Interesting business. just looking at the balance sheet and income statements in screener, looks like a solid business but with not a lot of growth in the last 3 years. A lot of money is spent on giving back in dividends and buybacks (which should have propped the stock but didnt?!) Looks like a cash generating business with not much upside in revenue as growth has plateaued and company is not ready to invest in additional tech/innovation/acquisition? PE is 22’s.

Confounding! Am i missing anything?

3 Likes

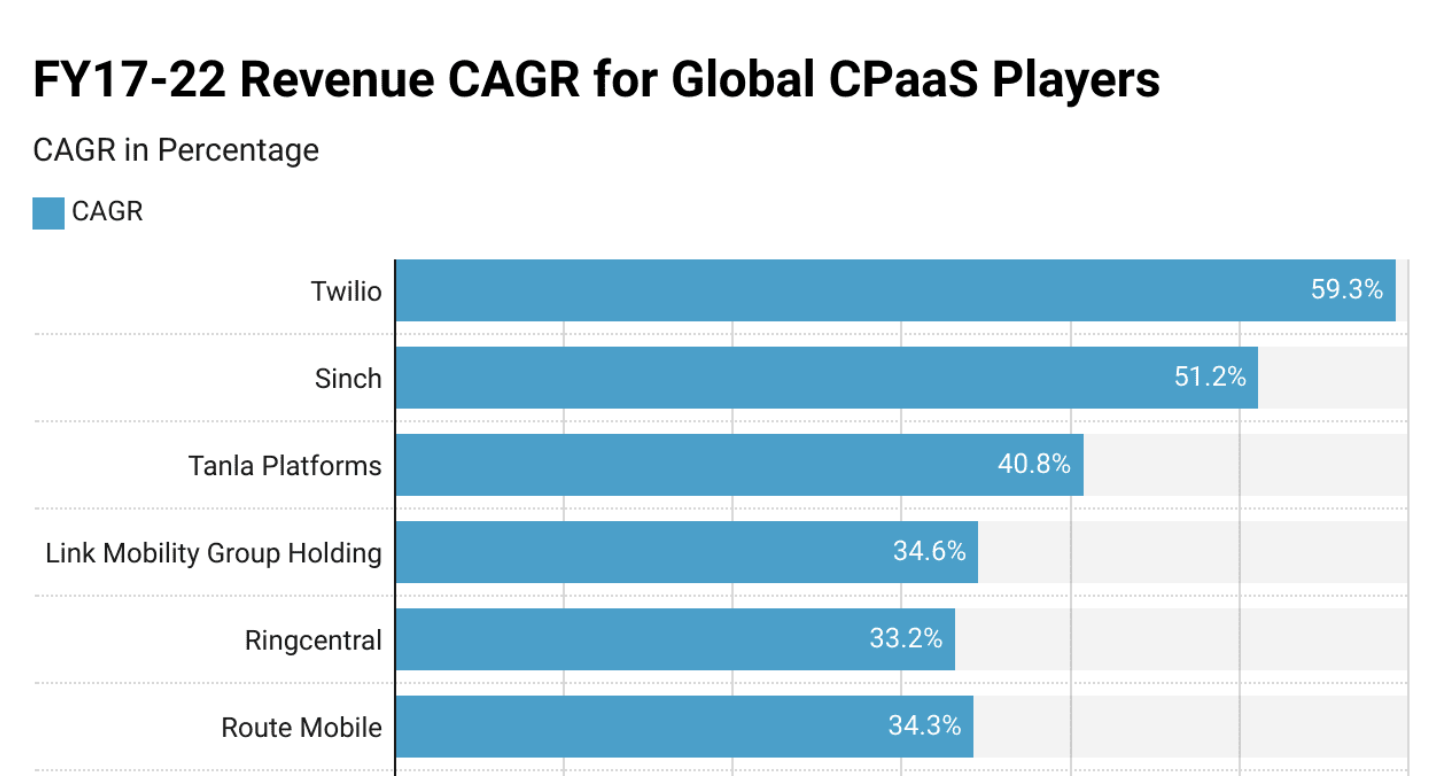

Digispice is the company which own them and this is what they mentioned in May’23 earning Call in the CPAAS space , Which highlight the competitiveness and Customer sticky ness.

