Among the FMCG companies it is trading at lower PE. The only point keeps bothering me is their operating profit margin. For any other FMCG company, OPM is approximately 25%. One good thing about this company is they keep increasing their revenues and increasing their portfolio of products. One can acquire it in corrections and suitable for long term

5 Likes

Management on Q3 result

1 Like

Interesting to note that Kottaram Agro Foods, the company which owns the ‘Soulfull’ brand is founded by Dr. KK Narayanan who was earlier the MD of Metahelix, which is Tata group company under Rallis. So TCPL should have a good idea of the quality of management and the technical capabilities of Soulfull.

Here is the link to Dr. KK Narayanan’s linkedin profile: https://www.linkedin.com/in/narayanan-kottaram-8852526/?originalSubdomain=in

10 Likes

Ya. But TCPmajor revenue from Tea and salt . Both are commodity type material. I check with other tea coffee player same as OPM(screener) . Once the other business vertical revenue shares increase OPM could improve…

Invested…

1 Like

Tata Group to buy 68% stake in Big Basket

2 Likes

Tata Consumer is not buying Big basket. Tata group is buying it. Most probably they will buy it via unlisted Tata Digital.

3 Likes

Though Tata group is buying the stake in Big Basket, finally it is Tata consumer products which could get immensly benefitted since all its Groceries would be promoted through Big basket.

Currently , following Tata digital platforms are available for selling Tata consumer products for door delivery of groceries.

Apart from above, Swiggy is also tied up to door deliver Tata consumer products.

www.tatacliq.com

(For other Tata products)

Tata consumer products are also available in all brick and mortar super markets…

Now big basket has its own Apps which is vey popular- I have been big basket customer for the last 5 years - and I like it the most since it gives same day door delivery of all the Groceries & fresh good quality veggies- and many exotic vegetables and fruits which are not easily available anywhere else on line or brick and mortar stores and they always run schemes with credit card where you get up to 10% cashback…and with big basket deliveries I don’t need to plan in advance…even if I order by 1 PM , I get it by 7 PM…the delivery boys have bikes…and deliver orders…

In any case we need to see how various Tata consumer e- commerce divisions get consolidated with the help of the new proposed Tata Master Apps and whatever may be the consolidation process it is Tata consumer which makes all groceries would get immensely benefitted out of the consolidation process.

3 Likes

I think buying of big basket will open a new domain for TATA group

Why only products of Tata consumer may be products of other companies will also be promoted

Company has successfully completed the acquisition of 100% of the equity share capital of the Kottaram Agro Foods Private Limited

1 Like

7 Likes

Tata Consumer looks like a good long term investment candidate - especially in terms of growth runway and product innovation.

Would you have any thoughts on:-

-

Surprisingly lower margins in Q4 21 - expected to get better?

-

Should we expect next year growth to be impacted by a high COVID base?

-

Current valuations being quite high even versus a Marico and Dabur - anything I might be missing or is this just because of future growth potential?

I know these questions probably sound a bit negative, but to be honest they are just smaller doubts in a larger thesis with an overall positive interpretation for the company.

Discl : Invested

2 Likes

My thoughts on these points would be

- Margins were lower mostly because of inflation of commodity prices specially Tea…now commodity is cyclical and all good FMCG firms gain market share from not so good firms or unorganised sector during inflationary times, so I would assume this pressure to keep fluctuating and not something permanent. However, the huge dependency on Tea prices is very much evident…and as a long term investor for me that is the area and scope of improvement which Mr D’Souza and his team would help bring in for his company and me. He has already started working on this by investing in high margin brands like Soulful. Such conscious efforts to improve margin profile of the firm is encouraging.

- We do not know if next year would also be a covid year or not yet, although I pray Covid ends soon. Having said above, market is well aware of a high base for not only TCP but all FMCG firms with a predominant foods portfolio. Some of these, including TCP have some elements of out of home consumption as well which would kick in if next year is not a covid year. New product launches relevant to type of year would kick in. Many people simply forget Starbucks giant in making…which will also kick in…the final end result QoQ or YoY I cannot comment but I am well aware that this company has all the elements that I need.

- Market values topline growth the most along with high margin product range or a movement towards such range…ever since Tatas became serious about FMCG, it trusts the intention and execution capabilities of new revamped management. I think we might see market respecting Marico also significantly more once it’s revamped Foods portfolio performs consistently. I would say that in few years, we would be comparing valuations of TCP with HUL, Nestle and P&G instead if TCP executes well.

Disc: Invested so highly biased. Can be completely wrong in my assessment. Not a buy/sell recommendation

8 Likes

Thanks for the inputs - I would agree on all points.

I quite like the LGQP investment framework - and I believe on longetivity, growth and quality TCPL checks all the points. Right price - I am

still not sure.

I also believe it could be amongst the strongest plays in the unorganised to organised shift - considering that almost all FMCG products they play in fall in this bracket - versus say a personal care player.

I actually think the likes of Marico and TCPL should be valued higher than Nestle and HUL, these companies are fantastically managed as well and there is the potential for international expansion and product premiumization - something which the behemoths have already substantially unlocked value in. I see a PE range narrowing happening here - whether the big ones go down or the emerging ones go up is anyone’s guess - but I think FMCG is overall in for a short term tough time considering high base and input prices in the next few months.

