Agreed. I missed out on the cement part of the business. I initially did not comment as i thought they weren’t generating enough revenue to move the topline needle of the company and considered it as a minor business of the company.

TCL manufactured 362 Kt in 2019-20 and 440 Kt in 2018-19. Since i could not find any individual figures for cement revenue in their AR, i looked up at Indiamart to see similar prices of its peers such as JK, Ambuja, etc. It usually fluctuates around Rs 300 per bag of 50 Kg. Sometimes it goes to the Rs 380 - 400 per bag too but i am taking here Rs 300 for calculations.

So in 2018-19, they manufactured 440 Kt of cement. Assuming Rs 300 per bag of 50 Kg, they generate around Rs 264 crore of revenues (mind you that i took a lot of assumptions and this year production was down more than 20%) . The division roughly translates around less than 3% of revenue of the company. Also in AR, it is written that they have capacity around 500 Kt.

From their latest AR-

" To serve this growing demand, we have planned to further augment our

production capacity by 0.3 MMT by FY 2021-22"

So, it seems that this division can clock a turnover of more than 500 crores by FY22 if there is high capacity utilization and stable cement prices. It would translate to roughly 5% of their revenue in FY20 terms. I could not find their OPM or net profit figures for this division. Neither do they mention much about it in their Investor presentations or last few concalls (would be great if someone could gather some information about it) . I believe that this division is not the core focus of the company. And neither have i seen any Tata cement bag commercially or in advertisements. I wouldn’t expect it to be a major focus or high revenue generator for the company.

The only problem with TCL is that their high potential businesses (Nutraceuticals, Materials Sciences and Energy) barring the agrochemicals business contribute very little to the topline and it may take nearly a decade for these segments to contribute meaningfully to the bottomline.

