Agree. Tanla doesn’t want to acquire companies and investment in creating platforms can be financed on the fly with the monthly earnings. Buyback is only way to use cash. Unfortunately it’s not directly available to it. Most of earning of Tanla is in two subsidiaries - the Singapore one and Karix. This cramps the style totally. They need to figure this out. And doing last year kind of buyback is a waste of time - didn’t move the needle at all. It has to be proper buyback like in 2020, but how to get money from subsidiary without doling out 25% income tax First on the dividend income ???

1 Like

I agree. Under some circumstances a benefit of doubt can be given to management for that “one-off” action.

They were disposing their platforms and deployments since the announcement of Karix acquisition in late 2018-19.

And although strange, Trubloq is really an impressive platform. The scale it works at Airtel and Vodafone should be appreciated. Airtel DLT registration page infact credits Tanla ![]()

And managements response to that action has been satisfactory to say the least. The appointment of Sanjay Kapoor as Director and advisor is a very strong move. The reporting has been good, the MWC participation was very good too.

Disc - invested ~3% of portfolio and on a watch out for managements response in next year to increase the holding

2 Likes

There is a way called inbound mergers, one of our client is doing it to save taxes. Issue is not about ways, issue is about intent. whether tanla wants to do it or not.

Tanla appoints TRAI’s veteran as Chief Trust Officer.

Another great synergic appointment from Tanla. Accumulating a good team from major telcos and TRAI in the last 3-4 years.

