Tarson has a brutal correction in this market. Poor sales growth (in-fact a decline in sales in 2024 vs 2025; this is after the acquisition of Nerbe - so the standalone older business has collapsed even more), fall in OPM (34% in 2024 vs. 51% in 2022) and huge fall in EPS (8 in 2024 vs. 18 in 2022). Looks like the smart promoter did IPO at peak of cycle

The hope as others in the thread have mentioned is the capacity expansion. They incurred 3000 Cr capex for Panchla plant and another 3000 cr is planned for Amta, Jangapur and Dhulagurh. Again incurring fixed capacity does not mean higher future revenues and depends on capital utilization also

If we apply IPO P/E to this stock, it must trade at 7 * 30 to 35 which is in the 210-275 range and it is near to that valuation now. I think it is a good candidate for tax loss harvesting if you are already invested given the huge fall but if you are a fresh buyer, you can wait till it touches 210 - 275 range

I think with Tarsons its important to dig a little deeper into the numbers to fully understand the business cycle and impact of CAPEX cycles. It has been a learning to see how massive Capexs while positive in nature can cause severe short-medium term pain due to the drag on EPS. Similar has been seen in Clean Science and other pharma and chemical names.

After a year of slowdowns and pain the financials are finally turning. EPS drag continues to higher depreciation and interest but EBIDTA is turning. Revenues even for standalone are at record high and this is even before Panchla has started commercial production. Also I think there is typo in your CAPEX it is not 3000cr but 500cr for both Panchla and Amta combined.

Personally I think Q4 or latest Q1FY26 should be better and will start seeing YoY PAT growth finally. However very important lesson in business and impact of CAPEX cycles that must be added to mental models for future!!

Disc - Invested at 470 levels and holding will add if PAT starts growing

Capex increase leads to profits & Sales increase eventually if there is demand uptick that results in higher utilization. Else, with low utilization, profits & Sales will see no improvement. Capex is in anticipation of demand; but the demand is not certain

On a separate note, if you bought at 470, good to do tax loss harvesting now.

Capex plan started 2 yrs back. Are we able to arrive at estimate for peak utilisation that could perhaps happen in next 4 yes ? May be in FY 29 this could get into 750 crore revenue based on 0.8 times fixed assets …if the margin expands perhaps 35 percent it could get to 220 crore net profit so eps around 33 ?with PE of 40 …share price of 1250…the estimates could be way off

Again if we can not predict the cashflow with a rough estimate we don’t know what it’s worth today based on discounted value and if we can’t value it we can’t put more into it until we have a proper estimate that makes sense 200 still seems enticing though

Looks like it was priced to perfection with the promoter planning for several years to have the highest margins by dressing the balance sheets and over a couple of years, the real state of the business comes out.

Wonder what type of accounting checks Marcellus did to pick this as a Little Champion?

I bought it around 600 level first, then downward averaged it at 450 then again at 360. Now it’s below 300 levels. I’m still holding on hoping for that the new capex will result in increased topline

What if 1) Tarsons put up excess capacity due to a large demand (capital returns) and now isn’t able to find demand 2) why not wait for better capacity utilisation or some kind of order book flow ? Same is happening with GMM pfaudlr. Why take such high oppurtunity costs unless the demand drivers are not clear ?

I have been following this company since its IPO days. Best of my understanding, there was no window dressing. This IPO came sometime in late 2021 and just after COVID. During that time, if we remember anything to do with medical (drugs, equipments, gloves) had bumper profits.

I believe we as investors were at fault when we presumed and assumed the continuation of those extraordinary profits even during normal / ordinary times.

If we spend enough time by listening to all the calls together, we can see that things were not adding up.

I have the benefit of hindsight.

Disclosure - No holding.

Typical curse of chasing stocks invested by Marcellus. Let this serve as a lesson to never buy a stock because some bigshot investor or popular fund is buying at inflated valuations especially at the cyclical peak.

Disc: took an L on this stock as there were better opportunities

As usual and as expected poor results once again. Going forward, the company may give much worse results, as the depreciation cost keeps rising, and existing capacity utilization itself is not great. I wonder what they will do with the upcoming capacity.

Over and above these, US tariffs are not helping with 10%+ exports to US.

Hi guys.. posting after a long time, as i mostly dont feel theres much value addition i can do!!

Coming to tarsons .. with the recent fall below 250 it interests me a lot.. as most returns flow as a function of your purchase price!

As far as the business is concerned its in a typical cycle where company has undergone huge capex ,resulting in operating deleverage, high interest costs, high depreciation. These are all normal, their topline and gross margin seem to be doing fine. Cashflow from operations are also 100cr+ which is damn good for current market cap..

They have a decent brand and have a very competitive cost structure. So the strategy to do large capex and concentrate on export markets can work well because of indian costs. ( a bit like balkrishna of labware market)

As with everything.. this needs time and patience to play out and obviously holds risks like tarrifs and general protectionism.

