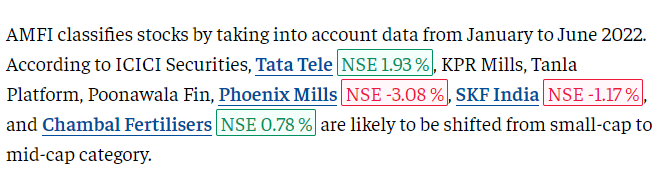

Extract From ET: amfi: Adani Power, Chola Invest, BoB may get AMFI's large-cap tag - The Economic Times

Extract From ET: amfi: Adani Power, Chola Invest, BoB may get AMFI's large-cap tag - The Economic Times

Ecosystem play is a different ball game altogether. It gives an opportunity for several players to participate in the consortium with a common objective of achieving greater value for themselves than they could capture alone. It helps create and share value in collective for a common set of customers.

At the core, CPaaS is a commodity business and hence a volume game. Given this, the best strategy should be to attain scale & value propositions (to lock-in customer) with minimal effort and capital. However, since technological innovations pose a risk of disruption to the business, it is better to align with it to keep pace with the change. In other words, technology becomes a means to an end and not an end in itself. Doing so, also reduces the business/market risk on a single player as all brands together bring in value propositions in the pursuit to capture & retain marketshare. Can therefore expect Tanla’s percentage revenue share with the different brands to be varying (including MNOP who now get a significant share) based on the value they bring to the table - a game changer; collaborate initially to get volume to later compete on value

What role Tanla plays in the ecosystem apart from just being an orchestrator (network backbone/organizer) is something to be seen as the strategy evolves. However, with this strategy, one can expect the mgmt to focus on customer experiences/engagement, market dynamics and trends and operational efficiency, helping it build a good nest egg, which can be deployed later for acquisitions, if need be. Note that Tanla has already acquired some capabilities such as marketing automation platform, customer data platform (CDP) and recommendation engine from previous acquisitions.

The rapid pace of consolidation in the CPaaS industry might probabaly lead to only 3-4 global players in the coming years. From the annual reports, it seems Twilio has gone overboard on innovation (developer focus), burning cash with series of acquisitions, getting into adjacencies, and now facing the heat of competition. Sinch too seems to be on similar lines but better placed than Twilio.

An excerpt from Sinch’s AR “The variations in operator tariffs affect our margins. The cost per message charged by operators can be ten times higher in one country than another, which means that our gross margin varies significantly between markets even though we earn the same gross profit per message.” Both seem to be gaining marketshare and adding complementary offerings by way of acquisitions but at the cost of profitability and equity dilutions.

Below are some statistics from Morningstar: -

Finally, to assess the effectiveness of the ecosystem strategy, one would need to monitor the numbers for Tanla in the coming quarters/years with focus on sales growth (from existing and new customers), OPM/EBITDA margin, EPS growth, FCF, ROA & ROCE/ROIC.

P.S. This is not to be construed as a buy/sell recommendation.

Trading at 25X trailing P/E. FY22 sales and profit growth was 37% and 52% respectively.

According to management, " As you know, Tanla is single mindedly focused on the enterprises. And we are the market leaders in CPaaS. And that is really making the difference in our last year results. Our strategy is working very well. FY22 has been a phenomenal year on all metrics. And we achieved an INR 3,000 crore revenue milestone. We had a very strong revenue growth with best-in-class margins on cash flow profile. Revenue grew 37% year-on-year, gross margin grew 57% year-on-year

and we generated over INR 425 crore of free cash flow. And our cash balance

is over INR 20 crore. Our organic growth mission is in full flight. Our revenue and EBITDA has grown by 6x and 12x in the last six years. Uniqueness of Tanla is that while we grow like a startup, we have the balance sheet and cash flows of a market leader.

**As I look forward, digitalization is opportunity of this generation. We are seeing an explosion of the digital interactions in India. Transacting users have doubled in the last three years to over 200 million users, while digital clock has increased 3x in the same time. We are operating at the Rule of 60, which is aspirational Page 3 of 18 for most of the SaaS companies. We are pretty confident the momentum will continue.

