In theory all 3 taxes - Dividend tax, STCG, LTCG are applicable for those who had DVR shares and opted for it to be converted.

However, the calculations involved are little complex, depending on your purchase date, qty, Deemed Dividend concept, TDS deduction by Tata Motors on the Deemed Dividend amount, potential offset of some LTCG against the same, deduction of STCG etc. I would suggest you download the sample tax calculator that they had issued before the conversion. Plug-in your numbers and change the value of Deemed Dividend as per the latest value they published after conversion…you will get all the answers.

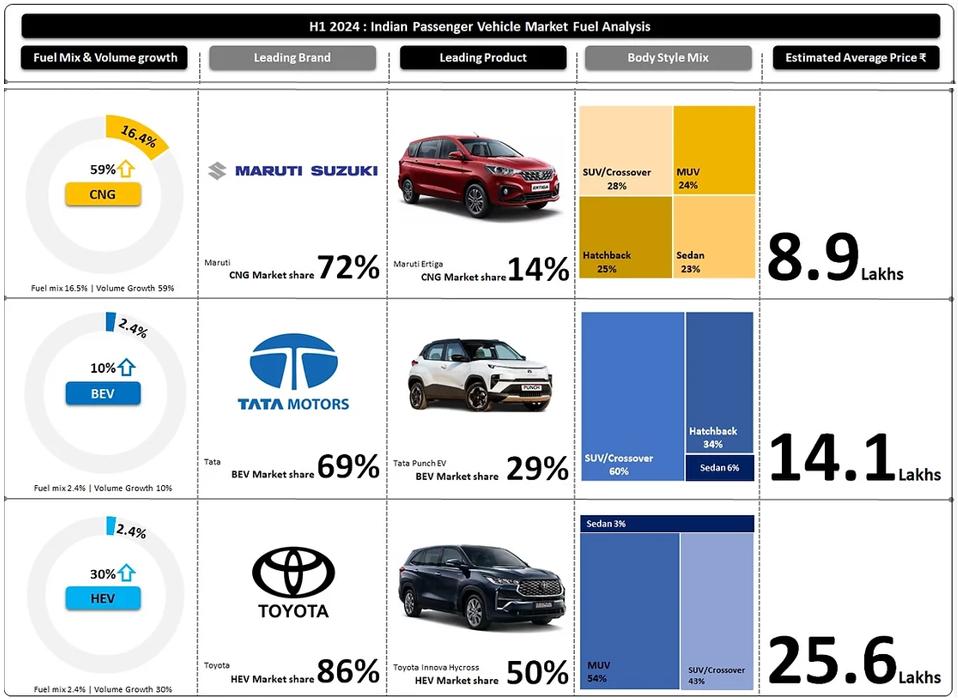

Growth in CNGs was largely driven by new products like Tata Punch with dual-CNG tank, and Maruti Fronx, both launched in H2-2023. The rest of the growth came from higher sales of Maruti products: Ertiga (+19%), Dzire (+12%) and Brezza (+10%).

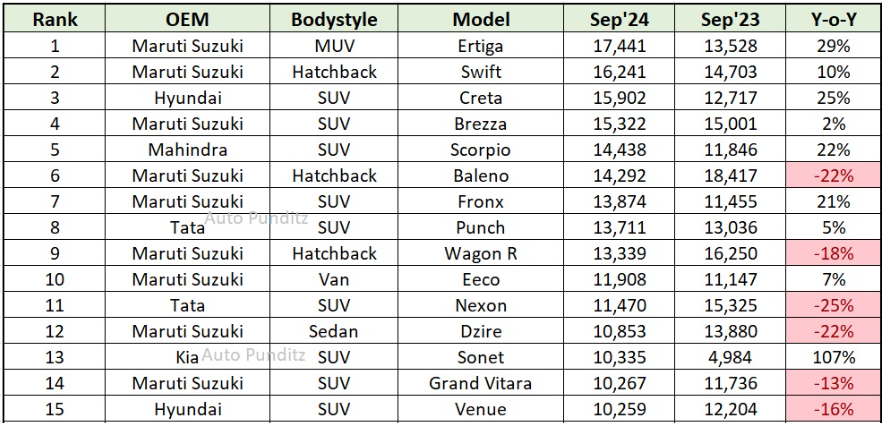

Mahindra with its SUV-heavy portfolio has taken over Tata Motors September sales fig. and is behind Hyundai with a mere 40 units gap.