5 Likes

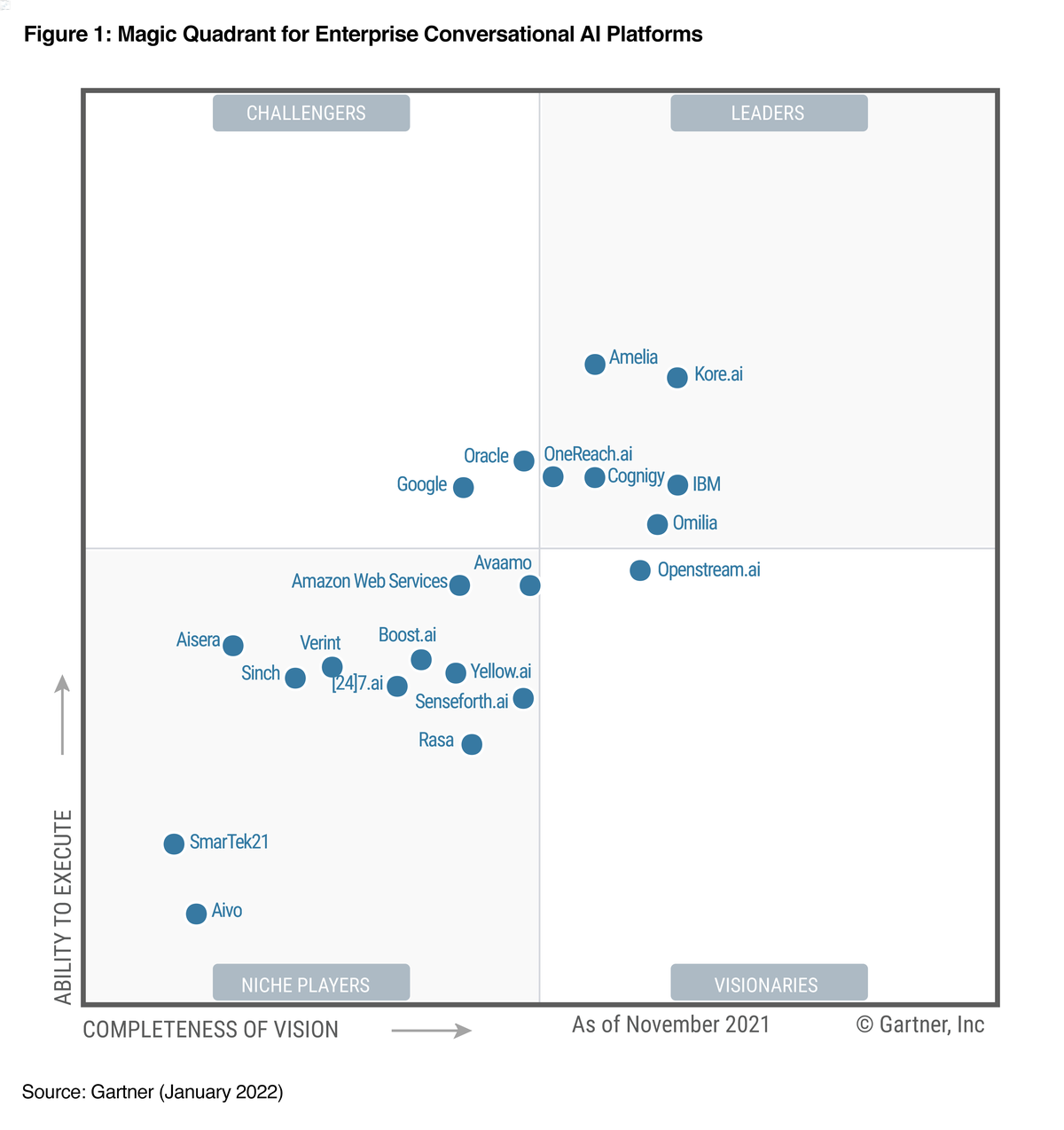

Partnership with Kore.ai to deliver conversational AI solutions on Wisely in SE Asian geographies. Unlike Vodafone, which is a customer for Wisely, this seems to be a supplier partnership which enhances the capabilities and revenue generating potential of Wisely.

They mention that the partnership is exclusive, probably means that Kore.ai cannot tie up with any other CPaaS players in the mentioned geographies.

Anybody know anything about Kore.ai or have any experience? Would be good to hear some feedback.

1 Like

Some details about this company available on crunchbase.

Would be good to know the kind of partnership forged. The one with truecaller was revenue sharing.

1 Like

Leader in Gartner Magic quadrant for “Enterprise conversational AI Platforms” says something Real good stuff about Kore.ai, will definitely bring in considerable transactions.

Revenue will be the key monitorable. Or will Tanla learn from the leading player and offer their own solutions for rest of the world!!!

2 Likes

Most announcements by Tanla sound very nice. Unfortunately, there is very little understanding with most investors as to what it means for revenue, market share , competitiveness, customer acquisition/retention and bottom line over a period of time. Feel good is there, but modelling is not possible.

Hope Tanla investor relation does a better job imparting understanding to investors what such alliances, partnerships or capabilities will deliver to the company in terms of measurables.

One thing I do pick up and could try to correlate - the 4 markets where it got exclusivity besides India, could potentially be markets where it plans to foray internationally with Wisely to begin with. So far, we haven’t heard anything about it - but this seems plausible. All 4 are good markets - that’s promising.

Disc: invested , but circumspect.

3 Likes

Hope Tanla investor relation does a better job imparting understanding to investors what such alliances, partnerships or capabilities will deliver to the company in terms of measurables.

Its possible to write to Tanla’s Investor relations cell seeking clarity on nature of partnerships. Joining the quarterly concall to ask these specific questions directly to management is also possible.

While I do agree that Tanla can improve its product/capability related communication (I don’t think their website is up to the mark), I don’t think its realistic to expect revenue projection guidance from Tanla management regarding such partnerships. These are partnerships for a brand new platform and therefore will not be immediately material to top line in my view. Vodafone-Idea is an exception because they have been Tanla’s clients already (VIL has, not Idea). Truecaller partnership is about a completely new vertical for Truecaller, so again revenue expectations should not be high. Kore.ai is not even a revenue partnership, its a capability partnership. Wisely can now offer top notch conversational AI capabilities in select geographies via Kore.ai. How does Management put any numbers to that at this early stage? Not possible in my view.

Personally, I wouldn’t be in a hurry to project Wisely revenues at this stage. Q1 will be the first quarter of Wisely with Vi-Idea, let’s see the incremental top line delivered. Projections can be done post that.