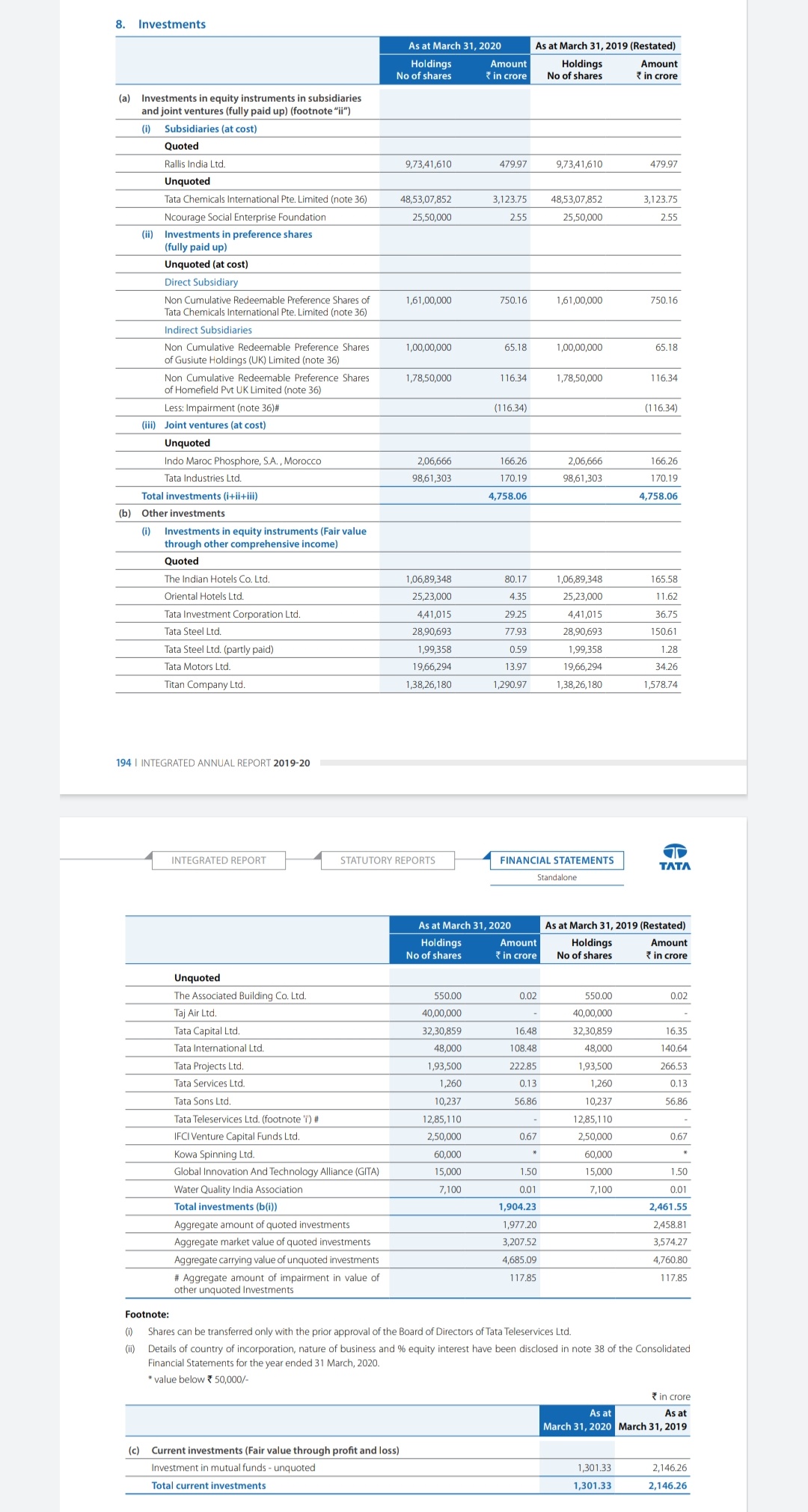

according to the latest annual report of Tata Chemicals the lastest value of its stake in various listed and unlisted companies is provided, kindly go through the annual report

According to Wikipedia Tata sons that is valued at about $120-$130 billion and Tata chemical holds 2.53% stake in the company, but the annual report values this stake at 56Cr which is no where close to the value that Wikipedia is implying. This kind of difference in an annual report is not possible and also institutional investors would have taken a note of such an opportunity and the stock would already have run up.

I think confirming this from a source other than wikipedia would clarify things.

I have another question here…Whatever maybe the value of the holdings of Tata Chemicals in Tata Sons…is it ever going to create any value for Tata Chemicals shareholders as Tata Sons is and will remain a Privately held company and its shares will never be sold. Well, there maybe a remote possibility that Tata Sons restructure and buy back their shares from Tata Chemicals and if that happens, I suppose then the valuations in the annual report would hold. Pls correct me if wrong?

Tata group has shown interest in restructuring the group’s cross holdings and has already restructured by selling Tata Global few months back. Also they have been increasing their holdings in Tata Chemicals and other group companies and restructuring their businesses.

Tata Chemicals is trading at 0.57 times its consolidated book value and also has a number of new business initiatives like Nutrachemicals, Sillica, Energy and also they have cement that can lead to re rating if these products start contributing to the top line in a substantial manner. They also have huge cash balance and are debt free, but patience is needed in Tata Chemicals and it might prove to be a multibager.

Wanted to know your thoughts on the Tata sons holdings, that you mentioned, that how it can be of value to minority shareholders…however you mention some other points now. Among other known, I was not sure if Tata chemicals is really debt free? Can you pls confirm source.

SP Group (Cyrus Mistry family) has valued Tata Sons at Rs. 2.4 crore per share.

Tata Chemicals holds 2.53% (10237 shares) stake in Tata Sons which is valued at around ₹24,500 crs.

If the valuation of Tata Sons is correct, this would make TCL extremely undervalued.

Thank you for sharing the report.

The value of the shares of Tata sons held by Tata chemicals is 2.5 times more than market cap of Tata chemicals.

Even if holding company discount comes in it has potential to rerate Tata chemicals and it can double also from these levels.

But the question is how the value unlocking will happen?In the situation of Tata sons acquiring the stakes from SP group,Tata sons will require lots of cash.highly unlikely it is going to buy the shares from Tata chemicals or other group companies.And also most of the times group company do hold shares of the parent company so that promoter stake dilution doesnot happen.In these type of cases I wonder market will give any rerating to group companies holding shares of Tata sons.because they are unlikely to get rid of these shares in future also.

So this whole event can be also a non event kind of thing for group companies…let’s see what happens…this is my view.

This is a valid point. But the same applies for holding companies like Bajaj Holdings. Even Bajaj Holding will never sell shares of any Bajaj companies. They still trade at around 50% discount.