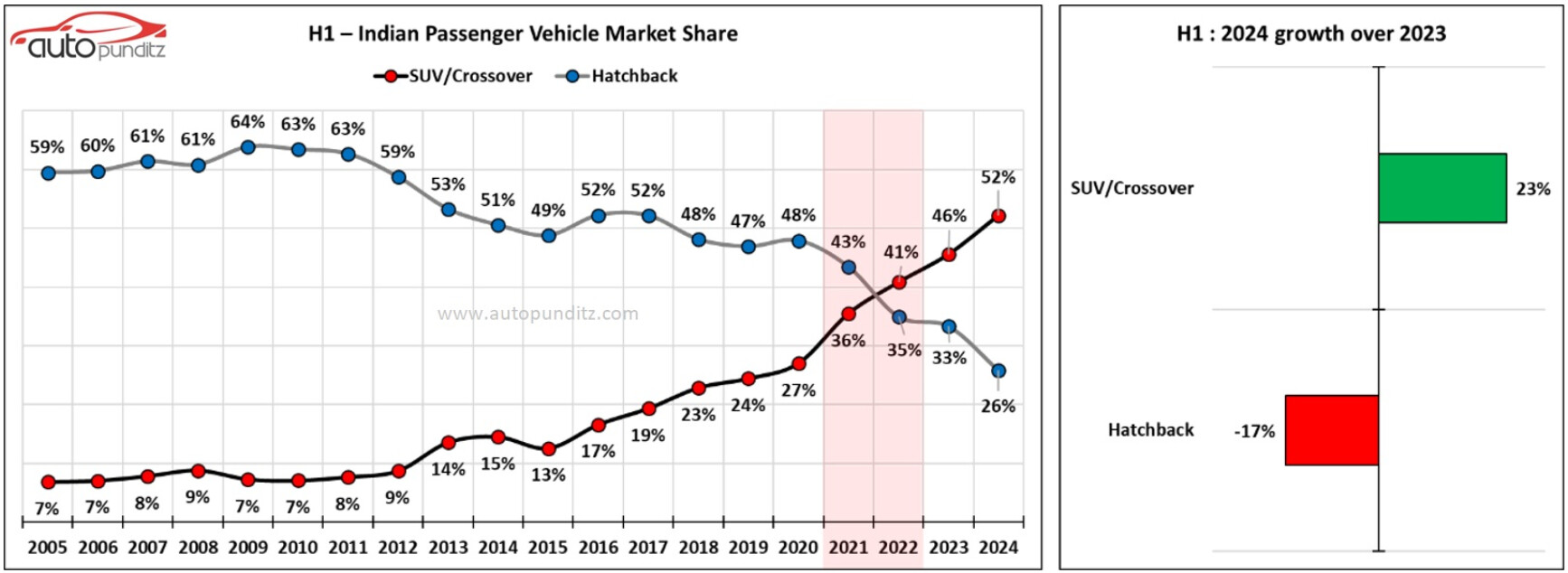

We're all aware that there is a shift towards SUVs/MUVs by the aspiring

Middle class, for the better looks and superior feeling of ownership.

But what about the shift from EVs?

India mirroring the trend in global EV sales.

Europe which saw BEVs record their largest YoY decline since January 2017 – of 36 percent in August – demand for EVs in India fell to a 19-month low of 5,733 units in September 2024.

Demand rose consistently and hit a high of 9,661 units in the month of March 2024. However, since then, as per retail sales data from the Vahan website, monthly numbers have gone down, dropping to 6,630 units (down 5 percent YoY) in August and now 5,733 units in September.