Tanla’s underperformance continues to be a worry. There are few factors that needs to be looked at as we approach 25th July when Tanla will declare 1st Qtr results:

Typically Q1 has seen a de-growth from Q4 historically. However, in last 2 years Covid impact was severe in Q1. This time this factor is not there. Additionally Idea deal should also chip in. I would like to see a sequential growth in topline of atleast 4-5% magnitude. Unless they have lost some large business /account this should be feasible. This could perhaps help stem the negative journey and send it into positive territory to a decent level.

Tanla doesnt have cash in the parent company. Most of its income is generated in Karix and Singapore entity. This impacts its ability to either declare dividends or do buybacks beyond 60-70 crores. Tanla perhaps need to merge Karix with itself to partly address the issue.

Tanla ROCE will keep falling as it generates cash and sits on it. The cash in Singapore doesnt earn any interest either. Further Uday Reddy has declared multiple times that he won’t do acquisitions. Then what is going to be the use of cash sitting out in Singapore entity? That has to be addressed. I would rather they do a meaningful acquisition as valuations curently are low and could be best deployment of cash. Else pay dividends out of that company, incur income tax but get atleast 3/4th of that money into use - do buybacks, if you don’t want to do acquisitions.

It had last year mentioned that it will launch wisely internationally in Q4FY21. Then it moved the goalpost to Q2FY22 saying needs to make Idea successful and create case study. Idea in now live for nearly 3 months (29th April onwards) - hope they can come out with a clear blueprint of the international foray incl addressing - geographies, customer segments (carriers vs enterprise), teams etc. The entire charm and valuation beyond PE of 20x will depend upon this. I believe this has the potential to take its price to 5 digits over 5 years if it is successful. But first it needs to articulate in meaningful terms and investors (particulary Indian MF’s) to buy into that vision.

Truecaller & Kore.ai partnership - Truecaller was to go commercial end of June. So by 25th July it would have been commercial for nearly a month. What traction it has acheived in terms of actual volumes and pipeline of potential customers? Some quantification of that needs to emerge. Similarly for Kore.ai partnership - what kind of topline accretion can it potentially bring over 2-3 years?

Address issues of regulatory overhang - incl Nascom lobbying for app based notification instead of sms (which I believe wont happen quickly and when it happens, impact will be minimal as banks are not involved) and of consent management (this is upside to Trubloq business).

Overall Tanla leadership/management needs to acknowlege the fact that Tanla has fallen perhaps the highest in this meltdown. This is despite some very postive sounding announcements/actions including Idea & Truecaller which are both live now and Kore.ai. Also Uday Reddy’s guidance (sort of) implying 35+ growth (rule of 60, divide between growth and EBITDA as you want) is there. All this have done nothing to stem the slide. Topline sluggishness is one of the key reasons, which is where the 1st point (of this post) is very important. Perhaps even more imporant is that the Tanla story is not clear to larger investors and/or trust issues are there (legacy) - this is something Uday Reddy as founder and CEO needs to address directly and squarely.

Overall, CPaSS is an industry where Indian companies can transform themselves into large meaningful global players. Will Tanla be able to acheive that and move from good to great? Possibly yes. Would the current investors be able to enjoy that? - possibly yes, if management is able to articulate the vision in meaningful quantitative terms rather than adjectives. For example, (a) setting out a vision of when Tanla could acheive revenues of $1bn (b) setting out its quantitative targets for wisely international foray to investor community (just like it would be doing for employees)… Let’s see what all out of this is there for investors on 25th July.

Disc: Invested and highly concerned.

Agree with most of the points you have raised. The Tanla CPaaS story is clearly not understood by Institutional investors yet.

One correction - Management has indicated it will use the cash to do buybacks. As per SEBI rules a company cannot do a fresh buyback within 1 year of expiry of last buyback. So Tanla can’t execute a buyback before September. I wouldn’t want a growth company focusing on dividends at all. I would much rather the cash is used either in buybacks or better still in sharp acquisitions or partnerships.

Addressing the regulatory concern regarding in-app notifications vs SMS is of paramount importance and I hope this question gets asked in the upcoming concall. I will ask this question if I get a chance to ask it. As per the company response to my email, I am not concerned about this being a true threat, but clarity in concall is the best way to dispel this overhang.