Even in case of HDFC, brokerages do consider the value of all its subsidiaries. Tata chemicals also holds round 1300 crores worth of Titan shares.

Bajaj Holdings companies are market traded and operational and give regular dividends. I am not sure if Tata Sons give any dividends to its shareholders and neither it is directly operational…so there is significant difference in this case. Is there any such similar comparison?

Found it to be an interesting development for Tata Chemicals in the long term.

1. Tata Chemicals planning to enter into lithium ion battery manufacturing. Currently it derives no revenues from this segment. It will be a collaboration between Tata Chemicals, Tata Power and Tata Motors.

2. Tata Chemicals already has land site of 127 acres in Dholera, Gujarat, which can house the manufacturing of actives, cells and batteries upto 10 GWh p.a., as well as recycling operations.

3. Tata Chemicals aspires to capture 25% of domestic lithium ion battery market.

4. They are already working with some of the largest 2-wheeler, 3-wheeler and 4-wheeler automobile companies for their electric vehicle programmes.

5. Stake in Tata Sons (worth 2x current market cap, though perceived as dead investment due to no means to monetise it) is positive.

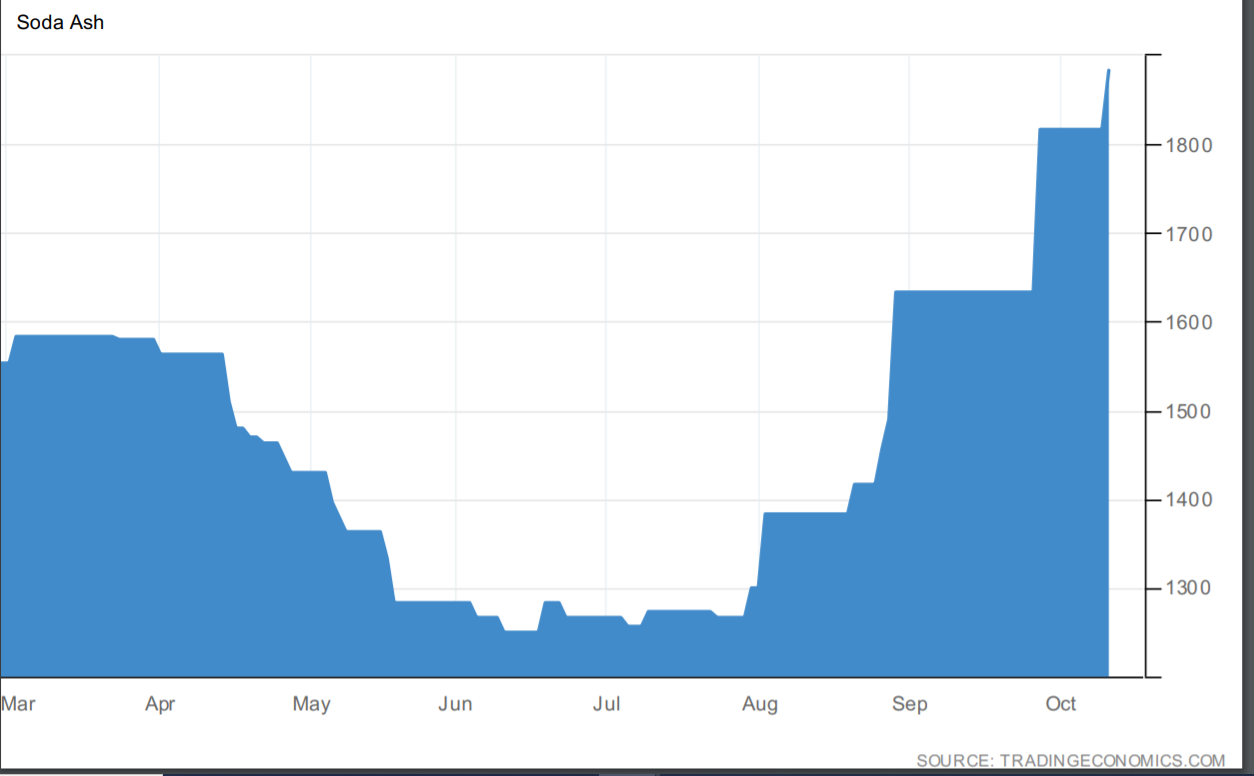

6. Strong recovery in soda ash prices will contribute in the coming quarters.