Thanks for reply Ashar and will keep it in mind.

Recent Capex announcement is much appreciated and shows where the promoter is focusing. INR 160 crores capex on a gross block of INR 163 crores in the highest margin biz and also entry into Wind EPC cranes rental biz. I’m guessing that we’ll be seeing margin expansion here. Let’s see how it plays out.

Disc: Invested and biased.

2 Likes

The revision in outlook factors in the improved operating performance, with revenues of Rs 125 crores achieved till December 2023, the run rate is estimated to continue through the full year backed by healthy execution of orders in hand. Further, an orderbook of around 316 crores as on March 2024.

Revenue estimated to be around Rs 150-160 crores for fiscal 2024.

3 Likes

I think they should be able to close the year somewhere in between 165 to 170 crores.

1 Like

@VIMAL_AGRAWAL @Meetkatrodiya @Ashar_Mann

The order book is ~ 325 Cr.

Let say FY Revenue comes out 170 Cr.

How much order they would be left with at start of FY25 ?

I’ve started tracking recently but before i make a move ![]() CMP doubled just in a 1 month from 144.

CMP doubled just in a 1 month from 144.

I find tarachand to be good name with bright prospects for few more years.but Before i give into FOMO. I wish to study & understand what could be prudent approach to hook up with ? ![]() . Let it migrate to mainboard or wait for a blimp ? What could be Base/Bear case scenario ?

. Let it migrate to mainboard or wait for a blimp ? What could be Base/Bear case scenario ?

Market cap is ~400 Cr.PE~34, CMP ~ 5.03 times book value ![]()

1 Like

1st thing 1st

PE shouldnt be the metrics that you should be viewing this are high depreciating co. Look at cashflow

2nd thing how does it matter weather it is at SME or main board? Think of it this way if you wanted to buy Parle G but the same wasnt available in Dmart hence you bought the same from local vendor. How does this matter eod its the biscut (In this case business you are buying)

The business did 50 crores of Op. Cashflow last year on Mcap of 400 crores (12.5% yield)

The co. Is doing 170 cr. Of capex mostly towards renewable side where there is shortage of cranes

It can do another 40 cr. Of cashflow easily with better rental yield and good utilisation

Get out of price baisness if you are holding the business

There is nothing such as bear case scenario if you want to buy the business

If you have any bear case scenarios dont buy it simple

Maybe baised, DYD

7 Likes

@LarryWink I had nothing to add .

Very true, not only hold for this biz. but for everyone.

1 Like

Cumulativa PAT since 2017: INR 47 crores

Cumulative CFO since 2017: INR 181 crores

And this is an asset heavy biz. blend of B2B and B2G biz. we’re talking about and when it was at 140 levels it was a no brainer for me because EVEBITDA was less than 5. I won’t be surprised once this 160 crores capex is done and they start getting order from wind sector people will be happy to pay EVEBITDA of 15 times.

PE might look elevated in the near term because of huge upfront depreciation.

Plus, margins would expand because of the mix change.

Yes, the run up in last month is huge and personally unexpected, I see growth accelerating in business from hereon.

And by looking at latest numbers of wind capex, I think we’re seeing a new sunrise.

7 Likes

@Ashar_Mann

I will not add any emojis, for now(I may edit it later though) as you seem to dislike and may be wont pay attention to what i intend to explain or question i asked in earlier post.

anyway ill repeat question, if you happen to have experienced it or know the answer you may reply.

When a name migrates to mainboard, generally speaking, it would have wider participation and number of shareholders would increase. hence some early investors may try to book little profit and cmp may go sideway for a while ?

1.Posting & tagging , VP has loads of threads and people do tag anyone they think are connected or expert , there is very little one can do about it. they may ignore or flag it.Do you have any suggestions for managing this?

2.Emojis may seem childish to some, i was strict/single visioned when i was in final phase of my studies ~1.5 decade ago but to me the numbers are dull and boring. Emojis, though perhaps deemed childish by some, can serve to lighten the mood and facilitate engagement even when people discuss complex engineering/chemistrytopics. i agree there are people with different style but there is very little one can do about it. if i would wanted to change my communication style i would have been on different platform than VP.