If others here are significantly invested in Tanla, they should reach out with their questions to Tanla Management either in concalls or via emails to their IR team.

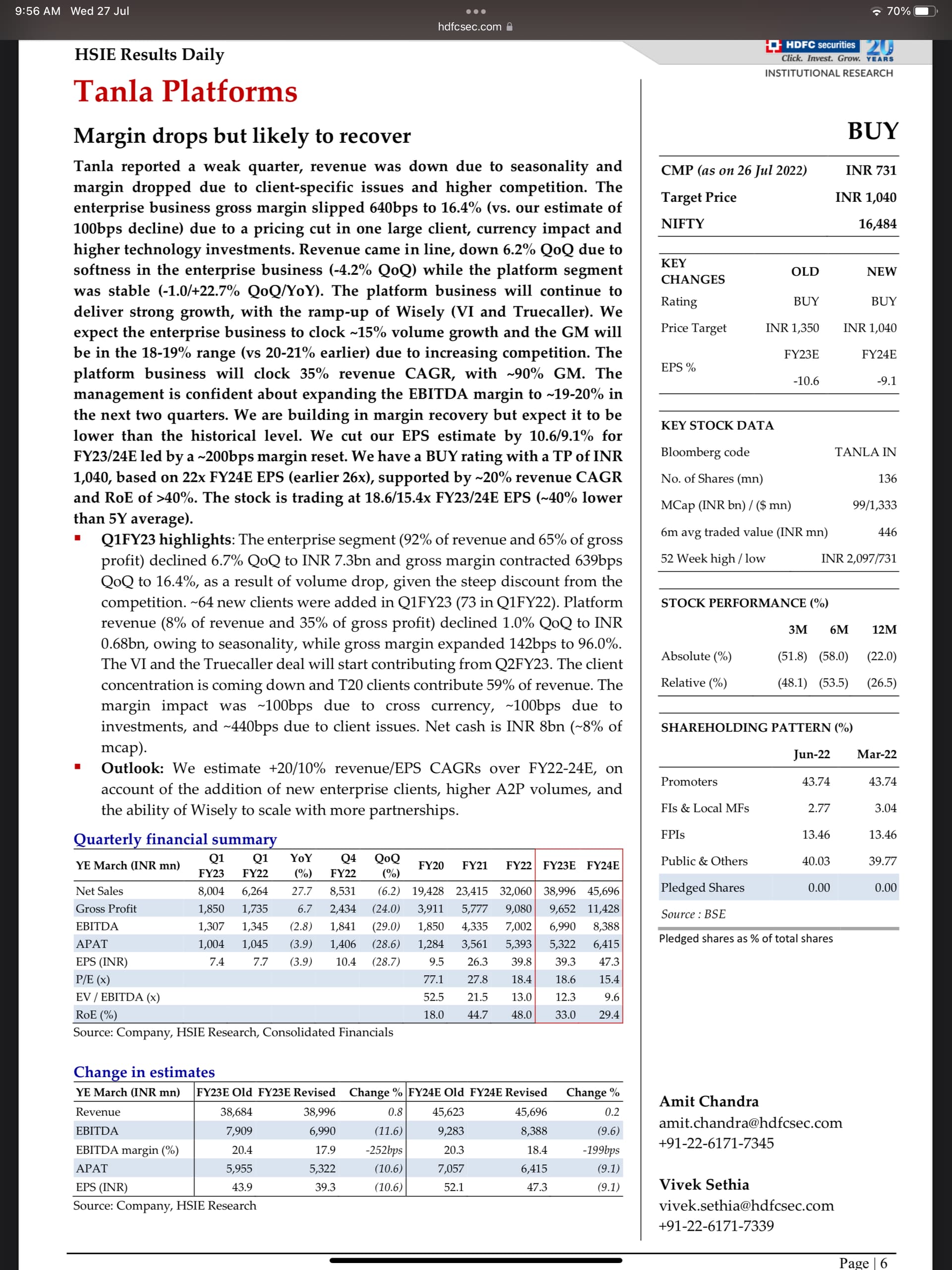

HDFC has significantly lowered its target price for Tanla in its latest update (Page 10 in attached report). That’s why one should never trust the pricing guidance in an analyst report - scan the report to find new information or insights but that’s about it.

