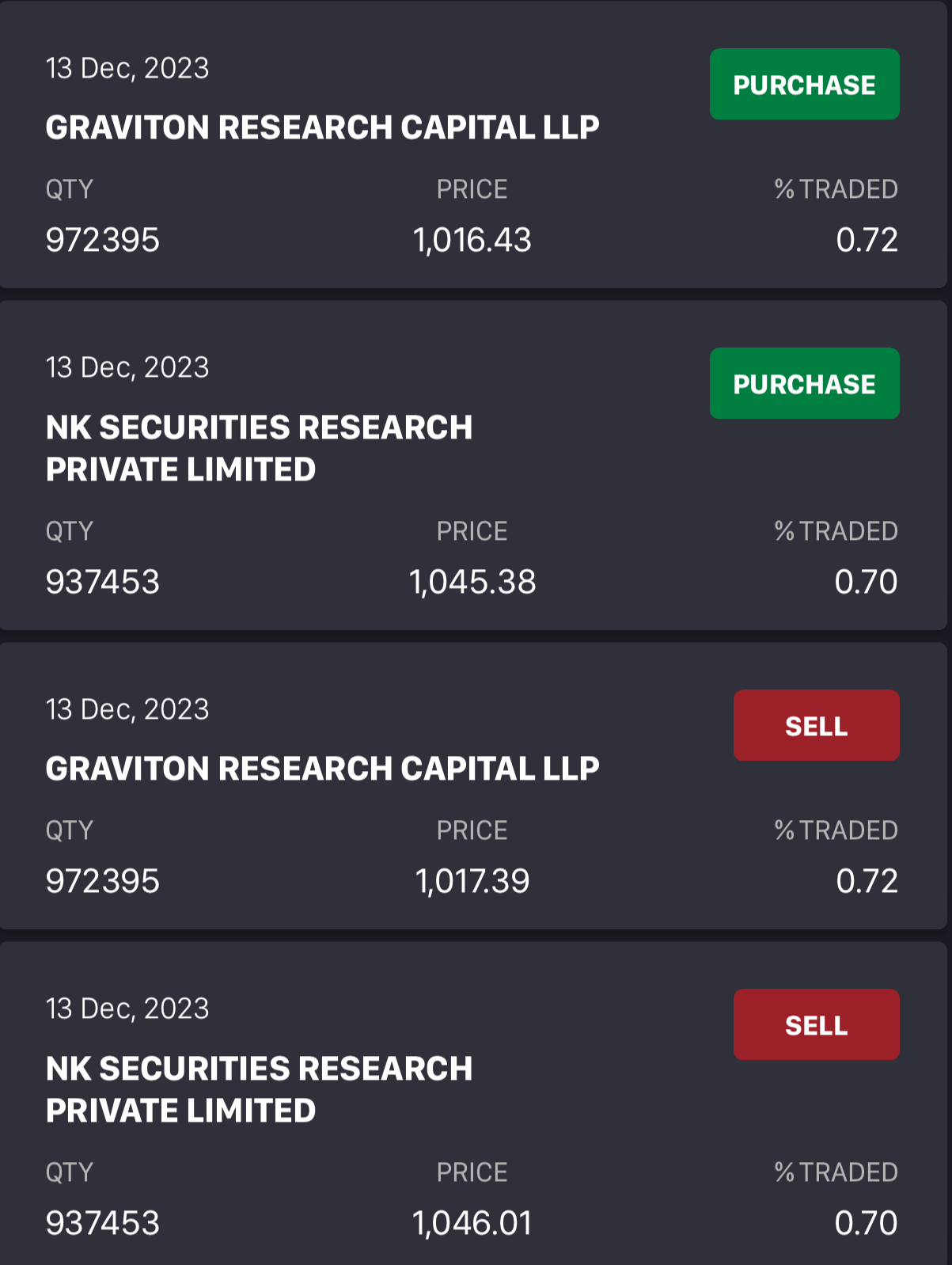

Huge volumes traded today. More than 10% of total shares. Any idea who’s buying?

2 Likes

I see its insider trade with very less delivery percentage; It’s a bad sign that these large LLP funds placing a trade without holding delivery to befool retail investors again.

Both are high frequency trading firms.

1 Like

Flattish QoQ results.

www.bseindia.com/xml-data/corpfiling/AttachLive/74bcb9ab-d48e-4180-bd3f-5dc2196931ed.pdf

Strangely company is sending sms of quarter results to shareholders! Too much focus on promotion

They always do that. Considering the company is into CPaaS business, this is not way over the line. And they do this irrespective of whether the results are good or bad

4 Likes

Sms of results is fine considering the field they’re in but the self promotion on social media im not a fan off.

