Not participating in Battery PLI does not mean they don’t have an alternate plan.

Things in EV/Renewables are developing very fast. They have lined up for Li ion Battery Manufacturing. In the meantime , with Reliance planning to manufacture sodium ion battery 100% indigenous, then the case for Li ion battery becomes little weak due to cost and supply chain issues involved and even if Li ion battery is manufactured in India, we have to import key raw material Li, Cobalt, Ni from China / other countries.

So with regards to EV battery , they would do whatever is the best for the company and best for the country.

But let us look at the Role of Tata chemicals in the entire Eco-structure of Renewable /EV.

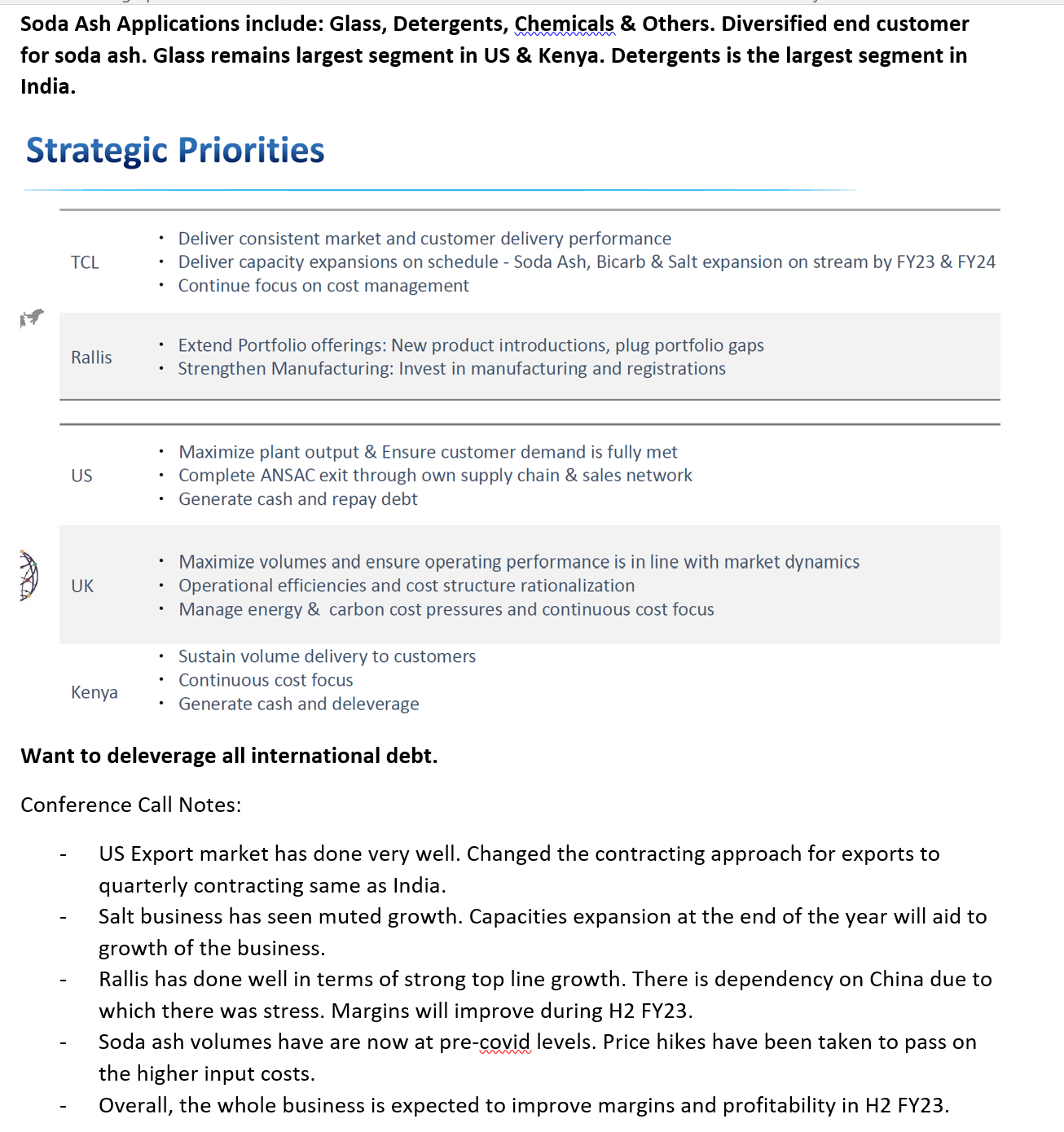

Tata chemical is among the top 5 Soda ash manufacturers of the world.

