Looks like a case of Screener messing the expenses than anything else. The AR is the most reliable source to get this info and there 86/144 (60%) is employee expenses.

1 Like

With Twilio making headways into India market (more after acquisition of ValueFirst), Amazon chime, MS ACS etc and tons of other established players with deep pockets, many are investing to get a pie of the cpaas market. It seems to be getting crowded.

Unless there is unique value proposition, I wonder if Tanla will be able to retain/increase its pie of business, both domestic and international.

Disc: researching. Not invested.

Amazon chime, MS acs seems some video conferencing and communication services. Not Cpaas

1 Like

Interesting. Any idea of the current volumes on AWS and MS?

An interesting article on Uday Reddy published today in Forbes India.

2 Likes

853 Cr topline, 22% EBITDA and 10.35 EPS. That’s a 31.5% YOY revenue growth, 3.6% QoQ revenue de-growth and 37.5% PAT growth.

Tanla ends the year with INR 3206 Cr revenue and INR 546Cr PAT, YOY growths of 37% and 56%.

Vodafone Wisely commercial launch happened yesterday, so the expected 1 month delta revenue in March did not materialise. This and Truecaller should contribute healthily in Q1 FY23.

8 Likes

Great set of Q4 results on YOY basis. QOQ basis is not comparable, as Q3 has always been best quarter. FY 23 seems to be high growth phase with wisely coming into play along with new partnerships.

c04e148d-9902-4346-9e6b-13506e208ea2.pdf (708.8 KB)

Tanla, always surprises me with lots of detailing in unique ways. This time they are addressing the shareholders with this report.

aa740c6d-29f1-4d57-a618-8ccfe92f64c2.pdf (837.7 KB)

Discl: Invested at lower levels.

6 Likes

Hi, What do you expect as revenues from Truecaller deal on quarterly basis? What are the assumptions behind the same.

disc: I too am invested in Tanla and generally not very happy with management’s level of disclosure. Modelling expected revenue range (broad range) from Truecaller or Voda/IDea deal is pure guess work. I would be happy to have some of the guess work taken out.

Don’t think Indian acquisition of foreign players have done well. Perhaps Tanla and/or Route are taking market share away from them. No published data to substantiate this is available to my knowledge - so can’t be fully certain.

Hi,

Truecaller revenues are anybody’s guess at this point. Its a partnership for a new business i.e. Truecaller business messaging which I assume will directly compete with Whatsapp business messaging. I don’t think the revenues here will start out very large. I am also waiting to figure this out.

The Vodafone-Idea deal was announced as the largest CPaaS deal of its kind by Tanla in its announcement. Vodafone was already a customer of Tanla’s but Idea wasn’t. So I expect good incremental revenues to come in from this deal. Quantum of revenues - have to wait and watch, not clear to me yet.

What is the issue with disclosures? I believe Tanla’s disclosures have improved by leaps and bounds over the last few quarters and their quarterly presentation and shareholder communication is some of the most detailed I have seen out there.

6 Likes

The management dont see any acquisition opportunity, but have a lot of cash on the books. If they haven’t declared any dividend or buyback in this quarter, what’s the plan with the cash?

Disc - Invested in small quantity

The management has clearly said in a number of calls that, they intend to re-invest the cash in expansion of platforms and new products. They do not want to do acquisitions for numbers. Btw; they have declared a final dividend of 200% in Q4 and hope the same trend to continue in the coming years.