The things we realized during COVID specially, is that a lot of

companies, the stickiness of large enterprise customers to their CPaaS platforms continued.

So, we saw very little churn happening and every time someone went in with pricing as an

option, the existing vendors match the pricing to cool down to the customer. We also saw

global players in CPaaS enter the space and acquire some of the domestic companies. So, we

saw a lot of M&A activity as well. Net net, we realized that the CPaaS space was a lot more

competitive than we thought it was.

1 Like

@Anna, I wanted to ask who the DLT partners are for Airtel and Jio, similar to Tanla for Vi. Do you think the URL whitelisting rule will help Tanla gain market share, especially with the rush to register URLs? Also, it seems like funding in the sector has dried up, which I think might be a good thing—what’s your take on that? Lastly, do you think Airtel will have an edge over OTT messaging, like they do with SMS? I feel the market is going to shift dramatically from SMS to OTT, and India seems like a massive opportunity—for instance, WhatsApp has the most active users here. Too many questions, I know ![]()

1 Like

Tanla has more questions than answers. ![]()

Airtel is 2 partner in DLT incl Tanla. Jio is insourced/tech mahindra.

URL whitelisting - no i don’t think it increases market share. On the con call you should ask if it increases revenue ?

Airtel will have edge in SMS and maybe RCS. Rest no.

SMS to OTT will happen for marketing and Airlines. Rest bank transactional , OTP etc really no. There is no incentive to shift.

Tanla should lay out for shareholders the impact of regulatory changes. These questions should be asked on con call.

3 Likes

Thanks for the reply, Anna! Haha, there are definitely a lot of questions to ask in the conference call.

I see Tanla as a ‘Buffett-style’ business, if I may say so—it’s currently facing some industrial headwinds but has strong cash flow and an agile management team. They have a solid moat, at least in the platform side of the business, with offerings like Trubloq, ATP, and Truecaller. I recall from one of the previous calls that they mentioned having the lowest costs among peers in the enterprise segment and that they continue to invest in technology. Even in tough industrial conditions, their market share has risen. As the platform business becomes bigger, eventually their margins will increase, don’t know when though.

Of course, there are some concerns—things keep cropping up. Recently, it’s been the issue with ILD pricing and I hope they are able to diversify to other countries.

Btw, I think that they’ve signed BSNL onto their ATP platform. Just guessing it is with TP, because it mentions “before they reach you” and Mr. Bajpayee retweeted it. BSNL has around 9cr subscribers, which is slightly lesser than the number of customers of HDFC bank.

3 Likes

There’s no need to react to every piece of news. As a long-term investor, it’s important to focus on the bigger picture rather than getting caught up in short-term fluctuations. A marginal decline in quarterly year-over-year profit should not cause concern if the company’s fundamentals remain strong.

Remember, successful investing is about patience and conviction in your strategy. Long-term wealth is built by staying committed to your investments and not being swayed by temporary market noise or minor setbacks. Keep your eyes on the overall growth trajectory of the business.