(1) Soda ash is being used to produce lithium Ion battery - 1 tonne Soda ash is required for producing 1 Tonne lithium carbonate.

(2) Soda Ash is required to produce Sodium Ion battery.

(3) They have already set-up a Lithium ion battery recycling plant, which perhaps would be the largest in the world. when lithium ion battery uses all scarce material, it makes sense to recycle them.

(4) Soda ash is required to produce Solar Flat Glass - Solar energy

(5) Needless to mention the other traditional uses of Soda ash and other products of Tata chemicals. The overall business in these segments which would depend upon overall

Growth of economy.

(6) As you can see all these developments are getting reflected in Q2 and now Q3 results of 2022.

The 4 -Tata companies (Tata Motors, Tata Power, Tata Elexi , Tata chemicals) are definitely going to play an active role in creating an Eco-structure for EV, Renewables -Solar/Wind & Green Hydrogen.

Discl: it is not an investment advice…I have Invested and I may be biased . Please do your own assessment before investing.

There could be many reasons why they rejected the proposal as they might not be needing the funding if we look at the list other than reliance other may need to allocate new funds to do so while in tata chemical case they already have plans for self-funding.

One more reason could be the amount of battery they need to supply or make other manufacturers like other automobile players take this battery at the same cost as tata motors that might be a big reason why they will be wanting this for the time being to only supply to tata motors that government will never entertain and when you have cash then why take PIL and also the obligation might also not be in there favor.

As for how synergy is been building in tata group they just might be wanting tata chemical to stay away from many other matters of supply and trade restriction as others might not be wanting these majors that early.

As a person who has invested long time ago this is worry point to look over but not to sell .