India Internet - Path to profitability - HSIE-202207202034115322785_HDFC.pdf (1.3 MB)

They have quoted a Wisely potential revenue number of INR 2-3bn which is INR 200-300Cr. They haven’t mentioned a time-frame for this figure - whether its quarterly potential or yearly. I am not sure how to interpret this number. Also they are saying Wisely revenues are now pushed to Q2 instead of Q1. This conflicts with IR team guidance given to me as mentioned above.

Key questions for concall.

Losing wallet share is not good. However, the report does not mention about kore.ai which should provide incremental revenues.

This report paints a rather subdued picture, but there are important element in this.

As i mentioned in my earlier post, Tanla has huge potential but management has to be transparent and help investors understand the business and numbers better. My hopes for a 3-4% sequential growth are fading with the dip in wallet share of two large enterprise accounts.

I think that’s because Tanla took a much bigger share of DLT revenue when DLT was launched. If Route is handling a customer’s enterprise messages, the SMS traffic may still use Tanla’s DLT for scrubbing.

- Loss of wallet market share/accounts - 2 large accounts. See Route section in the same report and it says they have won one large bank and Amazon. Most likely Route has taken away these business from Tanla. Impact IMO 5-6% of topline, maybe 3-4% at EBITDA level. More worrying than this is whether this is all or it will happen in more accounts?

3-4% EBITDA decline based on loss in wallet share of 2 enterprise customers? Don’t you think that’s too much?

My hopes for a 3-4% sequential growth are fading with the dip in wallet share of two large enterprise accounts.

Yes, I will be happy if the quarter is flat Q-o-Q as Q1 is seasonally the weakest quarter. Expect EBITDA to be 20%+.

If that customer happens to be someone like HDFC Bank, SBI or ICICI or FB or MSFT, Amazon it can easily be. The volume of large Indian Banks is staggering. Each of them will be spending 150crore or more on SMS annually.

With respect to DLT it doesn’t matter. Airtel and Voda/Idea DLT is with Tanla, JIo has other partners. 100% of A2P business has to go thru DLT. So simply speaking Volume of A2P sms and DLT volume will be similar. The report also mentions Tanla is losing market share in DLT, which is possible as Idea is losing market share. Hence, A2P sms market grows x, DLT will be similar. The difference is not understandable by me.

This report mentions for Route - “To enter the DLT platform, the company signed a business transfer agreement with Teledgers to acquire the DLT blockchain platform. This will compete with Trubloq of Tanla in the SMS filtering and fraud detection space.”

But as far as I understand, Tanla has Trubloq deployed with Airtel and Idea. And DLT would be an exclusive deployment, meaning Route can’t deploy their DLT with Airtel right? So how will Route implement their SMS filtering and fraud detection?

Also, was there any update from Tanla about the strategy for Etisalat? I remember they signed up with both UAE operators last year, but no updates since.

I think Amazon entering CpaaS space is a worrying sign. They already have the cloud ecosystem and are developer friendly. Any insight how Karix manages developer integration?

The results are worse than I could have even imagined. Worse than topline drop is the margin erosion. This sets back the business by 1yr+ . It seems enterprise business is getting beaten up pretty bad not only from revenue perspective , but even more so by margin perspective.

Will understand better when investor presentation comes out. But these are first thoughts for now. Unless Uday Reddy gives an honest account for the business in call tomorrow, lots of investors are gonna foldup.

The recent dramatic drawdown and now the disappointing quarter!

I am afraid that possibly somebody else may be eating Tanla’s lunch.

“We are progressing well on our one platform strategy-Wisely. Q1 had some operational headwinds in the Enterprise business, but we have our building blocks in place to accelerate our momentum in the coming quarters. We have a strong balance sheet and excited by the opportunities ahead of us.” - Uday Reddy, Founder Chairman & CEO

“Market disruption: We saw market disruption of pricing both in NLD and ILD business in select customers which impacted our EBITDA. We have been quick to respond by taking an approach of making focused investments on our priority customers.”

Could somebody who speaks “management” decode this? To me, it appears competitors provided better pricing forcing Tanla to reduce their pricing? The usage of “priority customers” is very worrying. This means some big customers are bargaining hard on pricing.

