Tamboli Capital: owns 100% in Tamboli Castings:

Disc: Invested since 2 qtrs at about INR 80 levels.

History:

On 25thFeb 09 Investment & Precision Castings Ltd informed BSE that the Board of Directors of the Company have determined March 20, 2009 as the Record Date. The swap ratio fixed by the Board is as below:

2 New Equity Shares of Tamboli Capital Ltd for every 1 share of Investment and Precision

This is the link of the announcement made on BSE:

http://www.bseindia.com/qresann/news.asp?newsid={8FB1F5B1-9F82-4049-9950-47EEC08A18EA}

Business: The Global Investment Casting market size in 2021 was $14.09 BN USD.

What is Investment Castings:

Investment casting process produces precise components

with close tolerances

-Large volume batches can be manufactured using this process making it economically viable

-Ensures production of very intricate parts and required metallurgical properties

Hence it is process of preference for design engineers worldwide

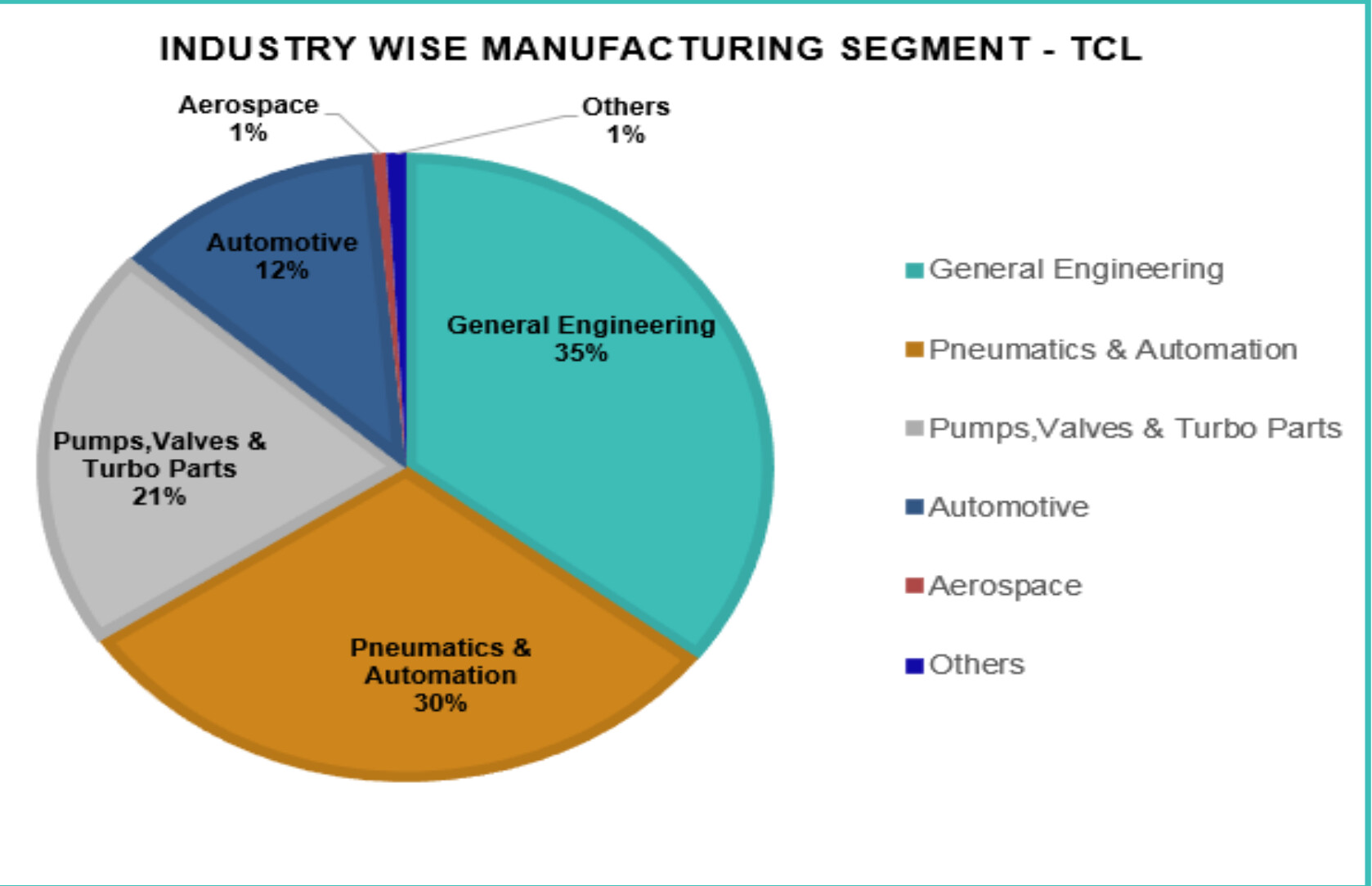

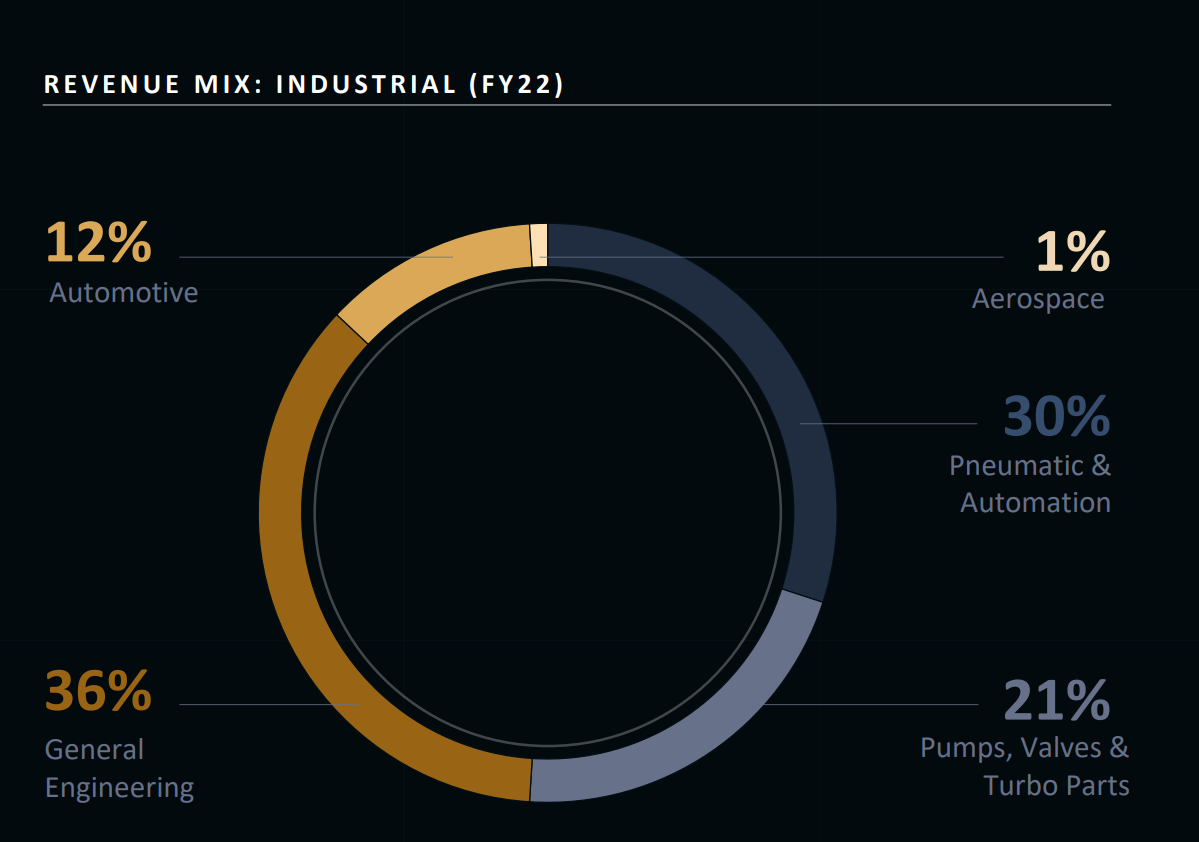

Usage ::

