Competition from Airtel

@anna What do you think about Tanla? It seems that the stock’s performance solely depends on Wisely ATP. ATP, though authentic and a deep value product, faces regulatory issues. Your analysis has been pretty good on Tanla. What do you think the future holds? And is it cheap at 20PE?

Tanla has suffered from a series of issues and when it overcomes one, the next one is there.

- 2 years back there was intense competition leading to revenue fall and margin loss in NLD business.

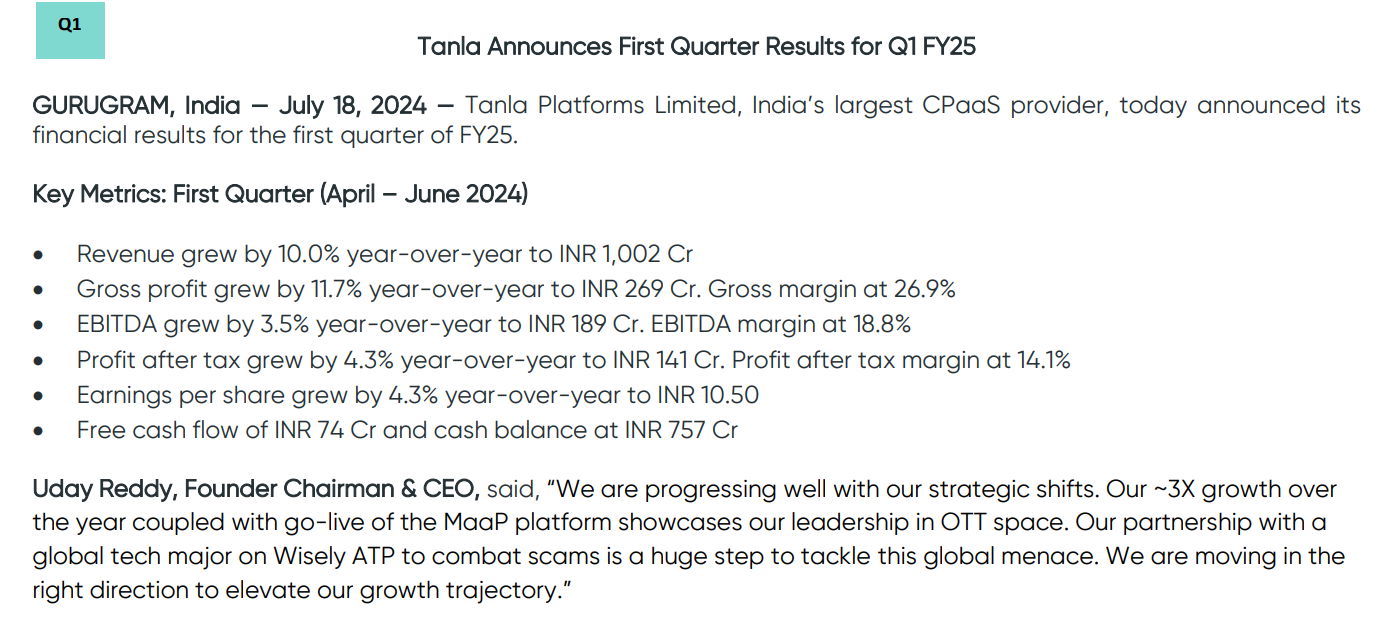

- While the above has stabilized now, ILD business has tanked over last few quarters. At one time Tanla had 75% of revenue in this market. Now it has 25% possibly. Hopefully in Q1FY25, it will stabilize.

- New platform launches have not performed in general. Wisely ATP is same boat.

- Vodafone-Idea deal which was delivering ~70crores GM, is gone and last 5-6Cr/qtr will come in Q1 and then the platform business losses will be over

- Industry went through consolidation. Each of the acquired players such as valuefirst or Kaleyra would have been giving business to Tanla. Even TeleSign would have been giving. These business would have already gone away, or if any of Telesign is left, will go away in Q1.

- So, it seems in a way all the bad things that could happen, will be over and done by in Q1FY25. Last 2 years havent been great and the entire benefit of buying Valuefirst business somehow got lost in all these.

