Tata Investment Corporation (TIC) - NBFC type of business - buys and sells equity, with a self declared long term focus: also holding company kind of structure and holds shares of Tata Group companies.

the strategic holdings are unlikely ever to be realised completely due to the holding structure

holds an array of companies and receives dividends from them and also makes money when they sell those shares

regularly declares their Net Asses Value (NAV) based on the value of their holding- (details on their website)

-Similarity to a mutual fund, is noted.

Rationale for investment

The share price always has a discount to NAV

long term share price discount to NAV is around 40% over last many years.

during the financial crisis the discount to NAV went up to around 58-60%

current NAV (Dec15) is 1295

at the share price of 500, this is a discount of 60-61%

the possibility of the discount to NAV returning to usual baseline or reducing from current levels - is reasonably high

Downside is likely limited, but the upside is more than the risk of significant decline.

-are things as bad as financial crisis now- doesnt look like it

is the current NAV likely to be higher than 1295 - likely, the way the market has gone up (guess on my part)

Cons

Can the discount continue to widen further, to lets say 70% of NAV , of course it can/ may- but there has been no precedence in recent years as far as I can find.

When will the discount to NAV return to mean- I dont know, may take a while; Can get 3.5% dividend, while you wait ;

-What could trigger the discount to NAV return to mean- I dont know (usual claims of delisting etc, are not clear or predictable): the low share price or huge discount might itself be a trigger

Is it for a very long term investment - I doubt it with complicated structure, issuing of warrants etc and equity dilution, fairly static dividend payout for last few years, not a stellar growth story or anything; I doubt its the kind of stock that you keep to send your kid to university. Have done their share of buying suzlon, satyam etc in the past and selling huge pile of Eicher motors shares in ?2009 (If only !!)

The NAV can come crashing if the market crashes; but looking at the last many years, its not usually a dramatic drop in NAV, but a slower one than the market drop.

Conflict: invested

Declaration: I am a novice and have no finance background at all- so please go slow if the above is way off the mark and not according to VP standards

From my experience holding companies always have a discount of around 30pc

It makes sense as they hold large amounts of stock and its unreasonable to assume they will get list price secondly they have expenses which eat into the profits so 30pc discount looks thereabout right

Thanks. You are absolutely right about valuation of holding companies- its messy. My way of thinking is purely based probability; its not based on intrinsic value or for long tern holding.

My way of looking at the situation is as below

Why has something that has not happened in the last 12-14 years happening now without any specific triggers ?

Is there a likelihood that the discount to NAV eventually return to its usual base line of around 40 odd percent from the current 61%; from whats happened over the last more than a decade, over bull and bear phases,I think there is a strong probability that it is likely to happen (I might be wrong, as most probability based interpretations can be)

-Is there a chance that I will lose my capital permanently- very unlikely (the time frame for the discount to narrow is an unknown, so opportunity costs may be an issue)

-Over the last many many years, the share price has neatly tracked the NAV within a band of discount - I tend to believe that what has happened before will continue to happen, as there are no new determinants to change the probability.

Thanks for your comments

I think it would be a good idea to check what dividend you would get if you were directly invested in the underlying stocks and what dividend the holding company is giving out