6 Likes

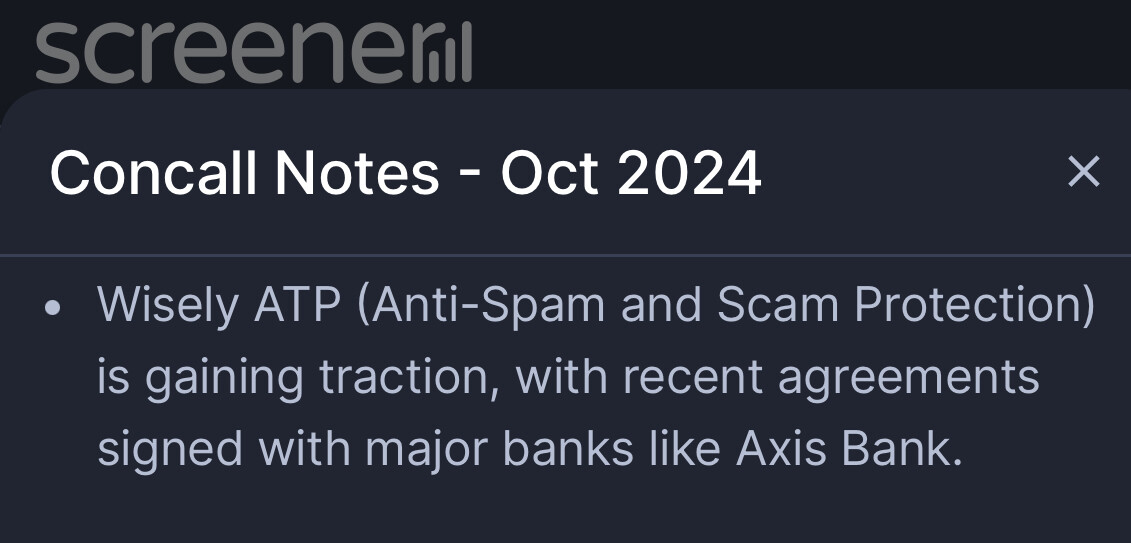

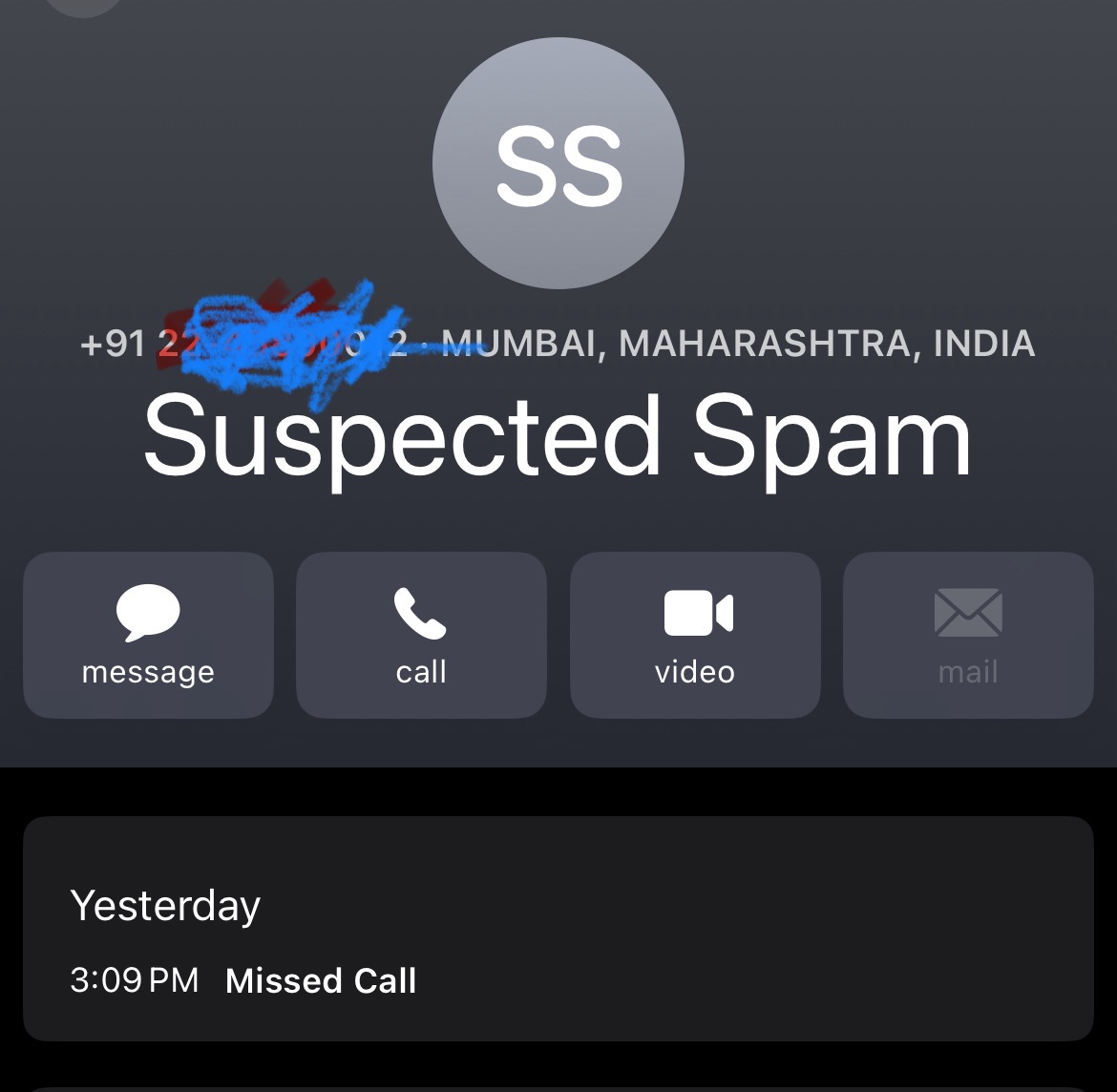

One Very Interesting thing to note in Tanla Concall -

- Airtel Lanuched its own Anti Spam

- Received a call, (Airtel Sim) showing potential Spam - Did not lift

- Tanla - is the first to recognize this problem and worked a solution - ATP

- Slowly onboarding customers especially banks

@anna Any insights how Big is this Opportunity, in India and Globally??

1 Like

I don’t think that is positive for Tanla if Telcos start rolling out such Anti-Spam, Anti-Phising solutions, correct me if I’m wrong.

4 Likes

The biggest con which is why I believe both Tanla and Route don’t have a durable moat is that large clients(at least the ones that have only domestic business like banks etc) will start integrating with Jio and Airtel CPAAS directly.

Jio and airtel combined have 70% + market share. So for any large client(and even smaller clients that later become large) it will make sense to make that one time investment to integrate it with Jio and Airtel CPAAS directly as it will be more reliable(reduces end-to-end latency and makes it easier to track message delivery status) and cheaper.

5 Likes

Well I think this is exactly why I think both tanla and route will thrive, here is my view anyone who opts for jio or airtel knows that switching cost will be higher and they cant use other modes ,

First problem I see is that, Not everyone uses jio, or airtel , now that BSNL is throwing their hat in the ring,

Second, if at all anyone who is having better distribution it’s Whatsapp rather than JIO or airtel, companies seems to move towards liking of OTT messaging

However, due to regulatory approvals we need to use SMS for banking transactions and stuff, since whatsapp if the whatsapp is down for few hours it ll lead to chaos and its single point of failure, so companies wont be willing to reduce this risk

Third, for International Long Distance messaging, you still need to rely on them,

