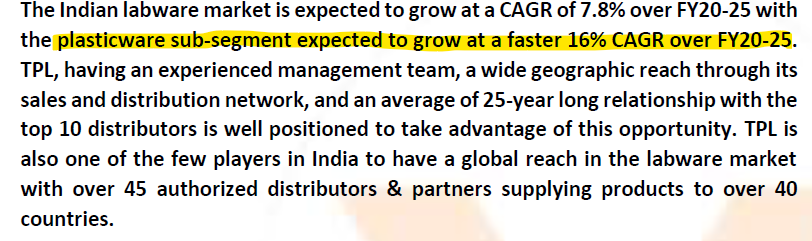

IMHO these projections can be achieved. From the above we can derive the end market CAGR is 15.38%

If the end market is growing at this rate then we can safely assume the labware will go either at the same rate or more than that ( in my view the labware market can grow beyond this )

Check the gross margin, though they depend on the imports but their gross margins are very consistent.

One of the raw material that they use is a bi product of phenolics production (Deepak Nitrite ) , since the market size / demand for these material is very low , none of the Indian chemical players are producing any of these.

Lot of noise around

It is a plastic, government can ban them - What is the alternative ? (We moved from glass bottles for beverage drinks to plastic , this is the case everywhere , we are now replacing the steel gas cylinders with PVC cylinders - Read Time Technoplast ) , look around us plastic is everywhere , so far governments not able to implement (including developed nations) plastic bag ban.

We cannot compare this company with Thermo Fisher etcc… and both are strong in their own way. I have checked with many people the common response is " Tarsons is the go to brand for them due to cheap pricing when compared to glassware " , quality wise they kind OK. But again if you compare the like to like glass vs plastic of the same SKU then obliviously glassware is better product.

This is a very good proxy play for the entire healthcare sector.

Few good reports (IPO notes ) Tarsons Products Ltd IPO Note (2).pdf (622.7 KB)

Tarsons Products Ltd.pdf (525.5 KB)