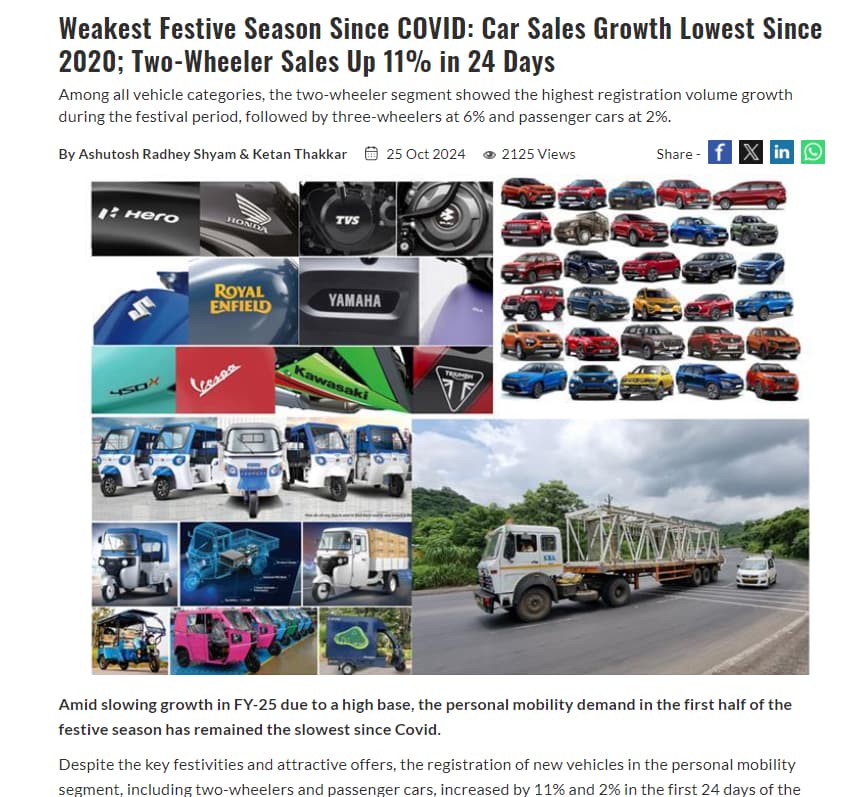

Slowdown in the entire Auto sector during this festive season.

Tata Curvv looks promising. It gives the vibes of Lamborghini Urus. It has sold 8,218 units in the 2 months since its launch and contributes 10% to Tata Motors’ passenger vehicle wholesales. I hope the management learns what types of cars consumers prefer and makes more of these

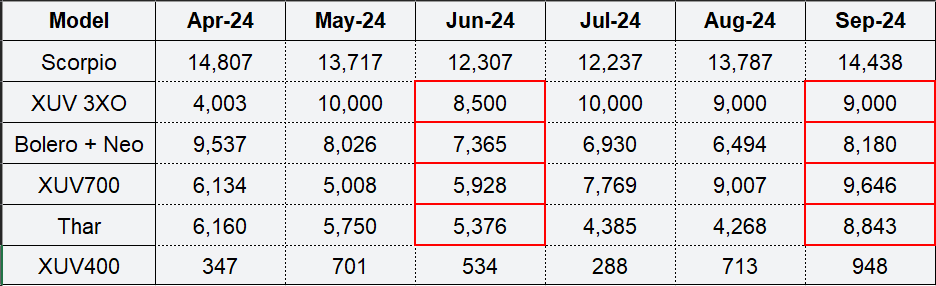

Design preference is highly subjective. Tata Curvv will compete in mid-end SUV space which is already dominated by Maruti, Hyundai. Now, Mahindra’s new 3XO is also selling like hot cakes with monthly 9,000-10,000 units. I’m sure Tata Curvv will also find its place in this fragmented market, but…

More emphasis should be given upon the fact that Tata’s dominated space of BEVs is facing a major slowdown and no signs of recovery. Tata’s dominating place in BEVs and JLR segment was the only reason I was interested in this company. However both the businesses are facing a slowdown.

I believe a lot of this has already been factored into Tata Motors’ valuation. It’s trading close to its all-time low PE. If the sales pick up in the coming years, the stock should get re-rated quickly.

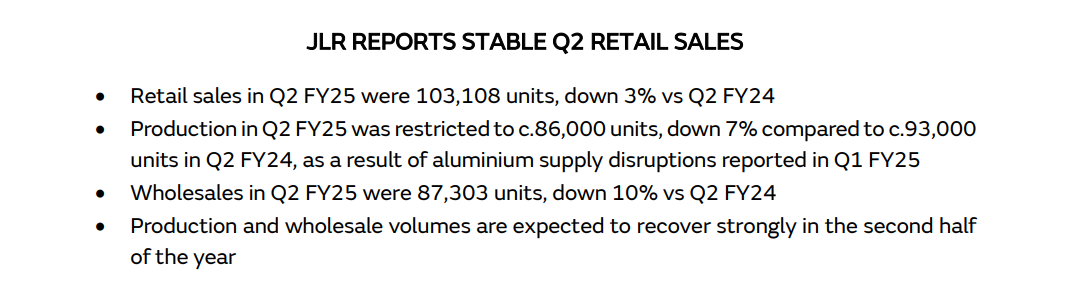

JLR has been transparent about expected muted demand and some supply chain issues, but they’re still aiming for an 8.5%+ EBIT margin for FY2025. Also, Tata Motors market share in domestic PV market has improved from 5% in FY20 to 13.3 % in H1FY25