Who can do all these things ?? It’s Tanla, and ROUTE, when you have the established solution already (switching cost and features built around it like analytics and customer segmentation, engagement, security etc.,)

Well whether Jio and airtel can build their own CPaaS vertical and extend the same sort of functionality to others or not is the matters of their long term strategic vision.

If at all , you call this as sunset industry then it will be due to OTT messaging apps such as whatsapp not from jio or airtel.

the real risk/downside I see here is

- Free R&D Labs for OTT Platforms:

- CPaaS platforms take on the risks and costs of innovation, while OTT platforms cherry-pick successful ideas.

- Commoditized Middlemen:

- Over time, CPaaS platforms lose their ability to differentiate as OTT platforms build similar tools natively.

Well this could take quite longer, honestly, enterprises don’t change their vendor often. But growth will be difficult,

TLDR;

Telcos building their own CPaaS isn’t a big threat because:

- Network Lock-In: Businesses integrating with one telco (Jio, Airtel) are stuck with that network, losing flexibility. CPaaS providers like Tanla and Route already offer multi-network solutions.

- Global Messaging: Telcos can’t match the global messaging capabilities of CPaaS platforms, which would take them a lot of effort to replicate.

- OTT Threat: The real risk is OTT platforms (like WhatsApp), which already dominate user bases and are expanding enterprise solutions, bypassing telcos.

So, telcos won’t easily replace CPaaS providers, and the real disruption comes from OTT.

Disclosure: Not invested, Tracking both Tanla and Route for potential investment in this over heated market currently, Tanla seems to be good candidate for further study in valuation comfort front and no debt , but ROUTE promoter has increased their shareholding recently too and profitability front with substantial debt

3 Likes

The real challenge for telcos building their own CPaaS is the need for multi-network integration, which is exactly what Tanla and Route have already mastered.

