Tata Power has sought bids for the supply of wind turbines with a total capacity of 3 gigawatts. The wind turbines will be installed at the company’s renewable energy facilities across the country in the next three to five years, the report said.

Suzlon is one of the listed company in the race for the bid.

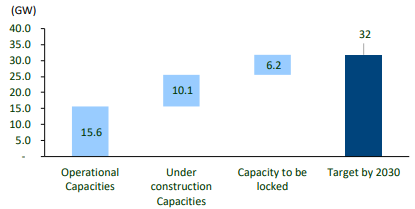

Tata Power Targets 20GW Renewable energy capacity by 2030. Current - 10.5 GW (Double)

Tata Power: A Strategic Play on Renewable Energy and Infrastructure Growth

Growth Targets & Financial Projections:

Revenue, EBITDA, and PAT expected to grow 1.6x, 2.4x, and 2.5x respectively by FY30.

Capex guidance increased to Rs. 25,000 crore annually, with a cumulative Rs. 1.46 lakh crore spend till FY30.

EBITDA share from renewable energy expected to rise from 27% in FY24 to 51% in FY30.

Renewable Energy Expansion:

Tata Power to increase renewable capacity from 6.7GW to 23GW by FY30, with a strong 5.6GW pipeline (100% land visibility, 90% PPAs signed).

Targeting 45GW of annual capacity additions across India to meet the 500GW renewable target by FY30.

Solar rooftop market poised for strong growth, with Tata Power holding a 13.1% share and revenue expected to rise from Rs. 1,715 crore to Rs. 11,000 crore by FY30 at 36% CAGR.

Transmission & Distribution:

Transmission capacity to grow significantly, from 4,633 Ckm to 10,500 Ckm by FY30, with a Rs. 24,850 crore capex plan.

Distribution business to expand to 40 million customers by FY30, up from 12.5 million today.

Pumped Storage Projects (PSP) & Hydro:

Tata Power targets 12GW of pumped storage capacity, with construction of 1GW Bhivpuri PSP beginning in 2025 and 1.8GW Shirwata PSP in mid-2025.

Total hydro capacity expected to rise to 5GW by FY30 with PSP and Bhutan projects.

Strategic Asset Divestment:

Company plans to divest non-core overseas coal and hydro assets, focusing on growing its footprint in India’s renewable energy sector.

Strong Domestic Solar Demand & Government Support:

Protectionist measures, including 40% BCD on imported solar modules and 25% BCD on solar cells, effective from Apr’22, are enhancing the competitiveness of domestic players.

Government schemes like PM-KUSUM, PM-Surya Ghar Muft Bijli Yojana, and the CPSU scheme promote domestic content requirement (DCR) solar modules, boosting demand for Tata Power’s domestic production.

With the implementation of Approved List of Models and Manufacturers (ALMM) and the introduction of Approved List of Cell Manufacturers (ALCM), demand for domestic cell manufacturers like Tata Power will increase.

Key Risks:

Slower-than-expected ramp-up in renewable energy and distribution growth.

Lower-than-expected profitability in the solar EPC business.

Sources:

Reports by Axis Securities & Mirae Asset Sharekhan

Tata Power, through its renewable arm Tata Power Renewable Energy , has partnered with the Odisha Renewable Energy Development Agency (OREDA) to drive awareness and accelerate rooftop solar adoption under the Pradhan Mantri Surya Ghar Yojana (PMSGY).

Odisha offers the highest solar subsidies in India, providing up to ₹60,000 for rooftop solar systems up to 3 kW.

Combined with the ₹78,000 central government subsidy, consumers can avail total subsidies of up to ₹1,38,000 for rooftop solar units upto 3 kW, making solar energy more accessible and affordable for residential customers.

