current deal is at 15X EBDITA ( equity + debt at 50K cr and 4K cr for 10% stake), at similar valuations multiple Renewable platform itself could be 180 K cr, even at some discount 150 K cr.

Even if rest of biz which is running at Transmission at 30K cr/ yr and 10K cr/yr at generation( q3 annualized), grows modest at 10% + and valuations are at 1-1.5 X sales ( utilities), could be valued at 70K cr to 100K cr at 5 years.

Sum of parts between, 230K cr to 280K cr by 5 years. Current mkt cap is sub 90K cr.

Another way to look at it would be valuations in more mature market, here are top 10 renewable companies worldwide and are valued 2 to 4X revenue range. Tata power renewable valuations is on upper range being lower base and high growth, so aligned.

This is very dynamic space and capital intensive, renewable energy sector is under lot of attention and re-rating, lot can and will happen including further value unlocking, above calculations are back of envelope and could be off.

Invested

6 Likes

The deal values the renewable unit at Rs 34,000 crore. With a debt of Rs 16,000 crore disclosed by the company, the enterprise value works out to Rs 50,000 crore.

In Feb 2022, Tata Power was looking for a valuation of 6-7B dollars i.e. 45000-50000cr for its renewable business (via CPPIB and General Atlantic) and today’s valuation according to 4000cr raise is at 34000cr so I don’t understand how they are selling it at premium

The other business is valued at 53000cr(at cmp) which is mostly thermal and not growing so this business should not trade for more than it’s book value. The book value for the whole company including the renewable segment is 66.6(according to screener.com) so if I give it 1x book value the share price should be 66.6 + 106.25 (for renewable division) so roughly the fair value should be around 170rs. I’m not even considering debt else the fair value will be far far less.

4 Likes

Key Takeaways from the Conference Call on 14th April, 2022

(Renewable Transaction - Analyst call recording - YouTube)

– EV of TPREL (100% owned subsidiary of Tata Power) - 34k crs Equity valuation + Debt 15k crs = 50k crs.

Valuation may vary on the performance of FY23 (as the stake could be between 9.76 to 11.46, average 10.5 - 34k crs, if stake is 9.76 - valuation will move up else if it goes to 11.46 - it will move down) #important trigger to be noted at the end of FY23

– Invt of 4k crs in the renewable platform (2k in July and 2k crs in 6 months, max by the end of FY23 - through Compulsorily Convertible Preference Shares allotment) – First tranche of proceeds will be received in 6-8 weeks as some statutory approvals are to be completed. Second tranche is dependant on some more CPs. Full money to be received during FY23. Using it for all growth businesses i.e. mfg, utility scale or ev charging. Second tranche will be used on the investments in the growth businesses of the invt platform.

– Mfg of renewable cells & modules, O&M of installed modules, rooftop solar, solar pumps and recharge station business + all future businesses

– Current Op. capacity of 3.3.GW + Pipeline of 1.6GW (to be commissioned in this year).

– Largest EPC co. 1 GW solar cell and module mfg capacity + Addl 4 GW mfg capacity to be built in the near future

– 15k EV chargers have been installed till date.

– Set up of Green platform - providing wide spectrum of products and services under one platform fully consolidating all offerings is the goal of the subsidiary

– Basic Customs Duty on imports of solar cells and mfg applicable from 1st April, 22 hence imports have become more expensive benefitting the co and other indigenous mfrs

– India – Total 150GW installed (Renewable + Hydro), targeting 500GW by 2030-2031.

– Renewable Purchase obligation to go up from 20-25% now to 30-35% in the future.

– Also coal and hydro based producers of electricity, will need to have 20-25% of RE sources of generation installed to supply electricity as well staggered over some time.

– Potential unlocking seen in Rooftop solar and solar pumps

– Hybrid solutions - Solar + wind storage, solar + hydro + wind storage, solar + hydro storage are also going to come up in the future. Co. will stand to benefit from this.

– Co. has no intention of an IPO at the moment nor any immediate dilution of equity

– No change in accounting policies or reporting.

– Net debt target - Rs. 250 bn for FY23

– Cant use current money to deleverage Tata Power standalone.

– CGPL carry forward losses benefit will be available to Tata Power standalone after merger.

7 Likes

The carry forward loss of CGPL will help savings in terms of taxes for TATA POWER over the next 10 years. It’s a huge positive thing.

1 Like

As per the news item in the case of companies like Adani Power, Tata Power’s subsidiary Coast Gujarat Power Ltd and Essar Power, the government has decided that the entire cost of imported coal shall be allowed as pass through until December 2022 without any ceiling if the imported coal prices remain above the pre-Covid level.

Hope this will bring cheers for TATA POWER.

5 Likes

Analysts downgrade Tata Power after the deal

1 Like

1 Like

3 Likes

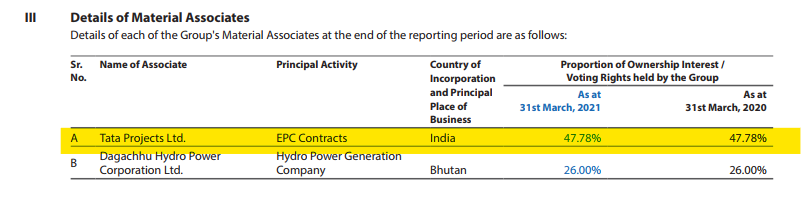

Here in the below article of Business Standard, they have mentioned “Tata Power holds 47.78 per cent stake in TPL (Tata Projects Limited) , while the rest is owned by its promoter Tata Sons.”

Construction, EPC business in India is growing at good pace.

Can experts please throw some light on this stake and subsidiary ?

Thanks.

4 Likes

Thank You Abhishek Sir. I appreciate your reply. I did find that in the Annual report.

My query was regarding the TPL as a whole, as I didn’t found much about management commentry, future plans regarding this stake, this subsidiary is less discussed as it will add more wings to Tata Power if performed well. (As 47.78 is substantial stake).

Please delete this post if found repetitive, or if it doesn’t add any value to the thread.

1 Like

1 Like

I did not read this article as not actively tracking tata Power, but correct me if wrong, how can tata copy Reliance/Adani…Tata Bp Solar had been years back into renewables…much before and ahead of others?