@Rahul_Monkvestor you are essentially screening for PE<18 ( which in today’s day and age will mostly give you cyclicals, financials or companies which may be struggling for some temporary reason or just bad companies (and which the market judges as bad).

7 Likes

Agreed, @basumallick Sir.

The point I was trying to convey is that a platform business, particularly one in the rapidly growing CPaaS market (projected to grow at a 20% CAGR, as shown in the attached snippet), at a P/E ratio of 16.8, can typically only be available when growth has temporarily slowed down.

Furthermore, Tanla holds a 35% market share in CPaaS, and with the market size expanding, I believe it may be a strategic decision to invest in the sector leader. This is why I allocated 2% of my portfolio to this company. I will only consider increasing my investment if there are positive signals, either fundamentally or technically.

As for the list of companies I shared, my intention was to highlight those that fit the category of beaten-down stocks due to a subdued outlook in their respective industries. In contrast, CPaaS is a sector showing strong growth potential.

These are my personal insights based on my research, and I welcome any differing opinions or thoughts.

I also encourage any feedback or suggestions regarding my posts. I am committed to adhering to all community guidelines and appreciate your support in helping me stay aligned with the group’s standards.

Disclaimer - Invested in Tanla around 2% of entire portfolio, might increase allocations with any positive fundamental or technical cue.

2 Likes

Trai’s mandates Telecom companies in India for voice and SMS-only tariff packs

Telecom Regulatory Authority of India mandated that the trail of all messages from Senders/Principal Entities to Combat Spam Calls and SMS

TRAI issued Direction on 20th August 2024 and mandated that the trail of all messages from

Senders/Principal Entities to recipients must be traceable from 1st November 2024

Principal Entities opportunity

Principal Entities (PEs):

Principal Entities are businesses or organizations that send promotional messages to consumers. These include:

- Banks and financial institutions

- E-commerce platforms (e.g., Amazon, Flipkart)

- Government and non-government services (e.g., utilities, public health services)

- Telecom providers themselves (e.g., for their own customer notifications)

- Insurance companies

- Education and coaching institutes

- Retailers and brands

- Political parties (for campaign messages)

- Advertising agencies

Trubloq - Blockchain-Enabled Spam Protection

Wisely ATP - Anti - Phishing Platform

As far I researched no one has this capability yet except tanla, they have been proactive on this, positive news.

It seems everything is good for tanla, if they deliver good results in upcoming quarters, we should start seeing the upmoves this counter deserves

@nirvana_laha your current take/commentary will be appreciated, looking forward to it , thanks

Disclaimer - Invested in Tanla and ROUTE, trying not to be biased

7 Likes

Does someone know if the digital platforms business is under standalone entity or under one of the subsidiaries? If in a subsidiary, which one?

Hi,

Any reason behind the deep correction?

Yes, the topline hasn’t improved for over a year however the PE still seems rather low. For a growing industry like CPaaS with a fair technological moat, I would expect a better PE.