Increasing applications in Industrial Machinery

-Growing demand from Aerospace and Defense Industries

-high volume Automotive segment

- AeroSpace and Defence

- Food & Medical Industry

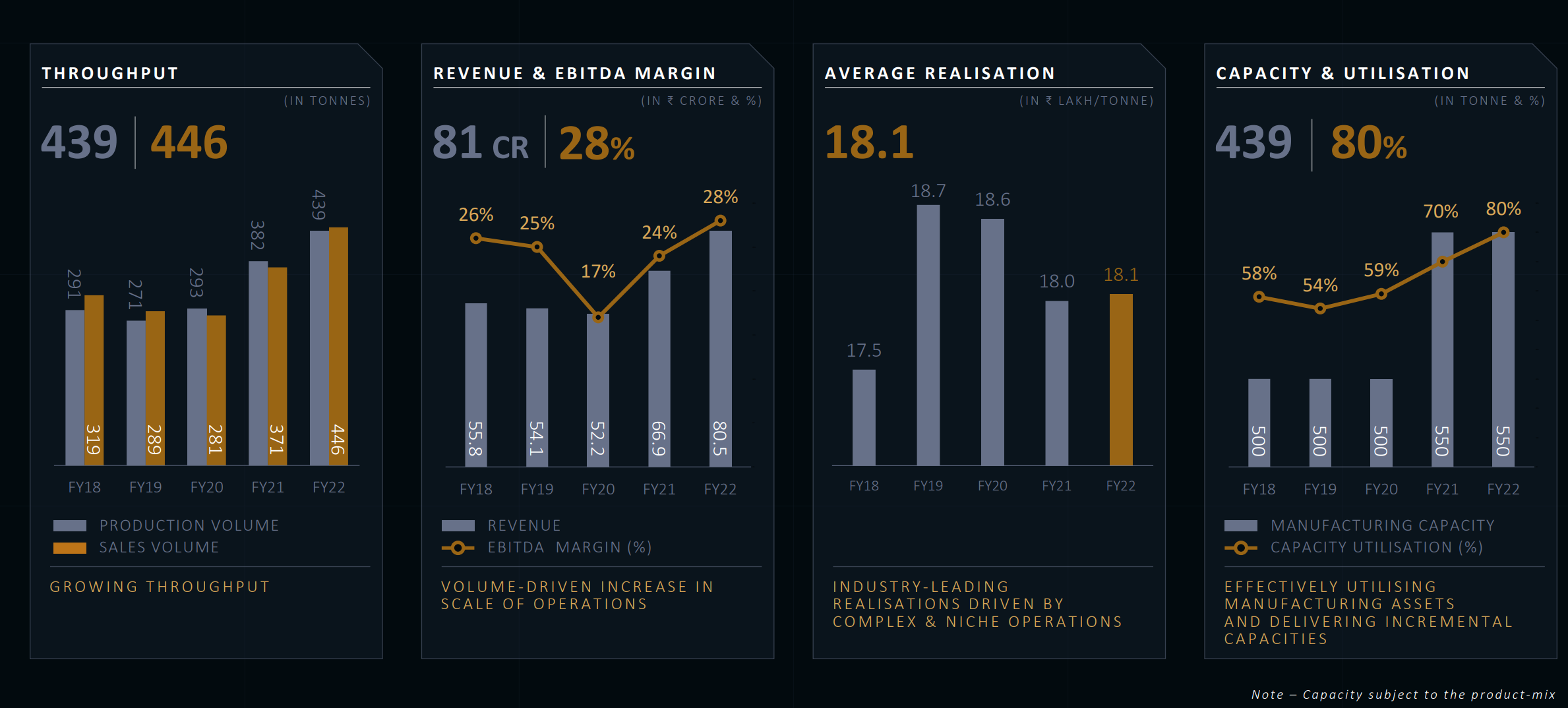

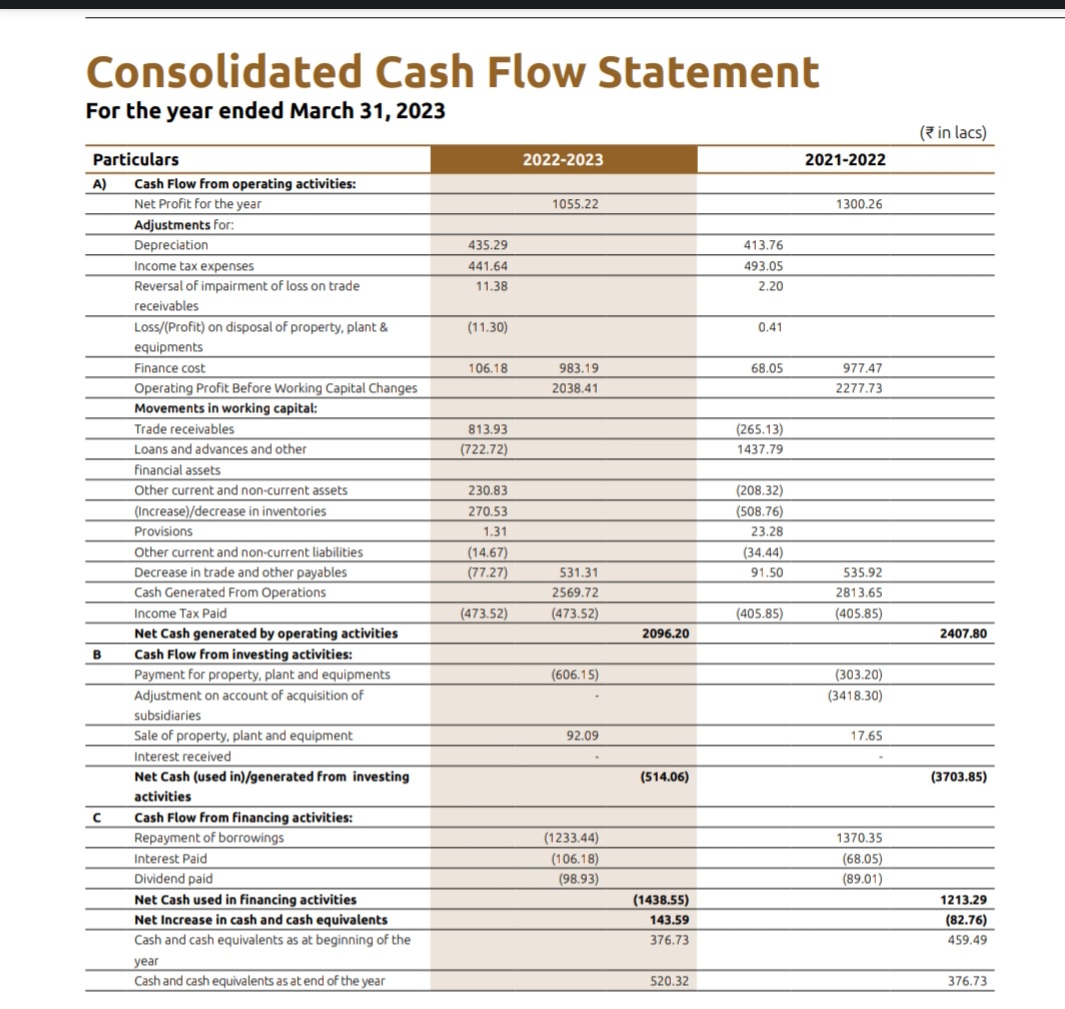

Last 5 yrs numbers:

| Mar-17 | Mar-18 | Mar-19 | Mar-20 | Mar-21 | Mar-22 | |

|---|---|---|---|---|---|---|

| Sales | 55.20 | 55.83 | 54.13 | 52.16 | 66.90 | 80 |

| Expenses | 40.39 | 40.96 | 40.98 | 44.81 | 51.34 | 59 |

| Operating Profit | 14.81 | 14.87 | 13.15 | 7.35 | 15.56 | 21.00 |

| OPM | 27% | 27% | 24% | 14% | 23% | 26% |

| Other Income | 0.05 | -0.01 | 0.46 | 1.43 | 0.64 | 1 |

| Depreciation | 3.35 | 3.43 | 3.34 | 2.97 | 3.30 | 4 |

| Interest | 0.90 | 0.88 | 0.60 | 0.39 | 0.20 | 1 |

| Profit before tax | 10.61 | 10.55 | 9.67 | 5.42 | 12.70 | 18.00 |

| Tax | 3.57 | 3.56 | 2.71 | 1.37 | 3.32 | 5 |

| Net profit | 7.04 | 7.00 | 6.96 | 4.05 | 9.38 | 13 |

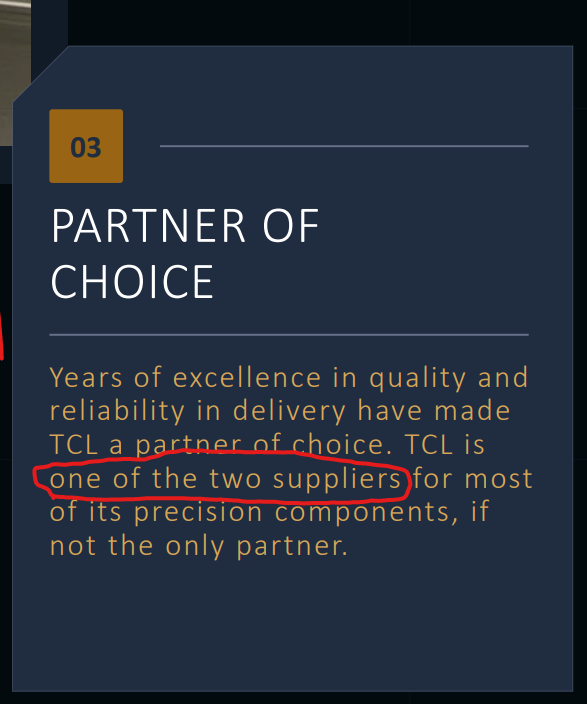

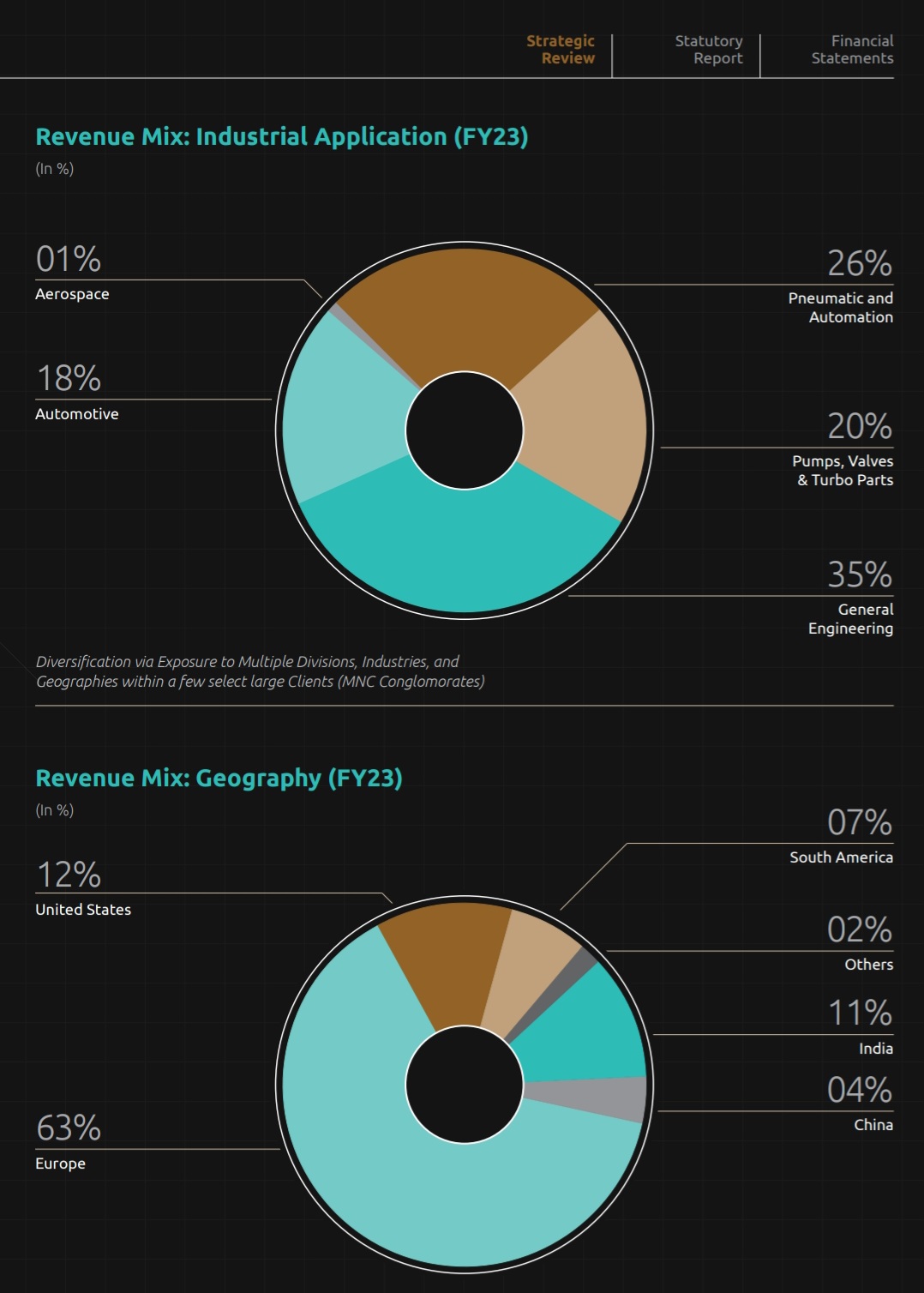

Key clients: Fetso as per credit report. Also some desktop work suggest they do supply to Bosch as a Tier 2.