I agree…this is normal, all shareholders get the message since a long time now…

i see, might have missed the message last time around. Disc: Exited today

Yes. Even others like Indusind bank also do this

-

TANLA IS VALUED SAME AS ROUTE MOBILE BUT IT CONSIST OF PLATFORM BUSINESS TO WHICH HAVE A GROSS PROFIT MARGIN OF 98%. PLATFORM BUSINESS IS GROWING MUCH FASTER THEN ENTERPRISES BUSINESS. I THINK IF WE VALUE PLATFORM AND ENTERPRISES SAPARETLY, WHILE GIVING PE OF 25 FOR ENTERPRISES AND 40 PE OF PLATFORM BUSINESS GETTING AN UPSIDE FOR 56 % PLEASE SHARE YOUR VIEWS IF I AM MISSING SOMETHING PLEASE POINT THEM OUT.

-

DIS:INVESTED

1. List item

1 Like

Summarising analysis after Q3 results.

Positives

High market share (2-3 major players in India)

Zero debt

Increase in OPM from 10% to 20% in last 5 years

More than 500cr cash at Q3

Bought more than 400 cr intangible assets in Q3 (gives huge potential in future)

Median PE 29.8 current PE 24.6

Roce > 37%

Roe > 31%

Stock price came down 25% since Q3 results (consolidation phase) which gives us an opportunity to look at good entry point

Support on daily 200MA

Support on weekly 44MA

Negatives

High customer concentration

Low promoter holding (but promoters raised almost 10% stake in the last 3-4 years from 33 to 43)

Low organic growth (mostly coming from new acquisition valuefirst)

High negative cash from finance activities (mostly due to buyback and dividend, buyback is a good indication)

PB approx 6 (not cheap)

PE 24 (not ideal)

Evebidta above 10 again not ideal

Investment View long term 2-4 years where the acquisitions and latest capex benefits might start unfolding, value creation to the company.

What am I missing?

NOT A RECOMMENDATION

Disc. (Not invested)

Share your views

1 Like

Will that affect TANLA negatively? What if the platform the video is talking about will have tanla wisely as interface

Q3-FY2023-24 Notes

ILD (International Long Distance) Business Overview:

- ILD Revenue Contribution: 25%

- Recent Softness in ILD Business

NLD (National Long Distance) Business Overview:

- NLD Revenue Contribution: 50%

- Expected Organic Growth:

- Mid-single digits in Q3

- Momentum in domestic business

ILD Business Challenges and Outlook:

- ILD Pricing Pressure:

- Approximately 40x-50x compared to domestic pricing

- Shift to OTT Channels Impact:

- Shift in use cases to OTT channels, affecting ILD volumes

- Bottom Reached:

- Confidence in no further decline

- Shifts have stabilized post-October

- Future Growth Expectations:

- Sluggish growth anticipated

- WhatsApp price increase and ILD message support changes may impact positively

ILD Customer Landscape:

- Major Customers:

- Amazon, Snapchat, Microsoft

- Large customers send messages only when necessary

Enterprise Business Growth:

- Steady State Growth:

- Industry growth focused on domestic market

- New use cases contributing to double-digit growth

- Increasing adoption of alternate channels (OTT, WhatsApp, RCS, Truecaller)

Gross Margin Impact:

- ILD Contribution to Gross Margin:

- Absolute revenue higher but margin percentage lower than domestic

- Offshore construct: Higher realizations, higher costs

- Overall Impact:

- No significant dilution in gross margin expected

ILD Revenue and Shift to Other Channels:

- ILD Challenges: Shift to alternative channels due to cost-cutting.

- Promotional Messages: Negligible on ILD; focus on OTPs and informative messages.

- Future Shifts: Meta planning to increase prices; potential return of volumes.

NLD Promotional Messages and RCS Impact:

- RCS Effectiveness: RCS allows rich media, offering better ROI for promotional messages.

- RCS Adoption: Karix and ValueFirst hold over 40% share in the Indian RCS market.

- NLD Promotional Shift: Possibility of promotional messages shifting to RCS for increased impact.

Platform Business and Vi Deal Impact:

- Platform Business Growth: 22% YoY growth, impacted by reduction in international messaging market.

- Vi Contract Exit Impact: Expected to see further impact in Q4; focus on growth in other platforms.

ATP Platform and Commercial Contracts:

- ATP Contracts: Subscription-based model with per-user monthly payments.

- Commercial Contracts: Signed first customer contract, expecting revenues to start in the current quarter.

- Pipeline Growth: Aggressive pursuit of new customers, full impact expected in Q1.

- ATP User Base: Large-scale adoption by one of India’s largest private banks.