5 Likes

It’s not only revenue projection that one is looking for. Understanding what a particular partnership or capability does for the business is most important.

In this case for example, did Tanla already had some conversational capabilities? Were they falling short of market expectations ? How long will Tanla take to bring this capability to market ? What kind of customers will it be able to address with it? What is the size and dynamics of market being addressed … There are many such questions.

I understand not all questions may be answered or answerable immediately. But accessing impact of such partnership /Capabilities require some to be answered. Otherwise it’s just a good feel for me at the best.

5 Likes

A big anti thesis point to CPaaS companies if following is considered and rolls out.

Given the number of scenarios where financial institution sends messages, I doubt the practicality of in-app messaging. People having smartphones doesn’t necessarily mean they are comfortable with banking apps. I have no data to back my claim but someone who understands and can act on in-app messages is not the prey of frauds.

Looks like there are lot of technical (technology) queries around this capability and it’s relevance to the CPaaS platform and business.

This capability will simply add conversational AI features to the CPaaS platform (wisely) enabling P2A and A2P communication across the various channels. This is very similar to BOT support on WhatsApp for airline booking and is in-line with Uday’s mention of contact centre automation. Once the two platforms are integrated, it will provide a seamless and uniform interface to all customers. Don’t think Integration should be a huge effort as these are driven through API calls.

From business strategy point of view, the management seems to have decided to go for an ongoing partnership with Kore.ai rather than acquiring it, which could be on a revenue sharing basis - API monetization. Perhaps, to keep the innovations/technological advancements across the two areas/platforms independent and separate in the long run.

Refer below link for more details:-

2 Likes

This need not be a concern as omnichannel is here to stay.

1 Like

Thanks, the link is quite helpful.

I do understand how this partnership will work. But looking ahead what I would like to understand gradually is the strategic path for Wisely development i.e. the partner vs build vs acquire question.

- Which capabilities are core enough to be built in-house or acquired?

- Does Tanla have the software development bandwidth to deliver multiple capabilities on top of Wisely in-house? It sounds like a challenging task as there are varied capabilities that could be built on top of Wisely.

- Are acquisitions to obtain such capabilities good capital deployment? Will the ROCE of such acquisitions be good? Synch and Twilio keep acquiring but both those companies are nowhere near profitability even at operating levels, so can’t really tell.

As I understand right now, Wisely as-is provides a blockchain enabled, end-to-end encrypted and secure edge-to-edge CPaaS network. To make it a thriving CPaaS Platform ecosystem, a lot of capabilities have to be plugged into it such as CAI.

How effectively Tanla deploys capital or partners to bring in these capabilities on Wisely with exclusivity (Important to have a competitive differentiation) will determine how well the platform can do globally and whether it can challenge the leaders in Western markets.

Tanla’s story in India is clear and that growth will continue. Whether Wisely can fire up a serious global growth engine is going to unfold in the next few quarters. How many Indian SaaS companies have launched truly globally accepted products till date? Is it only Freshworks and Zoho? It won’t be easy but then turning the company around from zero also wasn’t easy.

5 Likes

So far, I don’t find anything wrong with the business strategy. From the concall, I gather that Uday understands the domain and technology well (important for platform business) and his focus around profitable growth seems intact. It appears that while other players have all along focussed on platform/aggregation business, Tanla seems one step ahead prepared for an ecosystem play.

Refer Wisely webapge which onboards “aggregators” apart from MNOP and enterprises: -

As far as technology/platform upgradation is concerned, the mgmt may look at a mix of build vs partner. I would think acquisition to be the last option since Tanla seems at the forefront of technological innovations. CAI in itself is not as simple as the example I gave above. It would require deep understanding and construction of models across each vertical to cater effectively to customer queries/requirements. However, if you have some capabilities in mind or found in other CPaaS, send it across and I can take a look.

I have not tracked Freshworks and Zoho but a cursory glance shows that they are mainly horizontal SaaS products. If so, it is not an apple to apple comparison.

3 Likes

Has anyone picked up anything on a further ILD SMS price hike for off-net sms effective from July’22? Would like to understand correctness of this. If true, for Tanla it could perhaps help deliver an additional 3-5% topline (and bottomline) increase YOY.

