The service centre problems are well aware of, but low quality cars, I am hearing for the first time. How or why do you say that?

1 Like

I saw this issue mainly with Harrier Cars where their infotainment systems have lots of bugs, body panels are not fit properly on the cars, the bonet of the car doesn’t properly align during closing and many more issue. These are mainly because of improper quality checks and issues with production line. Many customers bring their cars to the dealership after 10-15 days after delivery and the dealer are facing lots of troubles due to these issues. Some issues they fix it but issues like body pannel allignment it is really tough for them. As you can see from one of the old thread that how much Tata’s spend in warranty compared to other brands. But this issue is associated to Tata Motor and not on JLR. But for valuation perspective if you want a apple to apple comparison then I see value in Benz and BMW which are the trading at 4-5 PE and a dividend Yield of 7-8%.

4 Likes

Fair point, however I don’t see these quality issues bearing a meaningful drag on sales or valuations. Also the India PV is hardly 15-18% of overall sales (please verify).

I think with the demerger of CV and PV, there should be some value unlocking. I think there next step will be carving out EV from PV separately, as they already have raised multiple fundings on the EV biz. The healthy balance sheet, coupled with EV shift seems like a relatively safer stock, with moderate growth potential.

3 Likes

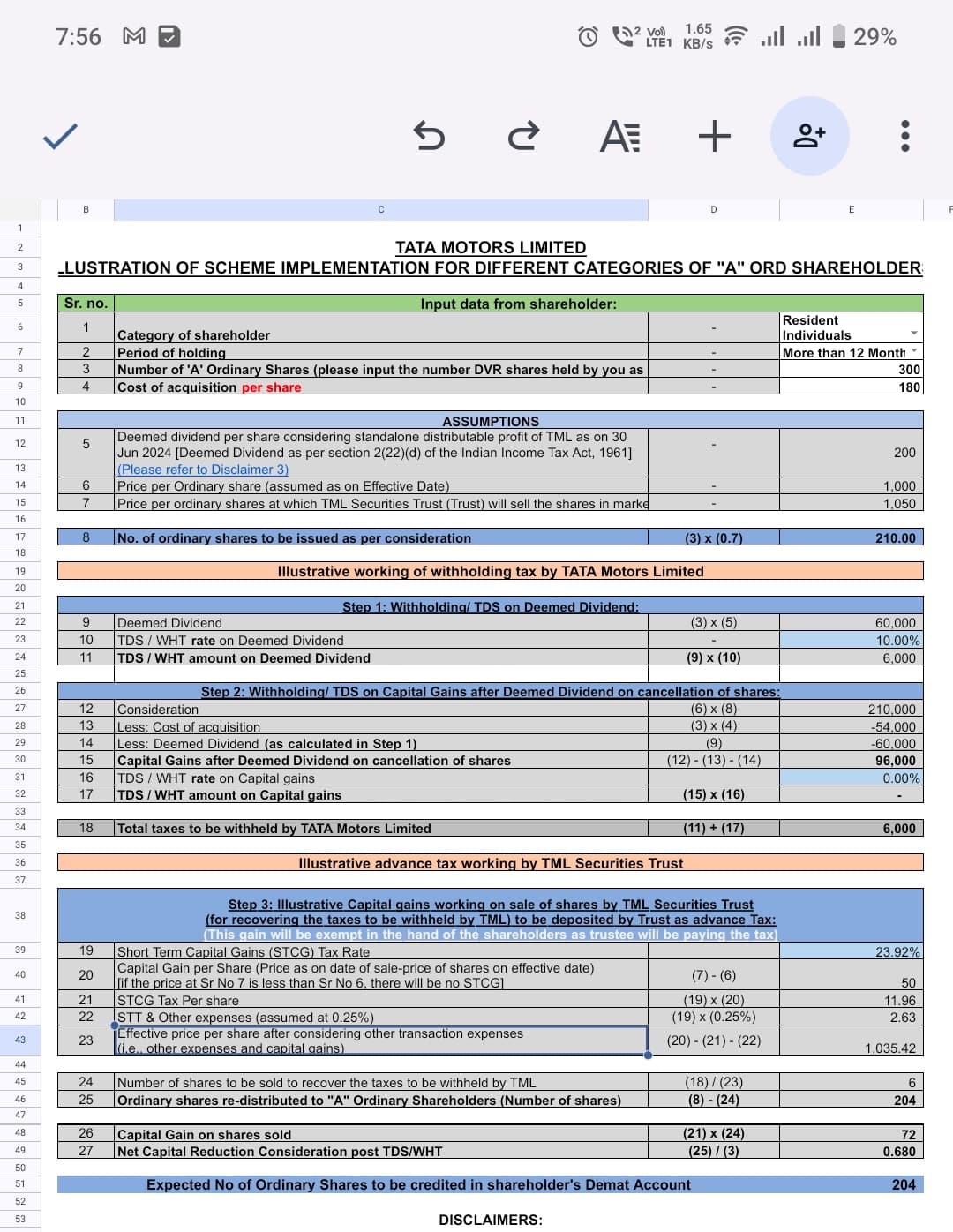

Has anyone studied the tax implications arising out of conversion from DVR to Ordinary shares? As per the detailed email sent by the company the implications cut across 3 categories - deemed dividend, short term capital gains and long term capital gains…please note that all 3 may become applicable as part of conversion journey (without you selling any of the shares).

Biggest cause of worry for me is Deemed Dividend amount of Rs. 194 per share that they have indicated in the sample calculation under annexure 1 of the detailed email. Tax liability on deemed dividend itself can go very high for those in higher tax brackets. And depending on your original cost of acquisition of DVRs and timeline, long term may also kick in. Minor short term capital gains will also kick as company has to deduct TDS. Company will sell TDS amount worth equivalent shares in open market and credit the rest.

