I Recently Came Across this Microcap Company

With Business model Combined to that of ACE and Sanghvi Movers

I have Made my notes on it and sharing the same

Views are welcomed

Disclaimer - Not Invested but Tracking to get better Price

Tara Chand Infralogistic Solutions Ltd.pdf (851.9 KB)

13 Likes

You need to put detailed risk analysis. Also need to put content on the thread. Pdf file is not preferred.

thanks Ashar for the detailed insights. I have recently taken position in the company.

Key triggers:

- 100 crore capex done in last 3 years - Big number for any micro cap. Can be highly valuable if INDIA’s growth story in steel, construction sector with timely capex done.

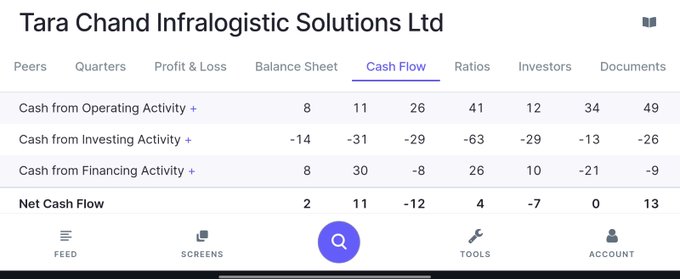

- Undervalued due to high depreciation leading to low ROE but consistent & increasing positive cash from operations.

- Exposure to steel transport and warehousing plus equipment rental business - 2 very strong growing businesses.

- Equipment fleet of 300 Machines includes Heavy Cranes (up to800MT), Hydraulic Piling Rigs, Steel Processing, and Concrete Equipment. working on High-Speed Bullet Train and Metro Line projects as well.

- 40 years vintage in steel logistics management.

- Well groomed and confident MD from 2nd generation and seemed to be quite transparent about business and any related issues.

Risks:

1.Exposure to cyclical Infra sector and receivables getting stuck although customers are quite diversified.(Had to write off some receivables in Covid time).

-

Excessive capex and inability to manage the same.

-

Company is from microcap space and can be iliiquid and risky bet.

Happy to hear others view on the stock.

4 Likes

Management invited at Alpha SME ideas conference. Everyone can subscribe to Alpha ideas since they keep hosting lot of SME’s.

2 Likes

Thanks For the input

Certain Point to be added Are that since the company’s Major tailwind will be Bharat’s Capex Cycle

We have to continuously track Capex Spend of Various Sector

See Sanghvi Movers for example during the time of Slow growth in Economy during 2015- 2019 the company suffered a lot on bottom lines

But one thing to add is that Sanghvi is more dependent upon Wind Energy Space

That makes them heavily reliant on single Sector

Where as Tarachand is Equally diversified in Mining, Railway, Cement, and Infra

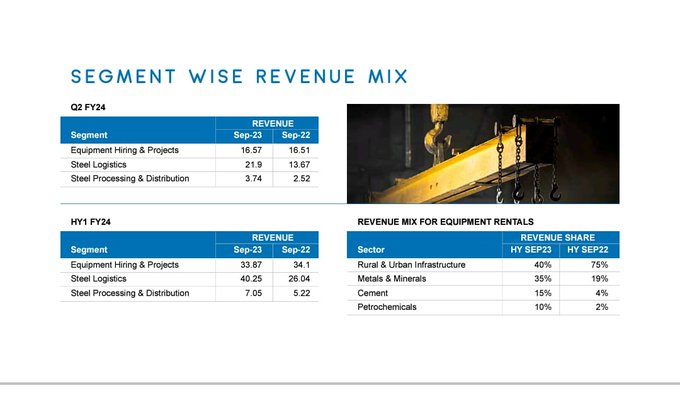

In Recent concall they said they want to take Revenue from Equipment rental in Cement capex to be taken at current Mining’s Level (35%)

For Such a small Company and having Clients like ACC, Ambuja, LT) is quite Big

also they have the product Portfolio Equally competitive as that of ACE and Sanghvi their largest Vehicle In Fleet is of the same size of that of Sanghvi

and correction on your comment imo about

They Have Left this work since this work was majorly Sub contracting and they were loss making there

Imo the real growth will start in next 2 Years when the Machinery is half way Depreciated and there is better pricing and also Utilization of the equipment’s

Very true But the sector is very Similar to Economy as large and if economy is seeing down turn that will be the first clue of Anti thesis being hit

I don’t think this will be the issue tbh, From Operational Standpoint they are Quite Fantastic

Very True but still the Alpha is also generated in this type Micro cap with Solid Business with Great Tailwinds

1 Like

thanks Ashar for the comments. Have highlighted few macro risks only. I dont feel any major risk to the company or stock at present. Also would like to add that have even reviewed the financials and AR and could not see any forensic or accounting issues here.