3.I try to follow sectoral trend/momentum especially on equity thingy. My purpose of being in this thread or VP is to get ideas passively and not debate. This thread/VP has been incredibly useful to me - in terms of making money by getting ideas. While i like your focused bets and focused tracking of numbers.my style is to ask questions to have clarity for a particular doubt i may have.

Hope all is good for now, yes ? ( because i am going to edit and add emojis later…bahaha).Bytheway Tarachand is on mainboard today, i took tracking position, intend to increase allocation as my conviction grows.

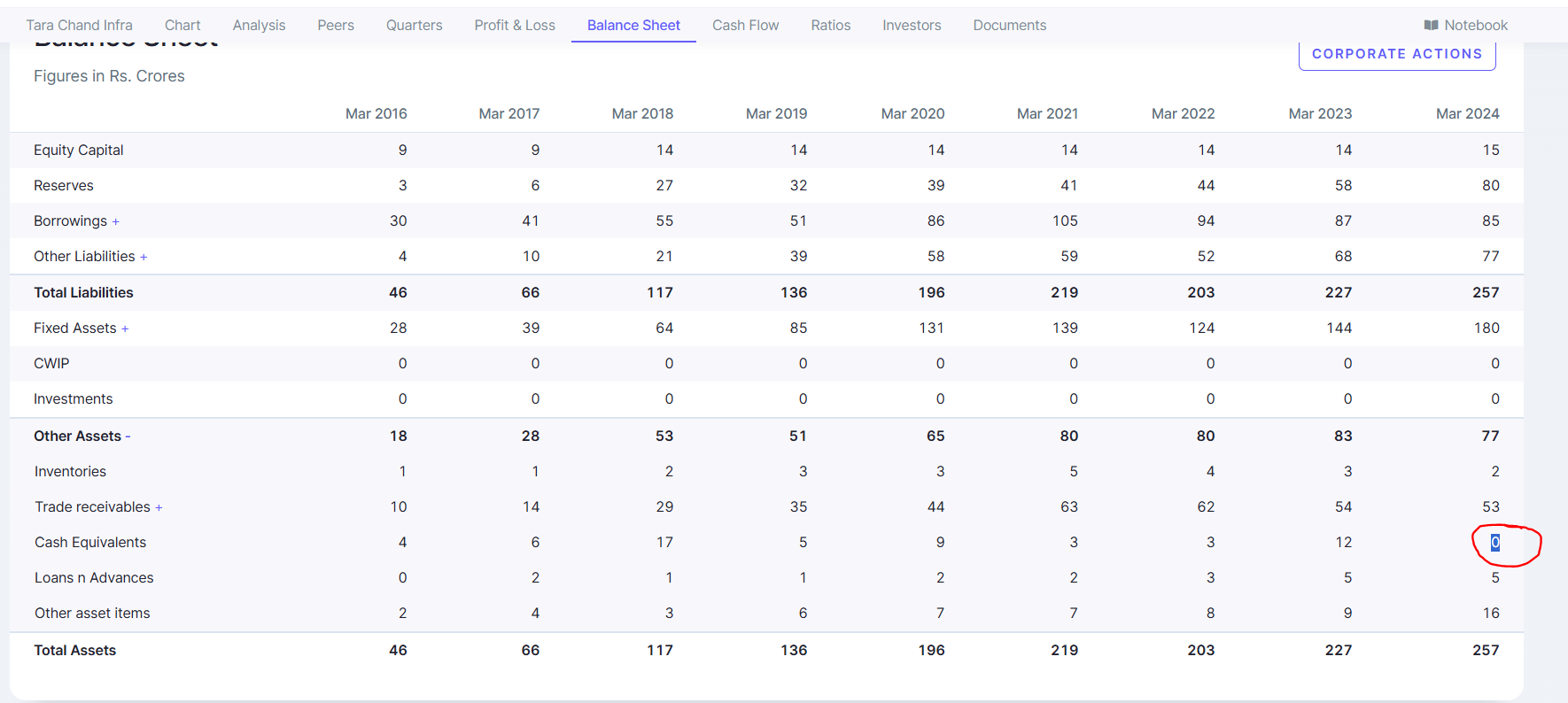

Gross block before the new capex is Rs. 236 Cr as on FY23.

