I think at this stage Tata chemicals is really cheap. I am not sure whether I am missing something that the market knows but it is available at half the book value and single digit P/E. Cash flows are an issue but they have been doing big expansions and operating cash flows have been great.

It seems like a good bet right now. After the COVID 19 impact on markets and the lockdowns, the stock is still depressed. There might be a few reasons investors are not flocking to it. Demerger of its consumer business and commodity nature of the business at hand is a starter as investors tend to stay away from commodities. Lack of free cash flow in past few years might be another problem as well but they have been undertaking massive expansions. Debt is also an issue but they have strong assets with financial support of TATA group.

The major business they deal are commodities i.e. Soda Ash, Bicarbonates and Salt. But despite being commodities , they have been consistently earning well form them for the past 10 years. They are venturing into new businesses and doing aggressive Capex Plans which might yield great cash flows in the future.

- Basic Chemistry Business – It consists of 3 major products. Soda Ash , Bicarbonates and Salt. Revenue rom this division last fiscal was around 8300 Cr( 7600 Cr in FY2018) with EBIT of 1300 Cr (1450 Cr). The revenue is geographically diversified with India contributing around 2000 Cr, Europe with 1400 Cr, America with 3000 Cr with rest going to other parts of Asia and Africa. It also manufactures cement but the revenue from it is miniscule compared to other divisons.