If my understanding is correct, THIS SHOWS MINIMAL SWITCHING COST FOR CUSTOMERS- a definite negative for Tanla?

“From an internal perspective, we had some challenges in scaling our legacy infrastructure as our volumes have scaled substantially over the years.”

This is very worrying. Tanla keeps accumulating cash and does not upgrade infrastructure on a timely basis? Have they been boosting free cash flow at the expense of timely upgrade of computing infrastructure. Quite shocking tbh.

For now, my call is to sit tight. Will await Q2 results and take a call whether to REDUCE. I am afraid the stock will take a major beating in the coming days for sure.

Disc - Invested and hurting bad. Clearly, you should not take my words as

investment advice.

I’d recommend everybody to read into Tanlas previous bullish run. Some of it has been mentioned in the fraud thread at VP.

All things which tanla has right now, relationship with Voda, Brokerage reports with buy target, promoter open market purchases, cash on books, high growth, is what tanla boasted in the 2007 era. Many veterans on VP have made losses in it in the past.

Not saying they are fraudulent, but links to the current CM of Andhra are proven with the promoter.

Also read the forbes article on Dasari Uday Kumar Reddy, it seems off to me(as though it has been made to create a halo around promoter, speculating not sure how true what I’m saying is, just keep the tone of that article in mind)

Disc - exited a month back at minor profits.

Who do you think the real competitors are in the enterprise space?

The addition of new customers is still good. But for whatever promise the platform business shows it’s just 10-15% off the total revenues. It’s not going to scale up overnight. Hoping that Truecaller can be the start of better times ahead.

While you can see significant progress in our strategic focus areas, we have had operational headwinds in Q1. While our revenue grew 28% YoY in a seasonally weak quarter, we had pressure on our profitability. Our EBITDA and PAT margins are industry-leading even at Q1 levels, but it is lower than the levels we have operated at in the past. We have delivered 20%+ EBITDA for the past 5 quarters and that is the level we continue to aspire for. Our operational headwinds in Q1 is due to a combination of external and internal factors:

Market disruption: We saw market disruption of pricing both in NLD and ILD business in select customers which impacted our EBITDA. We have been quick to respond by taking an approach of making focused investments on our priority customers. We are confident that at the end of this cycle, we will come out stronger with our customers and be able to get back to better profitability systematically over the course of this financial year.

Legacy systems and infrastructure modernization: From an internal perspective, we had some challenges in scaling our legacy infrastructure as our volumes have scaled substantially over the years. We have used this opportunity to completely modernize our legacy systems and infrastructure to the highest standards. We had an impact in Q1 on EBITDA, but we do not see this impact going forward.

Forex impact: The sharp depreciation of the Euro against the USD had an impact on EBITDA.

More details here

Competitors - Route, Valuefirst (twilio), ACL (Sinch), Ghupshup & few others. Most of them have market share between 5-10% except Route - which will be higher now.

Yes, platform is less than 10% of revenues right now. However, accounting for 25%+ share of gross margin (this quarter it is 30%) and hence extremely revelant. A doubling of platform revenue (going from 10% to 20%) would mean adding 25-30% on Gross Margin. Truecaller will be a mix of enterprise and platform revenue I guess - but wont be sizeable in value terms this FY. India’s dialy volume of A2P sms is 1.5bn+, I think they are just targeting 1bn+ message for the 1st year (from Truecaller Press release) which will amount to 10-20 Crore topline. Key is wisely international rollout on which they are delayed by over 2 quarters now.

Concall Recording:

Important points from the ConCall:

Edit: More info here:

Please consider some points I might have misunderstood or missed add if any.

Comments: Market reaction is obviously based on their past, surely over reacting, Industry itself growing by 25-30%, massive disruption, unless management goof up, massive opportunity lies a head, with nearly 1000 cr cash on Balance sheet, EV value @ Billion dollar now, let’s c how route mobile results will be, bullish on Cpaas industry.

HDFC sec q1 update:

Disclosure: Invested.

Again I want to mention that Tanlas drop might not be a a pure market reaction to margin drop/biz pf.

Please read into the past.

Arre you flashing any corporate governance issues?