- Scalability: Scalable within the bank based on the user base.

ATP Adoption Challenges:

- Regulatory Hurdles: Delays due to regulatory approvals and navigating discussions.

- Regulator Urgency: Frustration with the lack of urgency from regulators.

- Organizational Adoption: Challenges in organizations obtaining regulatory approvals for deployment.

Vi Impact and ATP Platform Comparison:

- Vi Impact Mitigation: Not comparing new ATP deals to Vi loss; confident in overcoming Vi impact.

- Vi Traffic Decline: 30-40% traffic loss in Q3; impact expected to continue until end of March.

- ATP Platform Confidence: ATP deals and other platforms expected to offset Vi impact.

WhatsApp Revenue Target and Current Status:

- ₹100 Crores Quarterly Run Rate: Achieved in Q3.

- Exponential Growth on OTT: Focus on OTT contributing to significant revenue increase.

Unlocking Platform Business Value:

- Platform Business Potential: Run rate of ₹400-500 crores per annum.

- Capex Investment: Considerable investments in platforms.

VF Middle East Indonesia Merger:

- Expected Closure: Regulatory approvals causing delays; confident to close the merger in the current quarter.

Opportunities Beyond India:

- Overseas Potential: Recognizing opportunities to collaborate with telecom companies abroad.

- Regulatory Monitoring: Observing regulatory frameworks in neighboring countries like Saudi, Singapore, and Australia.

- Contributions to Regulations: Actively contributing to shaping regulations in various countries.

- International Deployment: Intent to deploy Wisely ATP platform outside India, contingent on regulatory approval.

Top Tier Talent Acquisition:

- Strategic Talent Addition: Emphasis on recruiting top-tier talent.

- R&D Focus: Allocation of funds (₹40-45 crores) for R&D, resulting in ongoing product development.

- Quarterly Average: Average spending of ₹12-14 crores per quarter on R&D.

- Upcoming Products: New products and solutions in the pipeline.

Digital Platform Growth Expectations:

- Current Growth: Achieving around 20% growth in the digital platform segment.

- Investment in Platforms: Significant investments made in building and expanding platforms.

- Greenfield Approach: Focused on greenfield opportunities, not aiming to replicate existing platforms.

- Market Potential: Recognizing substantial opportunities in the digital platform space.

- Future Growth Projection: Expecting to sustain a minimum of 20% growth in the next three to four years.

8 Likes

Tanla and Truecaller further collaborate on sending rich media to Truecaller. Preparing for videos from HDFC bank now ![]()

2 Likes

Tanla Platform-3-1.pdf (112.8 KB)

Hi everyone. I have conducted analysis on Tanla Platform. Do provide feedback on the analysis conducted

12 Likes

Tanla Platforms:

A lot of interesting developments have occurred in Tanla over the last few months. The company is now at the cusp of earnings acceleation which shall last a good few years.

The main driver of earnings growth will be the platform biz which operates at GM level of >90%. This biz is currently 10% of the overall revenue and is growing at ~30-35% YoY. The overall earnings are expected to grow at a minimum of 20-25% YoY for the foreseeable future.

However, there is a high chance that the earnings growth accelerates further and company grows faster than a conservative estimate of 25%. But for that we shall monitor the traction of the platform business in the coming few quarters.

Stock trades at a reasonable valuation of 23x PE.

High growth rate will lead to PE expansion.

So, the stock offers two-pronged opportunity emanating from earnings growth + PE re-rating.

Some key triggers for earnings acceleration are:

- Wisely Platform deployment with its AI capabilities

- ATP + Trubloq

- ONDC solution for SME through Whatsapp

- MaaP launch with Google RBM + Vodafone

- OTT channels explosive growth

Of these ONDC & Google RBM could be really really big and could potentially grow like J-curve.

8 Likes

To understand where the digital world is headed see the below video from Timestamp: 2:07:00 to 2:10:30 of Google RBM Head - Stephen Brough talk about the following:

-

Transition from Phone (1800) to Internet to App and going forward to Chat

-

Every Android phone will have Google RBM going forward

-

Apple will also support RCS

Note: Tanla is a strategic partner of Google and has the highest volume of Google RBM traffic globally and targeting about ~50% market share in India in FY25.

Live Stream // Tanla #MWC24 // Elevating Digital Experiences (youtube.com)

Note: The way businesses interact with customers for security(OTP), marketing or information dissemination services is undergoing a radical shift. Recently, banks, airlines, online travel cos., etc., have started delivering messages on Whatsapp rather than just SMS. This is referred to as OTT. This new trend is seeing explosive growth. Tanla is the market leader in this and its market share is greater than the combined share of 2nd, 3rd & 4th players put together.

21 Likes