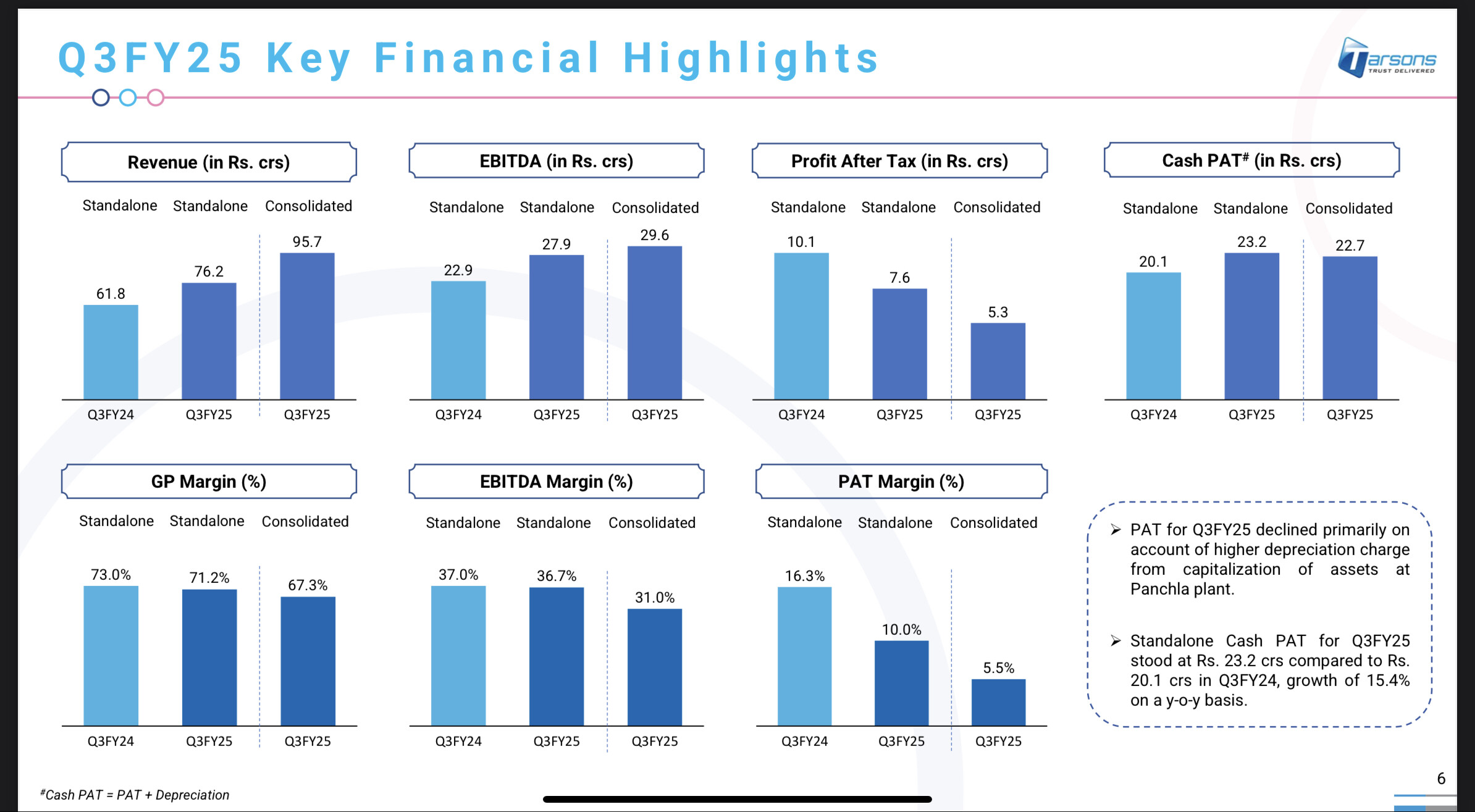

Been invested for about 2 years here and down about 50% on the position but continue doing tax-loss harvesting and restarting the position as I believe the company future once the CAPEX finally starts should be brighter. However this period of holding has been very frustrating with the company financials deteriorating across the board. Panchla was initially supposed to be fully operational by Q1FY25, that got pushed to Q3, Q4 and then H1FY26. Now management is saying it will only be fully operational in H1FY27, the management is regularly failing to ‘walk the talk’. Earlier guidance of 500CR for FY25 was rescinded and no further guidance is being provided. EBIDTA margins have fallen from 40-50% to now below 30%, part of this is due to Nerbe acquisition, but even standalone the performance is mid-30s. In general the feeling is that management had somehow pumped smoke into the financials before listing and now the reality is slowly coming out… I will continue to hold till the Panchla story unfolds but it has been very disheartening and frustrating so far..

The ebitda margins are down because of operational costs at panchla with no revenues. This is normal for any manufacturing business. The gross margins should be stable, which they seem to be.. at currently market cap it seems reasonable.. cash flow from operations could be around 120 cr for current FY.. rest we can leave it the market to value it correctly sooner or later

decline in profitability is primarily attributable to higher depreciation expenses of INR20 crores

arising from the partial capitalization of Panchla facility.

Also depreciation visibility

FY '26, my peak depreciation should be in the range of INR85 crores to INR90 crores, as I

already said. In FY '27, my peak depreciation will be in the range of INR100 crores to INR105

crores.

Post capex and at peak utilization, the fixed asset turnover would be 0.7-0.8 (claimed by management). I mean what’s the point in the business if it can’t recover even the Asset expense.

Please enlighten if my business understanding is naive.

Every business has different asset turns.. the roce is a function of asset turns and gross margins.. in tarsons case you can do the math at decent utilization and see if the resultant roce is worth your investment. Simpler way would be to see the peak roce in the previous cycle, (without the capex) and put a few percentage discount on that as margin of safety.. but hope the roce will be better due to higher scale..