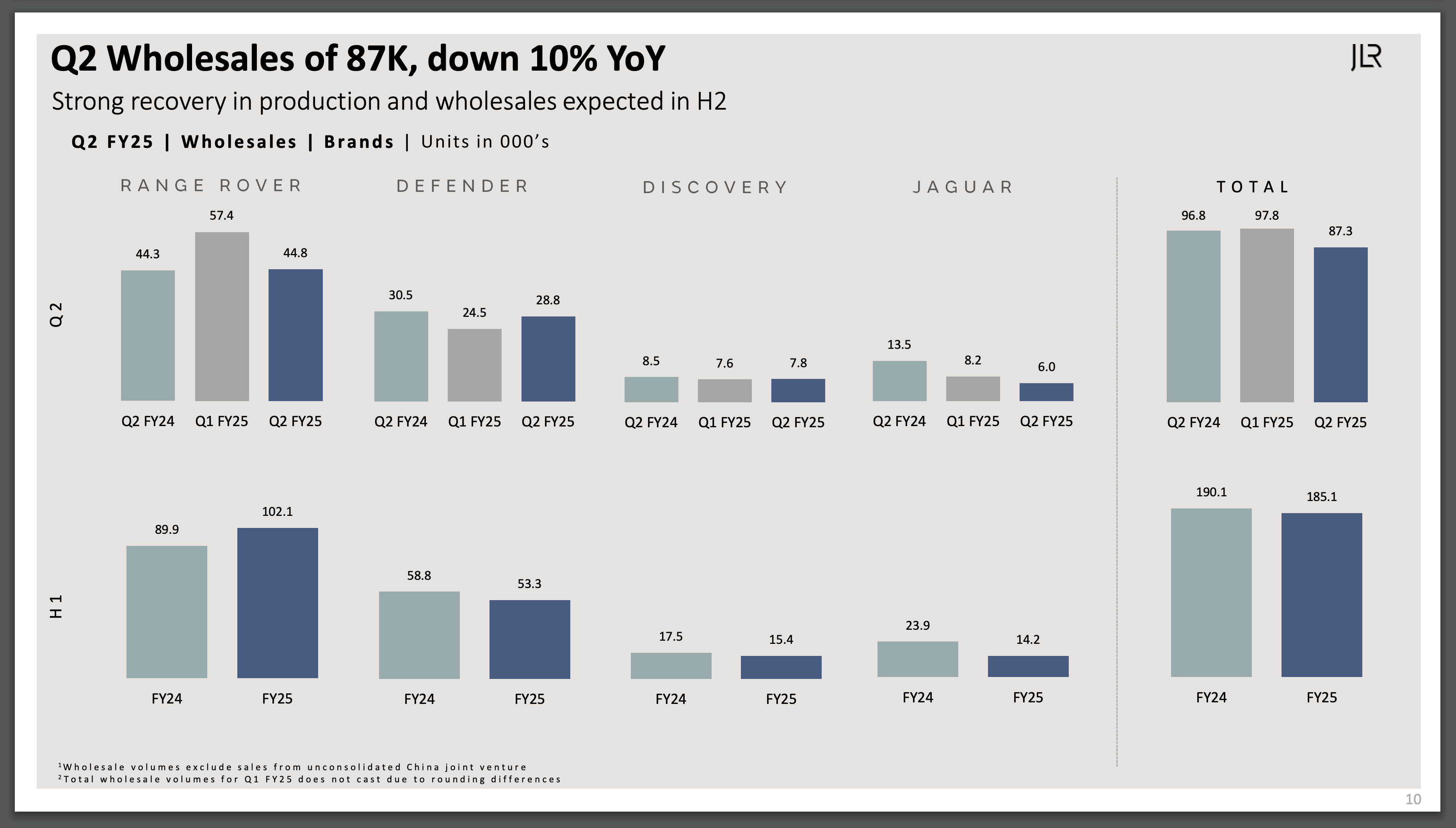

How do you read TataMo’s results? Overall weak numbers, even below lower expectations, however management seemed positive on recovery - both in JLR (one off Aluminium supply issue easing, China may remain a drag though), PV (good festive season demand pickup). Wholesale sales reduced to manage channel inventory. Overall, they kept FY guidance intact with recovery expected in H2.

