Finally, steps towards buy back. Board meeting on 16th. Let us see what they plan as promoter holding is already more than 74%

https://beta.bseindia.com/corporates/anndet_new.aspx?newsid=65f25ec9-aade-4d44-a8a2-c9c24ba1ae35

Disc: 6% of PF

Finally, steps towards buy back. Board meeting on 16th. Let us see what they plan as promoter holding is already more than 74%

https://beta.bseindia.com/corporates/anndet_new.aspx?newsid=65f25ec9-aade-4d44-a8a2-c9c24ba1ae35

Disc: 6% of PF

Received buyback email with tender form from company

Any idea about company specific 6% jump today?

Or it just frenetic search by people for small caps.

Back on Valuepickr after a long hiatus. One of my core stocks, TIC, is now at a 60% discount. Current NAV, post the rally from March, must be closer to 1900. Been communicating with the company on ideas to reduce to discount to NAV - both to Mr. Dalal and Mr. Manoj. They should further consolidate their portfolio into their winners and quality names + hike dividends by such divestment of small holdings. Not sure what purpose is served by investing 5-10 cr in 20 names in the bottom of their holdings when the overall portfolio size is nearing 10,000 cr. Company has to find ways to correct his humongous discount to NAV.

Largecaps are almost 10% low to 31st March on which date NAV was around 1400 so why do you think NAV should be around 1900.

Hello! I have taken the entire portfolio from their latest annual report and updated for current market prices for listed securities and taken the fair value as mentioned in the AR for the unlisted securities/debentures etc. The current NAV would be around Rs 1900 based on current prices of the underlying portfolio.

This post has discussion on Tata Investment Corporation.

The ideal valuation compare for this will be to S&P BSE Top 200 index. The co. itself measures its performance against this index. So, I suggest the rise in NAV can be compared to the change in dat index from March till now.

For relative performance, makes sense to check with the BSE 200, as the company does. Since the earlier question by the member was about how I estimated current NAV to be closer to Rs 1900, all we need is the updated valuation of its current portfolio, which is an easy exercise since we have the latest annual report.

Thank you. I read that article recently, an excellent one indeed. Given TIC’s pedigree, very high quality portfolio and good dividend yield, challenge is to find ways to compel the Board to take the effort to initiate steps to help bridge the enormous discount to NAV. I have shared ideas with the Mr. Dalal and Mr. Manoj. Let’s see if they translate into any action. Till then, happy to continue investing.

Hi,

Quarterly results are out and on an consolidate basis the PAT stands at 18.40 crore compared to 18.58 crore last year.Full results can be found in the below link.

Thanks,

Deb

As expected, the NAV as on end 31/06/2020 has seen strong growth and is at 1821. Given the upmove in July, current NAV should be even higher. The discount to NAV is at over 60% and the management needs to take steps to bridge this gap to a more acceptable level of closer to 20%. How can they do this? I’ve written into them with the following suggestions:

Liquidate low value holdings (bottom 20-30% of holdings) where they hold shares with 5-10 cr each and pay this out as dividends every year. Even 50-60 cr of such liquidation and paying out as dividends will immediately result in a jump in dividend yield closer to 4-5% plus and bring in new investors into the company.

Liquidate low value holdings and go in for another buyback at a price closer to NAV. This will signal to the market that the management believes that the stock price is significantly undervalued and such a big discount is not justified.

Liquidate all low value holdings and consolidate into their larger holdings that have strong growth prospects.

Liquidate all low value holdings and move into higher yielding stocks or bonds - high quality high dividend yield companies or increase allocation to fixed income instruments. This is important to increase yield on the portfolio to ensure that future dividends payments are sustained.

Increasing liquidity in the stock. No institution is going to touch the shares because of the low float and risk of an inability to exit when they want despite the very strong fundamentals. Maybe a combination of bonus shares and stock splits will help. (I’ve heard that one large investor is liquidating a part of their holding and hence the pressure on the stock price despite the strength in the market)

We must keep engaging with Mr. Dalal and Mr. Manoj so that the Board is forced to take value accretive measures. Their hands off approach isn’t helping long term shareholders.

Hi,

Cannot agree more.I am unable to find any rationale behind keeping such low holdings which are good for nothing.There are so many good investing opportunities which other mutual fund houses are tapping into.Management should act according to the suggestions provided by you.