To build a true CPaaS solution, telcos would need to integrate multiple telecom networks (domestic and international), OTT platforms, and other messaging channels into one unified system. This requires significant technical infrastructure, partnerships, and constant updates. Tanla and Route have spent years developing these integrations with hundreds of vendors across various networks, ensuring seamless communication across platforms.

For Jio or Airtel to replicate this, they would have to work with numerous other telcos, implement complex APIs, and manage cross-network issues—a process that’s time-consuming and costly. Moreover, it’s not as simple as just offering a messaging service over their own network. They would need a platform that supports global messaging, interoperability, advanced analytics, and customer engagement tools—all of which Tanla and Route already offer.

Thus, it doesn’t make sense for telcos to replicate the CPaaS model that is based on integrating multiple vendors and messaging channels. They would essentially be reinventing the wheel, and it’s a massive investment with uncertain returns. CPaaS providers already have the experience and infrastructure to offer a truly integrated solution, something telcos would struggle to achieve without years of investment and effort.

2 Likes

The CPaaS (Communications Platform as a Service) industry in India is experiencing significant growth, with the market expected to reach a size of $2.46 billion by 2029, growing at a CAGR of 24.83%

Tanla and Route even if they conservatively grow their top line, with the effect of platform mix, the margin should expand, available at reasonable valuation with the possibility of rereating if the growth comes back and with 700 crores of cash they have lot of optionality especially since they don’t have any debt unlike ROUTE

Everything hinges of execution, if they execute decently, given the sector growth, this should be multibagger, the risk reward is quite favourable for a cash rich company , even conservative 20-25PE would be a good investment

However there is always a reason why a company get derated by the market so needs to monitored QoQ closely

(Given the market condition this seems to good bet at current levels)

Disclosure: invested , small position

4 Likes

It is puzzling that DIIs (Mutual Funds) who have been buy small caps and illiquid microcaps left and right have somewhat ignored this company despite it having a good float. Should we be concerned or should we consider it as a sign of being early?

"When you locate a bargain, you must ask, ‘Why me, God? Why am I the only one who could find this bargain?’” - Charlie Munger

1 Like

CPaaS growing around 25% CAGR for next 5 years is huge.

Why is tanla and route not able to capitalize this growth is something to ponder. Even the management refuse to give guidance.

Is there something we are missing, because these companies should already have benefitted from the sectoral tailwinds. Also listening to concall doesn’t instill confidence about growth.