So, what’s the view from here: Is worst behind now for the stock after shap 35% correction from top? Or slower EV and continuous market share loss will continue to drag?

Technicals -

Might take support near 722 price range and then consolidate for the short term. RSI likely to reach oversold zone before consolidation starts.

CVs cycle is already at an advanced stage of its cycle in the short term (2 years), it has already shown a very strong growth of 30% CAGR in the last 3 years. There will be a slowdown in govt. infra and road construction capex.

Tata’s CVs sales were down by 20% in H1 FY2025.

Private Vehicles

CVs cycle is already 20% above its 2019 peak, already at advanced stage with expectations of low single digit growth in the short term (2 years).

Tata EVs will face fierce competition going forward. Mahindra to launch their two EVs on 26th Nov. Maruti to launch its first EV in Jan. and Hyundai will launch Creta EV in Jan. as well.

All these manufacturers will launch their EVs in the entry level segment where Tata Motor holds 70% market share. Since there is no subsidy push from the govt. for EV cars, this would only lead to loss of Tata Motor’s Market share.

Tata Punch EV and Nexon EV, which have 30% and 13% market share in EVs respectively, have already started facing competition from MG’s new Windsor EV with BAAS(Battery as a Service) making the buying price very aggressive. MG Windsor is much more spacious that Tata Nexon but cheaper by ₹2L. MG Windsor was the highest selling EV in the month of Oct., 30% of the total EVs sold.

This rental based model in EVs is also Tax beneficial for the Corporates so going forward other OEM’s are also likely to push BAAS for their EVs. So Tata Motors also needs to implement it.

Jaguar Land Rover JLR

I thought only JLR could save Tata Motors yet again but then came across this article… This only means company will have to book huge book exceptional loss in the coming quarters.

absolute bonkers. this is practically brand suicide. there is no way to fix this. decades of heritage undone in one campaign.

but the good part is they did not drag land rover into this mess. the volumes of Jaguar are much smaller, albeit nuking the brand equity like this is nothing short of a crime.

Please go through this article, you guys will have all your questions answered.

Key Notes :

The group overall is now profitable and is reducing its debt. One of the key elements is that success has been the ability of the Range Rover brand.

In 2019, the average sale price for a car from JLR was £44,000 ($55,000). By early 2023, it was £71,000 ($89,000). The company was selling 660,000 units a year in 2019, but not making a profit. By 2023, the volume had dropped to 300,000 units, but with a positive balance sheet.

The Range Rover and Land Rover models reportedly now make $25,000 profit each on average.

Jaguar was still making a loss per car.

Jaguar’s most popular model the F-type, only sold 64,241 units worldwide in 2023 out of JLR’s total of 431,733.

Jaguar is ending sales in the UK this month, which will mean a break of over a year before the EVs sales kicks in FY26.

Jaguar will reveal new electric car on 2nd December with a price expected to be above £100,000 ($125,000) and with this price range JLR’s avg. price per car is bound to go up.

The point is that everyone is now looking at Jaguar.

Unless the car can do magical stuff or there is twist on the next part of the ad where a jaguar eats the ghastly models , nobody but Keir Starmers ardent and rich followers are going to buy it. Jaguar management somehow took Elliot Carver too seriously . Disregarding 95% for the sake of 5% may seem a good idea to politicians but hardly any man or woman will want to be seen driving a car so explicitly promoted for the LGBTQ+ .

Dear Sir PLease guide me from where you received the calculation about dvr conversion and tax deduction? I have tried to contact linked in to get explanation but they have advised me to log in swayam portal and log in and make request. I am trying for that but most of the time server is not responding and I come back to circle back. I am NRI and I had 300 dvr shares and was allotted 140 instead of 210. My broker sharekhan also unable to give explanation and he says contact RA. I got credit of 1134.68 from tml securities on 25 sept 24 but no mail from tata motor dvr so far.

I will be great help to me to understand the conversion .