As per current calculations it looks like a losing scenario for those retail investors with significant DVR holdings. Not to talk about the additional downside of acquistion date of new shares getting reset to when they are issued (as against original acquisition of date of DVR shares). So selling in next 12 months could attract Short Term gains instead of long term.

Please note whatever I have written above is my understanding of the situation. I can be completely wrong here. Hence want to check with others on the forum who have independently done any study and calculations on tax implications to compare notes and take a decision.

Any inputs will be helpful.

6 Likes

The scenario of converting DVR to Ordinary shares has limited precedence in India. I have been holding DVR shares from last many years and have sold out yesterday due to the tax impact uncertainty.

AJ

Disclaimer: Opinion above is biased.

1 Like

Tata motors has released a FAQ on this and also a sample calculator. While it does not completely remove the ambiguity, it does help reduce the range of estimate.

FAQ:

Sample Calculator:

https://www.tatamotors.com/wp-content/uploads/2024/08/A-ordinary-shareholders-illustrator.xlsx

2 Likes

I am unable to understand how dvr purchased before 31 Jan 18 will be considered for tax calculations? The sample calculator does not consider grand fathering effect.

Secondly is it better to sale the dvr and get the grand fathering effect now?

Can somebody guide me. I am NRI and have invested in both dvr and ordinary shares in 2017

1 Like

Sorry . I have stated that I have purchased dvr in 2017 . it is wrong. they were purchased in 2021.

Regret the mistake I have done in my previous statement.

1 Like

Thanks for the Excel sheet.

I have put my holdings of 300 dvr shares at cost of acquisition 180 per share, all ltcg and bought after grandfathering.

I see there’s dividend withholding of 6000 TDS at 10% rate. I’m in 35% tax bracket so I have to pay 21k in total as tax.

The Excel sheet doesn’t consider shareholders other ltcg (if he has already crossed the 1 or 1.25 lakh limit).

The conversion factor of just 0.7 looks like short changing the dvr holders. I don’t see any advantage in converting the shares to ordinary shares compared to sell dvr and buy tata motors ordinary shares. It will be helpful if anyone can look at my case and say if I should convert or just sell now itself.