2 Likes

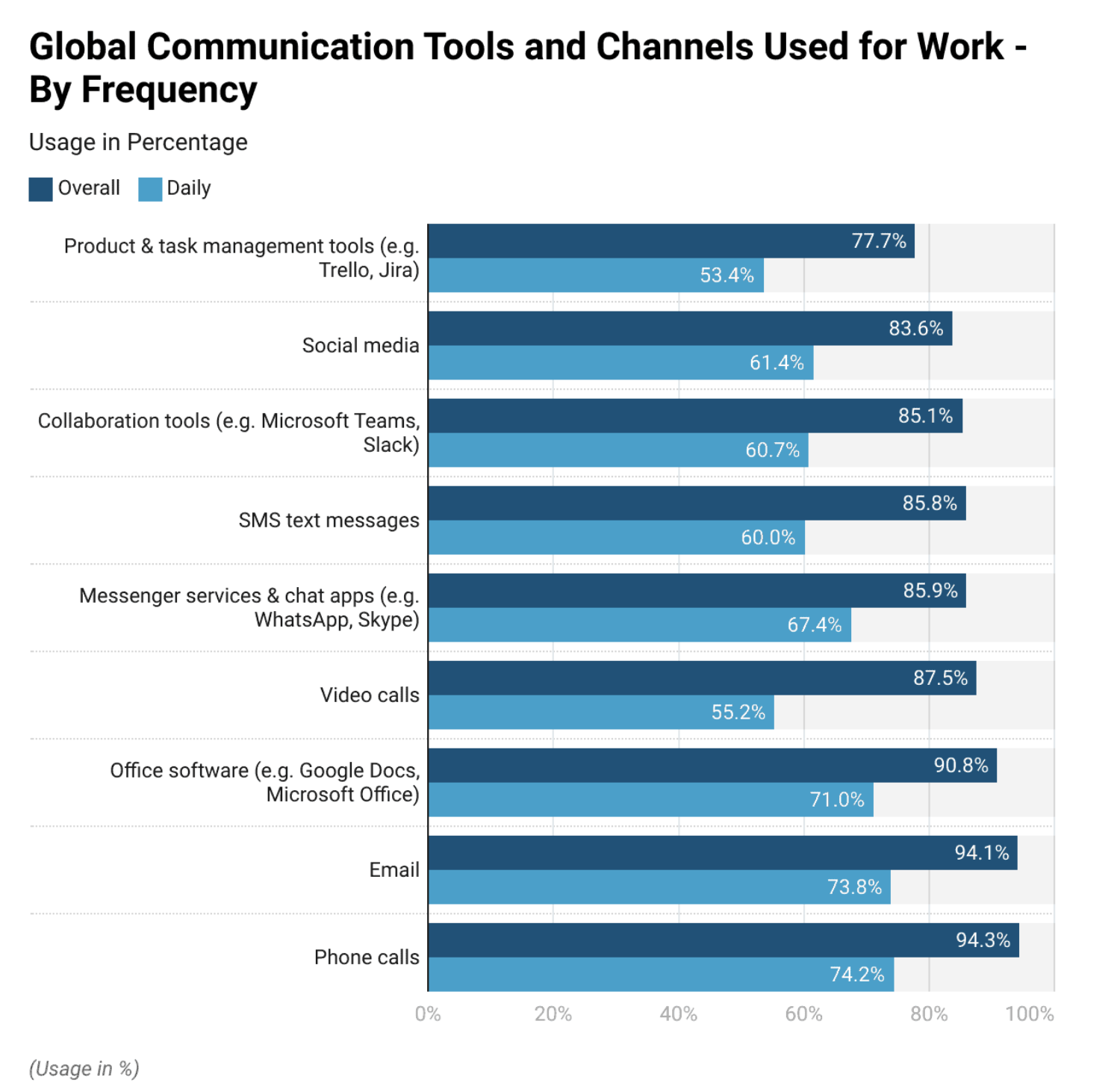

Channels and Frequency:

End user industry wise

Here comes the major answer for your question in my opinion

Technology Segregation:

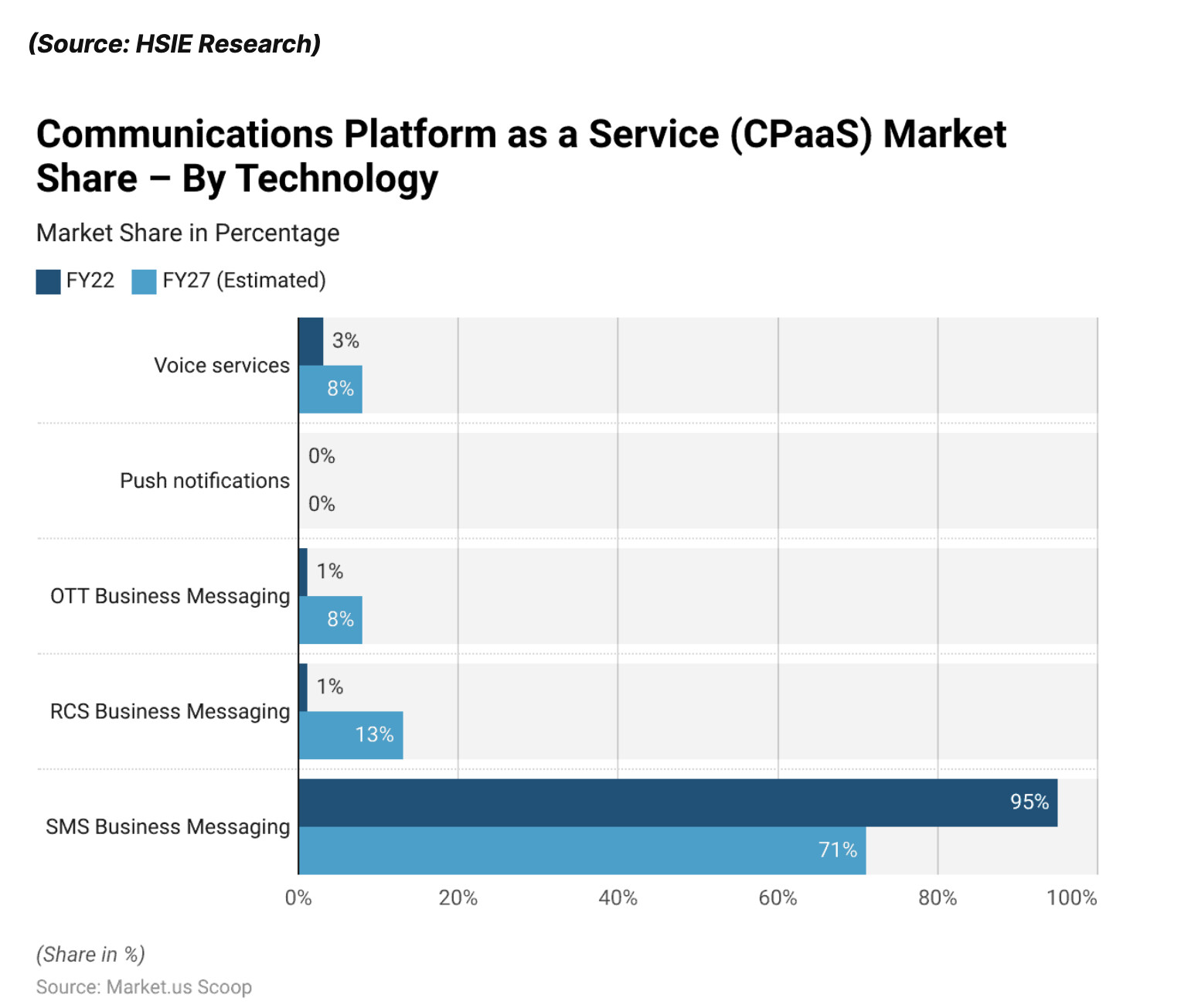

See Tanla and Route Combined made almost 8000crores of revenue which almost a $1 Billion, so that’s inline with the current market size of CPaas in India $0.89B , however the slowdown was attributed to the technology graph, if you see the SMS is on downward trending, both are now Focussing on High growth sections such as OTT, and RCS, however they are bit slow in adoption, tanla has better edge over ROUTE in this facet, they are going through product innovation route

Twilillo the largest global player recent acquired data analytics platform for next lever of growth, Tanla is focusing on in-house products in this catg, ROUTE choose to go via integration route of these tools built by other players.

TLDR;

The growth muted due to SMS trend is declining and the revenue are kinda inline with market size, however the newer segments are not right to win, they need to execute well in other segment such RCS (Google’s largest global RCS (Rich Communication Services) platform partner and has been recognized as Meta’s Growth Partner of the Year for the second consecutive year),

My thoughts:

I think tanla must be working on a propieratory product where communicating it in concall might affect their growth chances or they might struggle with product market fit.

Definitley there seems to competitive intensity in this sector now from smaller player it seems, however both tanla n ROUTE has lot of cash in their books for inorganic growth if needed,

All in all, we should get more clarity in which direct this company gonna in one or 2 quarters but by then if things are positive , we wont be getting it cheap. so in my opinion if there is no issues in terms of corporate governance both Tanla and Route Poised for growth to become multi baggers

Route has been optimistic in their growth outlook and given the new promoters Proximus group give me more confident on them

Tanla refused to share any future outlook, this could be due to launch of new product which they don’t wanna give away before getting first mover advantage since they work closely with TRAI (regulator), However they could be burning cash or genuine concerns on scalability or some other internal issue that may hamper them , i am not sure what it is, but i think the CMP factored those too. Still i can fall further too until they start showcasing for growth for few quarters, (Historically, thy had traded at 8-12 PE for almost an year so i m cautious on position sizing)