The current PE multiple and temporary headwinds prevent me from adding at current valuations though (I expect tea prices to be firm considering Assam lockdown at a similar time as last year and hence margins to be temporarily affected for the following year) and I personally prefer to buy companies on earnings as the core parameter versus say sales.

That said, looks like a great long term investment - but should give scope to add in a phased manner at hopefully lower prices in the near future (maybe I am being greedy) as we move ahead.

Discl : Invested

7 Likes

2 Likes

https://archives.nseindia.com/corporate/OutcomeoftheBoardMeetingheldonAugust32021_03082021180648.pdf

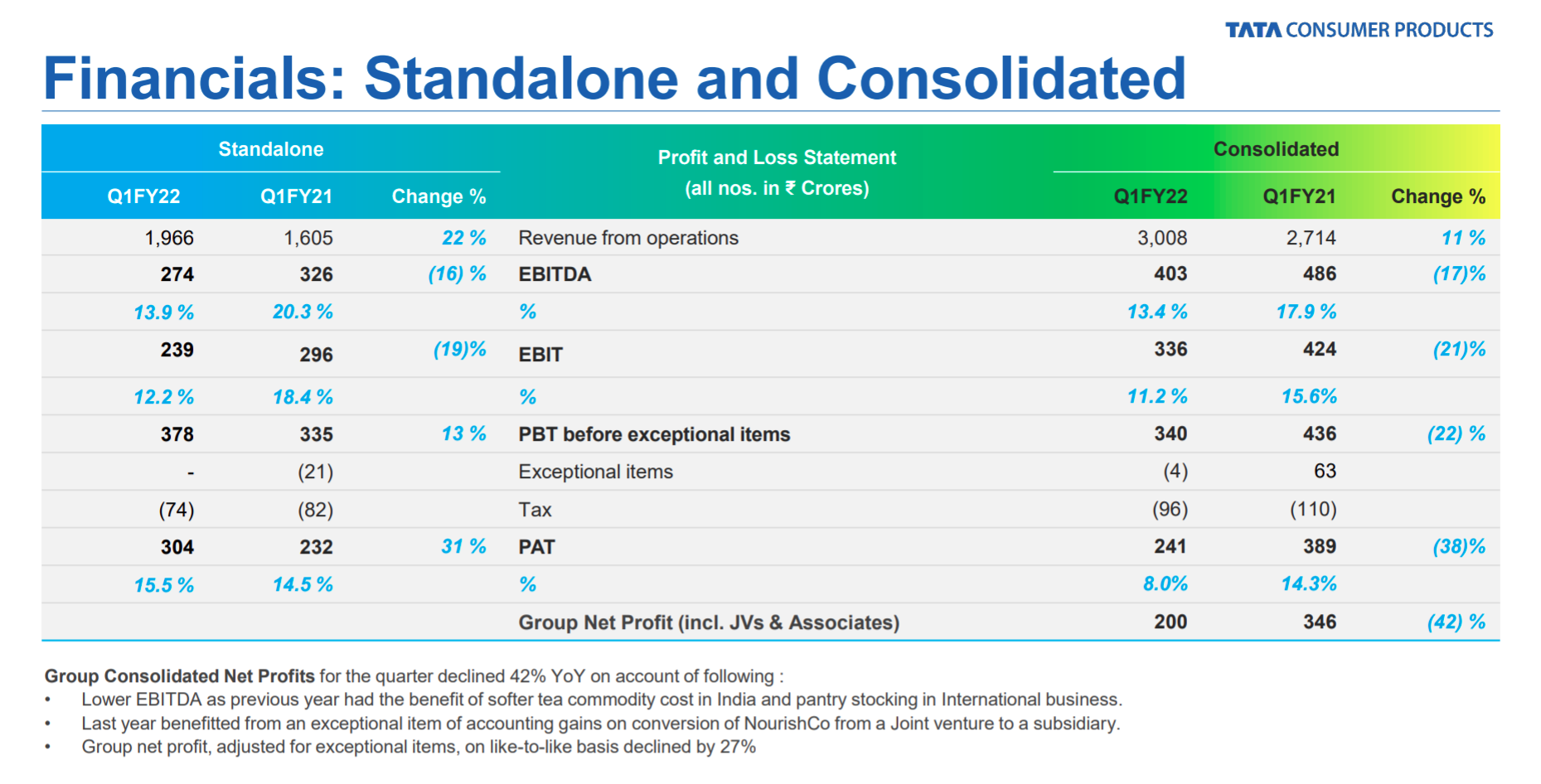

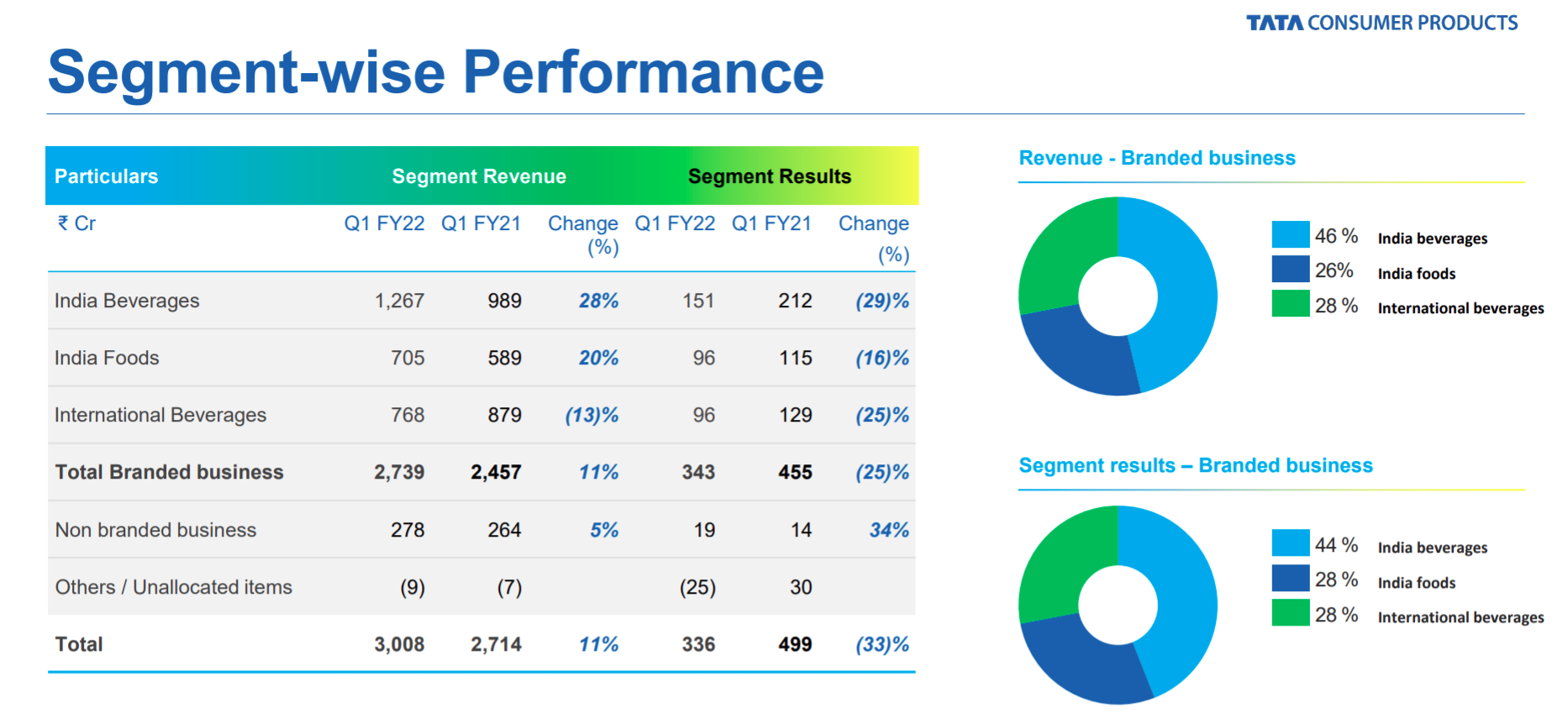

Excellent updates on all segments of the busniess in the deck.

Key slides below.

3 Likes

Interesting read…slowly and steadily Tatas are expanding their Tata Cha venture with 14th outlet in Bangalore! seems they are following a cluster based approach from city perspective rather than going pan India in one go…I guess, Tata consumer will be the only FMCG company in India with built in QSR in terms of 50% Starbucks and 100% Tata Cha ownership…would be interesting to see how these pan out and what future restructuring, if any, Tatas do…

Anyone from bangalore having first hand experience of Tata Cha would be useful insight…

Disc: Invested & biased. Not a buy/sell recommendation

11 Likes

Hello everyone,

Can someone please answer why TCP’s ROE is less over the years compared to other FMCG stocks? Is it (less ROE) not a negative factor?

ROE is low due to goodwill paid for acquiring foreign companies in the past. Below is excerpt from credit rating report explaining the same.

Overall return on capital employed remains under pressure despite improvement over the past few years

The performance of TCPL’s overseas entities has been impacted by declining demand trend in the black tea segment amidst the impact of Brexit and high competitive intensity in the developed market over the last few years. Subdued performance of the overseas businesses in the past had impacted the consolidated RoCE to an extent. However, the company has increased its focus on pursuing opportunities through new innovative products and strengthening of brands which are witnessing traction as evident from its improved financial performance. The improvement in the recent past has also been aided by revised strategy of business restructuring and consolidation, including exit from some of the marginal geographies, such as Czech Republic and the MAP business in Australia. However, notwithstanding the sequential improvement in the performance of its overseas operations, the overall RoCE of the consolidated entity remains under pressure. Going forward too, while ICRA expects the performance of the different businesses to remain healthy, the improvement in overall RoCE is likely to limited by the high consideration, funded by an all equity deal, for the acquisition of the food business which has led to substantial goodwill.

5 Likes