With DVR stock going for merger with Tata Motors, and then for bonus of another entity; should we start with SIP buying in this stock???

I am sitting at 240% increase in Tata Motors DVR. Should I start doing SIP in the stock now or should I wait for the merger to happen first?

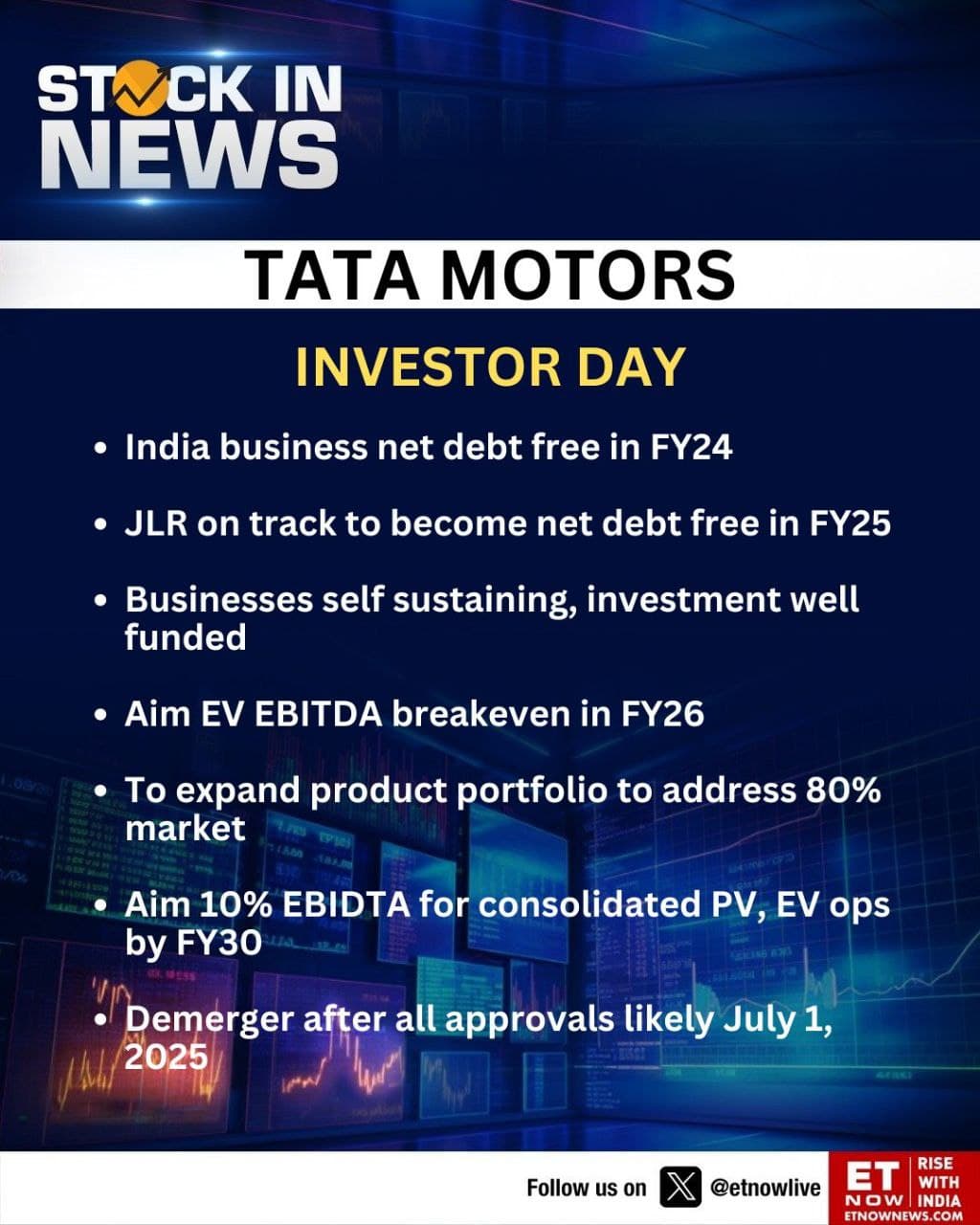

Tata Motors

EU MOVES AHEAD WITH PLANNED TARIFFS ON EV IMPORTS FROM CHINA - BBG

EU PROVISIONAL DUTIES ON CHINESE EV IMPORTS TAKE EFFECT JULY 5

EU TO ADD 37.6% AVG DUTY ON NON-COOPERATING CHINESE BEV MAKERS

EU TO ADD 20.8% AVG DUTY ON COOPERATING CHINESE BEV PRODUCERS

Tata motors trades at 10 P/E, which is substantially lower than the industry average of around 28. Any idea why is the case?

If you normalise the earnings for other income and tax, I think the PE will be close to the industry average. I find the stock fairly valued because it is PV + EV + JLR + CV + Lending. CV is coming off a high base. BMW and Daimler trade at 5-6PE with 6-7% dividend yield which is where JLR will eventually be valued too.

There’s a lot of segments in the business, you can’t value this stock based on industry multiples because majority of their EBITDA is from JLR, there’s no listed luxury car manufacturer in India so the comparison is not apples to apples.

Disc : Tata Motors DVR was 40% of the market value of my family fund. Entered at 200, exited at 680 few months back completely when demerger announcements came in.