1 Like

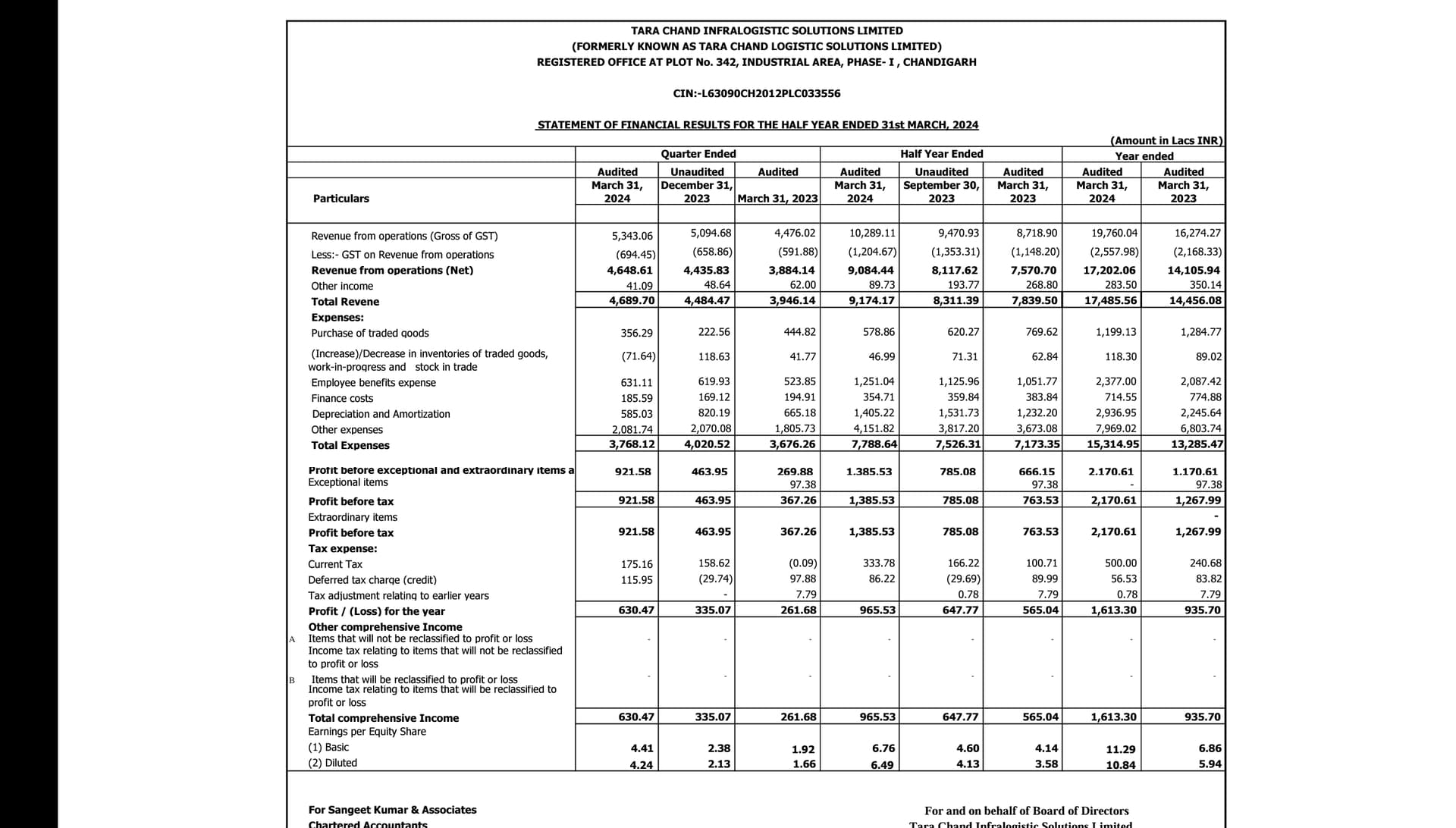

Tarachand what a marvelous results ![]()

![]()

![]()