Have invested in the company for long term only. Truly believe it is a sanghvi kind of story whereas sanghvi is exposed to wind sector only which is a bigger risk.

On the PE expansion, it can happen anytime if investors realise that Cranes have to be depreciated 20% every year as per Companies Act. Once the equipment gets little old, Dep shall go down and PAT shall go up resulting in PE expansion.

8 Likes

Tarachand infra logistics CMP-175 ( 14/jan / 24) MKT CAP - 248 crore P/E -21 Promoter holding - 73.3%

needs through Warehousing,

Transportation, Equipment Rental, &

Turnkey Infra-Project Execution. With 35+

years’ experience, we’re a top Steel

Warehousing & Transport entity, handling

10M+ tons of Steel annually.

Machines includes Heavy Cranes (up to

800MT), Hydraulic Piling Rigs, Steel

Processing, & Concrete Equipment. We’ve

contributed significantly to High-Speed

Bullet Train & Metro Line projects across

cities like Ahmedabad, Delhi, Mumbai,&

more

equipment serve sectors like Power, Oil &

Gas, Renewable Energy, & Urban & Rural

Infrastructure. We cater to 52 diverse

customers, spanning PSUs to Indian

multinationals, operating in 21 states &

even internationally in Mauritius.

Focus on acquisition of large tonnage cranes & higher capacity pillingrigs & aerial platform,cont capacity addition, cont pursuing opportunities to take up EPC projects, civil & mechanical construction of building

expanded operations to the j&k, Assam ,Kerala Odisha

OPM margin is v good

EPS growth is fantastic

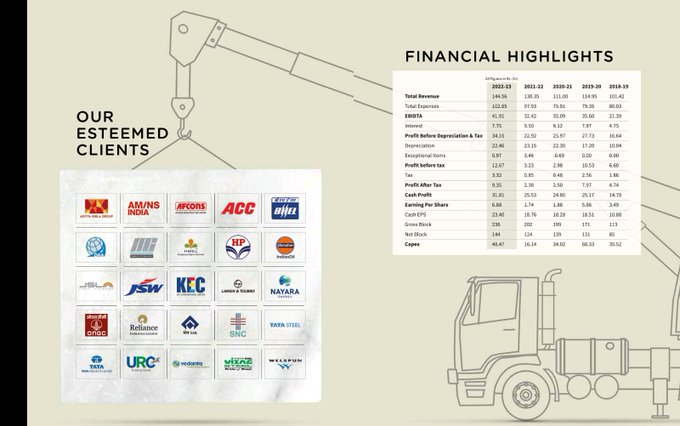

![]() Financial highlight and esteemed customer

Financial highlight and esteemed customer

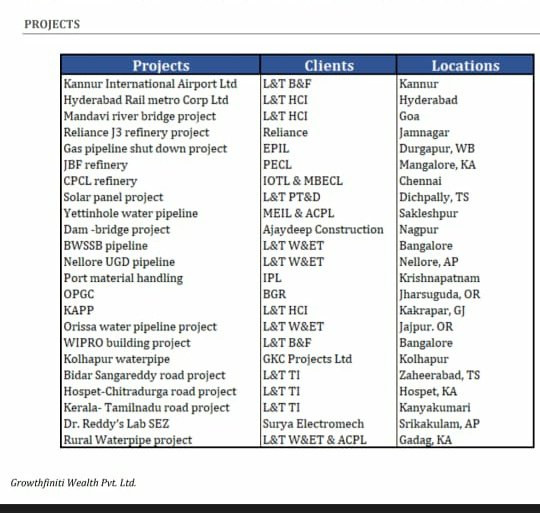

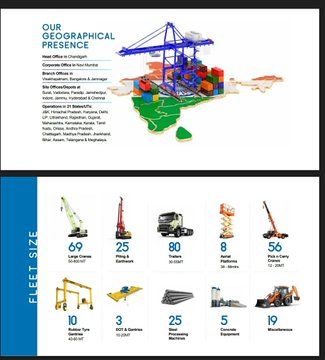

![]() Running project, client,& city, fleet size , geographical presence.