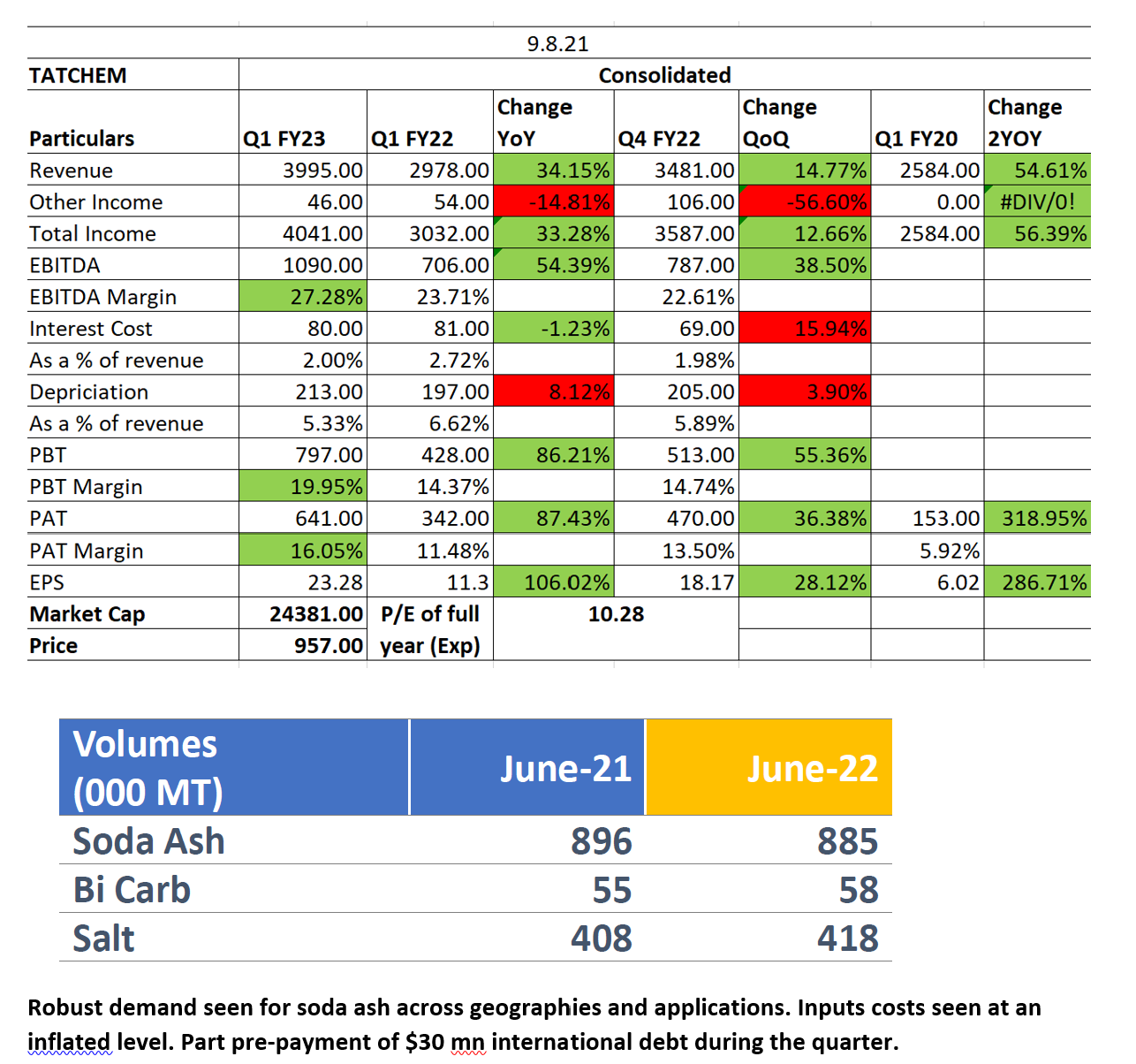

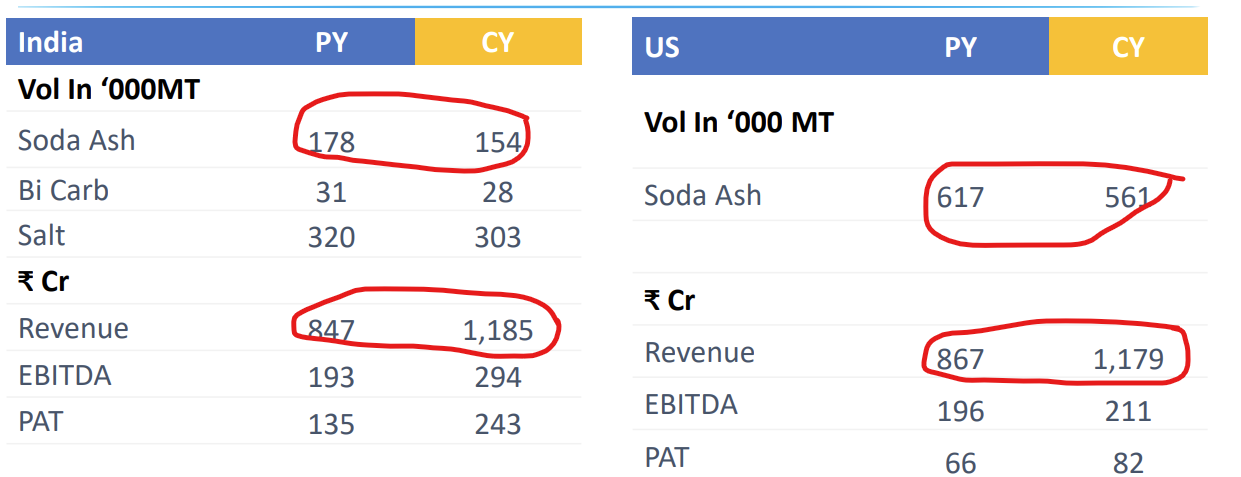

A good set of top line and bottom line nbers from Tata Chemicals both QoQ and YoY.