GROWTH -15% yoy& 5% qoq,

EBITDA - YOY 3X &QOQ 2X

PROFIT - YOY 2.5 X & QOQ 2X

DISC NO RECO ![]()

![]()

6 Likes

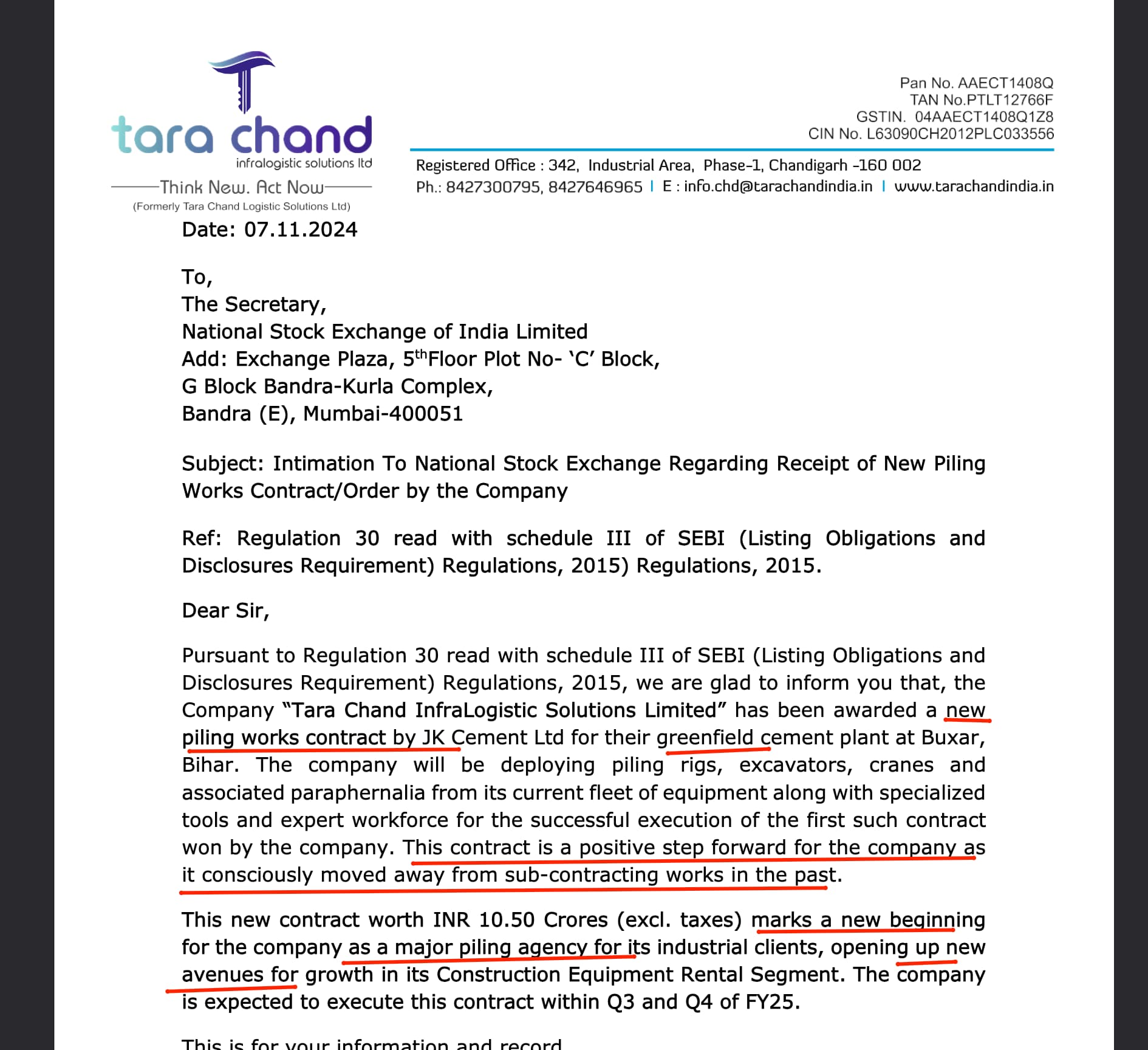

As per the filling this is new line of business, so orderbook can go higher than previously estimated by the Company.

5 Likes