Running project, client,& city, fleet size , geographical presence.

!Sanghvi mover is available at good valuation , good OPM ,

ACE construction

Demand of industrial production if someone down cycle comes it’s become heavy affected, other also some very good brands than tarachand can able to get to capture higher market share leading to loss, client concentrate L&T

Pl consultant your financial advisor before investing,

No buy & sell reco,

Invested & biased

first investment at dec 23

no transcation last 15 days

7 Likes

Concall Summary (Q3 of FY24)

Quarter Ended: December 31, 2023 (Q3 of FY24)

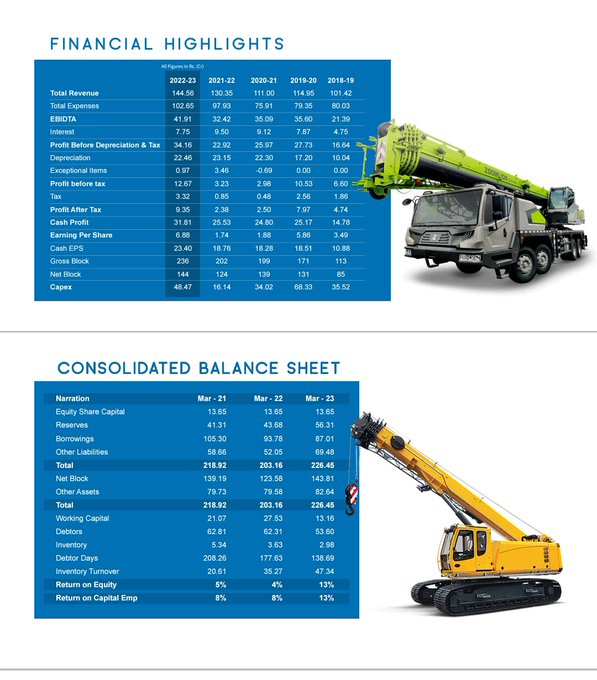

- Total Revenue: ₹44.85 Crores

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): ₹14.53 Crores

- EBITDA Percentage: 32%

- Profit After Tax (PAT): ₹3.35 Crores

- Cash Profit After Tax: ₹11.55 Crores

Period: 9 months ending on December 31, 23

- Total Revenue: ₹127.96 crores

- EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization): ₹41.30 crores

- EBITDA Percentage: 32%

- Profit After Tax (PAT): ₹9.83 crores

- Cash PAT: ₹33.35 crores

CapEx Overview (Year Ended 31st December 23):

- Total CapEx for the year: 48.52 crores

- CapEx for the quarter-ended 31st December 23: 14.06 crores

- Equipment addition is based on the order book with clients.

- Average Capex of 40 to 50 crores annually expected for the upcoming years

Net Block Increase:

- Year-on-year increase in netblock: 27.94%

- Net block as of 31st December 23: 172 crores (compared to 134.7 crores in the previous year period)

Gross block Growth:

- Gross block as of 31st December 23: 284.76 crores

- Percentage increase: 22.64%

Debt and Financial Ratios (as of 31st December 23):

- Total debt: 89.52 crores

- Debt-to-equity ratio: 1.08

Receivable Cycles Improvement:

- Receivable cycles as of 31st December 23: 110 days

- Improvement: 29 days compared to the previous financial year as of 31st March 2023

Order Book (as of 1st February 2024):

- Order book value: 36 crores

- Anticipation of new orders in the coming months for continued growth

Equipment Hiring Services (Segment A):

- Revenue of 20.42 crores in Last Quater

- Revenue of 54.29 crores in Last 9 Months

- Contracts have variable durations, ranging from a few months to several years.