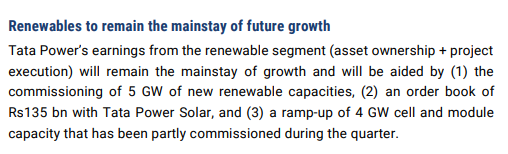

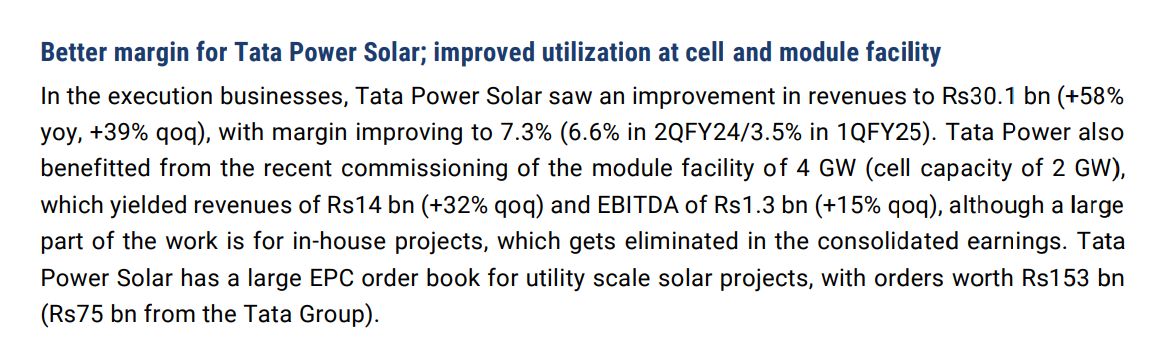

Better margins in Solar EPC segment (Order book INR 140bn)

RE portfolio

Mundra UMPP (as Section 11 has continued till Feb-25)

Capacity is increasing from 15GW to 22GW+ by FY27E

Investment thesis:

Tata Power being the largest private integrated utility and is present across the value chain, from generation to coal mining to power dist and power equipment

To achieve 15% ebitda CAGR over FY25-30E, it envisages INR 240-250 bn pa capex over FY26-30E with a mix of renewables at 60% transmission ~ 20% distribution 7% pumped hydro storage 10%.

Tata power is expected to report an annual OCF of INR 150 bn and b/s NDER is at 1.1x. Strong b/s will help undertake capex and additionally it is planning to sell/monetizeassets USD 1bn out of india

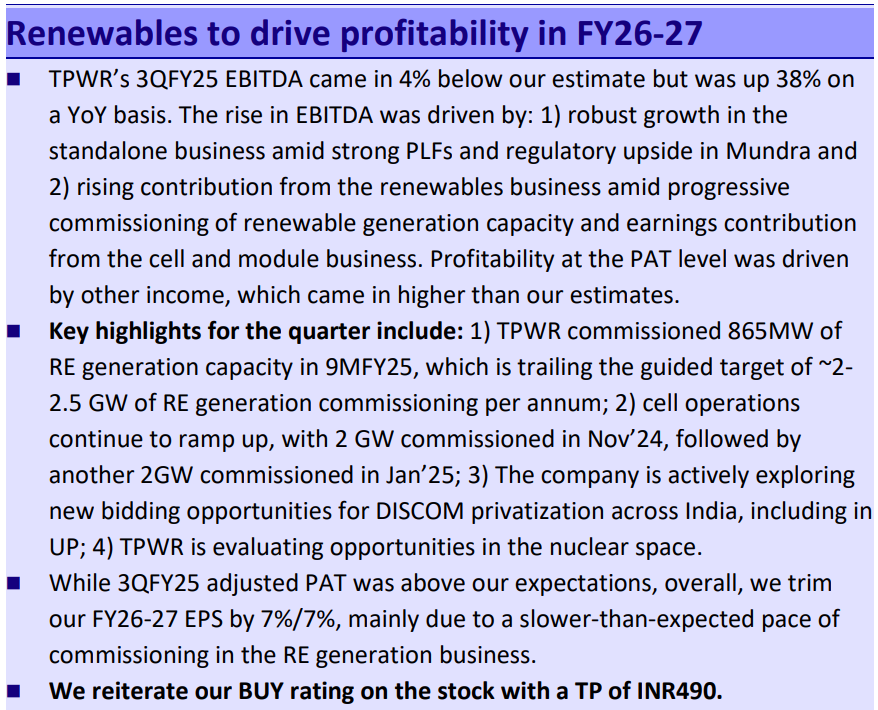

3QFY25 profit was boosted on account of the regulatory order for Mundra

Coal earnings decline gets arrested, further support from the extension of Section 11 order for Mundra