2 Likes

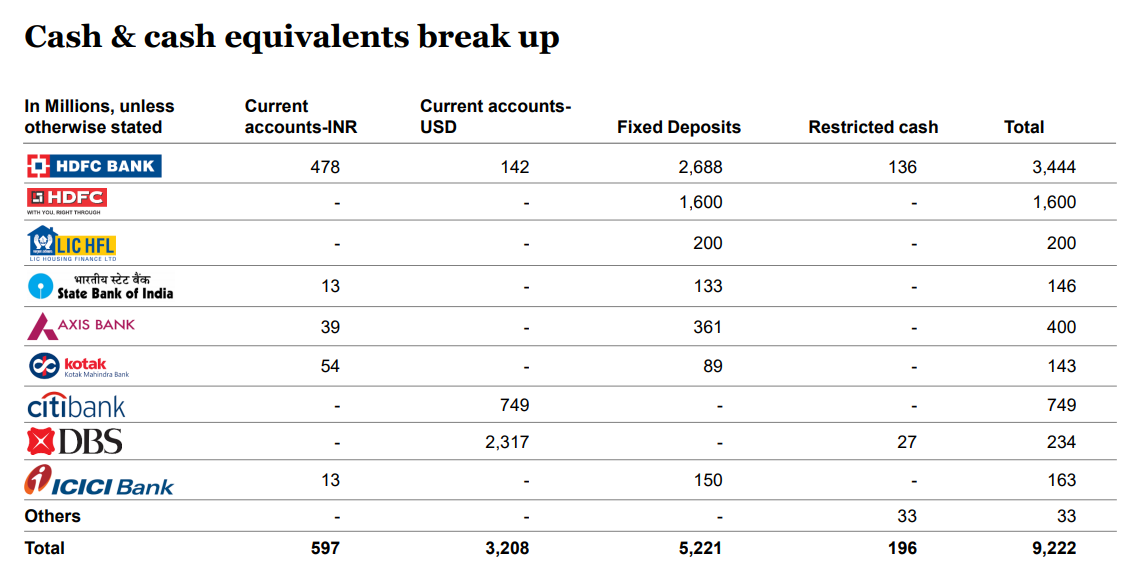

Wow…Have never seen any co. being this transparent interms of what they are doing, how the money is being invested, customer breakup, revenue breakup, etc.

They have even shared the CCE breakup - Which bank and in what currency…Truly Inspirational. This gives more confidence in the management and the corporate governance of the co.

Complete Presentation Link -

Discl. Invested & Biased

7 Likes

This indeed is impressive. But I still cant get my head around the fact that same management completely wrote off their platforms in 2020.

I dont know how to take that. Did they wake up one day and said “we are just trash, lets just buy Karix”?

400cr of platforms completely deprecated in one year. This is strange. Although I think the management is now in an overcompensate mode and trying to be really transparent.

4 Likes

This indeed is impressive. But I still cant get my head around the fact that same management completely wrote off their platforms in 2020.I don’t know how to take that. Did they wake up one day and said “we are just trash, lets just buy Karix”?

Indeed. And this is the reason many people stay away from the stock and the stock trades at a low 32x multiple even after delivering incredibly strong revenue and profit growth for the last 8 quarters in a row.

An investor can either believe that a company once tainted is never to be touched again or he can study the company and its management and gradually build conviction on a turnaround story. There’s no right or wrong with either approach.

Tanla management wrote off their legacy platforms in view of TRAI’s requirement for blockchain enabled platforms. Unfortunately, they did not do concalls at the time, so the only source of info. regarding why they chose to do what they chose to do is in the AR. And that’s also not much. My interactions with long term Tanla holders (Holding since 2010) is that indeed Management indeed decided to purge its old missteps and sins and embark on a fresh journey as a CPaaS company. It acquired strong, development focused companies and decided to build platforms to take advantage of the upcoming CPaaS revolution. And no matter how you perceive the previous faults of the Management, their execution since then has been top notch.

The way I see a company with a chequered past is to see the quality of its disclosures and the quality of cash held in the balance sheet. Both seem satisfactory for Tanla as of now. So, given the above comforts and at close to 30x valuations, I am reasonably comfortable discounting the past sins.

Regarding present price action, its not looking pretty for Tanla like many other IT stocks. Stock is below 200 EMA. People who believe in trading based on technical signals may want to book profits, exit and re-enter at lower levels etc. Or just hold on and ride the storm. Fundamentally nothing’s wrong with the business, its just that the liquidity environment and risk perception has changed wildly in a matter of weeks.

10 Likes

Go through the Q3 concall. Share buybacks are definitely part of the plan. As per SEBI rules, they can’t execute another buyback before Sep I think. So I am expecting buybacks after Sep if price remains depressed (Which, given the current bearish atmosphere, it may well be).

They may make acquisitions, but not horizontal ones that some competitors are making. They will make vertical acquisitions only which can be margin accretive. Uday Reddy has said consistently that his goal is to improve the gross margin of Tanla to bring it closer to global peers. Hence the focus on platforms.

3 Likes

Yes management is actually being very transparent. Their investor presentations are of the most detailed ones.

Also when someone in latest concall asked for trubloq volumes, the management said that they will get back regarding the same. The company then promptly filed a new investor presentation with the exchange highlighting trubloq volumes, in a matter of couple of days.

They do seem like overcompensating for the past but either way it bodes well for us investors.

8 Likes

I don’t understand if blockchain really provides some value here or it’s just TRAI on hype train forcing vendors to do the same. In my view, private centralised blockchains are no better than old fashioned databases.

Sure it does the job, but one needs to be cautious to attach additional value to the product just because it’s blockchain based.

1 Like

Hi,

Yes, the level of communication has gone up significantly and appreciate that. However, there are issues in my opinion (and most companies suffer from that ). Lets say for example Idea deal - launch was delayed by two months … Not a word on it. Secondly, they could have explained for shareholder benefit how the deal works. Whether it’s just revenue share from the platform deployed , or will they get the enterprise revenue also? This itself is a 1:6 or more kind of topline difference. Competitors know anyhow - Large investors with direct connection will know - question is how well you inform smaller investors who rely upon the quarterly or other interim disclosures.

I believe Tanla has to take this small leap, to ensure investor confidence stays, irrespective of whether the last quarters result are good or not so good. And this applies to most companies.

1 Like