Disc: invested and tracking

1 Like

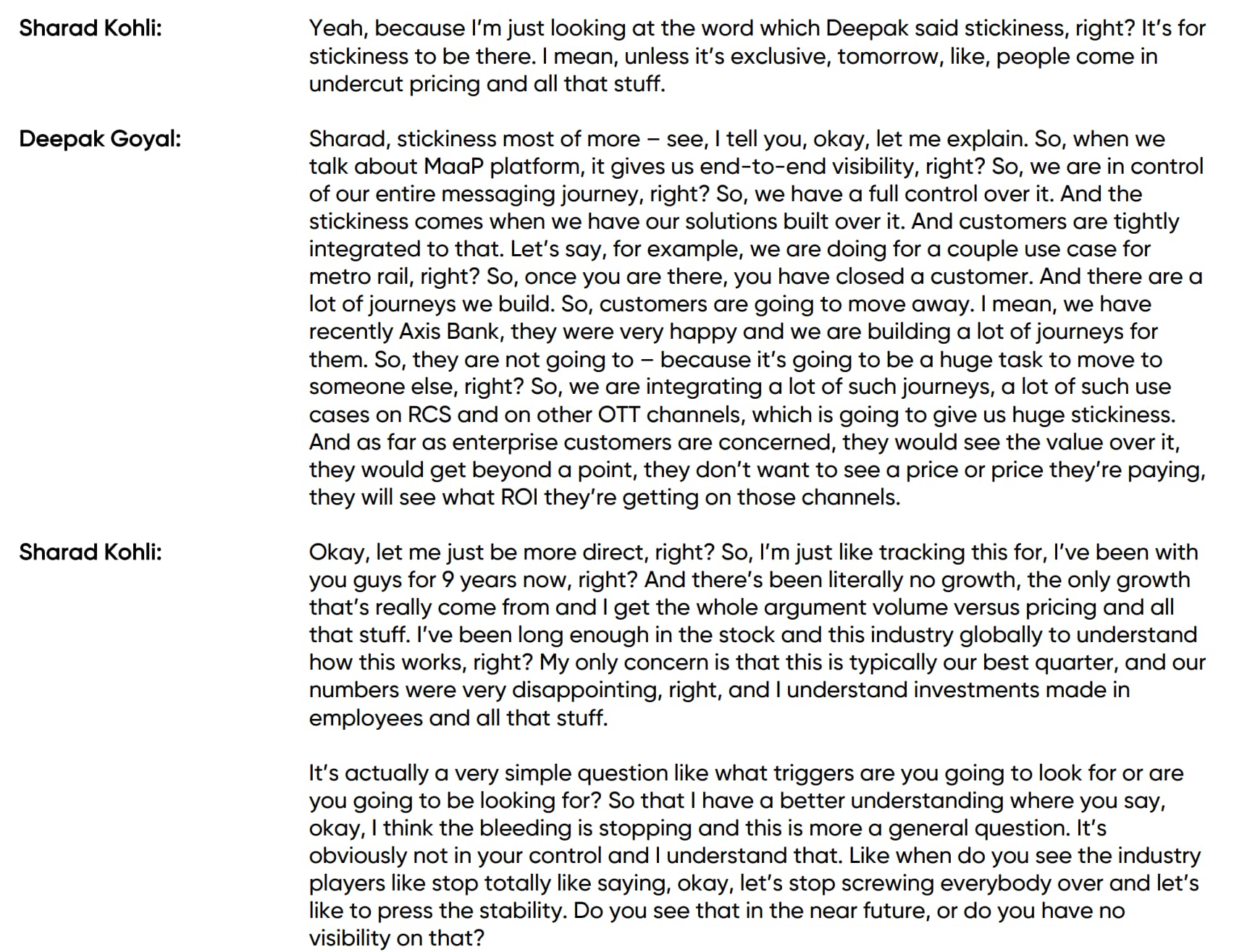

I think in the recent concall the management was asked some tough questions. May be the answers from the management are not satisfactory. Please go through the concall once