QoQ net profit up by 41% (Q4 22 over Q3 22)

QoQ revenue up by 12.7%

YoY net profit up by 32.8% (Q4 22 over Q4 21)

YoY revenue up by 3622 %

Net profit up by 390% (Fy 2022 over FY 2021)

Revenue up by 23%

Battery manufacturing in Tata chemical likely and this will change the dynamics of Tata chemicals

There was a question asked on this in the earning concall; it was answered that while chemistry might be with Tata Chem, manufacturing plans are not firm and Tata Chem team is not aware of any such plans either. I feel they are keeping it under the wraps atm. I recon it was mentioned previously that PLI was not applied due to the business wasnt sure if company can meet the strict timeline milestones for PLI.

Is this True? is it still a good idea to hold on to tata Chemicals?

but,

The simple answer is yes but with a string attach that you might need to lower your valuation and future projection as now they will play a lower margin heavy growth business than a high margin and high growth business.

But still, the raw material and recycling might be a good value that makes them easier to take a big market share and this will also help them to partner with other auto companies more easily now as the tech is now less linked.

Personally, I will lower my allocation in this as I was assuming higher growth than this but it still looks attractive in my opinion so no full exit will be there.

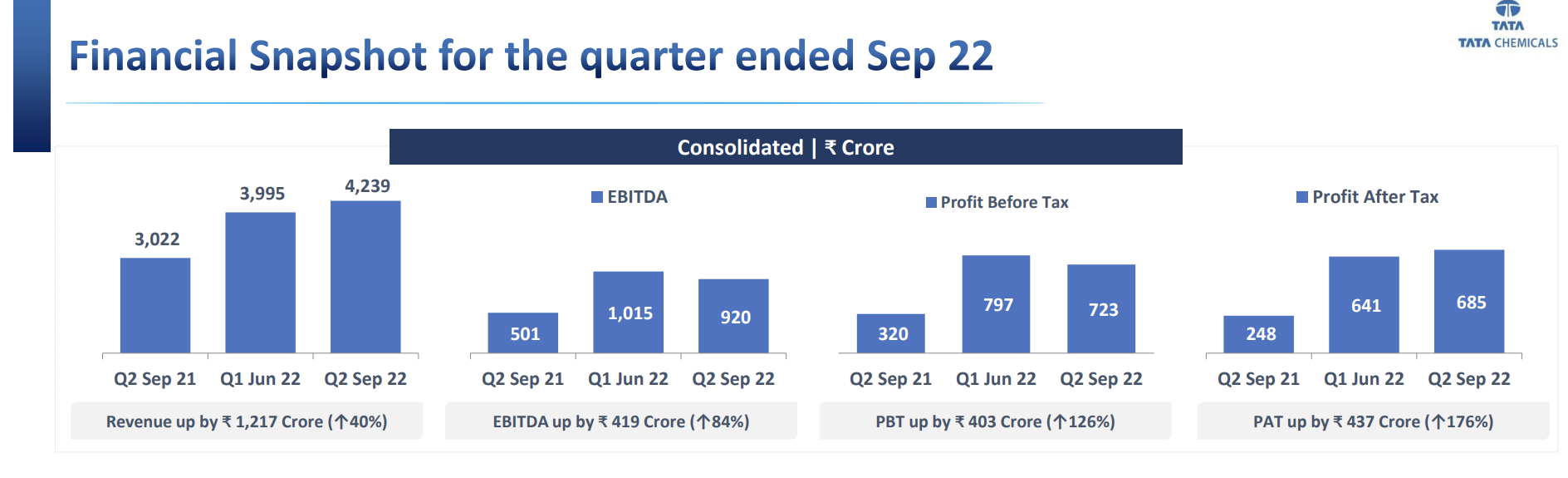

Excellent set of results from Tata chemicals- Both QoQ &YoY.