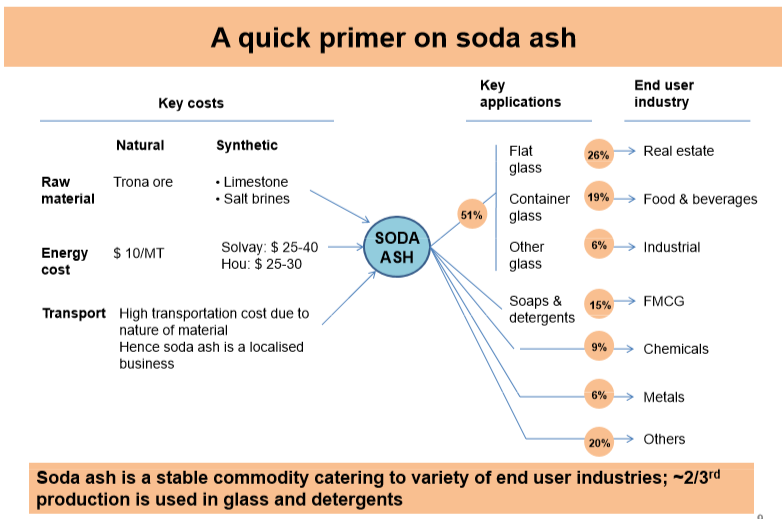

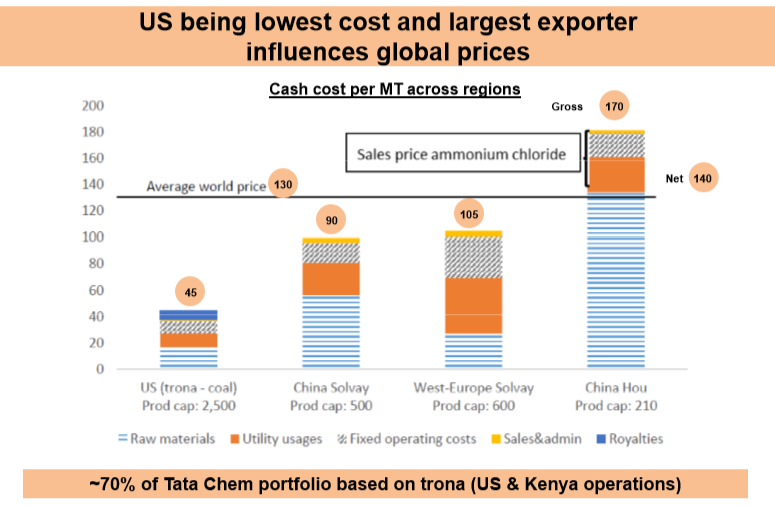

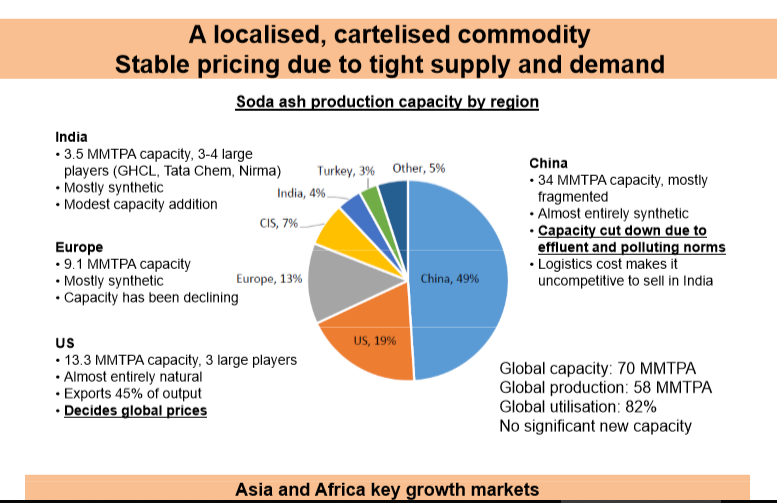

Soda Ash – It’s the third largest manufacturer in the world with plants in India and Kenya. Soda Ash has only 3 players in India. Nirma has market share of 27%, GHCL of 25% and Tata Chemicals has 20%. Rest are all imports. Considering the situation right now, these players can eat into the remaining share of imports and Tata chemicals has also recently expanded its Soda Ash capacity from 0.8 MTPA to 1 MTPA at Mithapur plant which might help them to cater the demand. TCL also imports Soda Ash from its plant at Magadi in Kenya. It has an overall capacity of 4.3 MTPA. Apparently, it works out for them despite the transportation as they have stated in the concalls. Also, Soda Ash is used in flat glass, container glass, detergent, metals, paper, etc. Glass and detergent use around 42% whereas glass demand in auto sector is about 15%. So, soda ash has many uses in lower value added segments in diverse industries. Also, management in one of their concalls stated that soda ash is one of the main materials for Lithium Carbonate which are used in Li ion battery for EV market. This may increase the demand for Soda Ash. So, some of the end user industries are cyclical whereas some are not. Global capacity is around 70.6 MT and the whole industry is in oversupply right now which limits pricing power as of the moment. There is no major capacity expansion happening right now and TCL is one of the few to do it.

So overall, Soda Ash is oversupplied worldwide. It is a commodity but scale is a big barrier to entry such that only three players in India are there. They earned 6000Cr in FY2019 form soda ash.

Salt- It is the largest salt manufacturer in India and was previously integrated as a consumer product. Now, with the demerger it manufactures salt and the branded business has since then gone to Tata consumer products. At mithapur, the capacity is undergoing an expansion from 1 MTPA to 1.4 MTPA. It will a big bulk of its manufactured salt to Tata Consumer branded salt business which commands more than 40% of branded salt market share in India. So, the business will be more or less stable considering a lot of the business deals in trade wit group entities. They earned 1600 Cr from Salt business last year but the breakup might be different this year considering the demerger. Overall, It is a much more stable business.

Bicarbonates-

They earned around 500 Cr in revenues from this division. They produce Medikarb and other pharmaceutical based Bicarbonates and are also currently expanding capacity.

-

They are the parent and own 51% in agrochemical-based company Rallis India. They are investing around 900 Cr in Rallis for expansion of its capacities and product portfolio. Rallis has a leading position in many agrochemical intermediates, pesticides and fertilizers. The agrochemical space in India has been growing. The recent ban on 27 pesticides does not impact much of Rallis revenue (estimates range about 1% or 2%). The business is not cyclical with limited pricing power and immense potential for growth.

-

Speciality Chemicals and Nutraceuticals Business- The management has many times stated that they want to venture into more speciality products which are higher margins and not commoditized. Currently nutraceuticals contribute to low percentage of revenue and that is unlikely to change but it can be a business of higher margins and can considerably improve the bottom-line and return ratios of the company. A 250 Crore plant at Nellore for Nutraceuticals has been almost done and over as stated in concall. Also for their speciality business, they have a pilot plant for manufacture in Sriperumbudur and a silica plant in cuddalore which is producing food grade and rubber grade material. Revenue estimates are unknown but it can be an area to watch out for.

-

Energy Business is a new venture for the company. For the Lithium plant, they have purchased the land and will be investing around 800 Cr for the manufacture of Li ion batteries. This can have a huge potential. Initially, there will a 2 GW plant and trial run will take place. As the demand picks up, more capacity will be added. A lot of area will be left vacant on the land purchased in case there are any future expansions. This is an optionality kind of business that can generate great returns for the company in the future. They have the financial backing and management to make it work. Its difficult to know the kind of revenue they can generate from this division as the market has not matured enough but it can be a major gamechanger.

Overall, the business generates most of its profit from basic chemistry division. Soda Ash being the major cash cow is somewhat with limited pricing power and fluctuating margins but over many years it has produced decent profits. It’s end user industries are varied and many of them are not cyclical. And over a long period of time cyclicality should not be a problem. Also, scale of operations does give it some advantage. Salt is somewhat more stable business and is not much impacted by cycles. Same with Bicarbonates.

There is good optionality regarding the company’s foray into speciality chemicals, nutraceuticals and Energy business. All of them have great major but energy business can be a major cash churner of the lot. But, It will likely take some years to materialize and make a major impact on the income statement even if things go out well. So, they can be seen as a growing revenue stream. Also, the company holds the majority holding in Rallis. So, TCL earns about 800 Cr in a bad year and 2000 Cr in a good year. It had only one bad year of performance in the last decade i.e. 2014 where it lost around 1000 Cr and has made free cash flows of around 7000 Cr in last 5 years despite a major capex in excess of 3600 Cr. The cyclicity is a concern but I believe that the risk is overly priced in. Also, the stock may not be seen attractively by investors since the demerger as consumer products are generally loved by investing community and did not see them favourably for the company. But, TCL earned a small portion of its profit or revenue from its consumer division.

So, It is a trusted and experienced management with financial backing of a strong group. It is available really cheap in terms of cash flow generated per year. Capex of in excess of around 3600 Cr is being carried out with 2500 Cr at Mithapur for debottleneck and expansion and 500 Cr at Nellore and Cuddalore and 800 Cr at Dholera. A lot of that Capex has already been done and its affect will likely show up in the income statement a few years from now. It is highly diversified as of now and in future, it will be more diversified than it is today with Energy and Speciality chemicals coming online. With its basic chemistry business alone it is cheap and with new businesses it may be a really good bargain. And it holds Rallis too. I think it may be a great bargain with less to lose from here and if certain things play out right, can give great returns.

Disclosure : Invested

I have tried my level best to understand the business and will be happy for some feedback. There may be some inaccuracies as well and will be happy to be pointed out by some fellow member.