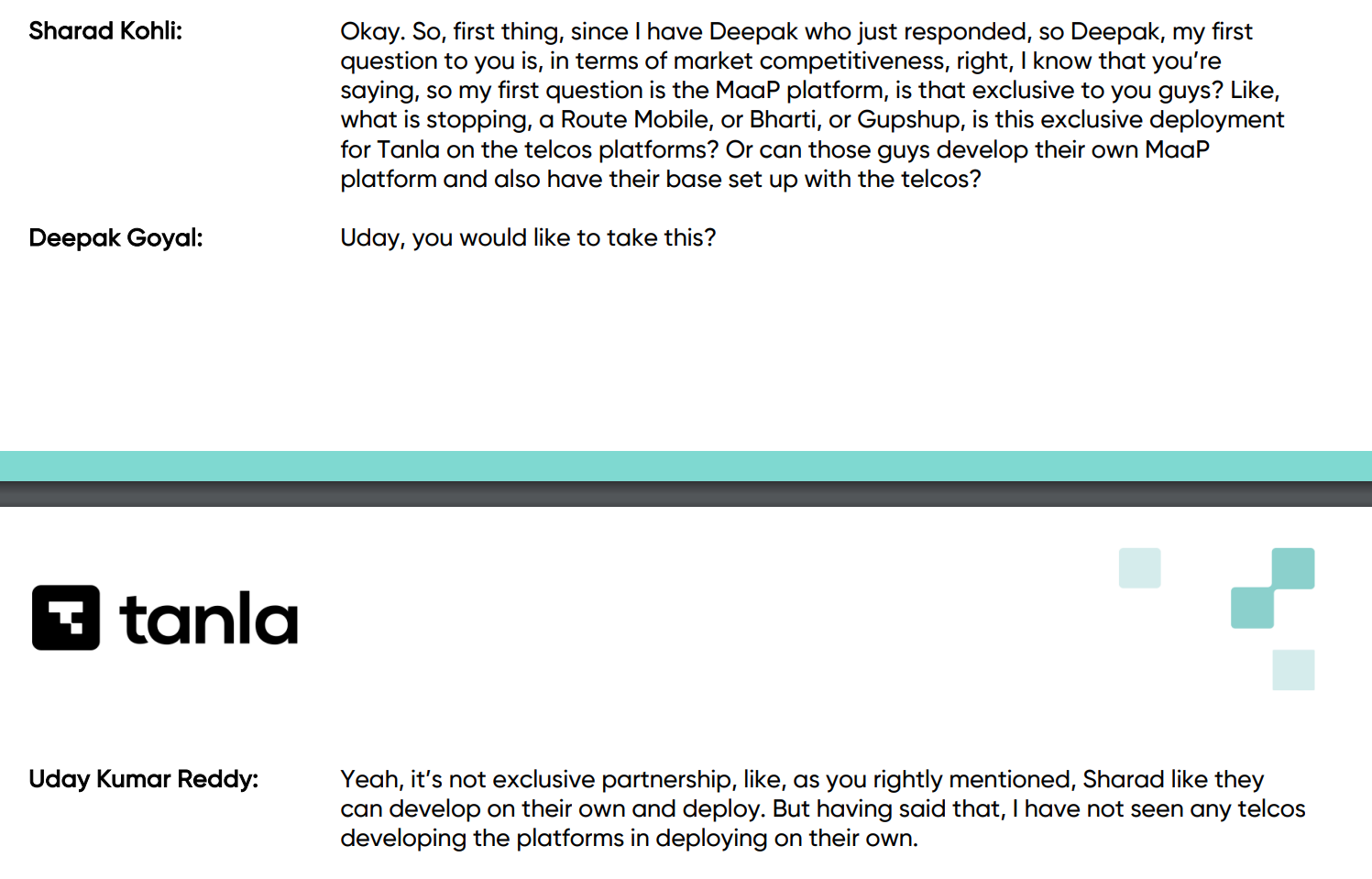

On MaaP Platform:

There are few more. May be because investors are thinking the lack of clarity on growth. I think to be frank it is trading cheaply now. But have to check if there is still a value in future or is it trading cheap because it ran too much ahead anticipating too much growth.

Any other thoughts are welcome. Still studying and trying to understand this space completely

Disc: Invested before concall tracking position. Waiting to buy more but it is falling like a knife.

7 Likes

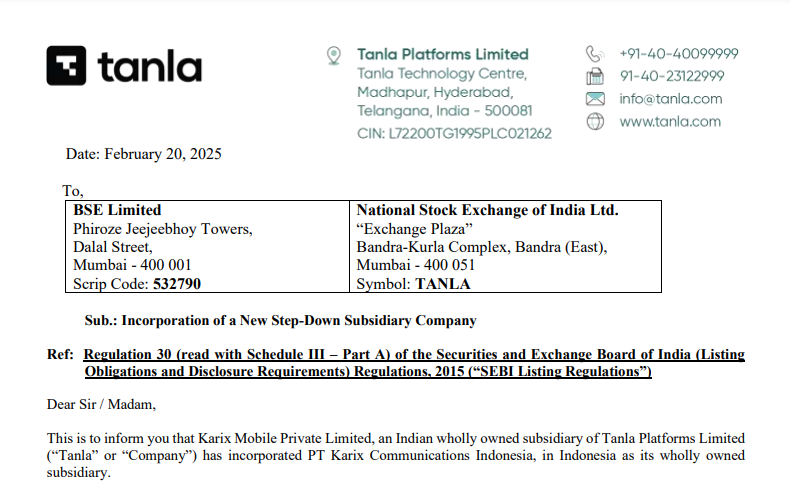

Tanla Platforms Update:

→ Karix Mobile (Tanla’s Indian subsidiary) incorporates PT Karix Communications Indonesia as a wholly owned subsidiary.