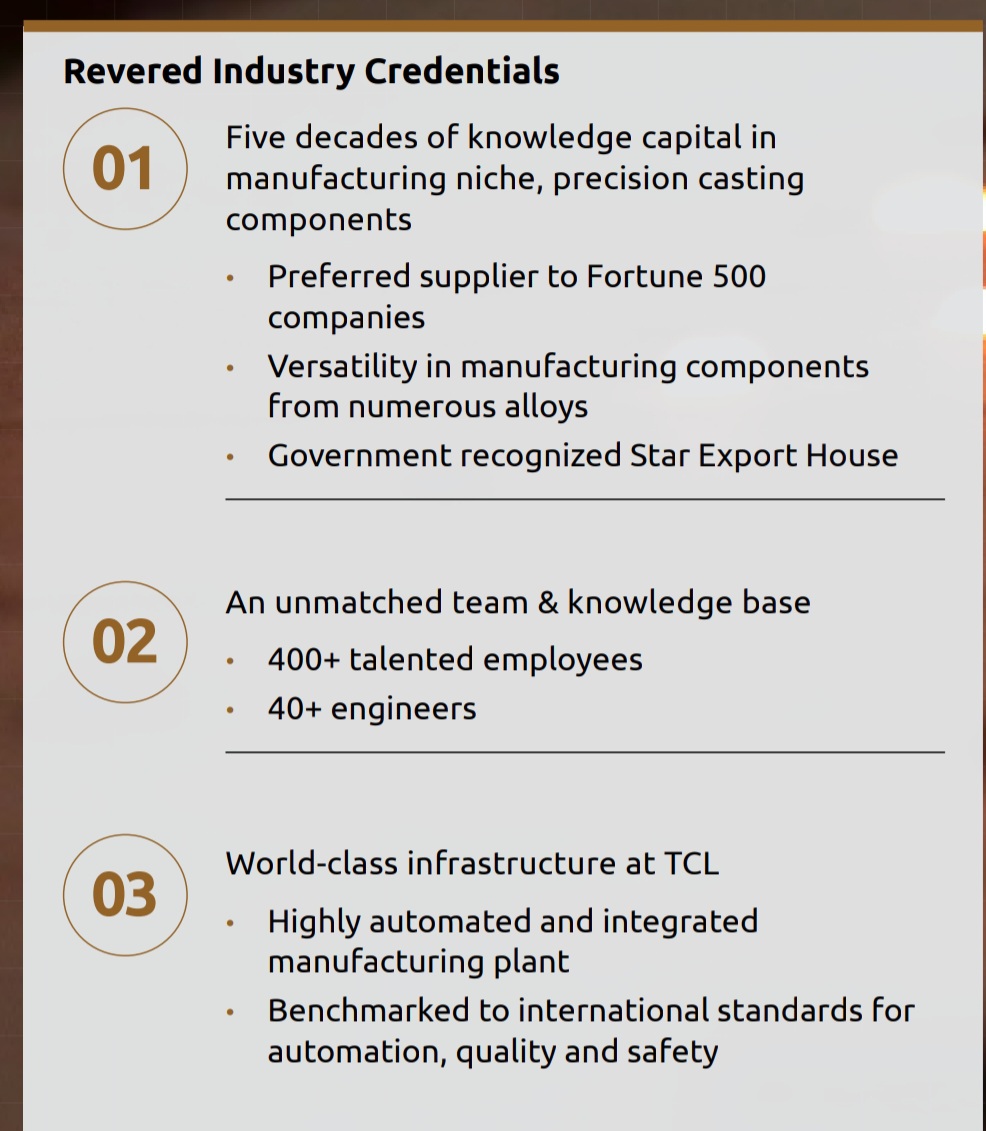

Key Hypothesis:

- More than 10 years of experience in castings business

- 100% EOU

- Festo the biggest client with 5 years of relationship

- Good margins > 20% + avg ( covid year 14%… Fy22 peak 27%)

- INR 23 cr odd GFA reporting 80 cr sales ( 3x + asset turnover)