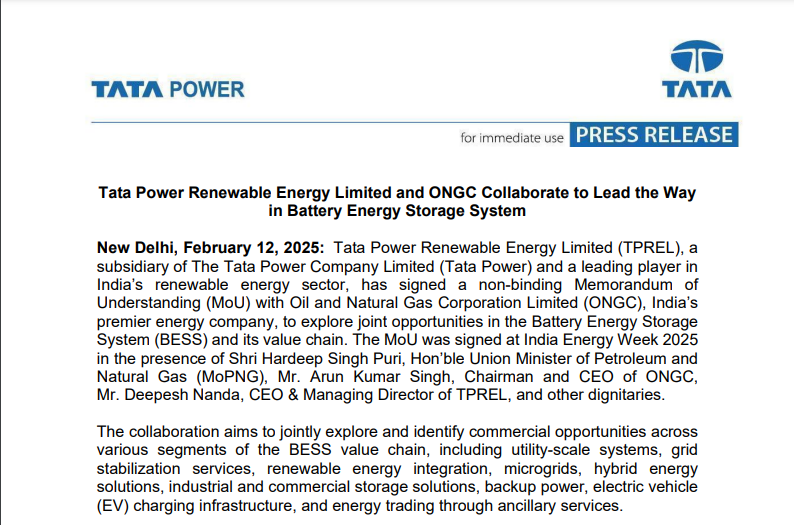

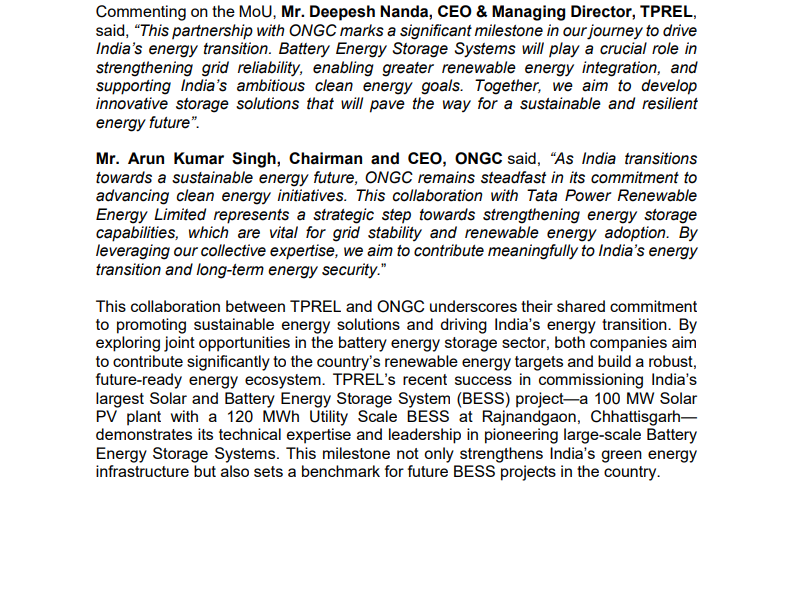

This is a Nonbinding MOU. While it is still a very good development, we need to wait for it to become a real value-generating partnership that adds to the top and bottom lines. May be in coming days more will be disclosed if anything turns into a contract.