Steel Logistics (Warehousing and Transportation) (Segment B)

- Revenue of 20.38 crores in Last Quater

- Revenue of 60.64 crores in Last 9 Months

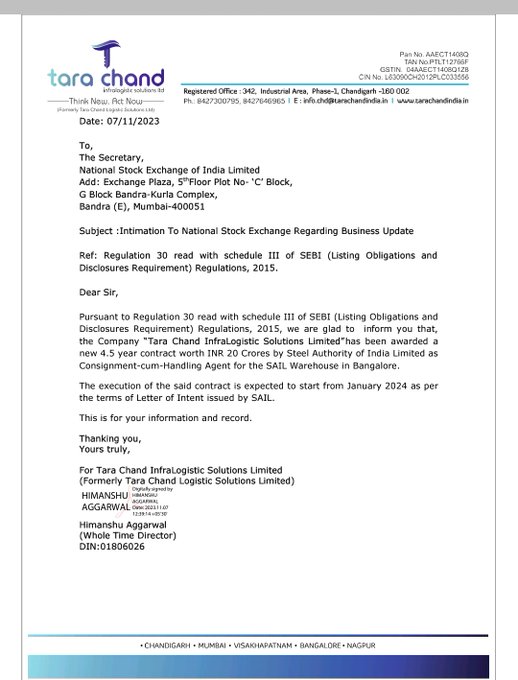

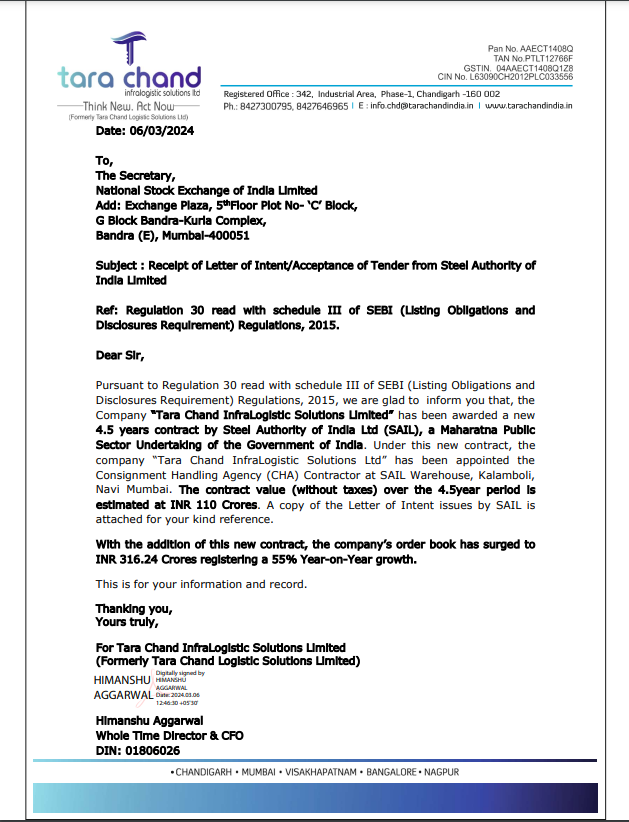

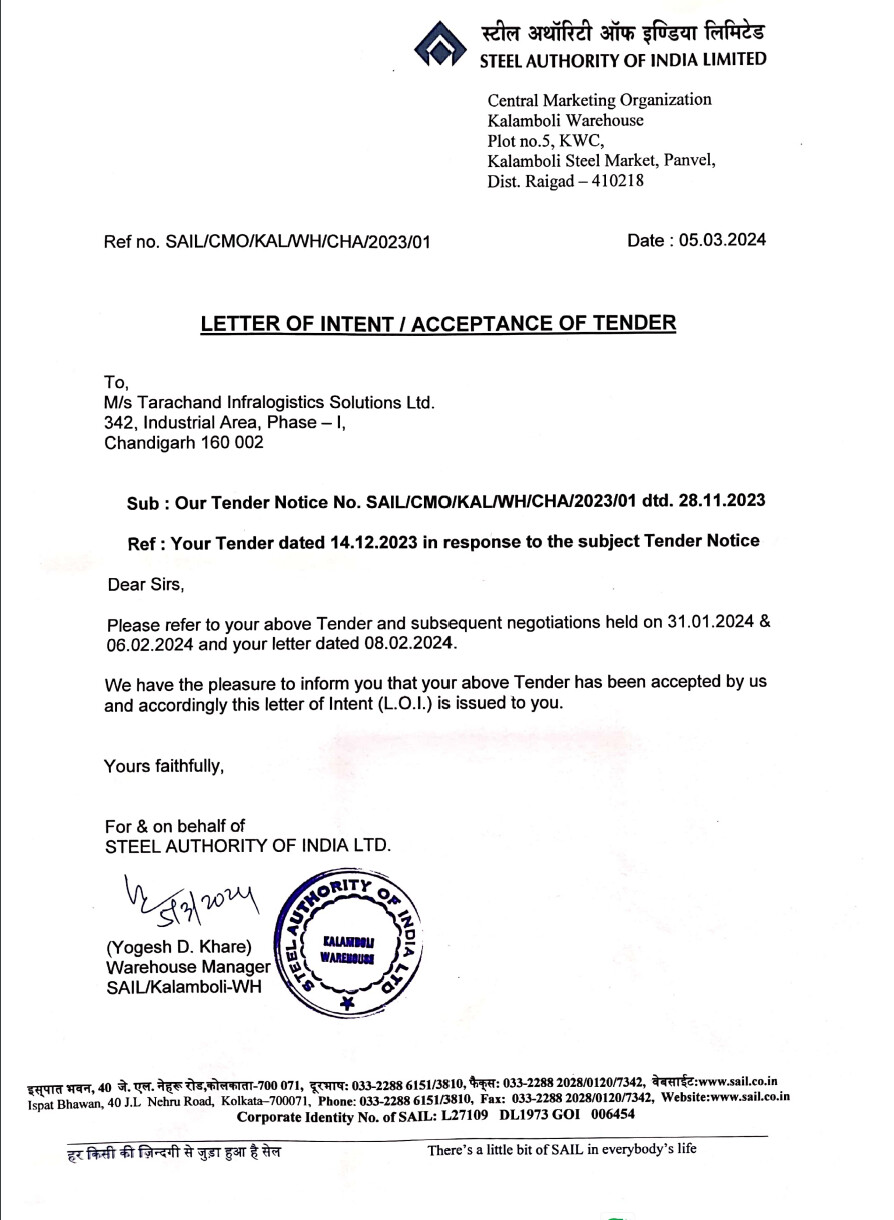

- Contracts in this segment involve working with public sector undertakings like SAIL (20 Crore Project) for 10 Years.

- Contract durations typically range from 4 to 7 years.

- Contracts are secured through government tenders.

EPC Business (Segment C):

- Revenue of 3.56 crores in Last Quater

- Revenue of 10.61 crores in Last 9 Months

- Anticipated tenders in the last quarter did not materialize as quickly due to a prolonged tendering process.

- Expectation of positive impact in the current quarter and subsequent quarters.

- Exploring entry into specialized EPC segment.

Capacity Expansion Projects in the Steel and Cement Sector:

- Reasons for Infra Projects:

- Equipment acquisition in recent years focused on capacity expansion projects.

- Equipment aligns with the ongoing expansion initiatives.

- Factors Driving Project Selection:

- Improved revenue mix and better pricing at selected plants.

- Long-term contracts are established with these plants.

- Effect of Subcontracting Discontinuation:

- Subcontracting work ceased in the last year.

- Resulted in a significant margin expansion across all quarters.

- Future Margins:

- Margin expansion is expected to persist with the ongoing growth in the top line.

Overall Business Growth and Future Plans:

- The company has experienced a growth rate of 20 to 25% in the past year.

- The average monthly yield is approximately 2.5%.

- Anticipating this growth trend to continue.

- Expecting additional growth with new orders in the pipeline.

- The fourth quarter is crucial for sector revenue and for growth.

- Target industries for expansion: cement, steel, and petrochemicals.

- Exploring the renewable energy sector, specifically the wind sector will be carefully evaluated but the equipment is already purchased.

- Continued focus on cement, steel, and petrochemicals expansion.

Interested and Tracking the Company

Regards,

Fawaaz.

