Hey @Tar

Any idea on the stelis would you think this might sold off or demerger given debt in their books?

Not an good idea for another acquisition though on Endo… Management has guided Q3 & Q4 will be slight better…

Hey @Tar

Any idea on the stelis would you think this might sold off or demerger given debt in their books?

Not an good idea for another acquisition though on Endo… Management has guided Q3 & Q4 will be slight better…

Dear Tar,

You may have analyzed the ARs of several other companies also. Here the 25+ cases, do you find it disproportionate to its size? In India, almost every chemical company has issues with environment and permanent closing are rare unless it becomes political issue like in the case of Sterlite copper plant. Mostly it will be notices to follow the regulations, in some cases temporary closure till you satisfy that you are following the norm.

Hi @Tar

Can you share any views on prakash pipes?

I have been hearing some corporate governance issue with prakash industires but since its not associated with PPL, do you think to continue my research with PPL.

Fundamentally it sounds good and there is already industry tail winds in this theme.

Your views will be highly appreciated

@Shikhar_Seth I could answer this, though you asked @Tar, as I’ve been holding this (and occasionally thinking of getting out) since pre-Covid and now at 2x.

Prakash Pipes was a subsidiary of Prakash Industries, and got listed itself ~3 years back - shares the same promoter (and probably even the address too). While it’s balance sheet is clean, and free of debts (compared to Prakash Industries), it suffers by association with the same promoter and their corporate behavior.

Just check most of the recent news, even in Prakash Pipes it’s all about how the promoter is increasing his stake with preferential allotment.

For the same growth and numbers the stock wouldn’t be valued so cheaply with a different half-decent promoter. I’ll hold this for now as I have a decent margin of safety, this is more or less a speculative position for me now,

thanks for highlighting it really helped.

Currently I might add few qty for tracking position and see where it leads

Hi @Tar

I have been a fan of you in tweeter. Thanks for all the knowledge you are sharing. Got a couple of questions just would like your views,

You have listed your portfolio from April till December 2021. I see there are only two stocks that have been retained in this whole period. The churn rate is very high. It feels like a momentum play more than value investing but at places you have also mentioned that you’re making a Longterm PF with a holding time of 10 years. What is your views on this?

I have also invested in Edelweiss China fund. Recently came across the ppfas video on china investment where they bring out a very important fact that investment in china companies are through shell companies constituted in cayman kind of islands which have a informal profit sharing with their Chinese counterparts. There is no strong legal binding on this and with a politically controversial government at any time laws can be tweaked. Moreover the Chinese government is more hostile towards foreign entities investing and are making very tight regulations while trying not to bend down to the US regulatories to bring out actual data for the us listed Chinese companies. E.g. Alibaba divesting in Ant without knowledge of major shareholder Yahoo. What are your views on the china investment considering these uncertainties?

Thanks in advance.

Kamal

Hi @Tar, you’ve been super bullish on the renewable energy revolution and your substack articles on the subject have been very interesting too. I wanted to pick your brains on the Solar EPC business and its economics. My initial sense is that this is a super competitive space and margins will always under pressure due to the bidding nature of the business, plus inflationary pressures arising from commodity price increases. That said, it can be extremely capital light and ROCE can be extremely high for efficient players. Your thoughts on whether Solar EPC players could make for good long term investments?

The specific opportunity is that Reliance recently took over as the promotor of Sterling and Wilson Solar (now Sterling and Wilson Renewable Energy Ltd). Now these guys have been industry leaders for a while, but had been marred by the inter-company deposit issues and margin compression. Their order book has been robust but delivery has been patchy over past couple of years. The ICDs also resulted in them facing bank guarantee challenges.

With Reliance taking over, many of those operational problems should be behind them. They have also announced their intention of entering EPC for energy storage and waste to energy. There is now an ambitious, cash rich promotor replacing a debt ridden inefficient promotor, and so it is a bit of a special situation play as well. The industry however remains very competitive and I am not being able to gauge how the unit economics work. Would love your thoughts.

Value, Momentum, Growth are just names and tags, I am in the market to make money, not to get my name attached to labels.

If you read the 6th post on this thread from top, you will see the above line. I am not in love with any company I invest in. if the story deviates, I will get out. Example, I was very bullish on Strides in the middle of 2021, when the story deviated I immediately got out unharmed. I know so many people who weren’t as bullish, yet remained invested cause ‘value investors’ and now are looking at 50% draw downs in their portfolio.

Have never called myself a value investor, nor will ever call myself one. All investing in my view is value investing.

You are looking at churn, but you’re not looking at weightage. Top 4 positions in my PF make up 52% of my PF and over time, if someone really is investing correctly, their portfolios should automatically concentrate as well.

The same video ends with saying, if you really want to invest in China have a low weightage. 5% of my PF is in China, how is that an issue?

All investments carry risk. In finance and valuations, discount rates are assigned to countries as well, these are known as country risk premiums. You can google these and find one for China as well as India.

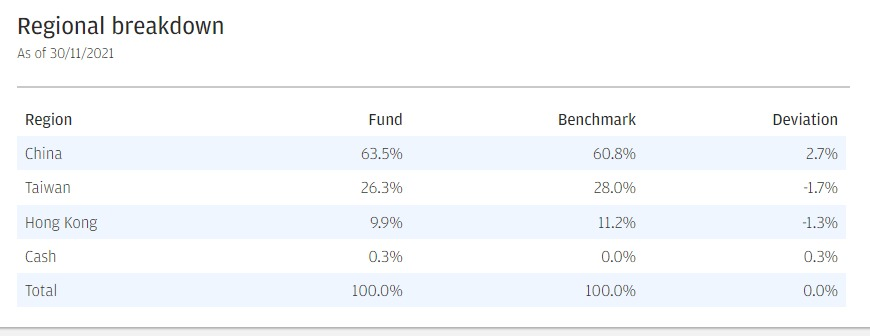

Risks related to China, in my view are okay to accept considering the valuations of these companies. Further, Edelweiss China Fund is not all just China. their largest position is TSMC.