Tata Power is at the cusp of an earnings inflection as its new 4.3GW solar-cell module manufacturing plant ramps up production and RE capacities get commissioned. Continued imposition of Section-11 will likely keep Mundra losses minimal, and tangible progress on UP distribution privatization is an optionality

Tata power is vertically integrated business model, allowing it to maximize value capture. H1 should inflect earnings as tata power begins partially placing its domestically manufactured cell-modules in high-margin rooftop and DCR projects.

Mundra losses in check; distribution privatisation anoptionality:

Thanks for this post. I was thinking the same yesterday. The Capex cycle for Solar Module Manufacturing factory has come to an end and its now time to reap its benefits in form of increased returns. And at current juncture where it has already fallen much from its previous highs, its perfectly a great time to get in Tata Power for a 3 to 6 Months trend upwards.

And i got into the Tata Power futures to enjoy the leverage of 5x capital. Reading your message today added to my conviction. Thanks.

Buying Futures come with leverage. You need to block only a margin(fraction) of exposure (capital) to buy futures. I would suggest you to look at Futures Module of Varsity by Zerodha if you are not very well informed about futures as a derivative. The concepts are very simple,unlike the horrors of options trading which i never understand at all.

This is a very nice instrument. If understood correctly and applied with an investment mindset, it can create wealth much beyond vanilla stock investment .

Discl: Personal views. Not sebi registered advisor. Consult your financial Advisor for right information.

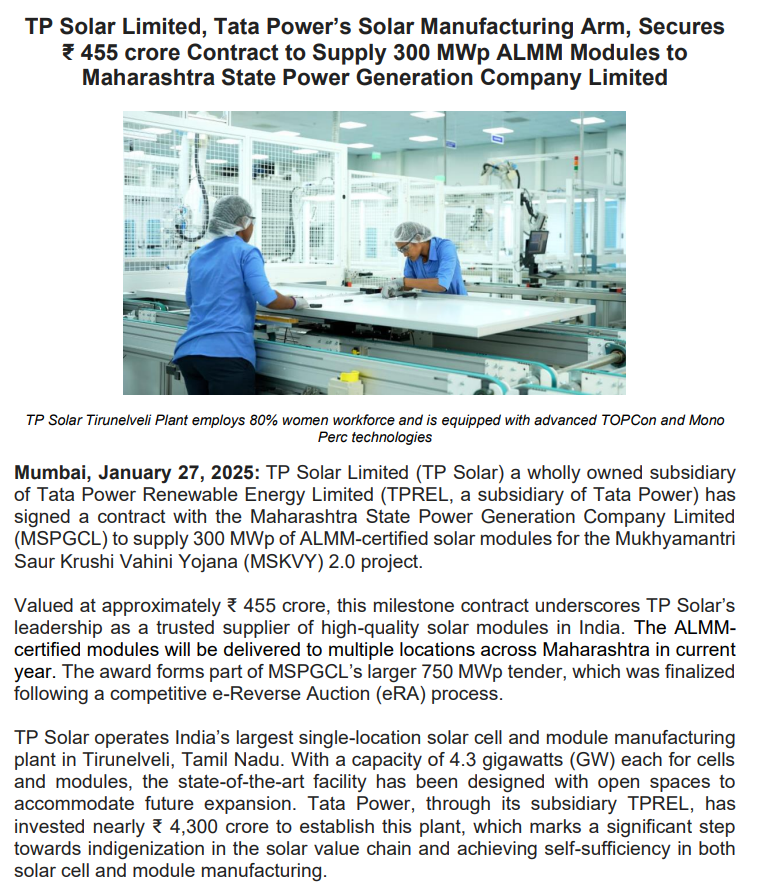

Small Wins. Such orders from PSU makes Tata Power a recognised vendor for all EPC projects. A lead against unfair players like Adani. This is truly symbolically very important for Tata power.

The tata power is a growth story that will be the next trent of Tata Group, just as trent was next Tata Motors. Its a story that can keep unfolding till 2030, when all its capex will start adding value to bottom line.

Discl: Not buy sell recomm. Views are biased. Invested since 2021 and it is a significant portion of my pf.