Some more details on Q1 2023 results and narratives from the company !

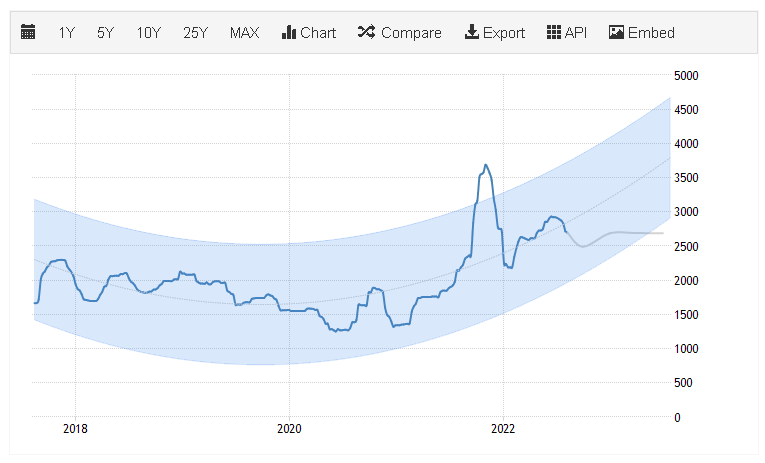

The spot market for soda ash exists mostly in China and Europe. Soda Ash is expected to trade at 2489.12 Yuan/MT by the end of this quarter, according to Trading Economics global macro models and analysts expectations. Looking forward, they estimate it to trade at 2686.01 in 12 months time.

This is because apart from the traditional uses of Soda Ash, the additional demand of Soda Ash is expected to come from ,

(1) Renewable energy - Soda ash is required to produce Solar Flat Glass - Solar energy which is here to stay…it is also a part of Green Hydrogen project and global demand for Green hydrogen could drive soda ash prices

(2) EV application -Soda ash is being used to produce lithium Ion battery - 1 tonne Soda ash is required for producing 1 Tonne lithium carbonate,

(3) EV - Soda Ash will also be required to produce Sodium Ion battery, which Reliance seems to be planning in a big way.

All Soda Ash manufacturers are likely to benefit from this demand though Tata chemical has highest capacity and it has the first mover advantage !

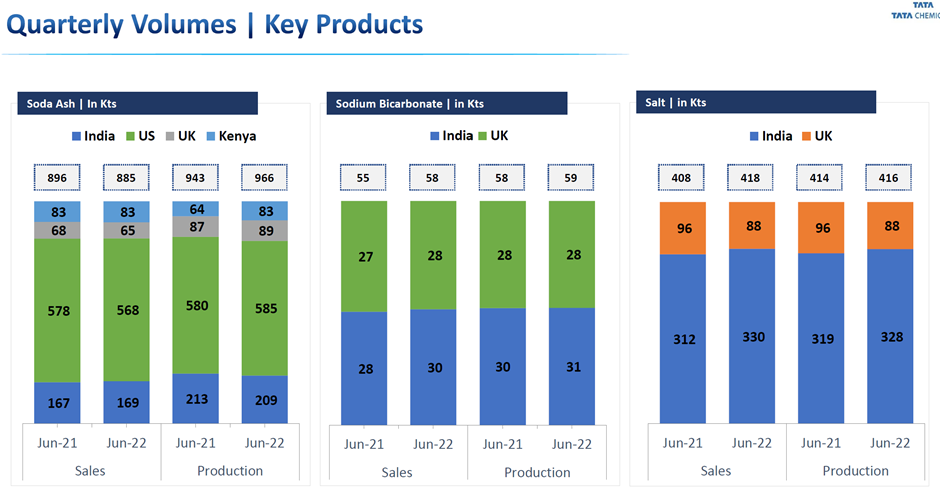

Tata chemicals is the 3rd largest soda ash manufacturer and 6th largest manufacturer of sodium bicarbonate in the world apart from the most popular “Tata Namak”.