- Now for good part (nothing great) -

a) the industry has gone thru consolidation. No one will presently want to do price wars. All acquirers will be wanting to bring up EBITDA. Competition intensity will be lower.

b) The NLD business (incl OTT) is still growing in range of ~15%. Once all disruptions are through, this growth will start showing. Tanla with laser focus on domestion enterprise business might overperform and add marginal marketshare.At stable gross margin of around 20%, it can hopefully, be predictable once again. The international business of Valuefirst is yet to be consolidated and it will give some drag as its EBITDA -ve or breakeven business.

c) Tanla seems to be doing well in OTT - this is re-assuring.

d) The platform business after Vi impact in Q1 can start showing 20-25% growth from Q2 without much help from Wisely ATP. If Wisely ATP deals happen it can do a crazy jig over next few quarters (but better not to count anything from it at this point - even the management is clueless on when business will happen - whether domestic or international)

Basically the business results would return to normalcy with steady growth. Few quarters of steady growth should be re-assuring for investors. If it can do some good acquisition to broadbase its business - it will be good. They generate good cash and investment requirement is not much. Unfortunately with Tanla’s standalone balance sheet they can’t do much of buy-back, unless they merge in karix and valuefirst. They need to figure out some good acquisitions either in CPaaS itself or in somewhat related space.

In short better days ahead, but great days can’t be there, unless platform start performing.

16 Likes

@anna thanks for the detailed analysis. How much PE should be attributed to such a company? Do you think it’s selling at fair price? I think it’s a tad expensive. 10,000cr could be fair price. What’s your opinion on this?

1 Like

Sorry Aishwary, somehow I am not very good at judging it. PE is often based on what market takes a fancy to, or on the reverse doesn’t understand well. At times it gets influenced by who is buying. In short, it is dynamic and beyond my capability to predict. There are reports from HDFC Securities and others, maybe you can refer to that - those guys are professionals and you will perhaps get a sense.

1 Like

No worries @anna. Thanks

8 Likes

Good analysis and view points. I do not hold this stock and haven’t researched much but just curious to hear from any long term investors in this stock on what they think and believe regarding this article and Tanla’s accounting practices?

I hold it and regard the above multiple flags article as useless.

Author comes across as a novice who doesn’t know the nuances of finance, who doesn’t know the legitimate accounting treatment to various line items in financial statements and who is quite ignorant about tech infra scope, scale and costs.

Could you please elaborate on what exactly was wrong with the analysis? since many of us are still novices here and could learn a thing or two from your expertise in this subject matter.

1 Like

Well, like someone said, why don’t you go ahead an elaborate the correct accounting treatment, and justify the immediate write offs of “computers” bought a year ago, acquisitions and simultaneous write offs of foreign subs, 0.5x NFAT for a tech firm, conversion of CWIP into intangibles when a seoarate line item exists for the purpose.

It could be that the author was incorrect or too cynical on some points, but multiple issues at once is surprising.

4 Likes

For those who follow Tanla will appreciate this ![]() is a big deal. This is the second deal for Wisely ATP deployment after the first one with a top private bank earlier this year.

is a big deal. This is the second deal for Wisely ATP deployment after the first one with a top private bank earlier this year.

WhatsApp inks deal with Tanla to detect and curb scams - The Economic Times (indiatimes.com)

7 Likes

Yesterday’s announcement for Wisely seems to be for whatsapp as reported by some newspapers.

Whatsapp has a nearly 50 crore user base in India.

If it covers the entire user base and is based on per user kind of pricing, even at 10 paise per month per user this deal can add 50 crore to EBITDA, assuming their costs are largely being met by the earlier deal. However, this is just one way of estimating and could be wrong by a huge margin either way. Important for company to spell out unit economics and revenue from such deals.

While this would definitely help regain some lustre for Tanla, particularly over the perception front, many such platform deals will be required to actually spell good days for Tanla from a numbers perspective and for the investing community to get its faith back on the “Platform” story.

Hope the day comes sooner, than later.

7 Likes

In the letter to Shareholder, CEO says that the agreement with the Global Tech Giant (which is Whatsapp as per ET article above), has global mandate - that is very interesting !!

4 Likes

Wouldnt there be some cost to tanla also for providing this?

Patent granted to Tanla by US Patent Office regarding security of SMS communication

3 Likes

Yesterday, Tanla declared that it has onboarded Axis Bank for its Wisely ATP platform.

This is great news but surprising the stock price did not move as expected.

I am reducing position size here and raising some cash. I will see how growth pans out over the next few months to decide to add back or reduce further or exit.

3 Likes

Really dull price movement…will be exiting completely for now…will watch the result to see if the platform biz starts to show jump in revenue & profitability…

1 Like

Tanla seems to be getting in the sweet spot , telecom regulatory environmemt wise.

TRAI seems to be meaning business this time.

Tanla’s real success in platform has been regulatory wise. Not Wisely.

No reco.

2 Likes