Disclaimer: invested in both companies less than 1.5%, as the market is now wobbly, I am looking to increase the allocation heavily to 8-10%(given the tailwinds and cash, debt free) as i build further conviction on the management and clarity on current hesitation by management

10 Likes

My Viewpoint on Airtel and Jio (telcos) entering/providing their own CPaaS solution:

So here’s the thing—telcos getting into the cPaaS game might look smart at first. They own the networks, so you’d think they can cut costs and maybe even kick off a price war to grab market share. But honestly, that so-called “advantage” doesn’t hold up. No single telco can cover all customers, and enterprises don’t want to lock themselves into one network. They need solutions that work across multiple networks, handle ILD messaging, and integrate with platforms like WhatsApp or RCS. Telcos trying to offer that would just be reinventing the wheel, which is both expensive and complicated.

Plus, let’s not forget BSNL. There’s talk of them getting back —they’ve got government backing and a strong rural presence. But for now, it’s more noise than reality. Unless they seriously step up their game, private players like Airtel and Jio will stay ahead.

At the end of the day, even if telcos improve their networks, it just ends up helping companies like TANLA and ROUTE. These guys create a layer over all the telcos and offer a simple, unified product that enterprises actually want. Telcos should stick to what they’re good at—networks—and leave the enterprise solutions to the specialists. It’s a win-win for everyone if they get this right.

Both Tanla and Route are poised for growth, although ROUTE seems to be just an integrator, TANLA wants to be innovator(which comes with its own peril). It may or may not test the patience further of existing investor, But I believe both will makeup for the lost past half decade of the investors, especially TANLA if the experiments on the platforms works out,

Disclaimer: Invested in both companies(Feel this is gonna be Oligopolies industry in India), looking forward to increase allocation incrementally

5 Likes

This is my first post on ValuePickr, and I welcome any feedback or suggestions. I strive to ensure that I adhere to all community guidelines and rules, and appreciate your support in helping me align with the group’s standards.

Over the past 11 years, Tanla Platforms has demonstrated remarkable growth, with revenue increasing by 34x and operating profit rising 65 times. However, we are currently seeing a period of stagnation in both revenue and profits over the last four quarters. This is not uncommon in Platform as a Service (PaaS) businesses, where growth can be cyclical.

Looking ahead, the next phase of growth for Tanla could follow a similar trajectory. PaaS models typically have low variable costs per new customer, which positions Tanla well for scalable growth. Moreover, the company has a proven track record as an innovator in this space.

Tanla Platforms currently holds a 35% share in the CPaaS market and boasts 5 patents, allowing businesses to integrate real-time communication features into their services. This strong position in the CPaaS market further strengthens its growth prospects.

As mentioned by @dark_hunter as well , once growth becomes more evident, it is unlikely that Tanla will continue to be available at such attractive valuations, especially considering its PEG ratio of just 0.19.

In my experience, the current market sentiment has been impacted by the company’s cautious management commentary, which, while prudent, may have contributed to the decline in share price.

That said, several factors support a positive outlook for Tanla:

- Strong Financial Position: With cash and cash equivalents exceeding ₹500 crore, Tanla is well-positioned for inorganic growth opportunities through acquisitions.

- Impressive Profitability: While quarterly revenue and profits have stagnated, the company still reported a net profit of ₹542 crore over the last 4 quarters. Notably, fewer than 40 companies in the Indian stock market have an annual net profit of over ₹500 crore, with a market capitalization under ₹9,000 crore.

Additionally, Tanla continues to work closely with TRAI to secure necessary approvals, which could further enhance its growth prospects.

Disclaimer - Invested in Tanla around 2% of entire portfolio, might increase allocations with any positive fundamental or technical cue.

7 Likes

Is this statistics from screener? Could you post the list please?

2 Likes

Yes indeed @Sudhakar_Subramanian, this is from screener. I keep on building different screens. Below are the screenshots of these 39 companies including Tanla Platforms.

The query I ran on Screener was as following:

Market Capitalization < 9000 AND

Net profit preceding 12months > 500

Hope this helps.

7 Likes