→ The new entity will operate in CPaaS (Communication Platform as a Service), enabling seamless business-consumer connectivity.

1 Like

As it is already discussed, Airtel has come up with Anti Spam alert and they are working good on this, it is kind of red flag for Tanla.

Secondly, I feel, companies like Tanla and route are dependent on telecom providers, so that is kind of reduce the profit margin and somewhere Airtel is playing on that.

Concept wise and technical solution wise it is best, but seems like competition is extremely tough as telecom providers seems to be thinking, why cant we make the money since our backbone of messages is getting used to make money.

In recent concall, mgmt accepted that pricing power is not much in their hands.

I am wait n watch mode, although I have invested small amount. Currently valuation wise it has gone down a lot, so feeling like it will go up here

3 Likes

Even Route Mobile has stagnated revenues from the past 5 quarters. Also according to this concall ,industry players are competing leading to reduced profit growth.

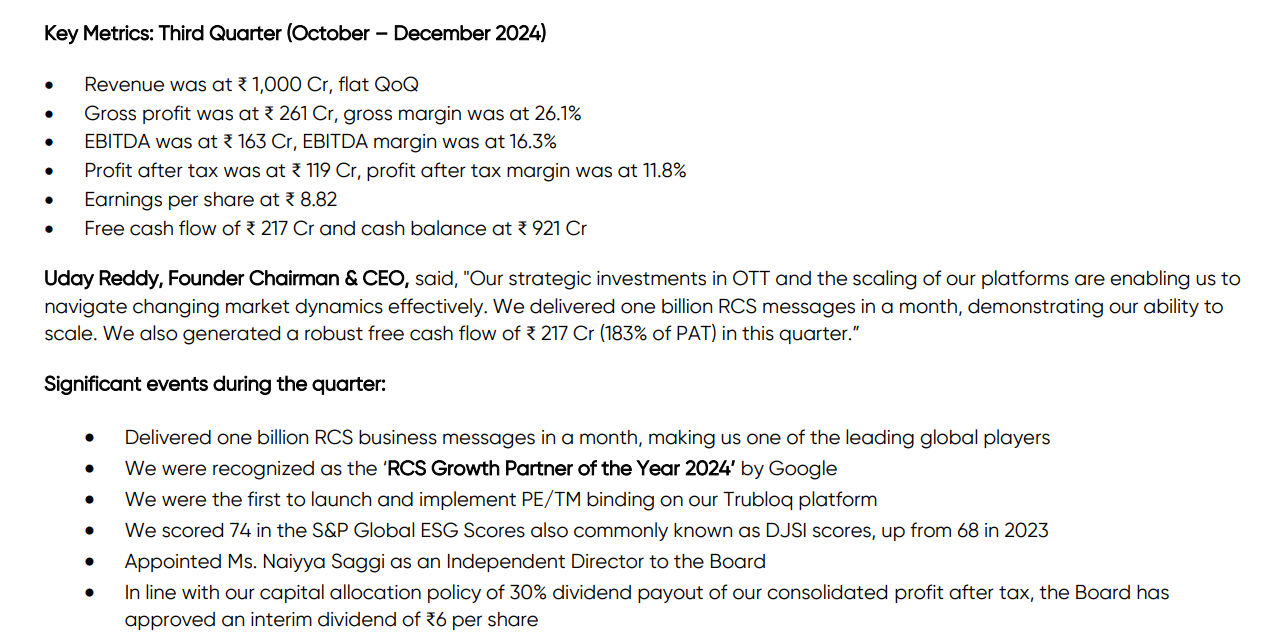

Yet another flat quarter, reflecting a cash cow business that generates steady cash flow but lacks growth.

