Tata Motors | Q3 Highlights

Outlook:

We expect underlying domestic demand to improve gradually on account of infrastructure spends, slew of exciting product launches and stable interest rates.

While JLR wholesales are expected to improve further in Q4 FY25, we remain watchful on the overall demand situation, particularly in China.

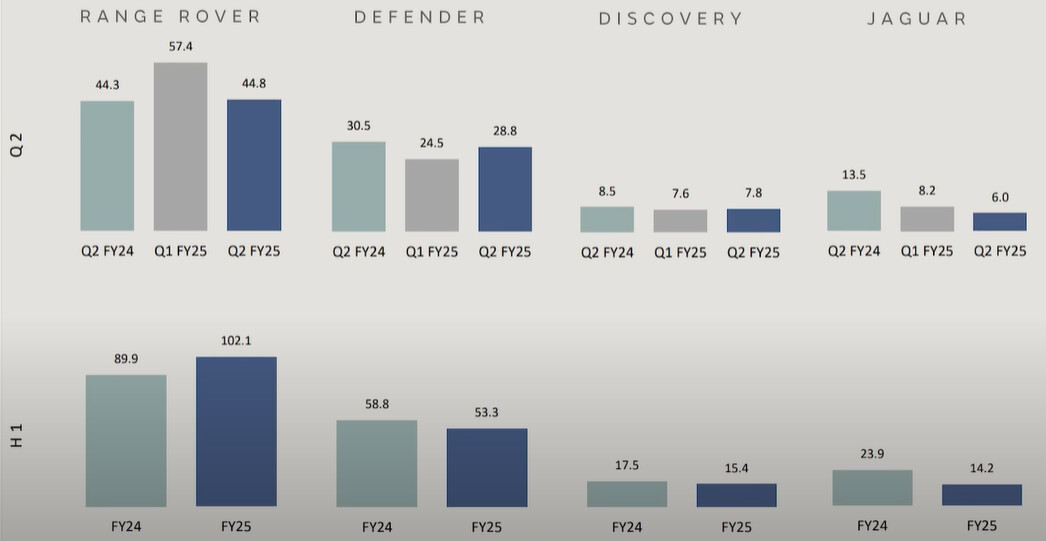

Q3 FY25 Revenue at £7.5 billion (+1.5%), EBITDA 14.2% (-200 bps), EBIT 9.0% (+20 bps), PBT (bei) £523 million

YTD FY25 Revenue at £21.2 billion (flat), EBITDA 14.0% (-180 bps), EBIT 7.8% (-50 bps), PBT (bei) £1,614 million

JLR delivered a robust third quarter in FY25, with record Q3 revenue, the highest EBIT margin in a decade and a ninth successive profitable quarter

Cash balance was £3.5 billion and net debt £1.1 billion, with gross debt of £4.6 billion

Total liquidity was £5.1 billion, including the £1.6 billion undrawn revolving credit facility

JLR Outlook; Looking ahead, while mindful of the challenging economic backdrop, the Company is on track to achieve its profitability and cash flow targets in FY25, with EBIT margin 28.5% and positive net cash.

JLR Revenue £7.5b up 1.5%, EBITDA at 14.2% (-200 bps), EBIT at 9.0% (+20 bps)

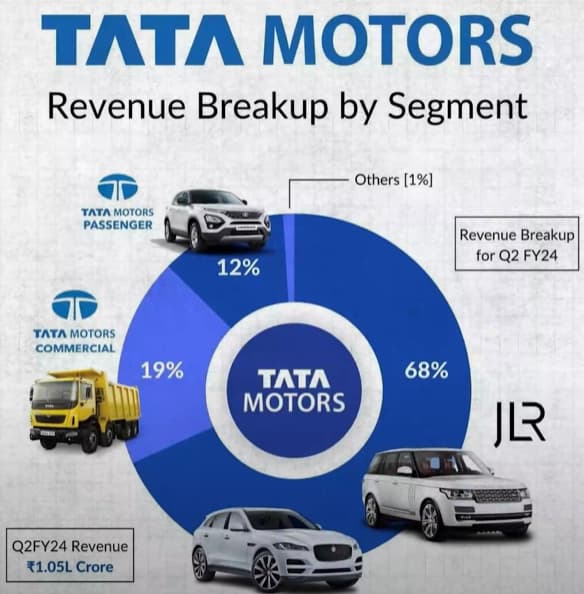

Tata CV Revenue ₹18.4K Cr, down 8.4%, EBITDA at 12.4% (+130 bps), EBIT at 9.6% (+100 bps)

Tata PV Revenue ₹12.4K Cr, down 4.3%, EBITDA at 7.8% (+120 bps), EBIT at 1.7% (-40 bps)