Thanks,

Deb

You need to invert. If you are the owner, why would you care if the market is pricing the co at the right price or not? Maybe all you care is the dividends that come.

All the options you suggest require efforts. And no management wants to take efforts if there is no clear upside for them. (Note that any effort = cost)

To their credit, they did the buyback which is extremely friendly towards minority share holders. But if I were them, I would let things be as is. This applies to all hold cos btw.

What’s the point of running a parallel portfolio of diverse equity holdings when there’s Tata Mutual Fund? Best to keep selling as the markets move up and buy back shares at 30% discount to NAV (versus 60% prevailing now). Doing this perpetually will take NAV to much higher levels. Their best investment will be in the company’s own shares to drive shareholder value…

I don’t think they can do another round of buy-back. Not much room is left. The promoter shareholder is very close to 75% already. So that option is out of question.

In Tender route, promoter also have right to participate in buyback, subject to stipulating expected quantities and entities which intend to participate in buyback in advance. Hence, there is possibility of buyback even if promoter holding is 75%, subject to promoter participating in buyback in my opinion.

There is one rare scenario when this could create higher than 75% shareholding for promoter despite participating, when mandatory reserve of 15% of value reserved for Small shareholders, disproportionately reduce their holding, resulting in higher promoter holding post buyback. However, it need more mathematical calculation to figure out and very difficult to develop that model in theoretical world with assumption.

This issue can also be addressed by promoter adjusting stake surrendering lower than pro-rata eligibility. So instead of 5% of 75% of equity surrendering in buyback by promoter, they have surrender 4.5-4.75% of 75% of equity which they hold. By this way, although they get lower than pro-rata eligibility, still can get buyback through tender route approved.

In case of open market buyback, any way, promoter can not participate. Hence, same can not be undertaken, once shareholding reached 75% for promoter. Reduction in public shares, would automatically increase promoter stake above 75% in open buyback.

Agree with all the points. But they’re all quite theoretical options. Practically it is unlikely Tata Sons will tender at buy-back prices unless buy-back price is close to fair value in which case it doesn’t make sense for TICL to do a buy-back in the first place. Selling down stake to comply with 75% is the least of the issues the Group may want to deal with right now especially if it is TICL. I’d think they would have pumped in more money if they had headroom.

The only possibility of a re-rating I can think of here is perhaps through increase in dividend. But that again won’t be a sustainable solution. It will be one time as it is unlikely they’ll keep selling core holdings to pay dividend. Or if they find a way of distribution of assets to shareholders. Otherwise this is only a dividend play, IMHO.

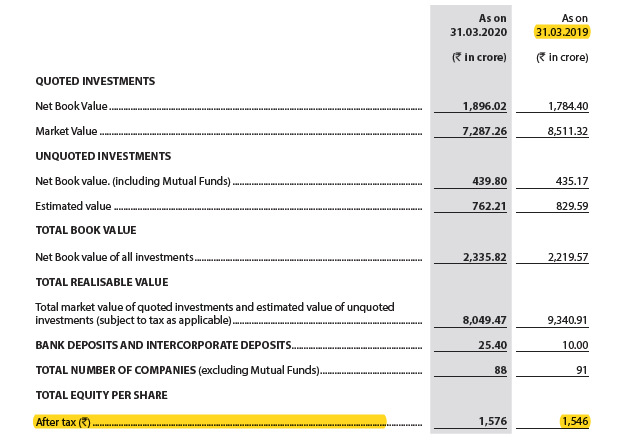

Most of buyback in Tender rate generally higher than 15-20% of announce date trading price. Even when last Tata Investment did buyback in Feb 2019 or so, the buyback price was Rs 1000 per share. In March 2019, Total equity value per share was Rs 1546 as per Annual report.

So the Tata Management did participate in buyback at Rs 1000 in Feb 2019 when expected Fair Value of the company share was around Rs 1546. Hence, as a management they would be keen to maintain their pro-rata share in company rather then fair value of business. In case of Tender buyback, by purchasing equity worth Rs 1500 per share at Rs 1000 per share, every shareholder gained pro-rata to the extent of holding. Hence, in my limited understanding, going by past experience, Tata Management would be willing to participate in tender buyback till they can manage their holding at 75%.

Market price of share during that period was around Rs 900 as against buyback price of Rs 1000 and fair value of Rs 1500.

Interesting! Let’s keep fingers crossed then.