5 Likes

Revenues stay flat, but management seems confident that the MaaP-platform will yield good results in the future. OTT balances sales mix and has growth potential, while margins remain at good levels around 25%, not to mention the exceptionla FCF generation. I’m considering adding this more, currently have position of ~ 2% in my portfolio.

Sources:

5 Likes

Businesses have switched their OTP/ Advts medium from SMSes to RCS and Whatsapp especially the international segment (which had good margins). Further, Telcos like Airtel, Jio and others have their own Spam tools now. The shift has hit Tanla suddenly and left it without the next revenue spinning product/ platform, thus, creating revenue stagnation.

With all the AI tools available in the market along with WhatsApp, Telegram, Discord & Google RCS’s own easy integration tools for business, Tanla may only grow in a incremental manner in future, unless they can figure out the next level growth product.

6 Likes

Thanks to everyone for their valuable inputs in this thread. I studied the company and had the below doubts. It would be great if somebody could address them.

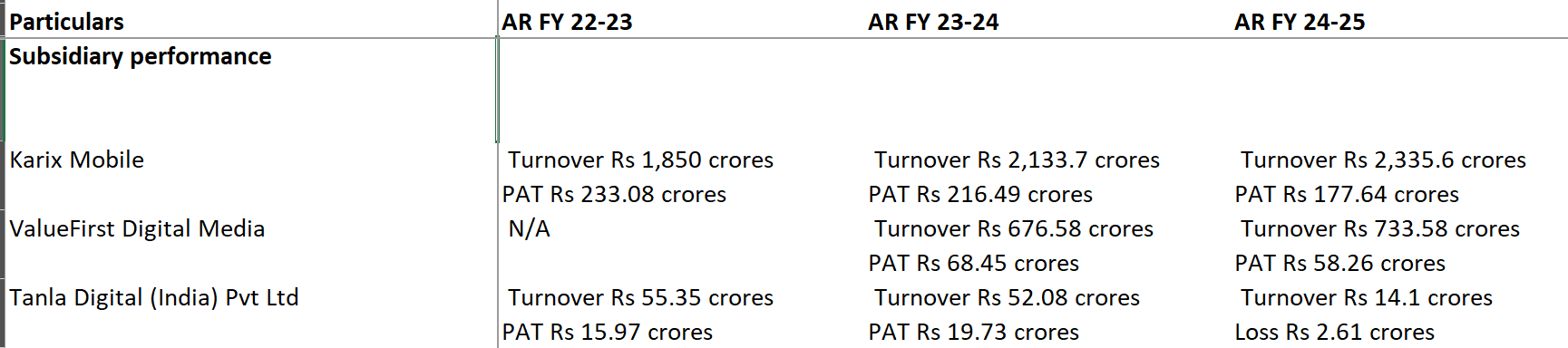

The revenue of the company from outside India witnessed a big jump in FY 24-25. I was not able to get the reason for the same. Was it some accounting change wherein the revenue has been billed from some other subsidiary? Because I don’t see much movement in ValueFirst’s revenue as well.

Also, there is no commentary in the AR or in the con calls which can explain that why are the margins in the subsidiaries deteriorating despite increase in turnover.

1 Like

Apologies if I’m violating any forum guidelines here by reposting one post in another forum but I’m invested in a software product company that seems to be on the verge of entering into something related to CPaaS

I wanted to understand if this poses any threat to the incumbents like Tanla/if it’s an adjacency

Any directions/guidance would be greatly appreciated since I’m new to the CPaaS industry

3 Likes

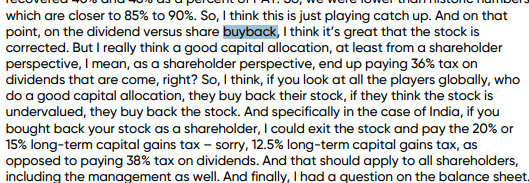

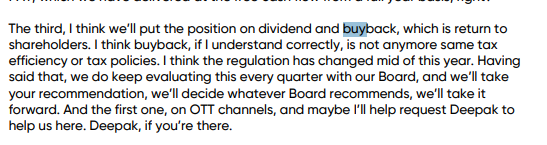

On the share buyback just want to point on one conversation which i observed two Quarters back. Sharad Kohli asked on this, saying instead of spending the cashflows by providing dividends better to go for a share buyback as it unlocks value to investors.