1 Like

I recently wrote to Tanla Investor relations asking some questions about Kore.ai, Wisely GTM, the existing partnerships status on Wisely and other aspects regarding recent news cycles on in-app notifications etc. Got a response from Tanla today. Summarizing the details below. Pretty happy with the quality of responses and quality of responsiveness to a retail investor

-

Kore.ai partnership – Kore and Tanla will work as partners to cross onboard new customers on each other’s platforms in the mentioned geographies. No movement of existing customers will happen. Partnership will be on a revenue share basis but % share of Tanla and Kore.ai can’t be disclosed. Partnership likely to go live in a few months.

-

Wisely GTM – Wisely will continue to act as an ecosystem, matching enterprise customers with service providers (like Kore.ai). So, expect many more such partnerships on a revenue-share basis. According to Tanla, acquisitions are not always efficient and acquiring a product will involve significant costs in integration with Wisely and might become similar to developing a new platform which would not make sense. Services like Kore.ai anyway will be integrated with the enterprise customer’s stack and not Wisely’s stack, so going ahead partnerships will continue to make sense.

-

Truecaller partnership – Beta testing is over and partnership will go live soon. Truecaller business messaging will be richer than normal SMS but not as rich as WhatsApp communication, somewhere in the middle.

-

Vodafone Wisely rollout –Tanla re-iterated that partnership is for all ILD traffic on Vi network originating outside India and coming into India and the originating network can be non-Vi also. Partnership is on a revenue share basis with Vi but no disclosure of revenue share %. Revenue potential can be calculated by estimating Vi ILD revenue. This Q1 will not see full revenue impact as go-live happened in end-April, Q2 will see full impact.

-

Tanla does not believe that push for in-app notifications over SMS makes sense in terms of security and accessibility. They gave examples of many folks in India with 2G/3G handsets who may not be able to get in-app notifications; also asked to examine how many of us have banking apps installed on our phones (not many) and indicated that developed economies are still using SMS because of security and efficiency even though many of those economies don’t have regulation regarding SMS as India has.

-

They are aware of need to 1. Revamp website 2. Bring forward AGM and Annual report and 3. Increase communication on explaining CpaaS and Wisely so that more non-tech investors can understand the space and Tanla’s products. They said that work is ongoing on all these aspects and will be visible in the coming months.

17 Likes

Thanks. It is very informative.

Truecaller will go live end June/ early July. Hope they are able to get to 1% share of the market in a rapid timeframe. Getting some critical mass on it early will be key to making it stick.

The push from fintech to get out of sms notification is not likely to happen/have much impact. Banks are having majority volume and they are unlikely to shift. This risk can be discounted by and large IMO, at least in the short run.

Wisely continues to remains a mystry. As for International foray, hopefully we will get some idea on Q1 concall.

I hope Kore.ai does well. Tanla’s own solution is pretty primitive. This can perhaps help Tanla get back in conversational game, where it is losing out.

Additionally Tanla and one other company are likely taking away market share in Enterprise business from the foreign companies Indian acquisitions … Though extent of same is not understood by me yet. This is a big +ve.

ILD sms on-net price increase, still there is no confirmation. That will be another positive of 3-5% additional growth, if true.

Uday Reddy did a good thing last year giving dates for the quarterly results in advance. Maybe he can add the annual report date for the next year as well. In any case, I believe all companies should ideally give out their last year Annual report before giving out Q1 results.

Lastly , I am awaiting the opening up of experience center in Hyd and a chance for share-holders to be able to visit - this was mentioned 2 or maybe 3 quarters back. All product / tech related questions can be addressed that way.

2 Likes

Yes Tanla seems to be moving towards an ecosystem play with Wisely. Wisely will be the secure network backbone and multiple capabilities will be offered through Wisely via partnerships and maybe some in-house builds. Partnerships will be in a revenue share mode.

If you have an understanding of the global CPaaS space, how do you assess this strategy and would you be able to compare it with the likes of Synch and Twilio?

2 Likes