Is the company issuing new ordinary shares to compensate for dvr shareholders? If so, then free float is not going to reduce and eps will remain the same. No big advantage for dvr-converting and existing ordinary shareholders as well.

4 Likes

Since the test calculator is built on multiple assumptions (especially on profit pool attributed to DVR share holders which determines the “deemed dividend” amount), it is hard to say with any certainty whether the actual tax outgo will match with what is provided for in the sample calculator or will be higher or lower. Deemed dividend amount per share will likely be different on 1st Sept as current calculation is based on 30th June 2024 numbers. Whether it will be higher or lower, I have no clue.

Based on As Is comparison, my tax outgo would have been 40% higher if I had agreed to hold onto DVR shares and opt for conversion. The additional effort, time, anxiety and head ache of trying to figure out the actual tax outgo and whether it will be beneficial was not worth. So finally sold my shares today.

1 Like

This “scheme” is completely against retail investors I think

Issue DVR at 10% discount and swap them back at 30% discount

From news article…

“Post conversion, the promoters holding in Tata Motors will increase to 42.62 per cent from 41.23 per cent, while that of public will slip to 57.38 per cent from 58.77%”

With all these disclosures and FAQ’s, they should have given a FAQ from shareholders perspective too to highlight tax incidence for a retail investor

This proves to me that Tata Sons has always worked against retail investors - if one was to look at all the cross holdings by Tata listed companies with each other done over last 3-4 decades - all these were actually done on behest of Tata Sons instructions to benefit at the cost of acquiring Tata company’s retail shareholders

1 Like

On hindsight - Tata as a group keeps creating value for its enterprises and the corporate restructuring they undertake usually result in value unlocking for all share holders. I kept buying Tata Motors and DVR between 2018 and 2021 and the wealth this company has created between 2021 and 2024 is tremendous irrespective of relative adverse conversion ratio.

AJ

Disclaimer: No holdings currently. May re-enter at an opportune time. Consider my views as biased.

1 Like

So don’t get me wrong

Indeed it has created wealth

My limited point was that in past / recent past when a Tata group company was saved by another Tata group company… it come at the cost of investors of latter (saver) Tata group company - and that’s how Tata Sons operated and benefited.

2 Likes

Do you plan to buy the regular Tata motors shares with the proceeds? I had purchased the DVR shares in Dec 2020 for 75. Had no intention to sell. But now it looks like if I held onto the DVR, I have to pay more taxes so I sold them. The PE seems cheap and with the cancellation of DVR the EPS of regular shares get a 18 percent or so gain. That would make the PE

1 Like

Hey Vinkayaka, Thanks for the insights. What’s the rationals for 18% upside in PE after DVR shares merged in regular Tata shares?

1 Like

I got that from this video

It makes sense too since the DVR shares holders are being shortchanged by giving them 7 shares instead of 10. When I bought the DVR I assumed I was buying an equal part of the company as of a regular shareholder except I am giving up the right to vote which I don’t use anyway.

6 Likes

I have not yet made up my mind on buying Tata Motors. As of now, key drivers of Tata Motors profitability has been performance of JLR…On positive side anticipated, interest rate reductions in key geographies like US, EU and UK etc. may help. So also the fact that Sept-Oct is when UK based car companies usually launch new car models. On the negative side, one of the big contributors to JLR in recent past - China is undergoing its own challenges in the economy. So if you can reasonably guess how JLR is likely to perform in coming quarters, that should answer the question for you.

The other known trigger of demerger of PV and CV business is still some distance away (unless the demerger date has already been announced).

Hope this gives you some food for thought. No recommendations, please do your own due diligence.

3 Likes

Agreed. I sold my DVR around 750, and havent yet converted them to Tata motors. I am not eager to buy it either, if I get TATA Motors around 900 levels, I will consider adding it again.

I think I missed the opportunity to exit

Swap Trust Distribution (cash) / Dividend / Deemed dividend was so confusing to understand

Overall I think Tata Motors did a poor job with communication… and more importantly short changed retail investors with the discounted swap ratio.

5 Likes