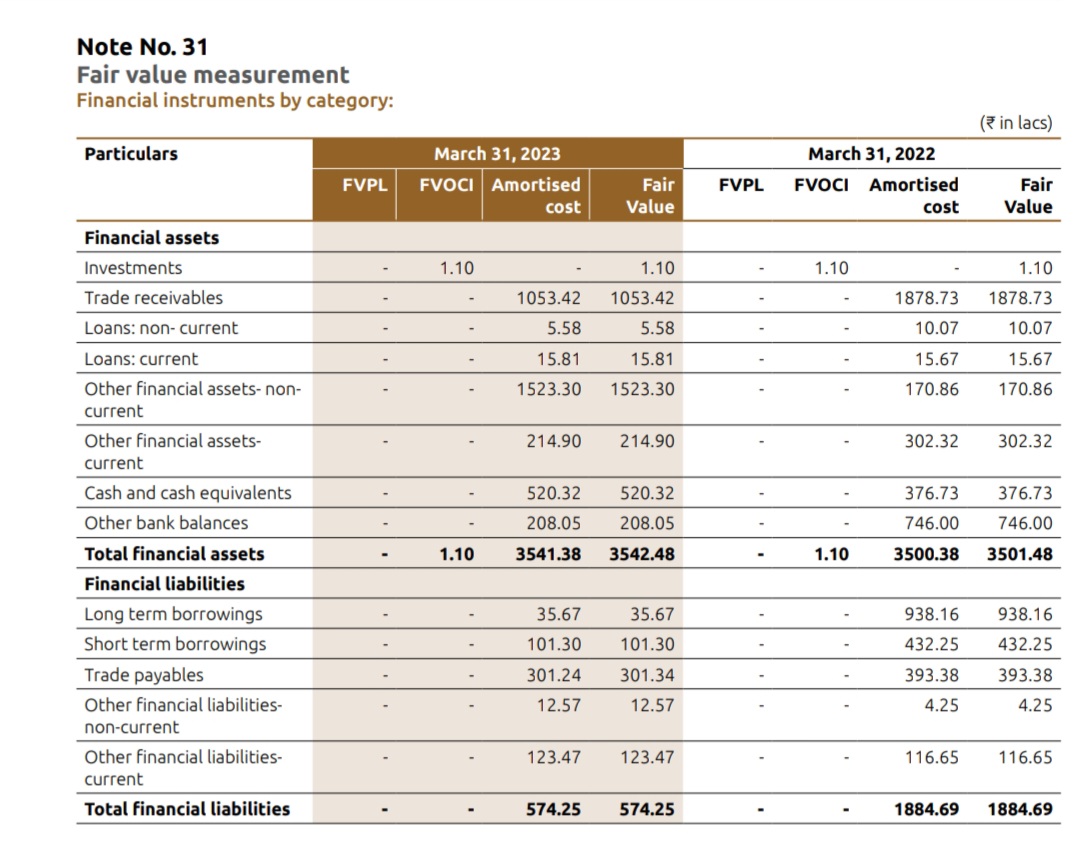

- INR 9 cr debt … INR 81 cr Net Worth… Adjusted CFO INR 14 cr… Trading at INR 85 cr Mcap

- INR 34 cr investments done…

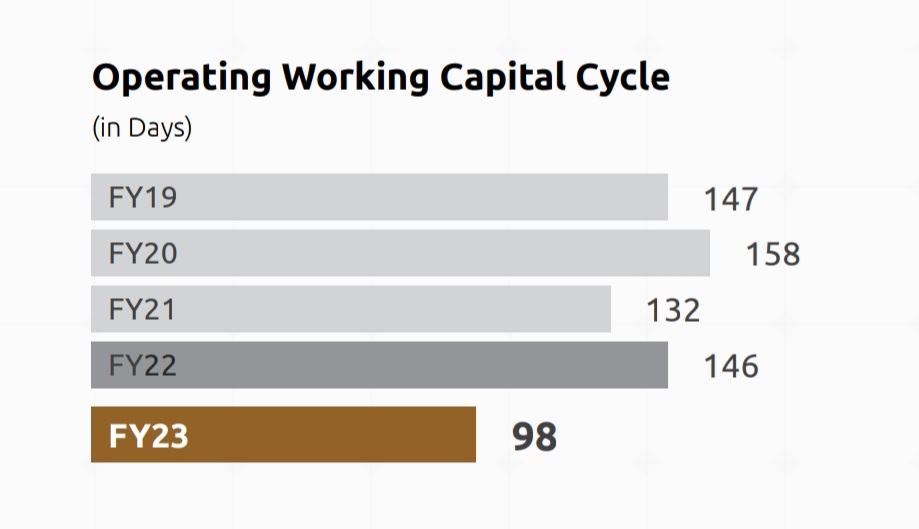

- 150 days + working capital cycle…

The company has 10 year + dividend paying track record.

Negative:

-The 2 bros have had some feud and court cases in the past.

-The company has been slow to ramp up top line.

-Does small business of silver trading etc less than 3 cr top line… negligible profit…

Growth:

Last year 35% vols growth. Tamboli is also investing in new capex. Need to understand more.

Looks inexpensive.

Dont kow:

Potential in other areas of Defense and management ambition and ability to scale up.

Key Links:

PPT : https://www.bseindia.com/xml-data/corpfiling/AttachHis/9cb4b16d-4725-4b4d-a468-6119f12bbfc1.pdf)

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/d5995a1d-a6a5-42e7-ab03-28899955dfe2.pdf

Do share your views.