Response from management:

3 Likes

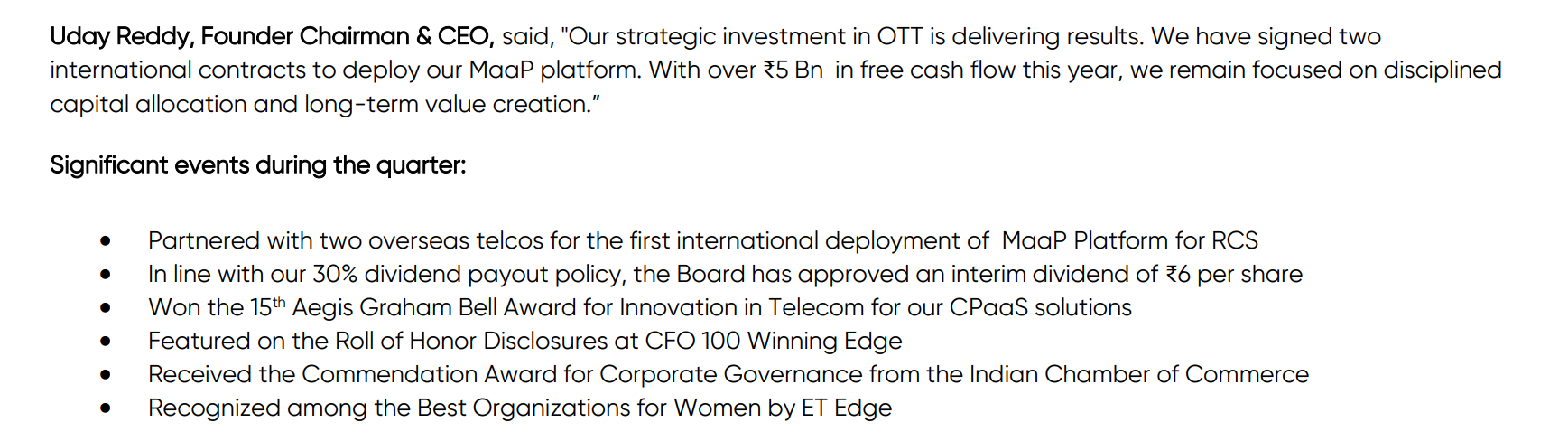

Management at the AGM today issued a guidance of 20% EBITDA growth YoY for the next 2 years. Management earlier had always shied away from giving any guidance but has done so today.

35:29 onwards

4 Likes

CPaaS and Tanla are clearly out of markets favour,

It is crawling its way back to topline growth, despite all kinds of headwind. In WhatsApp they have become No 2 and challenging for No1, against a struggling Gupshup, which had an extraordinary head start in the area.

For first Time they sort of quantified their growth aspirations , but rolled it back partially in q2, owing to govt ban on real money gaming and partially due to WhatsApp incentives and may be other things.

Yet, the cash flows even at lower EBITDA levels are still solid. A cash chest of nearly 1000 crores ….

Issue is if organic growth is difficult, then why not use that cash to grow inorganically? Particularly when the valuations are at rock bottom level? What good is paying out dividend in new age economy.. when the company should be chasing profitable growth?

I believe Tanla requires a course correction and fast on its growth strategy. Acquisition either in complimentary areas in India or for driving international expansion. Slow and steady won’t cut it. It doesn’t have a consumer brand like Nestle or HLL to play that game.

6 Likes

Read Bhavin Salva’s Q&A from the last two quarterly transcripts — absolute cinema.

It systematically exposes management’s buyback narrative for what it is: window dressing, not value creation.

EPS optics over shareholder economics. ![]()

1 Like

Hi, can you please share Bhavin Savla’s questions or comments? I can’t find it anywhere