my guess is that it is 60pc less, if not it’s a great buy

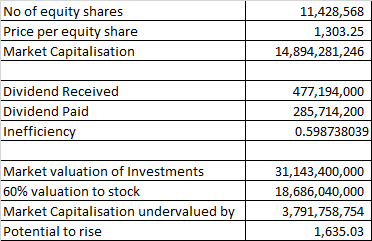

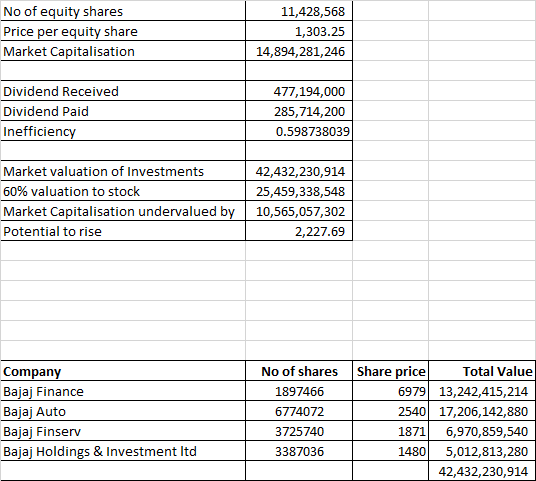

Mate, I did a back of an envelope calculation on Maharashtra Scooters

There is a potential for stock to rise to 1600

Disclosure: I dont own maharashtra scooters. I feel there are better stocks besides buying a holding company means I’ll have to research all the other stocks that the holding company holds. Its a lot of demand on time

@Sunnytv - Holding company discounts are sometimes as steep as 80%. Please do comparative valuations of holding companies. BBTC, VLS Finance, etc. The movement here usually track the movement of underlying companies.

Another interesting holding company discount story is Balmer lawrie Investments (BLI). Unlike TIC, Maharashtra Scooters, VLS, IDFC etc, BLI is a pure holding company with just a single asset - a 61.8% stake in Balmer lawrie. This one also trades at an average 40% discount to NAV and high dividend yield of over 4%. Will be interesting to see the results and dividend declared on May 18, 2016. Unfortunately highly illiquid, so an aam aadmi investment story, not for HNIs - though Barings India Private Equity owns 5%. And with a PSU at least there are no questions on quality of accounts.

Disclosure: I hold the stock - hoping that value will be eventually unlocked though PSU disinvestment

I have been trying to read up on holding companies and could not find much info; if anyone has any links or articles, it would be great if you could share it.

There is a great talk by Amit Wadhwaney on you tube on holding companies - its a great listen.

Essentially what I understood , is

you need to want to buy the parent company

The parent company should have all the investment qualities

There is no meaning in buying a holding company if the parent company is overvalued

The discount itself will not reduce your downside risk, if the parent company is overpriced

you need the combination of both undervalued/ fairly valued parent company and a higher than usual discount; this is often hard to come by

More comments would be welcome from experienced investors in holding companies.

It would be great to create a resource source for assessing holding companies.

Another interesting holdco discount story if PTC India where after accounting fro the value of stake of listed subsidiary and for cash, the EV of the core business is almost available for free

This stock is unlike others like Mah scooters etc is not into investing into promoter companies with high concentration risk .

It is like a balanced Mutual fund diversified into stocks and debt . The way to look at such fund is how NAV is increasing YOY . Assuming discount is at historic low you have two catalysts

Growth in NAV ( this is better than Nifty in long run)

Reduction in Discount

Additionally expense ratio of this fund is very low as compared to any mutual fund .

For Listed Investment companies like any mutual fund : NAV is only reliable valuation Metric .

You need to Look at NAV changes YOY vs Nifty Changes YOY

Say in this case if NAV march 2015 was 1270 and dropped to 1215 it has reduced by 4.6% and in same period Nifty has dropped from 8565 to 7738 ie reduced by 9.7% .

So Tata Investment has beaten nifty by 5+% . You can do the same for 3 years or 5 years and see if NAV is growing fast enough . If that happens it is good long term investment

On NAV - CMP Discount it is actually MOS ( margin of safety ) for sudden drop in general market levels

This is becoming a classic Mutual Fund at huge discount.

Current M Cap is < 2800 cr

.

Look its investments:

Non Tata Equity Holding: 2170 cr

Bond/Debenture/MF/Cash: 600 cr

NSE holding: 80 Cr @ 6000 Rs/share (expected listing price is 6000-8000 based on current valuation)

Total: 2850 cr

Nice balanced mutual fund at 2% discount.

Icing on the cake (This is much bigger than the cake itself)

3350 cr of Tata Blue Chip stocks like Titan/Tata Motors/Tata Chem/TCS/Tata Steel/Tata Global etc

500 cr of Tata non-listed

Discl: Hold 5% of my PF and adding more with declines.