4 Likes

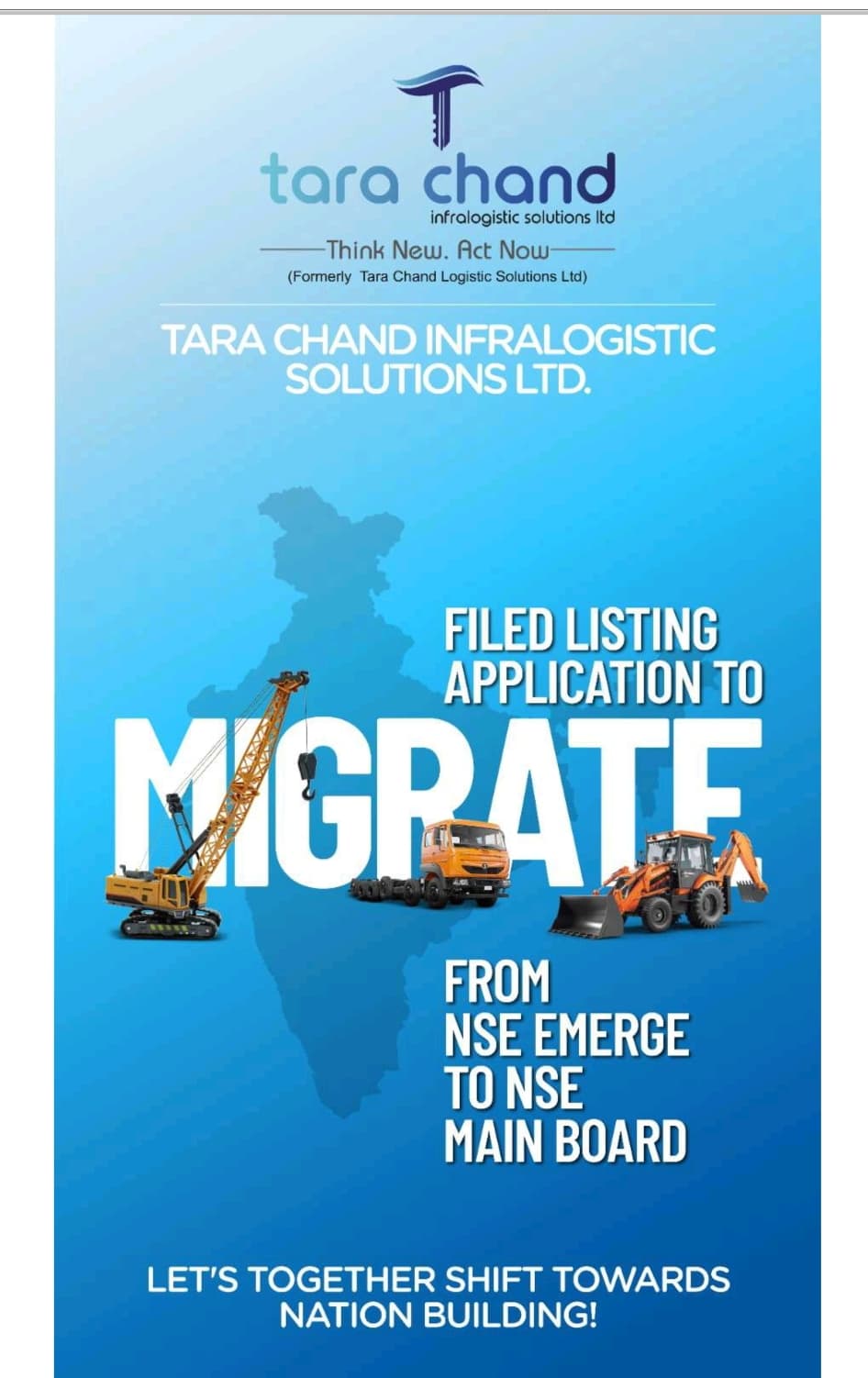

how long does it take one to migrate, when is it expected to complete ?

Anywhere between 20-25 days. As per concall Himanshu stated that Tarachand will be on NSE main board before end of this quarter.

2 Likes

Does conversion of warrants into equity shares have some lock-in period?

1 Like

Attatched is the following page of the document you attached.

For better understanding,

Does Letter of intent / Acceptance of tender means the contract is awarded?

Question from a novice investor.

Yes, Swadesh. The above image I shared is an update to NSE from Tara Chand about the same.

Much required triger imo

Management is capital prudent

Will have to see the terms of finance for further understanding

2 Likes

Any idea, when it’ll be migrated?

1 Like

Please do your due diligence first

Dont clutter thread with one liner questions

There was Prefrential issue at a price of 70

A simple screen search would have been sufficient