Thank you very much for your detailed response.

Hope you have recovered well.

I agree everybody is here to make money and how we do it differs. Your approach is quite different, it’s just that we need to be in a monitoring marathon to keep up with the pace. I am an entrepreneur and majority of my time goes managing my business in which case I cannot do this kind of shuffling by close monitoring. But you have been doing a great job.

I think everyone who invests in china fund needs to keep a close eye on allocation to keep the risks low. You have aptly pointed it and I am now doing my reallocation as I have allocated more on this fund.

Thanks again for all your tweets, seminars and knowledge shared in public spaces.

I just noticed that Edelweiss China fund is treated as a debt fund for capital gains taxation purposes. STCG for profit made on less than 3 years investment and taxed at the peak tax slab of the investor.

Hi, All international mutual funds are taxed as debt or fixed income security. Edilwise is no exception.

Parag parek long term equity, axis growth and sbi focussed are treated as India equity as they have less than 35% in foreign securities.

Nasadaq 100 investment also gets the same treatment not just china fund. All funds that invest outside India are treated as debt fund so you will be paying 20% after indexation for long term.

@casperkamal @Shashank_Yerdoor

Sorry to butt in here, but on the China investment piece, there is a Chinese internet company focused ETF called KWEB which is traded in the US which you guys should have a look at if you’re interested in China exposure.

This is made up of internet focused companies like Tencent, Meituan, Alibaba, Baidu, JD etc. It is presently trading at levels that it was trading at in 2016! Most of the shares are held on the Hong Kong exchange and some are held through American ADRs. In case of any delisting from Nasdaq of any of the company ADRs, the fund managers can easily convert their holding to Hong Kong shares and so there is no long term delisting risk. Personally I find this the safest, cleanest and cheapest exposure to Chinese tech growth.

Not a recommendation. Just putting it here for information as people seem to be interested in the subject. I am invested (and biased) with about 2% of the PF and will raise it to close to 5% over the next few months of interest rate led volatility.

Full portfolio here Vineet Jain portfolio

The uncertainty in the case of Chinese funds is not just the risk of delisting from US exchange but how these ADRs are structured. The PPFAS video on Chinese investments outlines that these ADRs are out of Shell companies located in the Cayman Islands. They have just a binding agreement with the actual Chinese companies. So I’m not sure the derisking happens if we invest in Hong Kong.

Next Edelweiss is a feeder fund for JP Morgan Greater China fund and JP Morgan also has spread the investments between China/Taiwan/Hongkong. In case of delisting shouldn’t they be able to do what KWEB does? Asking as I’m not sure of how it would turn out to be.

From a personal point of view, I’m staying invested in this fund. At present my exposure is high so i will be limiting my allocation going forward.

I should have clarified, if one invests in Hong Kong, one is not buying ADR shares at all. The Hong Kong exchange trades the company shares directly. ADRs are American Depositary Receipts - only for US markets. These are inter-changable with company shares on the Hong Kong exchange. Over 75% of KWEBs holdings are already in Hong Kong shares, not sure if that is the case with Edelweiss.

Irrespective, an institution can make this switch much more easily if required, as compared to individuals. This is why it is safer to invest in Chinese equities through these funds than through ADRs of individual companies which a lot of individual investors do these days.

My reason for preferring KWEB over Edelweiss is because KWEB invests only in internet focused, new economy companies - the primary growth driver for the Chinese economy. I don’t want exposure to other sectors of China, like real estate for example. This way I do miss out on say biologics or semiconductors though, which I am comfortable with. And the valuations at present are extremely attractive - like I said they are trading at 2016 levels.

Absolutely. In my latest post on my substack, I talk about risk appetite for an investor. For you my PF approach may not make sense and for me someone’s else’s may not. In a similar way, a concentrated PF for me makes sense as I have no dependents, stable high paying salary job, loads of free time to research and an entire 20+ year career ahead.

So that’s why I never understood these tags of momentum, value etc. in markets. Everyone is different and needs to plan their own journey based on their risk capacity which is dependent on a variety of factors.

Hi Tariq, you mentioned you hedged #Strides during the quarterly results, so you could limit your losses. Do you hedge your portfolio during the Budget? Is it good to consider hedging pf near the budget time ? Can you write a thread on Hedging a stock/pf. on twitter

hey tariq sir , just wanted to know your views on proxy’s of real estate sector boom ( acrysil ,astral)

and your views on equitas bank ( and bank and finance as a sector for this year)

loved your thread keep up the good work sir .

No, if you hedge your PF, don’t try to time it unless you buy it as an insurance. Insurance/ option premium paid will be your cost and will ultimately reduce your return in short term but should help in the long run. For example, you can buy Nifty shorts every for 3 months out and refresh them for next quarter.

The problem with this approach is that even next month out options are very illiquid and prices are usually inflated.

Stock specific option hedges I try out whenever ‘events’ are near, esp. earnings example Strides.

As more companies get added to F&O in India, this approach should help normalize the returns over time.

Hi, you dont have to call me sir, you can address me as Tar or Tariq

I missed out on Acrysil, others are quite expensive today. Find real estate companies better priced and available at decent margin of safety.

Sorry do not track Equitas bank.

Thank you for reading and all the support